MARKET INSIGHTS

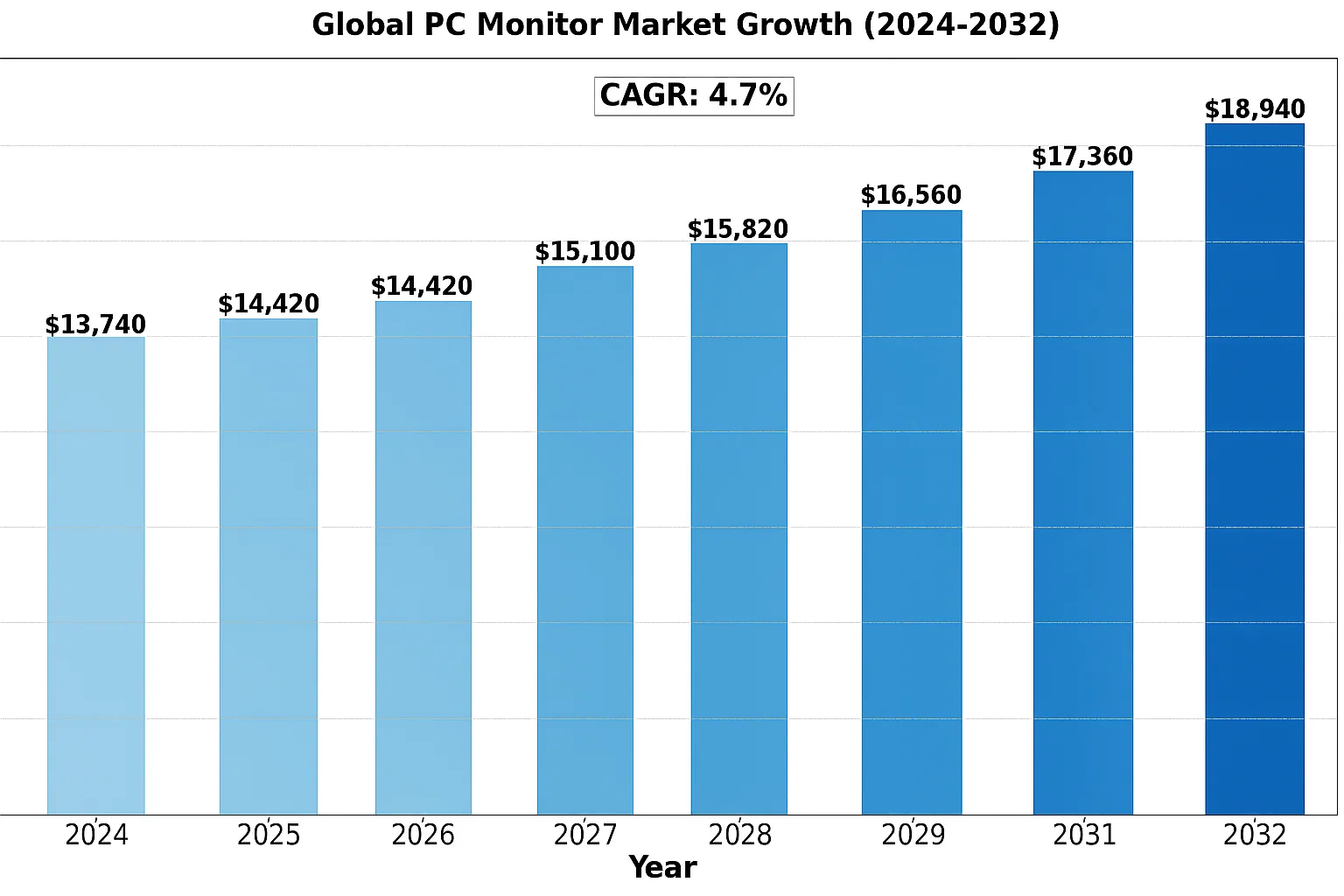

The Global Personal Computer (PC) Monitor Market size was valued at US$ 13,740 million in 2024 and is projected to reach US$ 18,940 million by 2032, at a CAGR of 4.7% during the forecast period 2025-2032.

PC monitors are display devices that connect to computer systems to provide visual output. These devices range from traditional LCD/LED panels to advanced gaming monitors with high refresh rates (144Hz-360Hz) and cutting-edge OLED displays offering superior color accuracy. Key specifications include resolution (HD, Full HD, 4K, 8K), panel type (IPS, TN, VA), screen size (ranging from 15″ to 49″ ultrawide formats), and specialized features like HDR and adaptive sync technologies.

The market growth is driven by increasing demand for high-resolution displays in professional and gaming applications, along with the rising adoption of multi-monitor setups in corporate environments. However, the segment faces challenges from the growing popularity of all-in-one PCs and laptop-first work cultures. Recent technological advancements like mini-LED backlighting and quantum dot enhancement films are creating new opportunities, particularly in the premium monitor segment where companies like Dell and Samsung are introducing innovative products with improved energy efficiency and slim bezel designs.

MARKET DYNAMICS

MARKET DRIVERS

Global Rise in Remote Work and Hybrid Offices Fueling PC Monitor Demand

The shift to remote work culture has become a permanent fixture across industries, driving sustained demand for PC monitors. With over 58% of American workers now operating in hybrid arrangements, home office setups require multiple displays for productivity. This trend accelerated during the pandemic and shows no signs of reversing, as companies realize the cost savings from reduced office footprints. High-resolution monitors between 24-27 inches have seen particular growth, becoming the new standard for professional use cases.

Esports Boom and Gaming Monitor Innovations Accelerating Market Growth

The global esports industry, valued at nearly $1.38 billion, continues to push monitor technology boundaries. Competitive gaming requires ultra-fast refresh rates (now reaching 500Hz) and near-instant response times under 1ms. Major manufacturers are responding with curved OLED panels featuring adaptive sync technologies. The gaming monitor segment grew by approximately 19% last year alone, representing one of the fastest-growing categories in the display market. New innovations like mini-LED backlighting further enhance contrast ratios for immersive gameplay experiences.

Moreover, content creators are driving adoption of 4K and 8K professional monitors. Photographers, video editors and 3D artists require perfect color accuracy (covering 99% Adobe RGB) and high pixel density for detailed work.

➤ For instance, LG’s 32-inch 8K monitor with 10-bit color depth and 1000-nit brightness has become an industry benchmark for creative professionals.

These high-end segments command premium pricing while pushing technological advancements that eventually trickle down to mainstream models.

MARKET RESTRAINTS

Smartphone and Tablet Cannibalization Impacting Entry-Level Monitor Sales

While premium monitor segments thrive, basic 1080p models face declining demand due to mobile device substitution. Many casual users now rely solely on smartphones and tablets for everyday computing tasks, delaying monitor purchases. This trend particularly affects emerging markets where mobile penetration exceeds computer ownership. Industry data suggests entry-level monitor shipments decreased by approximately 8% last year as consumers prioritize mobile upgrades over secondary displays.

Other Restraints

Supply Chain Volatility

Panel production remains concentrated in Asia, making the industry susceptible to geopolitical tensions and logistics disruptions. Display driver IC shortages continue impacting manufacturing schedules despite improving from pandemic-era crisis levels.

Environmental Regulations

Stricter energy efficiency requirements across regions compel redesigns that increase production costs. The EU’s latest EcoDesign regulations demand power consumption cuts up to 40% for certain monitor categories.

MARKET CHALLENGES

Panel Overcapacity Creating Pricing Pressures Across Market Segments

The display industry faces cyclical oversupply conditions as Chinese panel makers aggressively expand production capacity. This has led to dramatic price erosion – some 27-inch IPS panels now wholesale for 22% less than two years ago. While benefiting consumers, these conditions squeeze manufacturer margins and discourage R&D investment. Panel makers attempt to differentiate through features rather than competing solely on price, but the market remains extremely competitive.

Other Challenges

Technology Transition Costs

Shifting from LCD to next-gen technologies like microLED requires massive capital expenditures exceeding $5 billion per fabrication plant, creating financial barriers.

Channel Inventory Management

Retailers maintain leaner inventories post-pandemic, forcing manufacturers to implement just-in-time production strategies and sophisticated demand forecasting.

MARKET OPPORTUNITIES

Healthcare Sector Digital Transformation Creates New Monitor Applications

Hospital digitization initiatives worldwide are driving demand for specialized medical monitors. These displays must meet stringent regulatory requirements for brightness consistency (≤10% deviation), grayscale performance, and antimicrobial coatings. The medical monitor market grows approximately 9% annually as facilities upgrade diagnostic imaging systems and digital patient records infrastructure. New surgical monitors with 4K 3D visualization capabilities enable minimally invasive procedures with enhanced precision.

Emerging Markets Present Untapped Growth Potential

While mature markets approach saturation, developing regions in Southeast Asia, Latin America and Africa show strong monitor adoption curves. Improving internet infrastructure and growing IT sectors create demand for productivity displays. Government digital education programs also contribute – India’s edtech initiatives alone deployed over 2 million monitors to schools last year. Localization strategies including regional distribution partnerships and affordable installment payment options help manufacturers capitalize on these growth frontiers.

GLOBAL PERSONAL COMPUTER (PC) MONITOR MARKET TRENDS

Rising Demand for High Refresh Rate and Low Response Time Monitors

The increasing popularity of competitive gaming and esports has fueled significant demand for high-performance monitors with refresh rates exceeding 144Hz and response times below 1ms. Currently, gaming monitors account for over 30% of total PC monitor shipments, with this segment growing at nearly 15% annually. Consumers are prioritizing monitors with technologies like NVIDIA G-SYNC and AMD FreeSync to eliminate screen tearing during fast-paced gameplay. Major manufacturers have responded by introducing ultra-wide curved monitors with refresh rates up to 360Hz, catering specifically to professional gamers who require split-second response advantages.

Other Trends

4K/UHD Adoption Accelerates

The shift towards higher resolution displays continues gaining momentum, with 4K/UHD monitors now representing about 25% of total market revenues. This growth is driven by professionals in creative industries such as video editing, graphic design, and CAD engineering who require precise pixel-perfect displays. Declining panel production costs have made 4K monitors more affordable, with average selling prices dropping by approximately 35% over the past three years. Furthermore, the increasing availability of HDMI 2.1 and DisplayPort 2.0 compatible monitors ensures these high-resolution displays can fully leverage next-generation graphics hardware.

Remote Work Expansion Stimulates Monitor Market

The global shift towards hybrid and remote work arrangements has created sustained demand for home office setups featuring multi-monitor configurations. Recent surveys indicate that over 60% of knowledge workers now use two or more monitors, compared to just 35% pre-pandemic. This trend has particularly benefited the market for mid-range business monitors featuring eye-care technologies like flicker-free backlighting and low blue light emission. Manufacturers have responded by developing productivity-focused monitors with USB-C docking capabilities, built-in webcams, and adjustable ergonomic stands to accommodate extended work sessions.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Market Expansion Drive Competition in the PC Monitor Landscape

The global PC monitor market exhibits a highly competitive environment dominated by multinational electronics corporations and specialized display manufacturers. According to recent industry analyses, the market remains largely consolidated among top-tier players, though mid-size manufacturers continue to gain traction through strategic differentiation in gaming, professional, and budget segments.

Dell Technologies maintains leadership with approximately 22% market share in Q1 2023, credited to its commercial segment dominance and Alienware gaming monitor innovations. Close competitor HP Inc. follows with 18% share, benefiting from strong enterprise partnerships and its Omen gaming monitor lineup. Both companies leverage vertical integration advantages through their existing PC ecosystems.

Korean giants Samsung Electronics and LG Display collectively control nearly 30% of the premium monitor segment through OLED and quantum-dot display technologies. Their 2024 product refreshes emphasize 240Hz+ refresh rates and 8K resolution adoption, catering to professional creators and esports enthusiasts.

Meanwhile, TPV Technology (AOC/Philips monitors) and Lenovo have intensified competition through aggressive pricing strategies for mainstream 1080p and 1440p models. TPV reportedly shipped 12 million units in 2023 alone, primarily to Asian and European markets.

List of Key PC Monitor Manufacturers Profiled

- Dell Technologies (U.S.)

- HP Inc. (U.S.)

- TPV Technology Limited (Taiwan)

- Lenovo Group (China)

- LG Electronics (South Korea)

- Samsung Electronics (South Korea)

- AOC International (Netherlands)

- HUIKE ELECTRONICS (China)

Segment Analysis:

By Type

High-Resolution Monitors Segment Dominates Due to Growing Demand for Enhanced Visual Experience

The market is segmented based on type into:

- Esports Monitors

- Subtypes: Ultra-wide, Curved, and others

- High-Resolution Monitors

- Surface Monitors

- Standard Monitors

- Others

By Application

Gaming Series Leads Market Adoption Driven by Rising Esports and High-Performance Computing Needs

The market is segmented based on application into:

- Gaming Series

- Business Series

- Home Entertainment

- Professional Design

- Others

By Display Technology

LED Backlit LCDs Maintain Market Dominance Due to Cost-Effectiveness and Energy Efficiency

The market is segmented based on display technology into:

- LCD

- Subtypes: LED-backlit, CCFL-backlit

- OLED

- QLED

- Others

By Screen Size

27-32 Inches Segment Gains Traction as the Optimal Balance Between Workspace and Viewing Comfort

The market is segmented based on screen size into:

- Below 24 inches

- 24-27 inches

- 27-32 inches

- Above 32 inches

Regional Analysis: Global Personal Computer (PC) Monitor Market

North America

The North American PC monitor market is characterized by high adoption rates of premium displays, driven by robust gaming, corporate, and creative professional sectors. With major brands like Dell, HP, and LG dominating the landscape, the region sees strong demand for high-resolution (4K/8K) and ultrawide monitors, particularly in the U.S. and Canada. The work-from-home trend post-pandemic continues to influence purchasing patterns, with hybrid work models sustaining steady demand for ergonomic and productivity-focused monitors. However, market saturation in some segments has led manufacturers to focus on innovation in OLED and mini-LED technologies to stimulate upgrades. Environmental regulations, such as ENERGY STAR certification requirements, are shaping product development toward energy-efficient designs.

Europe

Europe’s mature market prioritizes sustainability and performance, with stringent EU energy efficiency directives pushing manufacturers toward eco-friendly monitors. Germany and the UK lead in adoption of business-class monitors, while Southern Europe shows growing interest in budget-friendly models. The gaming segment is expanding rapidly, fueled by increasing esports participation and demand for high-refresh-rate displays. Brands like AOC and Samsung are gaining traction with competitively priced curved and gaming-focused monitors. However, inflationary pressures and energy crises in some countries have temporarily slowed replacement cycles, particularly in price-sensitive consumer segments.

Asia-Pacific

As the largest and fastest-growing regional market, Asia-Pacific benefits from strong OEM presence and massive consumer bases in China, India, and Southeast Asia. China dominates both production and consumption, with local brands like TPV and HUIKE competing aggressively on price. The region shows divergent trends – while mature markets like Japan and South Korea demand cutting-edge technology, emerging economies prioritize affordability, driving sales of entry-level Full HD monitors. India’s expanding IT sector and gaming culture are creating new growth pockets. Manufacturing advantages in Taiwan and China keep production costs low, though supply chain diversification is underway due to geopolitical tensions.

South America

The South American market operates with distinct pricing sensitivities, where economic volatility often dictates purchasing power. Brazil and Argentina represent the largest markets, with consumers favoring value-oriented brands and smaller screen sizes (21-24 inches) for cost efficiency. Corporate purchases are gradually increasing as businesses modernize infrastructure, though adoption of advanced features like HDR and high refresh rates remains limited outside major metropolitan areas. Import dependencies and currency fluctuations create pricing challenges, leading some manufacturers to establish local assembly operations to improve affordability.

Middle East & Africa

This emerging market demonstrates two-tiered growth patterns. Gulf Cooperation Council (GCC) countries show appetite for premium gaming and professional monitors, driven by high disposable incomes and developing tech ecosystems. In contrast, African markets focus on affordable, durable displays for educational and entry-level business use. Infrastructure limitations like inconsistent power supply in some areas influence product specifications, with energy-efficient LED backlit models gaining preference. The region sees increasing competition from Chinese brands offering competitive warranties and localized support.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Personal Computer (PC) Monitor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global PC Monitor market was valued at USD 38.2 billion in 2024 and is projected to reach USD 48.5 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Esports Monitors, High Resolution Monitors, Surface Monitors), technology (LCD, OLED, QLED), application (Gaming, Business, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates with over 40% market share.

- Competitive Landscape: Profiles of leading market participants including Dell, HP, LG, Samsung, Lenovo, AOC, TPV, and HUIKE ELECTRONICS, including their product portfolios, R&D focus, manufacturing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies including mini-LED, micro-LED, high refresh rates (up to 360Hz), and HDR advancements.

- Market Drivers & Restraints: Evaluation of factors driving market growth (remote work trends, esports popularity) along with challenges (supply chain constraints, component shortages).

- Stakeholder Analysis: Insights for panel manufacturers, OEMs, distributors, retailers, and investors regarding strategic opportunities in the evolving display ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PC Monitor Market?

-> Personal Computer (PC) Monitor Market size was valued at US$ 13,740 million in 2024 and is projected to reach US$ 18,940 million by 2032, at a CAGR of 4.7% during the forecast period 2025-2032.

Which key companies operate in Global PC Monitor Market?

-> Key players include Dell, HP, LG, Samsung, Lenovo, AOC, TPV, and HUIKE ELECTRONICS.

What are the key growth drivers?

-> Key growth drivers include hybrid work models, gaming industry expansion, and demand for high-resolution displays.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (over 40%), driven by manufacturing hubs in China and growing demand in India.

What are the emerging trends?

-> Emerging trends include ultra-wide curved displays, 8K resolution adoption, and integration with IoT ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...