Glass Interposers Market Analysis:

The Global Glass Interposers Market size was valued at US$ 234.5 million in 2024 and is projected to reach US$ 478.9 million by 2030, at a CAGR of 12.6% during the forecast period 2024-2030.

The United States Glass Interposers market size was valued at US$ 61.5 million in 2024 and is projected to reach US$ 122.3 million by 2030, at a CAGR of 12.1% during the forecast period 2024-2030.

Glass-based interconnect substrates for advanced packaging solutions.

Industry Overview

The growing demand for high-performance, compact electronic devices is propelling the global glass interposers market’s notable expansion. The Global Glass Interposers Market size was valued at US$ 234.5 million in 2024 and is projected to reach US$ 478.9 million by 2030, at a CAGR of 12.6% during the forecast period 2024-2030.

Glass interposers are ideal for use in AI processors, data centres, and photonic devices because they provide better electrical insulation, thermal stability, and a higher interconnect density than conventional substrates. Their adoption is also being aided by the drive for advanced 2.5D/3D packaging technologies and heterogeneous integration.

Segmental Analysis

2.5D glass interposers dominate the market: By Type

The global market for glass interposers is divided into three types: 2D, 2.5D, and 3D. Each type of glass interposer serves different performance needs in semiconductor packaging, and the market is dominated by 2.5D glass interposers because of their ability to provide high interconnect density and enhanced thermal and electrical performance without the complexity of full 3D integration. These interposers are widely used in high-performance applications like data centres, AI processors, and GPUs, while 3D interposers are still in the early stages of commercial deployment but are gaining interest due to their potential to further miniaturise devices and increase bandwidth by stacking multiple active dies vertically. Despite being simpler and less expensive, 2D interposers are usually only used in low-end applications with modest performance requirements. 2.5D and 3D interposer types are anticipated to grow at the fastest rates as the semiconductor industry pushes for greater integration and faster data transmission.

Logic segment to dominate the market: By Application

Application-wise, the global glass interposers market is divided into Logic, Imaging & Optoelectronics, Memory, MEMS/Sensors, LED, and Others. The Logic segment is the market leader among these, thanks to the increasing use of glass interposers in AI chips and advanced processors, which allow for dense interconnects, low latency, and high signal integrity, all of which are essential for high-performance computing and data centre operations. Particularly in the areas of LiDAR systems, optical transceivers, and 3D sensing technologies, the Imaging & Optoelectronics segment is expanding quickly. The optical clarity and dimensional accuracy of glass interposers make them perfect for incorporating photonic components, which are becoming more and more important in high-speed data communication and driverless cars. As the need for small, energy-efficient solutions in graphics processing and AI acceleration increases, the Memory segment is also growing, particularly in high-bandwidth memory (HBM) stacks. With uses in smart wearable’s, automotive safety systems, and Internet of Things devices, MEMS/Sensors is a rapidly developing field where glass interposers offer low parasitic capacitance and thermal stability. Glass substrates in micro-LED and mini-LED technologies are advantageous to the LED segment because they allow for effective thermal management and miniaturization. Glass interposers’ dependability, flatness, and electrical insulation are crucial for mission-critical performance in the others category, which includes industrial, medical, and aerospace applications.

Industry Driver

Rising Demand for High-Speed, High-Density Electronics

One of the key factors propelling the growth of the global glass interposer market is the increase in demand for high-speed and high-density electronic devices. With the proliferation of advancement of technologies like the 5G, AI and the high-performance computing (HPC), the need for components that can support faster signal transmission, reduce signal loss and provide greater bandwidth has been increasing. Glass interposer, offering enhanced electrical insulation, dimensional stability and low electric loss offers a better platform for the integration of multiple chips and optical components in compact design. This leads to making them ideal for next-generation applications in data centres, photonics, and advanced semiconductor packaging.

Industry Restraint

High Cost of Manufacturing as well as Integration Challenges

One major factor restraining the global glass interposer market is the high cost of production, which is mainly because of the complex manufacturing process as well as the need for advanced technologies. Glass interposers are made using complex processes like through-glass via (TGV) formation, accurate metallization, and strict quality control procedures to guarantee performance and dependability. Due to the significant capital expenditure and specialized equipment needed for these processes, small and medium-sized businesses (SMEs) find it difficult to enter or grow in the market. Compatibility problems and the need for process modifications are two more challenges associated with integrating glass interposers into current semiconductor packaging flows. All of these elements work together to increase production costs and complexity, which limits the use of glass interposers in many different applications.

Industry trend

Integration of Glass Interposers in Advanced Packaging Technologies

The growing integration of glass interposers into cutting-edge semiconductor packaging technologies, specifically fan-out wafer-level packaging (FOWLP) and system-in-package (SiP) solutions, is a key trend influencing the global glass interposers market. Because these packaging techniques can meet the demands of high-density integration and miniaturization of contemporary electronic devices, they are becoming more and more popular. In these applications, glass interposers are increasingly being used as the preferred substrate due to their high interconnect density, superior electrical insulation, and thermal stability. Their use makes it easier to create small, powerful devices that meet the expanding demands of industries like consumer electronics, telecommunications, and high-performance computing. This pattern emphasizes how crucial glass interposers are to developing packaging technologies and satisfying the changing performance needs of electronic devices of the next generation.

Regional Analysis

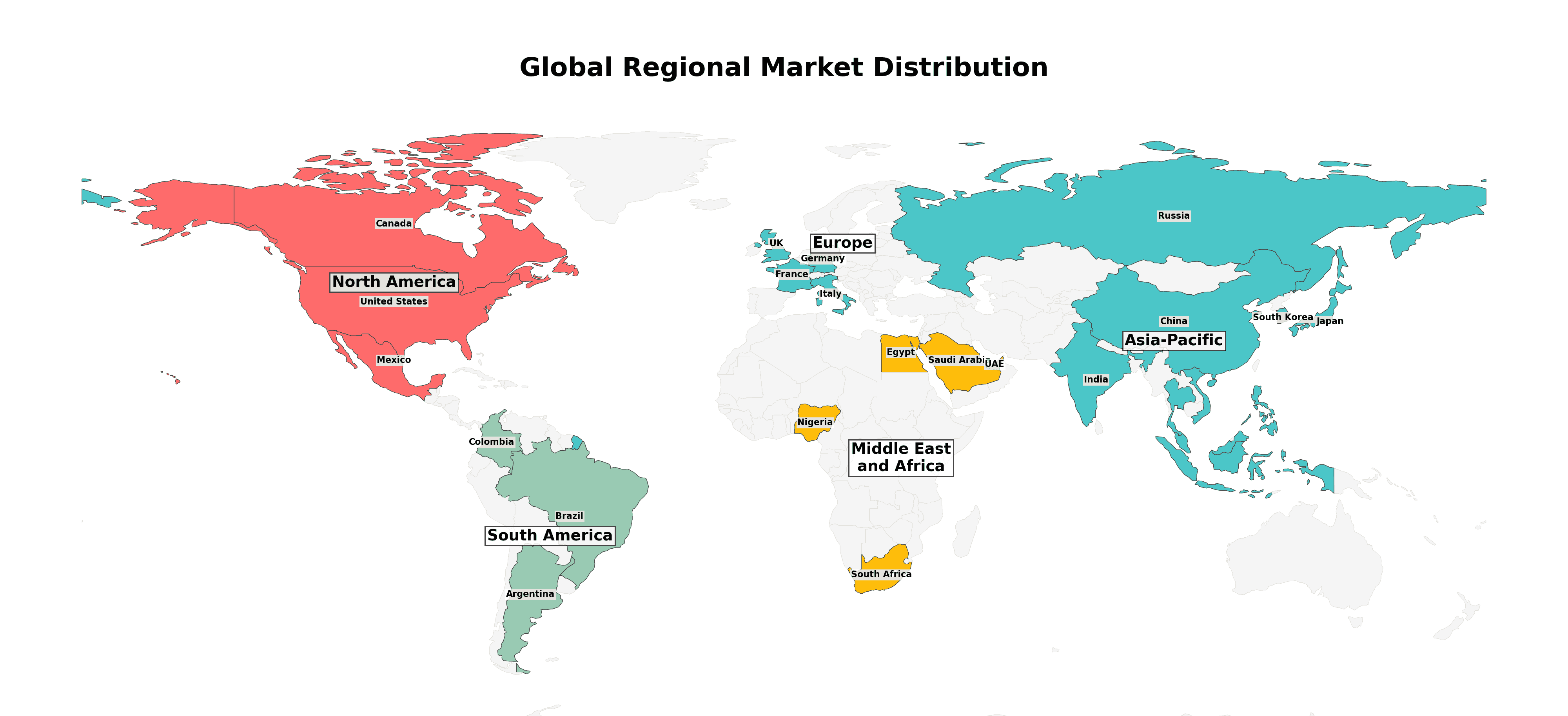

The Asia-Pacific region (APAC) leads the market, accounting for more than 30% of global revenue in 2024, driven by rapid industrialisation, significant semiconductor manufacturing hubs, and aggressive 5G rollouts in China, South Korea, and Japan. Government efforts aimed at promoting semiconductor self-reliance further boost demand. the north America, with the US market valued at US$ 61.5 million in 2024 and expected to to reach US$ 122.3 million by 2030 (CAGR 12.1%), follows closely, fuelled by leadership in AI, high-performance computing, and advanced semiconductor packaging technologies. Glass interposers—advanced materials used in semiconductor packaging—play a crucial role in enabling these innovations. With the help of stringent laws and investments in electric and driverless cars, Europe focuses on automotive electronics and industrial applications. Continuous global market expansion is ensured by the growing demand for small, fast, and energy-efficient devices.

Key Players

- Kiso Micro Co

- Plan Optik AG

- Ushio

- Corning

- 3D Glass Solutions, Inc

- Triton Microtechnologies, Inc

- Other Key Players

Recent Development

Through the Packaging Applications Center of Excellence (PACE), Onto Innovation and LPKF Laser & Electronics SE partnered in 2024 to expedite the mass manufacturing of glass core-based panel-level packages. The goal of this partnership is to satisfy the increasing need for cloud computing, artificial intelligence, and high-performance computing (HPC) applications.

Between 2025 and 2026, AMD plans to use glass substrates in its high-performance system-in-packages (SiPs). Advanced SiPs in data center applications can benefit from glass substrates’ superior flatness, mechanical strength, and thermal characteristics over conventional organic substrates.

Report Scope

The report includes Global & Regional market status and outlook for 2017-2028. Further, the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types, applications. The report also covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price, and Gross Margin 2017-2028 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

|

Attributes |

Details |

|

Segments |

By Type

By Application

|

|

Regional Analysis |

|

|

Key Market Players |

|

|

Report Coverage |

|

Glass Interposers Market Regional Analysis :

- North America:Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

- Europe:Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

- Asia-Pacific:Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

- South America:Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

- Middle East & Africa:Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Drivers

- Miniaturization of Electronic Components: With the growing demand for smaller and more powerful electronic devices, glass interposers are increasingly being used in semiconductor packaging due to their ability to accommodate a large number of components in a compact space. This miniaturization trend drives the need for interposers with superior electrical performance and high-density connections.

- High-Performance Computing and AI Applications: The expansion of high-performance computing (HPC) and artificial intelligence (AI) applications requires cutting-edge packaging technologies to support faster data transfer speeds and higher processing power. Glass interposers, with their superior electrical and thermal properties, offer a key advantage in meeting these needs, thus boosting market growth.

- Advancements in Semiconductor Packaging: Glass interposers are an important part of advanced packaging technologies such as 2.5D and 3D ICs, enabling efficient connections between different chip layers. Their ability to support fine-pitch wiring and improve signal integrity is driving their adoption in the semiconductor industry.

Restraints

- High Manufacturing Costs: One of the major challenges in the glass interposer market is the high cost associated with their production. Manufacturing glass interposers requires specialized equipment and techniques, leading to higher production costs compared to traditional materials like silicon. This could limit their adoption, particularly in price-sensitive markets.

- Complexity in Mass Production: The complex manufacturing process for glass interposers, including the need for precise etching and bonding, makes large-scale production challenging. This can lead to delays in the commercialization of new products and impact the overall supply chain.

- Availability of Alternatives: Although glass interposers offer superior performance, alternatives like silicon interposers and organic substrates are more commonly used due to their lower cost and established manufacturing processes. The competition from these alternatives could limit the market penetration of glass interposers.

Opportunities

- Growing Demand for 5G and Automotive Electronics: The increasing rollout of 5G networks and the rise in demand for automotive electronics (including autonomous driving and electric vehicles) create significant opportunities for the glass interposer market. These sectors require highly reliable, high-performance semiconductor packaging, which glass interposers can provide.

- Integration of New Materials: The combination of glass interposers with emerging materials like advanced semiconductors and photonic devices offers the potential for even more advanced packaging solutions. This could open new opportunities for glass interposers in cutting-edge applications, such as quantum computing, where high performance and low signal loss are critical.

- Strategic Partnerships and Collaborations: Collaborations between semiconductor companies, materials manufacturers, and packaging firms can accelerate the development of cost-effective manufacturing processes for glass interposers. Strategic alliances could also lead to innovations that make glass interposers more widely used in different sectors, such as medical devices or aerospace electronics.

Challenges

- Technical Limitations: While glass interposers offer many benefits, their ability to support very high interconnect densities and thermal management in extreme environments is still a challenge. Researchers are working on overcoming these limitations, but the technology is still evolving.

- Market Education and Acceptance: Many companies in the semiconductor industry have been using traditional packaging materials like silicon and organic substrates for years. Educating stakeholders about the advantages of glass interposers and convincing them to switch to this newer technology can be a slow process, especially when the initial costs are higher.

- Supply Chain Challenges: The production of glass interposers is still a niche segment, and the supply chain for their raw materials (such as specific types of glass) and specialized equipment is not as robust as for more widely used packaging materials. Any disruptions in the supply chain could lead to delays and higher costs.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Glass Interposers Market

- Overview of the regional outlook of the Glass Interposers Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q: What are the key driving factors and opportunities in the Glass Interposers market?

A: Rising demand for high-speed electronics, advancements in 2.5D/3D packaging, and growth in data centers and automotive sectors are key drivers and opportunities.

Q: Which region is projected to have the largest market share?

A: Asia-Pacific is expected to lead the market due to strong semiconductor manufacturing hubs and rapid industrialization.

Q: Who are the top players in the global Glass Interposers market?

A: Key players include Kiso Micro Co, Plan Optik AG, Ushio, Corning, 3D Glass Solutions, Inc, and Triton Microtechnologies, Inc.

Q: What are the latest technological advancements in the industry?

A: Innovations include through-glass via (TGV) formation, integration in fan-out wafer-level packaging (FOWLP), and use in advanced system-in-package (SiP) designs.

Q: What is the current size of the global Glass Interposers market?

A: The market was valued at approximately US$ 234.5 million in 2024 and is projected to reach US$ 478.9 million by 2030.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...