Market Insights

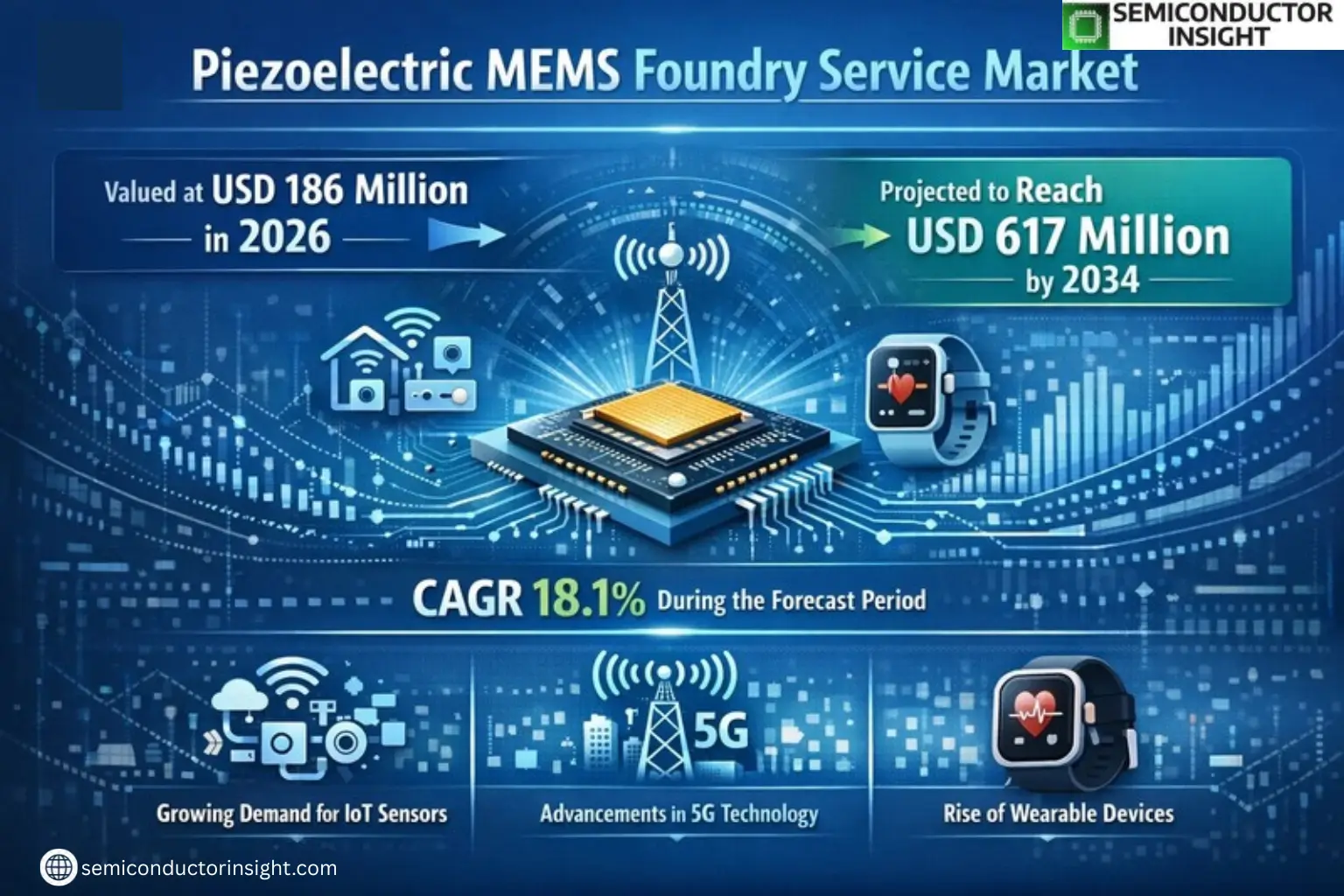

Global Piezoelectric MEMS Foundry Service Market was valued at USD 186 million in 2026 and is projected to reach USD 617 million by 2034, exhibiting a CAGR of 18.1% during the forecast period.

Piezoelectric MEMS (microelectromechanical systems) combine the precision of MEMS technology with the unique properties of piezoelectric materials, enabling applications in sensing, actuation, and energy harvesting. These devices are widely used in consumer electronics, automotive systems, medical devices, and industrial automation due to their high efficiency and compact size.

The market is experiencing rapid growth driven by increasing demand for IoT-enabled sensors, advancements in 5G communication technologies, and the rising adoption of wearable devices. Key players such as Bosch, STMicroelectronics, and ROHM dominate the market, collectively holding approximately 84% of the global share. North America leads regional demand with a 35% market share, followed by Europe (29%) and Asia-Pacific (28%). The industry’s gross profit margins typically range between 35%-55%, influenced by production complexity and customer requirements.

MARKET DRIVERS

Growing Demand for Miniaturized Sensors

Piezoelectric MEMS Foundry Service Market is experiencing significant growth due to the increasing demand for miniaturized sensors in consumer electronics, healthcare, and automotive applications. Companies are actively seeking Piezoelectric MEMS Foundry Services to develop high-performance, compact devices for ultrasonic, pressure, and inertial sensing.

Advancements in IoT and Wearable Technologies

The proliferation of IoT devices and wearables has created new opportunities for piezoelectric MEMS components, driving demand for specialized foundry services. Emerging applications in health monitoring, smart home systems, and industrial IoT require precision MEMS fabrication capabilities.

Increasing R&D investments in piezoelectric materials and MEMS fabrication techniques are further accelerating market expansion, with foundries developing advanced processes for higher yield and performance.

MARKET CHALLENGES

High Fabrication Complexity

The complex nature of piezoelectric MEMS fabrication presents significant technical challenges, including material integration issues and process control requirements. Foundries must maintain exceptionally tight tolerances during deposition, patterning, and etching of piezoelectric thin films.

Other Challenges

Yield Optimization Constraints

Achieving high production yields for piezoelectric MEMS devices remains challenging due to sensitive material properties and stringent performance requirements, increasing per-unit manufacturing costs.

Specialized Workforce Requirements

The market faces a shortage of skilled technicians and engineers with expertise in both piezoelectric materials and MEMS fabrication processes, limiting production scalability.

MARKET RESTRAINTS

High Capital Investment Requirements

Piezoelectric MEMS Foundry Service Market requires substantial upfront investments in specialized equipment and cleanroom facilities. Many potential entrants are deterred by the USD 50-100 million typically needed to establish a MEMS production facility meeting current industry standards.

MARKET OPPORTUNITIES

Emerging Biomedical Applications

New applications in medical diagnostics, drug delivery systems, and implantable devices are creating growth opportunities for Piezoelectric MEMS Foundry Services. The development of ultra-sensitive biosensors and microfluidic systems requires specialized fabrication capabilities that few foundries currently offer.

Piezoelectric MEMS Foundry Service Market Trends

Rapid Market Expansion Driven by IoT and 5G Demands

Global Piezoelectric MEMS Foundry Service Market, valued at USD 186 million in 2026, is projected to reach USD 617 million by 2034, growing at an 18.1% CAGR. This surge is primarily fueled by escalating demand from IoT, 5G communications, and wearable device applications. The technology’s ability to integrate sensing, actuation, and energy harvesting functions makes it indispensable for modern microsensors and actuators.

Other Trends

Material Processing Challenges and Advances

Stoichiometry and morphology control remain critical challenges in piezoelectric material production. Recent breakthroughs in chemical solution deposition, particularly with PZT films, have enabled better CMOS integration. The industry maintains gross margins of 35-55%, reflecting both the technological complexity and value of these solutions.

Regional Market Concentration and Competitive Landscape

North America leads the Piezoelectric MEMS Foundry Service Market with 35% share, followed by Europe (29%) and Asia-Pacific (28%). Bosch, STMicroelectronics, and ROHM dominate the sector, collectively holding 84% market share. The Asia-Pacific region shows particularly strong growth potential due to expanding electronics manufacturing ecosystems.

Application-Specific Growth Segments

Consumer electronics account for the largest application segment, driven by smartphone and wearable device adoption. Medical applications are emerging as the fastest-growing sector, with piezoelectric MEMS enabling new generations of compact, sensitive biosensors and implantable devices requiring minimal power.

Technological Integration and Miniaturization

Continuous miniaturization of piezoelectric MEMS components is enabling their integration into increasingly compact devices. The development of multi-axis combined sensors now allows for more sophisticated motion tracking and environmental sensing capabilities in constrained form factors.

COMPETITIVE LANDSCAPE

Key Industry Players

Dominance of Top Three Players in Piezoelectric MEMS Foundry Services

Global Piezoelectric MEMS Foundry Service Market is characterized by high concentration, with Bosch, STMicroelectronics, and ROHM collectively commanding approximately 84% market share. These leading players have established strong technological capabilities in piezoelectric material deposition and MEMS fabrication processes, particularly in PZT film integration. Their dominance stems from extensive R&D investments, proprietary manufacturing techniques, and long-standing relationships with major OEMs across consumer electronics, automotive, and medical sectors.

Beyond the top three, specialized foundries like Silex Microsystems and Innovative Micro Technology cater to niche applications requiring customized piezoelectric MEMS solutions. Emerging Asian players such as Asia Pacific Microsystems and MEMSCAP are gaining traction through cost-competitive offerings, particularly for mid-range sensor applications. The market also sees participation from semiconductor veterans like Texas Instruments and TDK Corporation, leveraging their existing MEMS platforms to offer piezoelectric integration services.

List of Key Piezoelectric MEMS Foundry Service Companies Profiled

- Bosch

- STMicroelectronics

- ROHM

- Silex Microsystems

- Innovative Micro Technology

- MEMSStar

- Asia Pacific Microsystems

- MEMSCAP

- Texas Instruments

- TDK Corporation

- Teledyne DALSA

- Murata Manufacturing

- OMRON Corporation

- PNI Sensor

- Vesper Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MEMS Sensor Foundry dominates due to:

|

| By Application |

|

Consumer Electronics leads due to:

|

| By End User |

|

OEMs represent the largest segment because:

|

| By Material |

|

PZT remains dominant due to:

|

| By Technology |

|

Thin Film Deposition leads because:

|

Regional Analysis: Global Piezoelectric MEMS Foundry Service Market

Asian foundries lead in developing novel piezoelectric thin-film deposition techniques, enabling higher sensitivity MEMS devices while maintaining production scalability. Advanced materials integration approaches give regional players competitive advantages.

Complete semiconductor supply chains across Japan and South Korea allow seamless transition from MEMS design to mass production. This vertical integration reduces time-to-market for piezoelectric sensor solutions.

Substantial R&D funding and tax incentives for MEMS development in China and Singapore encourage foundry expansion. National semiconductor initiatives prioritize piezoelectric technology for strategic applications.

Regional foundries are developing specialized piezoelectric MEMS solutions for wearable health monitors and smart infrastructure, capitalizing on Asia’s rapid IoT adoption and urbanization trends.

North America

North America maintains strong piezoelectric MEMS foundry capabilities, particularly in high-reliability applications for aerospace and medical sectors. The region benefits from close collaboration between research institutions and foundries, driving innovations in lead-free piezoelectric materials. Established MEMS design ecosystems in Silicon Valley and Boston support specialized foundry services, while defense contracts fuel development of ruggedized MEMS sensors. Challenges include higher production costs compared to Asian counterparts, pushing local foundries to focus on premium, high-margin applications.

Europe

European foundries excel in precision piezoelectric MEMS for automotive and industrial applications, leveraging decades of experience in high-performance sensors. Germany’s automotive industry drives demand for MEMS foundry services supporting advanced driver assistance systems. The region maintains leadership in environmentally sustainable MEMS manufacturing processes, with strong research networks facilitating technology transfer from labs to production. Cross-border collaborations within the EU enhance foundry capabilities, though market fragmentation remains a challenge for scaling operations.

Middle East & Africa

The MEA region shows emerging potential in piezoelectric MEMS foundry services, particularly in Israel’s thriving semiconductor sector. Growing investments in sensor technologies for oil/gas applications create new opportunities. Local foundries are developing expertise in harsh-environment MEMS solutions, though the market remains in early stages compared to global leaders. Strategic partnerships with international players help build regional capabilities while addressing infrastructure limitations.

South America

South America’s piezoelectric MEMS foundry sector remains nascent, with Brazil showing most activity through academic-industry collaborations. Focus areas include environmental monitoring sensors and medical applications. The region faces challenges in semiconductor manufacturing scale, with most complex MEMS production outsourced to global foundries. However, local prototyping services are growing to support regional electronics innovation.

Report Scope

This market research report provides a comprehensive analysis of the Piezoelectric MEMS Foundry Service Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Piezoelectric MEMS Foundry Service Market?

-> Piezoelectric MEMS Foundry Service Market was valued at USD 186 million in 2026 and is projected to reach USD 617 million by 2034, exhibiting a CAGR of 18.1% during the forecast period.

What is the expected growth rate (CAGR) of this market?

-> The market is expected to grow at a CAGR of 18.1% during the forecast period 2026–2034.

Which companies are the key players in this market?

-> Key players include Bosch, STMicroelectronics, ROHM (top three companies hold 84% market share), and Silex Microsystems.

Which region dominates the Piezoelectric MEMS Foundry Service Market?

-> North America is the largest market (35% share), followed by Europe (29%) and Asia Pacific (28%).

What are the main drivers of market growth?

-> Growth is driven by demand from IoT, 5G communications, wearable devices, medical sensors, and consumer electronics applications.

What are the major technology challenges in this market?

-> Key challenges include piezoelectric material integration with CMOS technology, crystallization process control, and maintaining 35%-55% gross profit margins.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...