MARKET INSIGHTS

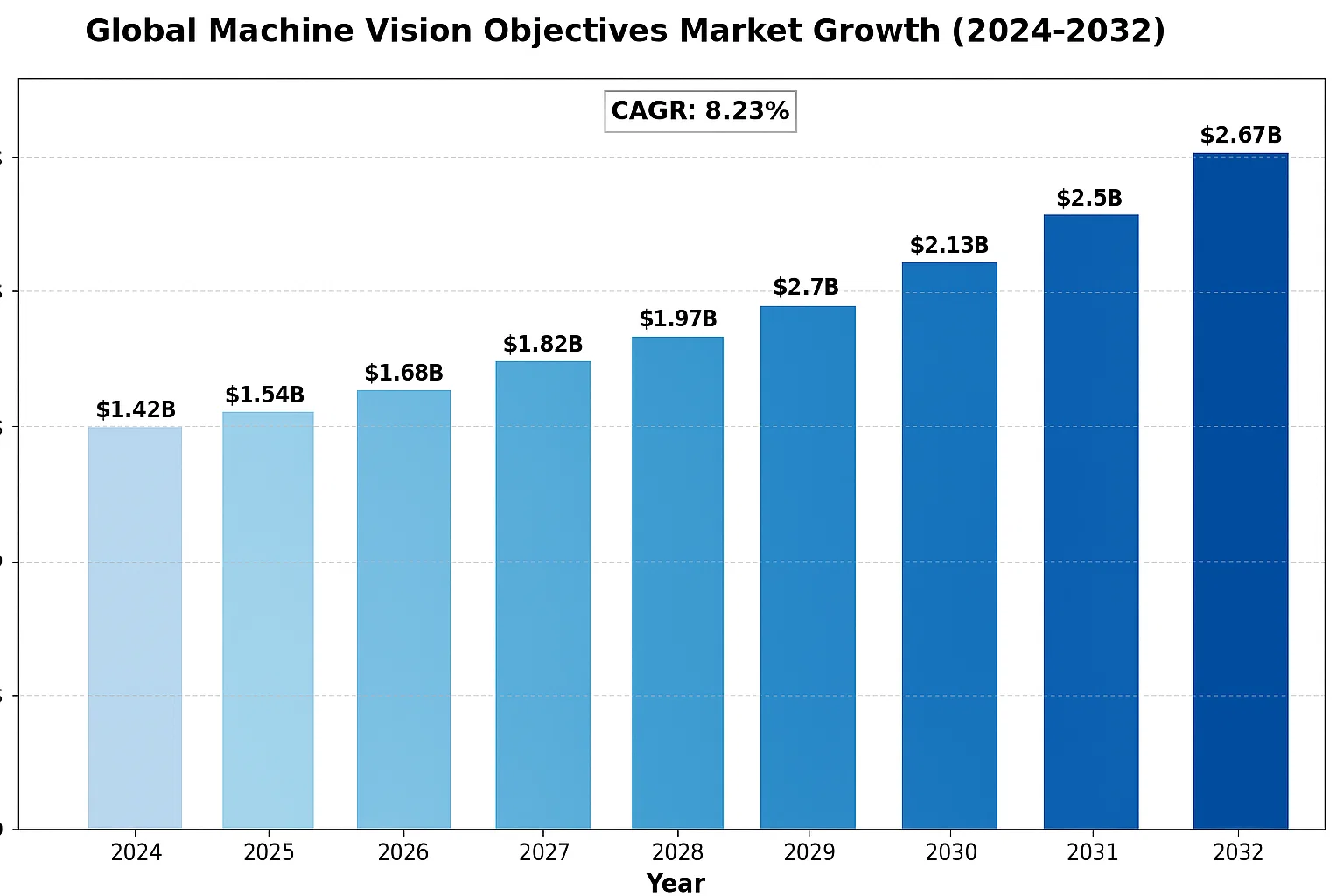

The global Machine Vision Objectives Market was valued at US$ 1.42 billion in 2024 and is projected to reach US$ 2.67 billion by 2032, at a CAGR of 8.23% during the forecast period 2025-2032.

Machine vision objectives are specialized optical components designed for industrial imaging systems, offering precise image capture with minimal distortion. These components include both spherical objectives (standard lenses with curved surfaces) and aspheric objectives (advanced lenses with complex surface profiles that reduce optical aberrations). They play a critical role in quality control, measurement, and inspection across manufacturing, pharmaceuticals, and automotive industries by providing high-resolution imaging with consistent accuracy.

The market growth is driven by increasing automation in manufacturing, stringent quality control regulations, and advancements in AI-powered visual inspection systems. The Asia-Pacific region dominates demand due to rapid industrialization, while North America shows strong growth from pharmaceutical and aerospace applications. Key players like Cognex, Edmund Optics, and FLIR Systems are expanding their product portfolios through technological innovations such as telecentric lenses for metrology applications.

MARKET DYNAMICS

MARKET DRIVERS

Industry 4.0 Adoption Accelerates Demand for Machine Vision Objectives

The global manufacturing sector’s rapid transition towards Industry 4.0 standards is transforming production facilities with advanced automation technologies. Machine vision systems have become critical components in smart factories, with the market projected to grow at a compound annual rate exceeding 10% through 2030. These systems rely on specialized objectives that provide precise imaging capabilities for quality inspection, robotic guidance, and measurement applications. The automotive industry alone accounts for over 25% of machine vision system deployments, where objectives must deliver micrometer-level accuracy for critical component verification.

E-Commerce Logistics Revolution Fuels Vision System Deployments

Explosive growth in e-commerce has created unprecedented demand for automated parcel handling solutions, with global warehouse automation investments surpassing $25 billion annually. Machine vision objectives enable high-speed barcode reading, package dimensioning, and damage detection at throughput rates exceeding 10,000 items per hour. Major logistics providers are retrofitting facilities with multi-camera inspection tunnels that require specialized wide-field objectives with minimal distortion. This sector’s continuous expansion, coupled with labor shortages in material handling, ensures sustained demand for vision components. Recent innovations in telecentric optics now allow single cameras to cover wider conveyor belts, reducing system costs while maintaining inspection accuracy.

Pharmaceutical Serialization Mandates Create Compliance-Driven Demand

Stringent pharmaceutical packaging regulations across major markets have mandated serialized tracking for prescription medications. This regulatory environment requires 100% inspection of unique identifiers on drug packaging, driving installations of high-resolution vision systems. Machine vision objectives in this sector must resolve microscopic print defects while maintaining consistent performance across varying surface finishes. The market for pharmaceutical inspection systems is expected to maintain 8-10% annual growth through 2028, with serialization compliance remaining a key adoption driver. Recent lens developments now incorporate anti-reflective coatings and specialized illumination geometries to handle challenging blister pack and vial inspection scenarios.

MARKET CHALLENGES

Precision Manufacturing Requirements Elevate Production Complexities

While machine vision objectives deliver transformative capabilities, their manufacturing presents significant technical hurdles. Aspheric lens elements, critical for distortion correction, require nanometer-level surface accuracy during polishing and coating. Yield rates for advanced multi-element objectives frequently fall below 60% due to stringent optical performance requirements. Additionally, the global semiconductor shortage has disrupted supply chains for specialized glass materials, with lead times for certain substrates extending beyond 12 months. These manufacturing constraints create bottlenecks that limit market expansion despite growing end-user demand.

Integration Challenges with Legacy Systems

Retrofitting machine vision solutions into existing production lines often requires substantial reengineering, particularly in brownfield manufacturing sites. Many older facilities lack the structural rigidity needed for micrometer-precision imaging, with vibration and thermal fluctuations degrading system performance. Vision objectives must frequently be customized with specially designed mounting interfaces, adding 15-20% to project costs. Furthermore, integrating new vision systems with legacy programmable logic controllers often requires additional gateway hardware, creating compatibility issues that delay deployment timelines.

Optical Performance Tradeoffs in Challenging Environments

Machine vision objectives must maintain imaging performance across extreme industrial conditions that include temperature variations exceeding 50°C, particulate contamination, and high-voltage electromagnetic interference. While protective housings can mitigate environmental factors, they frequently introduce optical path length constraints that compromise imaging performance. Recent field studies indicate that nearly 30% of vision system failures stem from optical component degradation in harsh operating environments. Developing objectives that balance ruggedness with optical performance remains an ongoing engineering challenge.

MARKET RESTRAINTS

High Initial Investment Costs Limit SME Adoption

The significant capital expenditure required for industrial machine vision systems creates adoption barriers for small-to-medium enterprises. A complete vision inspection station incorporating specialized objectives, lighting, and processing hardware typically represents an investment exceeding $50,000 per point of inspection. Additionally, system integration and validation often accounts for 40-60% of total project costs. Many manufacturers with limited automation budgets consequently delay vision system deployments despite recognizing their long-term benefits. This cost sensitivity is particularly pronounced in price-competitive industries with thin profit margins.

Technical Expertise Shortage Impacts Implementation Quality

The machine vision industry faces a critical shortage of qualified optical engineers and system integrators capable of properly specifying and deploying vision objectives. With fewer than 5,000 certified vision professionals globally, many end-users lack internal expertise to properly match lens specifications to application requirements. Incorrect objective selection frequently results in suboptimal system performance, with field studies indicating that nearly 35% of vision installations require post-deployment optical component upgrades. The complexity of modern multi-element objectives further exacerbates this knowledge gap, as proper performance validation requires specialized test equipment and measurement protocols.

MARKET OPPORTUNITIES

Emerging Electric Vehicle Manufacturing Creates New Application Verticals

The global transition to electric vehicles is driving billion-dollar investments in new battery production facilities that require unprecedented levels of quality control. Machine vision objectives are being adapted for specialized applications including electrode coating inspection, separator alignment verification, and weld seam analysis. These emerging use cases demand novel optical configurations that combine high resolution with extended depth of field. The EV battery sector alone is projected to require over 50,000 new vision systems annually by 2027, creating substantial opportunities for objective manufacturers to develop application-specific solutions.

Advancements in Computational Imaging Reshape Optical Requirements

Innovative computational imaging techniques are enabling machine vision systems to extract additional information from conventional optical systems. New multi-aperture designs allow single objectives to simultaneously capture images at multiple magnifications or focal planes, reducing the need for mechanical adjustment. Additionally, deep learning-based image processing can compensate for certain optical aberrations, allowing relaxed tolerances in some lens elements. These advancements are driving demand for objectives specifically designed to complement computational imaging pipelines, with the market for such systems growing at nearly 20% annually.

Miniaturization Trend Expands Applications in Micro-Manufacturing

The proliferation of miniature electronic components and medical devices has created demand for ultra-high magnification vision objectives capable of sub-micron resolution. New long-working-distance microscope objectives now enable inspection of microelectromechanical systems (MEMS) and precision medical components without physical contact. Furthermore, the development of compact 2-3mm diameter borescope objectives allows internal inspection of intricate assemblies. This miniaturization trend is expanding machine vision into applications previously inaccessible to conventional optics, with the medical device inspection segment alone projected to exceed $1.5 billion in vision component expenditures by 2026.

GLOBAL MACHINE VISION OBJECTIVES MARKET TRENDS

Industry 4.0 Adoption Fuels Demand for High-Precision Objectives

The global machine vision objectives market is experiencing robust growth driven by the widespread adoption of Industry 4.0 technologies across manufacturing sectors. As factories increasingly implement automated quality control systems, the need for high-resolution imaging with minimal distortion has surged. Spherical objectives currently dominate with approximately 65% market share due to their cost-effectiveness in standard inspection tasks. However, demand for aspheric objectives is growing at 8.2% CAGR as manufacturers seek superior aberration correction for complex inspections. The integration of machine vision with AI-powered analytics is further accelerating this shift, requiring optics with sub-micron accuracy for defect detection in semiconductor and electronics manufacturing.

Other Trends

Expansion in Pharmaceutical Quality Control

Pharmaceutical companies are significantly increasing investments in vision-based inspection systems to comply with stringent regulatory requirements. The sector now accounts for nearly 18% of machine vision objective sales, with particular demand for telecentric lenses that maintain measurement accuracy regardless of part positioning. This trend aligns with the industry’s 7.9% annual growth in automated quality assurance expenditure, as manual inspection methods fail to meet both throughput requirements and FDA 21 CFR Part 11 compliance standards for data integrity.

Automotive Sector Drives Innovation in Multi-Spectral Imaging

Automotive manufacturers are pushing the boundaries of machine vision capabilities to keep pace with advanced driver assistance systems (ADAS) production requirements. There’s growing adoption of multi-spectral objectives capable of simultaneous visible and infrared imaging for comprehensive component inspection. This aligns with the industry’s 12.4% annual growth in vision system deployments for autonomous vehicle component manufacturing. Recent developments include liquid lens integration for rapid focal length adjustment, reducing cycle times in high-speed production lines by approximately 23% compared to traditional mechanical focusing systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in Machine Vision Objectives Market

The global machine vision objectives market features a semi-consolidated competitive landscape, with established optical technology providers competing alongside specialized vision system manufacturers. Cognex Corporation has emerged as a dominant player, leveraging its integrated machine vision solutions and strong foothold in industrial automation across North America and Europe. The company commands approximately 18-22% market share in vision inspection systems, according to industry estimates.

Edmund Optics and Moritex Corporation represent significant competitors, particularly in precision optics for specialized applications. These companies benefit from decades of optical engineering expertise and have successfully expanded their product portfolios to include telecentric lenses and high-resolution objectives that meet growing demand for micron-level inspection accuracy.

Meanwhile, FLIR Systems (now Teledyne FLIR) has strengthened its position through strategic acquisitions, including the purchase of ISRA Vision in 2021, enhancing its capabilities in surface inspection and quality control solutions. This consolidation trend is expected to continue as companies seek to offer comprehensive vision systems rather than standalone optical components.

List of Key Machine Vision Objectives Companies Profiled

- Cognex Corporation (U.S.)

- Edmund Optics (U.S.)

- Excelitas Technologies Corp. (U.S.)

- VITRONIC GmbH (Germany)

- MORITEX Corporation (Japan)

- Opto Engineering S.p.A. (Italy)

- TAMRON Co., Ltd. (Japan)

- Resolve Optics Ltd. (UK)

- Universe Optics (U.S.)

- SEIWA Optical Co.,Ltd. (Japan)

- TKH Group (Netherlands)

- Teledyne FLIR (U.S.)

Segment Analysis:

By Type

Aspheric Objectives Drive Market Growth With Superior Optical Performance

The global machine vision objectives market is segmented based on type into:

- Spherical Objectives

- Aspheric Objectives

By Application

Industrial Applications Dominate Due to Automated Quality Inspection Needs

The market is segmented based on application into:

- Industrial Automation

- Agriculture

- Pharmaceutical

- Military & Defense

- Aerospace

- Others

By Technology

Telecentric Optics Lead in Precision Applications

The market is segmented based on technology into:

- Telecentric Objectives

- Fixed Focal Length Objectives

- Zoom Objectives

- Macro Objectives

By Mounting Type

C-Mount Dominates Due to Compatibility With Most Industrial Cameras

The market is segmented based on mounting type into:

- C-Mount

- CS-Mount

- F-Mount

- S-Mount

Regional Analysis: Global Machine Vision Objectives Market

North America

The North American machine vision objectives market is driven by strong industrial automation adoption and technological advancements, particularly in the U.S. and Canada. The region holds approximately 35% of the global market share due to widespread implementation in automotive manufacturing and semiconductor inspection. Leading players like Cognex and Edmund Optics dominate with innovations in high-resolution imaging and AI-integrated systems. Strict quality control requirements in pharmaceuticals and aerospace further propel demand for precision optics. However, high equipment costs and skilled labor shortages pose challenges to small and medium enterprises looking to adopt these solutions.

Europe

Europe’s market growth is fueled by its robust manufacturing sector, particularly in Germany’s automotive industry and France’s aerospace applications. The region emphasizes aspheric objectives for superior image quality in critical inspection processes. EU regulations on manufacturing quality standards drive the adoption of machine vision in food packaging and pharmaceutical production lines. Countries like Italy and the UK are investing significantly in smart factory initiatives, creating opportunities for vision system integrators. Competition remains intense among vendors, with companies like VITRONIC and Opto Engineering vying for market share through specialized optical solutions.

Asia-Pacific

As the fastest-growing region, Asia-Pacific accounts for over 40% of global demand, led by China’s massive electronics manufacturing sector and Japan’s robotics industry. The proliferation of smartphone production lines and EV battery inspection systems has created unprecedented need for compact, high-speed vision objectives. While cost-effective spherical lenses dominate in emerging markets like India and Vietnam, premium aspheric solutions are gaining traction in South Korea’s display panel manufacturing. The lack of standardized quality protocols in some countries, however, results in fragmented adoption of advanced machine vision technologies across the region.

South America

The South American market shows moderate growth, primarily driven by Brazil’s automotive sector and Argentina’s agricultural machinery manufacturing. Most demand stems from entry-level machine vision systems using basic spherical objectives due to budget constraints. Foreign manufacturers face challenges with local distribution networks and import restrictions on optical components. Recent economic fluctuations have delayed capital investments in advanced inspection systems, though the food processing industry continues to adopt basic quality control vision solutions. The market remains price-sensitive, favoring domestic suppliers offering maintenance and support services.

Middle East & Africa

This emerging region presents growth potential through infrastructure development and industrial diversification initiatives, particularly in the UAE and Saudi Arabia. Oil and gas pipeline inspection and smart city projects are driving demand for specialized thermal and long-range machine vision objectives. South Africa’s manufacturing sector shows increasing adoption of vision systems for automotive component inspection. However, limited local technical expertise and reliance on imported systems restrain market expansion. Government investments in Industry 4.0 technologies signal future opportunities, particularly in logistics and warehouse automation applications.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Machine Vision Objectives markets, covering the forecast period 2024–2030. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Machine Vision Objectives market was valued at US$ 1.42 billion in 2024 and is projected to reach US$ 2.67 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (spherical vs. aspheric objectives), application (industrial, agriculture, pharmaceuticals, military, aerospace), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with China and Germany showing strongest growth potential.

- Competitive Landscape: Profiles of 18 key players including Cognex, Edmund Optics, and FLIR Systems, covering their product portfolios, market share (top 5 players hold 45% market share), and strategic developments.

- Technology Trends: Assessment of emerging technologies including AI-integrated vision systems, high-resolution imaging (12MP+ adoption growing at 18% CAGR), and miniaturized optics.

- Market Drivers: Analysis of factors including Industry 4.0 adoption (global spending reached USD 130 billion in 2023), quality inspection automation, and smart manufacturing investments.

- Supply Chain Analysis: Evaluation of raw material sourcing, manufacturing clusters (70% production concentrated in Asia-Pacific), and distribution networks.

The report employs primary research (200+ industry interviews) and secondary research (analysis of 50+ proprietary databases) to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Machine Vision Objectives Market?

-> Machine Vision Objectives Market was valued at US$ 1.42 billion in 2024 and is projected to reach US$ 2.67 billion by 2032, at a CAGR of 8.23% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Major players include Cognex, Edmund Optics, FLIR Systems, Excelitas, VITRONIC, and Opto Engineering, with the top 5 companies holding 45% market share.

What are the key growth drivers?

-> Primary drivers are Industry 4.0 adoption, increasing automation in manufacturing (global robotics market reached USD 43.8 billion in 2022), and demand for high-precision inspection systems.

Which region dominates the market?

-> Asia-Pacific holds 42% market share (2023) and shows strongest growth (9.2% CAGR), while North America leads in technological innovation.

What are the emerging trends?

-> Key trends include AI-powered defect detection (adoption growing at 25% annually), hyperspectral imaging, and compact objectives for mobile robotics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...