MARKET INSIGHTS

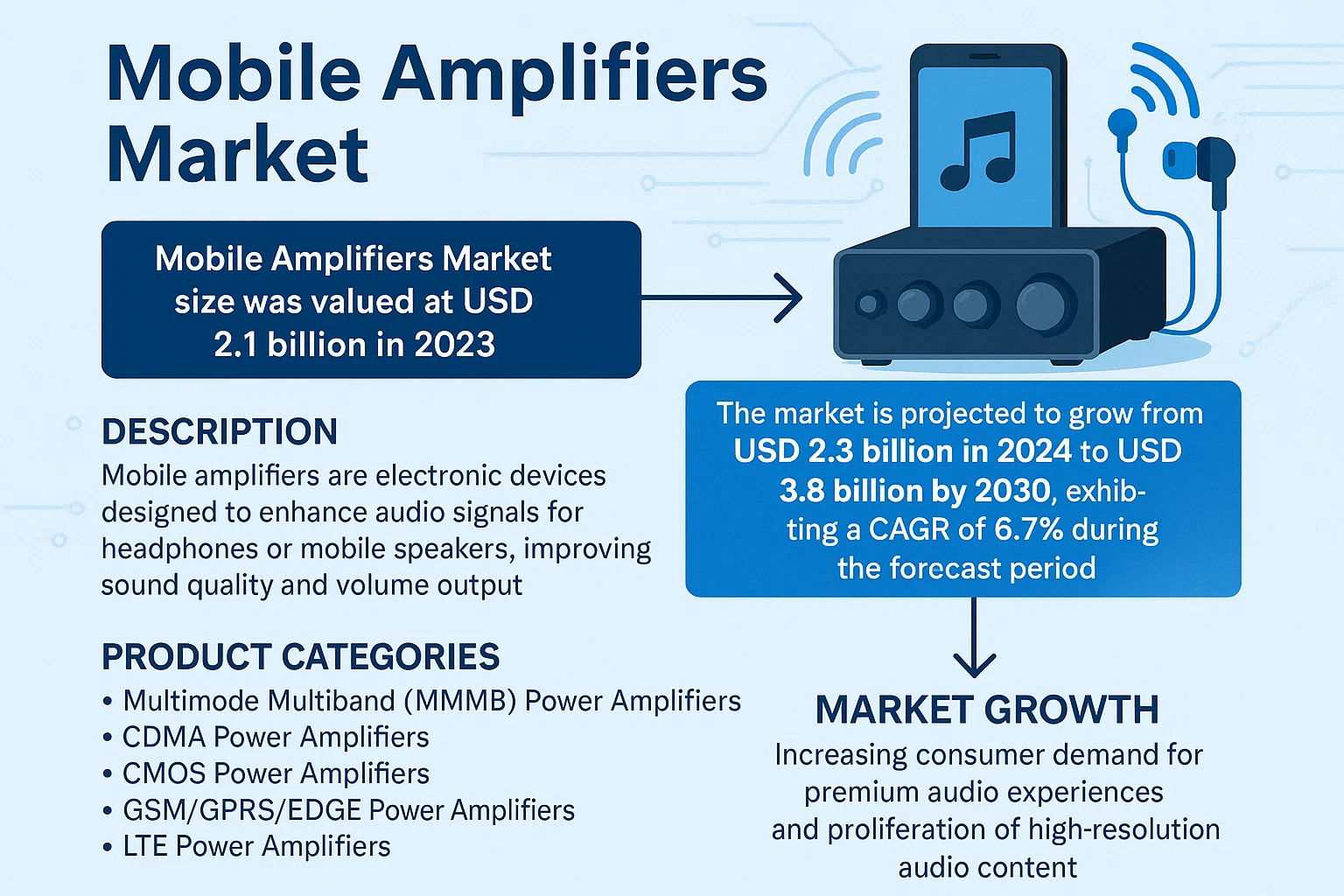

Global Mobile Amplifiers Market size was valued at USD 2.1 billion in 2023. The market is projected to grow from USD 2.3 billion in 2024 to USD 3.8 billion by 2030, exhibiting a CAGR of 6.7% during the forecast period.

Mobile amplifiers are electronic devices designed to enhance audio signals for headphones or mobile speakers, improving sound quality and volume output. These components play a critical role in delivering high-fidelity audio experiences across various portable devices, including smartphones, tablets, and wireless earbuds. The product categories include Multimode Multiband (MMMB) Power Amplifiers, CDMA Power Amplifiers, CMOS Power Amplifiers, GSM/GPRS/EDGE Power Amplifiers, and LTE Power Amplifiers, among others.

The market growth is driven by increasing consumer demand for premium audio experiences and the proliferation of high-resolution audio content. However, the industry faces challenges from miniaturization trends in consumer electronics. Recent technological advancements in power efficiency and noise reduction are creating new opportunities, particularly in IoT-enabled audio devices. Key players like Qorvo, Skyworks Solutions, and Rockford Fosgate are investing in R&D to develop next-generation amplifier solutions compatible with 5G networks and emerging audio formats.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of High-Impedance Audio Devices to Accelerate Market Expansion

The global mobile amplifiers market is experiencing substantial growth driven by the increasing adoption of high-impedance headphones and premium audio accessories. With over 75% of audiophile-grade headphones now featuring impedance ratings above 32 ohms, mobile devices struggle to deliver adequate power and audio fidelity without dedicated amplification. This technical gap has created a robust demand for portable amplification solutions that can unlock the full potential of high-end audio equipment. The market has responded with innovative product developments, including ultra-compact amplifiers with battery life exceeding 20 hours and signal-to-noise ratios better than 110 dB. These advancements enable consumers to experience studio-quality audio reproduction in mobile environments, driving both consumer adoption and manufacturer innovation across the audio ecosystem.

Rising Consumer Expenditure on Premium Audio Experiences to Fuel Market Growth

Consumer spending on high-fidelity audio equipment has demonstrated consistent growth, with the personal audio equipment market expanding at approximately 8% annually. This trend is particularly pronounced in the mobile amplifier segment, where consumers increasingly seek professional-grade audio performance from their portable devices. The convergence of multiple factors—including increased disposable income, growing awareness of audio quality differences, and the popularity of high-resolution audio streaming services—has created a perfect storm of demand. Mobile amplifiers bridge the critical gap between source devices and high-performance headphones, enabling consumers to achieve reference-level audio quality without stationary equipment. This value proposition has proven particularly compelling for mobile professionals, audiophiles, and content creators who require accurate audio monitoring in various environments.

Technological Advancements in Semiconductor Manufacturing to Drive Product Innovation

Breakthroughs in semiconductor technology have enabled manufacturers to develop increasingly sophisticated mobile amplification solutions. The adoption of advanced fabrication processes has allowed for the integration of multiple amplification stages, sophisticated digital signal processing, and efficient power management within remarkably small form factors. Modern mobile amplifiers now incorporate technologies such as fully differential amplification architectures, advanced thermal management systems, and ultra-low noise operational amplifiers that achieve noise levels below 1.2 nV/√Hz. These technical improvements have simultaneously reduced power consumption while improving audio performance, creating products that deliver both extended battery life and superior sonic characteristics. The continuous miniaturization of components has further enabled the development of amplifiers that are virtually indistinguishable in size from standard audio adapters while providing substantial power output capabilities.

Furthermore, integration with mobile operating systems through dedicated applications has enabled users to customize audio profiles, monitor battery status, and adjust gain settings seamlessly, enhancing both functionality and user experience across diverse listening scenarios.

MARKET RESTRAINTS

Pricing Sensitivity in Emerging Markets to Constrain Adoption Rates

The mobile amplifiers market faces significant price sensitivity challenges, particularly in developing economies where disposable income levels remain constrained. Premium mobile amplification products typically command prices ranging from 150% to 400% of standard audio accessories, creating a substantial barrier to entry for cost-conscious consumers. This pricing structure reflects the sophisticated components, research and development investments, and specialized manufacturing processes required to produce high-performance audio amplification. However, in markets where the average expenditure on audio accessories rarely exceeds certain thresholds, these premium products struggle to gain traction despite their technical superiority. Manufacturers must navigate this challenge through tiered product strategies, localized manufacturing, and innovative cost-reduction techniques without compromising audio quality.

Technical Integration Challenges with Mobile Devices to Limit Market Penetration

Mobile amplifiers face persistent technical integration challenges that restrain market growth. The rapid evolution of mobile device connectivity standards—including the removal of traditional audio jacks and the proliferation of proprietary connector systems—creates compatibility issues that complicate the user experience. Consumers must navigate an increasingly complex landscape of adapters, compatibility specifications, and power requirements when connecting amplification equipment to their mobile devices. Additionally, the electromagnetic interference generated by mobile devices can adversely affect amplifier performance, requiring sophisticated shielding and filtering technologies that increase both complexity and cost. These technical hurdles often discourage casual users from adopting dedicated amplification solutions, limiting the market primarily to audio enthusiasts and professionals who are willing to overcome these integration challenges.

Intense Competition from Integrated Audio Solutions to Restrict Market Expansion

The mobile amplifiers market operates within an increasingly competitive landscape dominated by integrated audio solutions developed by mobile device manufacturers. Recent advancements in onboard audio processing have enabled smartphones and tablets to deliver audio performance that satisfies the majority of mainstream consumers. These integrated solutions leverage sophisticated digital signal processing, customized amplification stages, and advanced audio codecs to provide competent audio performance without additional accessories. This technological progression has narrowed the performance gap between integrated audio and dedicated amplification, particularly for consumers using mainstream audio equipment. Consequently, the value proposition of external mobile amplifiers becomes less compelling for average users, restricting market expansion to segments where performance requirements exceed the capabilities of integrated solutions.

MARKET OPPORTUNITIES

Emergence of Wireless Amplification Technologies to Create New Market Segments

The development of advanced wireless amplification technologies presents significant growth opportunities for market participants. Bluetooth-enabled amplification systems that support high-resolution audio codecs including LDAC, aptX HD, and LHDC have gained substantial consumer interest, particularly among users seeking cable-free audio experiences without compromising quality. These systems typically incorporate sophisticated digital-to-analog conversion, multiple amplification stages, and advanced power management within compact form factors. The wireless amplification segment has demonstrated remarkable growth potential, with adoption rates increasing by approximately 40% annually as consumers embrace the convenience of wireless connectivity combined with high-fidelity audio performance. This convergence of wireless technology and high-performance audio creates entirely new product categories and usage scenarios that expand the addressable market beyond traditional wired amplification solutions.

Expansion into Professional and Creator Economies to Drive Premium Segment Growth

The rapid growth of content creation and mobile professional workflows has created substantial opportunities for specialized mobile amplification solutions. Content creators, podcasters, field recording professionals, and mobile broadcasters require accurate audio monitoring capabilities that traditional consumer audio solutions cannot provide. This professional segment demands features including ultra-low latency monitoring, multiple input/output configurations, advanced metering capabilities, and ruggedized construction suitable for field use. The addressing of these specialized requirements enables manufacturers to develop premium products with enhanced functionality and corresponding price points, creating higher-margin market segments. The professional audio market’s growth, particularly in mobile content creation, provides a fertile ground for innovation and premium product development that differs substantially from consumer-grade amplification solutions.

Integration with Smart Ecosystem Devices to Enable New Functionality

The increasing integration of mobile amplifiers with smart ecosystem devices presents compelling opportunities for market expansion. Modern amplification systems can now interface with smart assistants, home automation systems, and multi-room audio configurations, creating enhanced user experiences that transcend simple audio amplification. This connectivity enables features including voice-controlled audio adjustment, automatic scene detection, seamless switching between multiple audio sources, and intelligent power management based on usage patterns. The convergence of amplification technology with smart ecosystem capabilities creates products that serve as central hubs for personal audio ecosystems rather than simple signal amplification devices. This evolution toward connected, intelligent amplification systems opens new revenue streams and product differentiation opportunities that were previously unavailable in traditional amplification markets.

MARKET CHALLENGES

Consumer Education and Market Awareness Deficits to Hinder Adoption

The mobile amplifiers market faces significant challenges regarding consumer education and market awareness. A substantial portion of potential users remains unaware of the audio quality improvements achievable through dedicated amplification, particularly when using high-impedance headphones or sensitive in-ear monitors. This knowledge gap results in underappreciation of the value proposition offered by mobile amplification solutions, limiting market penetration to informed enthusiasts. Manufacturers must invest substantially in educational initiatives, demonstration platforms, and comparative listening experiences to communicate the tangible benefits of their products. However, these educational efforts face the inherent challenge of demonstrating audio quality differences in environments where consumers cannot directly compare amplified and unamplified performance, creating a persistent barrier to broader market adoption.

Other Challenges

Supply Chain Constraints

The mobile amplifiers market encounters persistent supply chain challenges affecting critical components including specialized operational amplifiers, high-quality digital-to-analog converters, and precision passive components. These supply constraints frequently result from concentrated manufacturing resources, complex production processes, and fluctuating demand across multiple industries. The specialized nature of audio-grade components further exacerbates these challenges, as alternative sourcing options are often limited or non-existent. Manufacturers must navigate these supply chain complexities while maintaining product quality and performance standards, creating operational challenges that affect both production timelines and cost structures.

Technical Standardization Issues

The absence of universal technical standards for mobile amplification creates interoperability challenges and consumer confusion. Various manufacturers implement different gain structures, input sensitivity specifications, and performance measurement methodologies, making direct product comparisons difficult for consumers. This lack of standardization complicates the purchasing process and may lead to suboptimal product selection based on incomplete or misleading specifications. The industry’s movement toward establishing consistent measurement standards and performance metrics remains gradual, perpetuating these challenges in the near to medium term.

GLOBAL MOBILE AMPLIFIERS MARKET TRENDS

Integration of Advanced Semiconductor Technologies to Emerge as a Trend in the Market

The global mobile amplifiers market is experiencing a significant transformation driven by the integration of advanced semiconductor technologies, particularly Gallium Nitride (GaN) and Silicon Carbide (SiC). These materials offer superior performance characteristics, including higher power density, improved thermal efficiency, and greater bandwidth capabilities compared to traditional silicon-based amplifiers. This technological shift is crucial for supporting the increasing demands of 5G networks, which require amplifiers to operate efficiently at higher frequencies and with lower power consumption. The adoption of GaN-based power amplifiers, for instance, has grown substantially because they enable more compact device designs while providing the necessary output power for next-generation mobile handsets and infrastructure. Furthermore, the push towards more efficient power management in mobile devices to extend battery life continues to drive innovation in amplifier design, focusing on reducing energy loss and heat generation during operation.

Other Trends

Proliferation of 5G Infrastructure and Smart Devices

The global rollout of 5G technology is a primary catalyst for the mobile amplifiers market, necessitating advanced components that can handle higher data rates and more complex signal modulation schemes. The transition to 5G requires amplifiers that support massive MIMO (Multiple Input Multiple Output) systems and operate across a broader range of frequency bands, including sub-6 GHz and millimeter-wave spectra. This expansion is not limited to smartphones but extends to a wide array of connected devices, such as tablets, laptops, IoT modules, and automotive communication systems. The increasing number of 5G subscriptions, projected to exceed 2 billion globally by 2025, underscores the massive scale of infrastructure deployment and device adoption, directly fueling demand for high-performance mobile amplifiers. This trend is further amplified by the growing consumer expectation for seamless high-speed connectivity and low-latency experiences in both urban and rural settings.

Rising Demand for Enhanced Audio Experiences in Mobile Devices

While RF amplifiers for cellular connectivity dominate the market, there is a concurrent and growing trend in the demand for high-fidelity audio amplifiers in mobile devices. Consumers increasingly use smartphones and tablets for media consumption, gaming, and professional audio applications, creating a need for superior sound quality and louder volume without distortion. This has led to the integration of more sophisticated audio amplifier chipsets that support technologies like high-resolution audio, Dolby Atmos, and advanced noise cancellation. Manufacturers are focusing on developing amplifiers that deliver clear, powerful audio while maintaining energy efficiency to preserve battery life. The audio amplifier segment, though a smaller part of the overall mobile amplifiers market, is experiencing robust growth because of these heightened consumer expectations for immersive multimedia experiences on portable devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global mobile amplifiers market exhibits a fragmented competitive structure, characterized by a mix of established semiconductor giants, specialized audio equipment manufacturers, and emerging technology firms. Qorvo, Inc. and Skyworks Solutions, Inc. are dominant forces, primarily due to their extensive portfolios of RF power amplifiers critical for 5G-enabled mobile handsets and their entrenched relationships with leading smartphone OEMs like Apple and Samsung. Their market leadership is further solidified by significant R&D investments; for instance, Skyworks allocated over $650 million to R&D in its 2023 fiscal year, focusing on advanced front-end modules that integrate amplifiers.

TOA Corporation and Rockford Fosgate maintain strong positions in the professional and automotive audio segments, respectively. TOA’s strength lies in its robust public address and commercial sound systems, which often incorporate high-fidelity mobile amplifier components. Rockford Fosgate continues to leverage its brand reputation in the car audio market, where its amplifiers are prized for their power output and reliability. The growth of these companies is intrinsically linked to the broader automotive infotainment and professional audio markets, which are experiencing steady demand.

Furthermore, companies are aggressively pursuing growth through strategic initiatives. This includes geographical expansion into high-growth regions like Asia-Pacific, where smartphone penetration is highest, and new product launches designed for emerging applications such as IoT and machine-to-machine (M2M) communication modules. These efforts are crucial for capturing market share in a rapidly evolving technological landscape.

Meanwhile, players like Wilson Electronics (a part of WilsonPro) and Creative Labs are strengthening their niches through focused innovation. Wilson Electronics specializes in cellular signal boosters that incorporate powerful amplifiers, a market that grew in relevance with the increase in remote work. Creative Labs continues to invest in its Super X-Fi technology for personal audio amplification, aiming to deliver immersive sound experiences on mobile devices. Their targeted strategies ensure they remain relevant and competitive alongside the larger semiconductor suppliers.

List of Key Mobile Amplifier Companies Profiled

- Qorvo, Inc. (U.S.)

- Skyworks Solutions, Inc. (U.S.)

- TOA Corporation (Japan)

- Rockford Fosgate (U.S.)

- Humantechnik (Germany)

- Elite Radio & Engineering Company (U.S.)

- Wilson Electronics (U.S.)

- Pyle (U.S.)

- Monoprice (U.S.)

- Supersonic (U.S.)

- Shaxon (Australia)

- OSD Audio (U.S.)

- Enermax (Taiwan)

- AmpliVox Sound Systems (U.S.)

- Cerwin-Vega Mobile (U.S.)

- Creative Labs (Singapore)

Segment Analysis:

By Type

LTE Power Amplifiers Segment Dominates the Market Due to Proliferation of High-Speed Mobile Networks

The market is segmented based on type into:

- Multimode Multiband (MMMB) Power Amplifiers

- CDMA Power Amplifiers

- CMOS Power Amplifiers

- GSM/GPRS/EDGE Power Amplifiers

- LTE Power Amplifiers

- Other

By Application

Mobile Handsets Segment Leads Due to Ubiquitous Smartphone Adoption and Advanced Audio Requirements

The market is segmented based on application into:

- Mobile Handsets

- Tablets And Laptops

- Data Cards

- Machine-To-Machine (M2M) Modules

- Other

By Technology

GaAs Technology Holds Significant Share Owing to Superior High-Frequency Performance

The market is segmented based on technology into:

- Gallium Arsenide (GaAs)

- Silicon Germanium (SiGe)

- Complementary Metal-Oxide-Semiconductor (CMOS)

- Gallium Nitride (GaN)

By End-User

Consumer Electronics Segment Prevails Driven by High Volume Demand for Personal Audio Devices

The market is segmented based on end-user into:

- Consumer Electronics

- Telecommunications

- Automotive

- Industrial

Regional Analysis: Global Mobile Amplifiers Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global mobile amplifiers market, both in terms of production and consumption. This dominance is fueled by the region’s position as the world’s electronics manufacturing hub, with countries like China, South Korea, and Taiwan housing the headquarters and major fabrication plants for key semiconductor companies such as Skyworks Solutions and Qorvo. The massive consumer base, particularly in China and India, with over 1.5 billion mobile phone subscribers combined, drives immense demand for mobile handsets and, consequently, the power amplifiers within them. The region is also at the forefront of adopting next-generation network technologies. The rapid rollout of 5G infrastructure, especially in China, Japan, and South Korea, is creating a significant surge in demand for advanced LTE and 5G New Radio (NR) power amplifiers. While cost-competitive, high-volume manufacturing defines a large segment of the market, there is a parallel and growing trend toward innovation, with local manufacturers increasingly investing in R&D to develop more efficient and integrated amplifier modules for the global stage.

North America

North America represents a highly advanced and technologically sophisticated market for mobile amplifiers, characterized by strong demand for high-performance components. The region is a critical center for research, development, and innovation, hosting the headquarters of major players like Qorvo and Skyworks Solutions. The aggressive deployment and adoption of 5G networks by major carriers have been a primary market driver, necessitating advanced amplifier solutions that support new frequency bands and complex carrier aggregation techniques. Furthermore, there is a robust and growing market for premium audio-focused mobile amplifiers, or headphone amps, driven by a consumer base with high disposable income and a strong appetite for high-fidelity audio experiences with their mobile devices and laptops. The market is also significantly influenced by the Internet of Things (IoT) and Machine-to-Machine (M2M) applications, where reliable connectivity is paramount, creating steady demand for amplifiers used in data cards and various modules beyond smartphones.

Europe

The European market for mobile amplifiers is mature and is primarily driven by stringent regulatory standards and a strong push for technological advancement. EU directives concerning radio equipment and electromagnetic compatibility ensure that amplifiers entering the market are highly efficient and generate minimal interference. This regulatory environment fosters innovation in amplifier design, particularly for energy efficiency and miniaturization. Similar to North America, Europe is experiencing a rapid transition to 5G, which is fueling demand for the latest LTE and 5G power amplifier technologies. The region also exhibits a significant market for high-quality consumer audio products. Brands focused on the premium audio segment find a receptive audience, supporting the market for external mobile headphone amplifiers that enhance sound quality from smartphones and tablets. The presence of a strong automotive industry also contributes to demand, as modern connected cars integrate numerous cellular modules for telematics and infotainment systems, each requiring its own RF power amplification.

South America

The mobile amplifiers market in South America is in a growth phase, largely tethered to the expansion and upgrading of mobile network infrastructure across the region. Countries like Brazil and Argentina are seeing increased investments in 4G LTE networks and the initial foundations for 5G, which in turn stimulates demand for mobile amplifiers in handsets and network equipment. The market is highly price-sensitive, with a strong presence of mid-range and budget mobile devices, which often utilize cost-effective amplifier solutions. While the adoption of external audio amplifiers remains a niche compared to other regions, it is growing among audiophiles and gaming enthusiasts in urban centers. Economic volatility remains a challenge, impacting consumer purchasing power and sometimes slowing the pace of network upgrades, which can create a somewhat fragmented and unpredictable demand landscape for amplifier manufacturers and suppliers.

Middle East & Africa

The Middle East and Africa region presents an emerging but promising market for mobile amplifiers, characterized by diverse levels of development. Gulf Cooperation Council (GCC) nations, such as Saudi Arabia and the UAE, are leaders in adopting cutting-edge technology. Their rapid deployment of 5G networks creates immediate demand for advanced amplifier modules, aligning closely with trends in developed markets. In contrast, many African nations are still focused on expanding basic 3G and 4G coverage to connect growing populations. This drives volume demand for more fundamental CDMA and GSM/GPRS/EDGE power amplifiers. The market for external audio amplifiers is nascent but has potential for growth in major urban areas as disposable incomes rise. Overall, the region’s growth is fueled by increasing mobile penetration, but it is uneven, with progress often dependent on political stability, economic conditions, and infrastructure investment.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Mobile Amplifiers markets, covering the forecast period 2024–2030. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mobile Amplifiers Market?

->Mobile Amplifiers Market size was valued at USD 2.1 billion in 2023. The market is projected to grow from USD 2.3 billion in 2024 to USD 3.8 billion by 2030, exhibiting a CAGR of 6.7% during the forecast period.

Which key companies operate in Global Mobile Amplifiers Market?

-> Key players include Qorvo, Skyworks Solutions, Broadcom Inc., Qualcomm, Texas Instruments, Analog Devices, NXP Semiconductors, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising smartphone penetration, deployment of 5G networks, increasing demand for high-fidelity audio in mobile devices, and growth in IoT and M2M communication.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 60% of global revenue, driven by high mobile device production and consumption in China, South Korea, and India.

What are the emerging trends?

-> Emerging trends include integration of AI for power optimization, development of ultra-compact amplifiers for wearables, adoption of GaN and SiC technologies for improved efficiency, and increasing focus on energy-efficient designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...