MARKET INSIGHTS

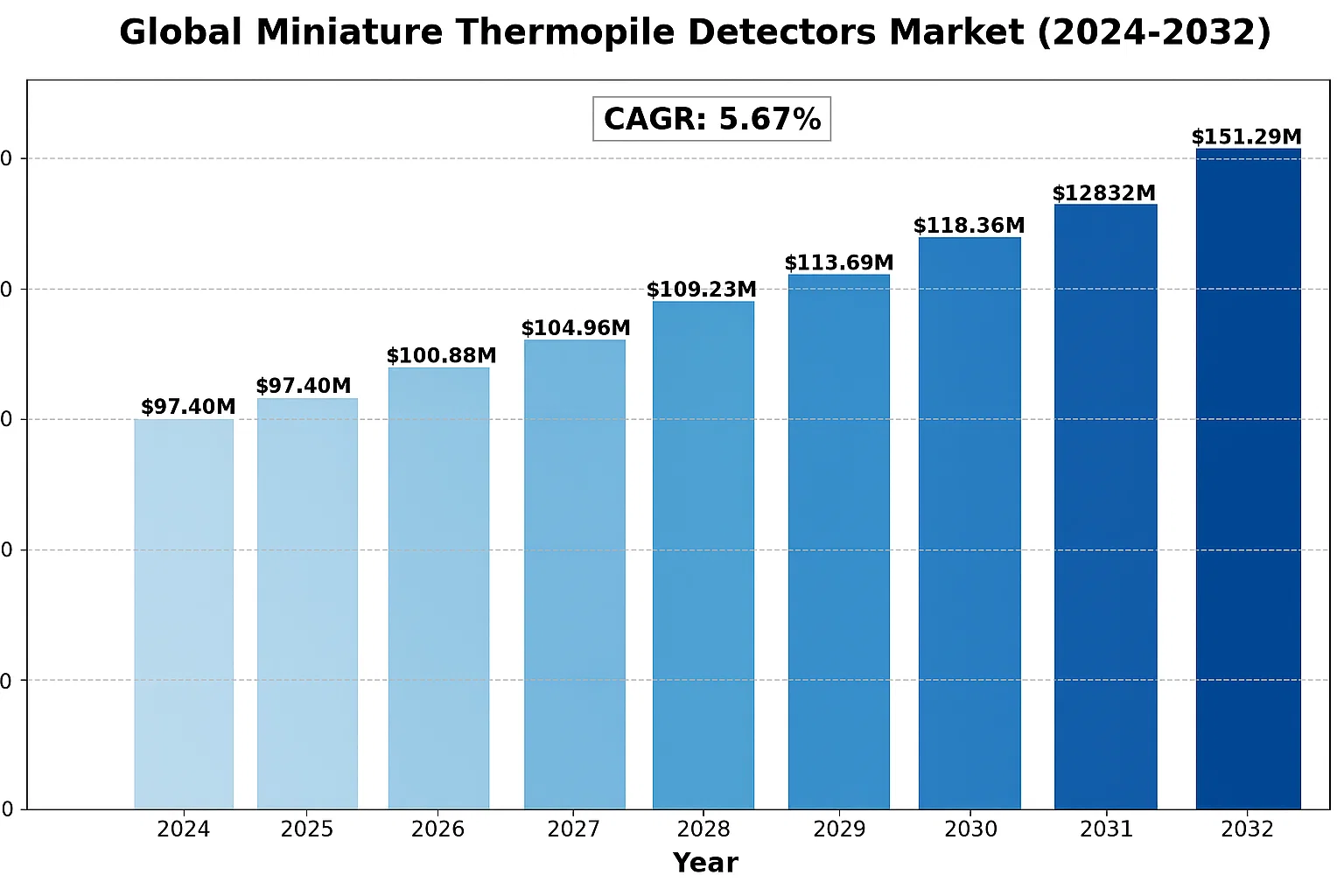

The global Miniature Thermopile Detectors Market was valued at US$ 97.4 million in 2024 and is projected to reach US$ 151.2 million by 2032, at a CAGR of 5.67% during the forecast period 2025-2032.

Miniature thermopile detectors are infrared sensors that convert thermal energy into electrical signals through the thermoelectric effect. These compact devices feature micro-sensor solutions, sensitive chips, and small optical windows, with integrated thermistors for ambient temperature compensation. They are widely used for non-contact temperature measurement across various industries due to their small form factor, high sensitivity, and fast response times.

The market growth is driven by increasing demand for miniaturized thermal sensors in medical devices, automotive applications, and consumer electronics. Advancements in MEMS technology have enabled cost-effective production, while the growing adoption of IoT devices creates new opportunities. However, competition from alternative technologies like pyroelectric detectors presents challenges. Key players such as Honeywell, Excelitas, and Hamamatsu Photonics are investing in product innovations to maintain market share, with recent developments focusing on improved accuracy and reduced power consumption for battery-operated applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Non-Contact Temperature Measurement to Accelerate Market Expansion

The global miniature thermopile detectors market is experiencing robust growth, primarily driven by the increasing demand for non-contact temperature measurement solutions across industries. These detectors offer significant advantages in applications requiring precision, speed, and hygiene – particularly in medical diagnostics where infrared thermometers became indispensable during recent health crises. The medical thermometer segment alone is projected to maintain a compound annual growth rate exceeding 7% through 2030, creating sustained demand for high-performance thermopile sensors.

Automotive Safety Innovations Fuel Adoption in Vehicle Systems

Automotive manufacturers are increasingly integrating miniature thermopile detectors into advanced driver assistance systems (ADAS) for pedestrian detection and cabin monitoring. This trend aligns with the industry’s shift toward autonomous vehicles, where thermal imaging complements traditional LiDAR and camera systems. Recent regulatory mandates in several countries requiring enhanced night vision capabilities have further stimulated demand. The global automotive infrared sensor market is expected to surpass $2 billion by 2027, with thermopile-based solutions capturing a growing share.

Smart Home Ecosystem Integration Creates New Application Horizons

The proliferation of smart home devices presents significant opportunities for miniature thermopile detectors, particularly in energy management systems and security applications. These sensors enable presence detection without privacy concerns associated with cameras while providing temperature monitoring capabilities. Major technology companies have begun incorporating thermopile arrays into their smart home platforms, driving standardization and reducing implementation costs. The smart home sensor market has grown at over 15% annually since 2020, with thermal detection emerging as a key differentiator for premium products.

MARKET RESTRAINTS

Performance Limitations in Harsh Environments Constrain Adoption

While miniature thermopile detectors offer numerous advantages, their performance can be significantly affected by environmental factors such as humidity, dust, and extreme temperatures. Industrial applications often require sensors that maintain accuracy in challenging conditions where competing technologies like RTDs or thermocouples may be preferred. The need for frequent calibration and compensation circuits adds complexity to system designs, particularly in cost-sensitive applications. These technical constraints limit market penetration in sectors like heavy manufacturing and outdoor infrastructure monitoring.

Supply Chain Vulnerabilities Impact Production Capacity

The miniature thermopile detector market faces significant supply chain challenges, particularly regarding specialty materials required for high-performance sensors. Many manufacturers rely on a limited number of suppliers for critical components such as thermoelectric materials and precision optical filters. Recent geopolitical tensions and trade restrictions have exacerbated these vulnerabilities, leading to extended lead times and price volatility. Industry analysts estimate that supply chain disruptions have caused average delivery times to increase by 30-45 days compared to pre-pandemic levels, creating bottlenecks for OEMs.

Intellectual Property Barriers Slow Market Entry

The competitive landscape in miniature thermopile detectors is shaped by extensive patent portfolios held by established players, creating barriers for new entrants. Core technologies related to sensor packaging, signal processing algorithms, and calibration methods are often protected by complex patent thickets. This intellectual property landscape requires significant legal and licensing expenditures for companies attempting to commercialize innovative designs, potentially stifling competition and slowing the pace of technological advancement. Smaller firms frequently face litigation risks that can delay product launches by 12-18 months.

MARKET OPPORTUNITIES

Emerging Medical Applications Open New Revenue Streams

The healthcare sector presents transformative opportunities for miniature thermopile detectors beyond traditional thermometry applications. Researchers are developing novel diagnostic tools that utilize thermal imaging for early detection of conditions ranging from vascular disorders to breast cancer. Recent clinical trials have demonstrated the potential for thermopile-based systems to reduce screening costs while improving accessibility in low-resource settings. The global medical infrared imaging market is projected to grow at a 9% CAGR through 2030, driven by these innovative applications.

Industrial IoT Integration Creates Scalable Deployment Models

The convergence of miniature thermopile detectors with industrial IoT platforms enables continuous equipment monitoring at scale. Predictive maintenance systems incorporating thermal sensors can identify overheating components before failure, reducing downtime in manufacturing facilities. Energy management applications are particularly promising, with thermopile arrays providing granular temperature data for optimizing HVAC systems in large commercial buildings. Manufacturing plants implementing these solutions have reported energy savings of 15-25%, demonstrating the compelling ROI for industrial users.

Advancements in MEMS Technology Enable Cost Reduction

Breakthroughs in microelectromechanical systems (MEMS) fabrication are lowering the production costs of miniature thermopile detectors while improving performance characteristics. New wafer-level packaging techniques and integrated signal conditioning circuits are reducing bill-of-materials costs by up to 40% for certain sensor configurations. These advancements are making thermopile solutions economically viable for consumer electronics applications that were previously cost-prohibitive. The MEMS sensor market is forecast to exceed $30 billion by 2028, with thermal detectors representing one of the fastest-growing segments.

GLOBAL MINIATURE THERMOPILE DETECTORS MARKET TRENDS

Integration of IoT and AI Driving Demand for Miniature Thermopile Detectors

The rapid advancement of Internet of Things (IoT) and Artificial Intelligence (AI) technologies has significantly increased the adoption of miniature thermopile detectors across various industries. These compact infrared sensors are becoming indispensable in smart home automation, industrial monitoring, and wearable health devices due to their ability to provide non-contact temperature measurements with high accuracy. The global market is projected to grow at a compound annual growth rate (CAGR) of approximately 6.5% from 2023 to 2028, fueled by increasing automation across sectors. Manufacturers are now incorporating advanced signal processing algorithms and machine learning capabilities into thermopile detectors, enabling real-time analytics and predictive maintenance applications.

Other Trends

Healthcare and Medical Applications

The healthcare sector’s growing emphasis on non-invasive patient monitoring is creating substantial opportunities for miniature thermopile detectors. Recent advancements in thermal imaging for fever detection, particularly in the post-pandemic era, have accelerated their adoption in hospitals and public spaces. These detectors are being integrated into portable medical devices for measuring body temperature, blood flow monitoring, and even early detection of certain medical conditions. The medical applications segment is expected to account for over 25% of the total market share by 2025, driven by increasing healthcare expenditure worldwide.

Automotive Industry Adoption Accelerating

The automotive sector is witnessing surging demand for miniature thermopile detectors, particularly for advanced driver-assistance systems (ADAS) and cabin comfort applications. Modern vehicles incorporate these sensors for occupant detection, climate control optimization, and pedestrian detection in night vision systems. With the global automotive infrared sensor market projected to exceed $2.5 billion by 2026, thermopile detectors are becoming a critical component in next-generation vehicles. Leading automakers are increasingly partnering with sensor manufacturers to develop customized solutions that meet stringent automotive safety and reliability standards while maintaining compact form factors.

Energy Efficiency Regulations Shaping Market Dynamics

Stringent energy efficiency regulations worldwide are prompting increased adoption of miniature thermopile detectors in building automation and smart infrastructure. These regulations, such as the EU’s Energy Performance of Buildings Directive (EPBD), have created strong demand for smart HVAC systems utilizing thermal sensors for optimized energy consumption. Building automation currently represents nearly 30% of the total miniature thermopile detector applications, with commercial buildings leading the adoption curve. Sensor manufacturers are responding with ultra-low power consumption designs that can operate on energy harvesting systems, further expanding their application potential in green building initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Miniaturization and Precision to Gain Competitive Edge

The global miniature thermopile detectors market exhibits a mix of established players and emerging competitors, with key manufacturers focusing on miniaturization, energy efficiency, and multi-spectral detection capabilities. Honeywell International Inc. dominates a significant portion of the market, leveraging its decades of experience in sensor technology and strong distribution networks across industrial sectors.

Hamamatsu Photonics and Excelitas Technologies have emerged as important players, particularly in medical and industrial applications where high-precision temperature measurement is critical. These companies continue to invest heavily in MEMS-based thermopile technology to maintain their market positions.

Recent industry trends show that competition is intensifying through strategic acquisitions and patent developments. TE Connectivity strengthened its market position by acquiring First Sensor AG in 2020, gaining access to advanced thermopile technologies for automotive applications. Similarly, Melexis continues to expand its portfolio of contactless temperature sensors for automotive and industrial markets.

Smaller specialized manufacturers like Heimann Sensor GmbH and LASER COMPONENTS are carving out niches in specific applications, particularly in HVAC and consumer electronics, through customized solutions and rapid prototyping capabilities.

List of Key Miniature Thermopile Detector Manufacturers

- Honeywell International Inc. (U.S.)

- Excelitas Technologies Corp. (U.S.)

- Thorlabs, Inc. (U.S.)

- Newport Corporation (U.S.)

- Hamamatsu Photonics K.K. (Japan)

- LASER COMPONENTS GmbH (Germany)

- TE Connectivity Ltd. (Switzerland)

- PerkinElmer, Inc. (U.S.)

- International Light Technologies (U.S.)

- SK-Advanced Co., Ltd. (South Korea)

- Heimann Sensor GmbH (Germany)

- Electro Optical Components, Inc. (U.S.)

- Melexis NV (Belgium)

- Fluke Corporation (U.S.)

- Jotrin Electronics Ltd. (China)

Segment Analysis:

By Type

Square Window Format Dominates Due to Higher Compatibility with Compact Device Integration

The market is segmented based on type into:

- Circular Window Format

- Square Window Format

By Application

Medical Industry Leads Through Extensive Use in Non-contact Temperature Measurement Devices

The market is segmented based on application into:

- Medical Industry

- Construction Industry

- Automobile Industry

- Electronic Products

- Others

By Detection Range

Medium Range Detectors (0°C to 300°C) Show Maximum Adoption Across Industries

The market is segmented based on detection range into:

- Low Range (-40°C to 100°C)

- Medium Range (0°C to 300°C)

- High Range (up to 600°C)

By Output Signal

Analog Output Remains Preferred Choice for Most Legacy Systems

The market is segmented based on output signal into:

- Analog Output

- Digital Output

Regional Analysis: Global Miniature Thermopile Detectors Market

North America

The North American miniature thermopile detectors market is driven by advanced manufacturing capabilities and strong demand from medical and industrial automation sectors. The U.S. accounts for over 60% of regional market share, with leading manufacturers like Honeywell and TE Connectivity focusing on high-precision sensors for healthcare diagnostics and smart home applications. Strict FDA regulations for medical-grade thermopiles are accelerating R&D investments in miniaturization and IoT integration. However, supply chain disruptions and semiconductor shortages have temporarily constrained production volumes in 2022-2023. The Canadian market shows promising growth in automotive thermal sensing applications, particularly for EV battery monitoring systems.

Europe

Europe’s market thrives on stringent industrial safety standards (EN ISO 13849) and growing adoption of thermopiles in building automation. Germany dominates with 35% of regional revenues, driven by its robust automotive sector’s demand for occupant detection systems. The EU’s EcoDesign Directive has pushed manufacturers like Melexis and Hamamatsu Photonics to develop energy-efficient detector solutions. While Western Europe shows maturity with steady 5-7% annual growth, Eastern Europe presents untapped potential – particularly in smart meter applications across Poland and Czech Republic. Brexit-related trade complexities continue to impact UK supply chains, creating minor logistical challenges.

Asia-Pacific

As the fastest-growing region, APAC is projected to capture 42% of global market share by 2025, led by China’s electronics manufacturing boom and India’s healthcare expansion. Japanese firms (Hamamatsu, Panasonic) lead in precision thermopile production, while Chinese manufacturers like SK-Advanced are gaining ground with cost-competitive alternatives. The proliferation of consumer electronics and government initiatives like India’s “Make in India” are accelerating adoption. However, quality standardization remains inconsistent across Southeast Asia, creating both opportunities and challenges for international suppliers. Temperature screening needs post-pandemic have spurred demand in public infrastructure projects throughout the region.

South America

South America presents a developing market with growth concentrated in Brazil and Argentina’s industrial sectors. While economic volatility limits large-scale investments, the automotive aftermarket and food processing industries show 12% annual demand increase for basic thermopile solutions. Local production remains limited with 85% of detectors being imported, primarily from China and the U.S. Regulatory frameworks are evolving, with Brazil’s INMETRO certification gaining importance for quality compliance. The region’s renewable energy sector is emerging as a potential growth avenue for thermopiles in solar thermal monitoring applications.

Middle East & Africa

MEA’s market is nascent but shows strategic growth in oil/gas infrastructure monitoring and healthcare modernization. The UAE and Saudi Arabia account for 70% of regional demand, driven by smart city projects and hospital expansions. African adoption is largely limited to South Africa’s mining sector, though telecommunications infrastructure development is creating new opportunities. Pricing sensitivity dominates procurement decisions, favoring mid-range Asian imports over premium Western products. Lack of local testing facilities and technical expertise remains a market restraint, though regional partnerships with European and Chinese firms are gradually improving technical capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Miniature Thermopile Detectors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Miniature Thermopile Detectors market was valued at US$ 97.4 million in 2024 and is projected to reach US$ 151.2 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Circular Window Format, Square Window Format), application (Medical, Automotive, Electronics), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis of key markets.

- Competitive Landscape: Profiles of 15+ leading market participants including Honeywell, Excelitas, Hamamatsu Photonics, and Melexis, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends: Analysis of MEMS-based sensors, IoT integration, and emerging applications in smart devices and industrial automation.

- Market Drivers & Restraints: Evaluation of factors including demand for non-contact temperature measurement, industrial automation growth, and challenges related to miniaturization.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory databases and company filings to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Miniature Thermopile Detectors Market?

-> Miniature Thermopile Detectors Market was valued at US$ 97.4 million in 2024 and is projected to reach US$ 151.2 million by 2032, at a CAGR of 5.67% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Honeywell, Excelitas, Hamamatsu Photonics, Thorlabs, TE Connectivity, and Melexis among others.

What are the key growth drivers?

-> Growth is driven by increasing automation, demand for contactless temperature measurement, and expanding applications in medical devices and automotive systems.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (38% in 2024), while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include MEMS-based detectors, integration with IoT platforms, and development of ultra-miniature sensors for wearable devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...