MARKET INSIGHTS

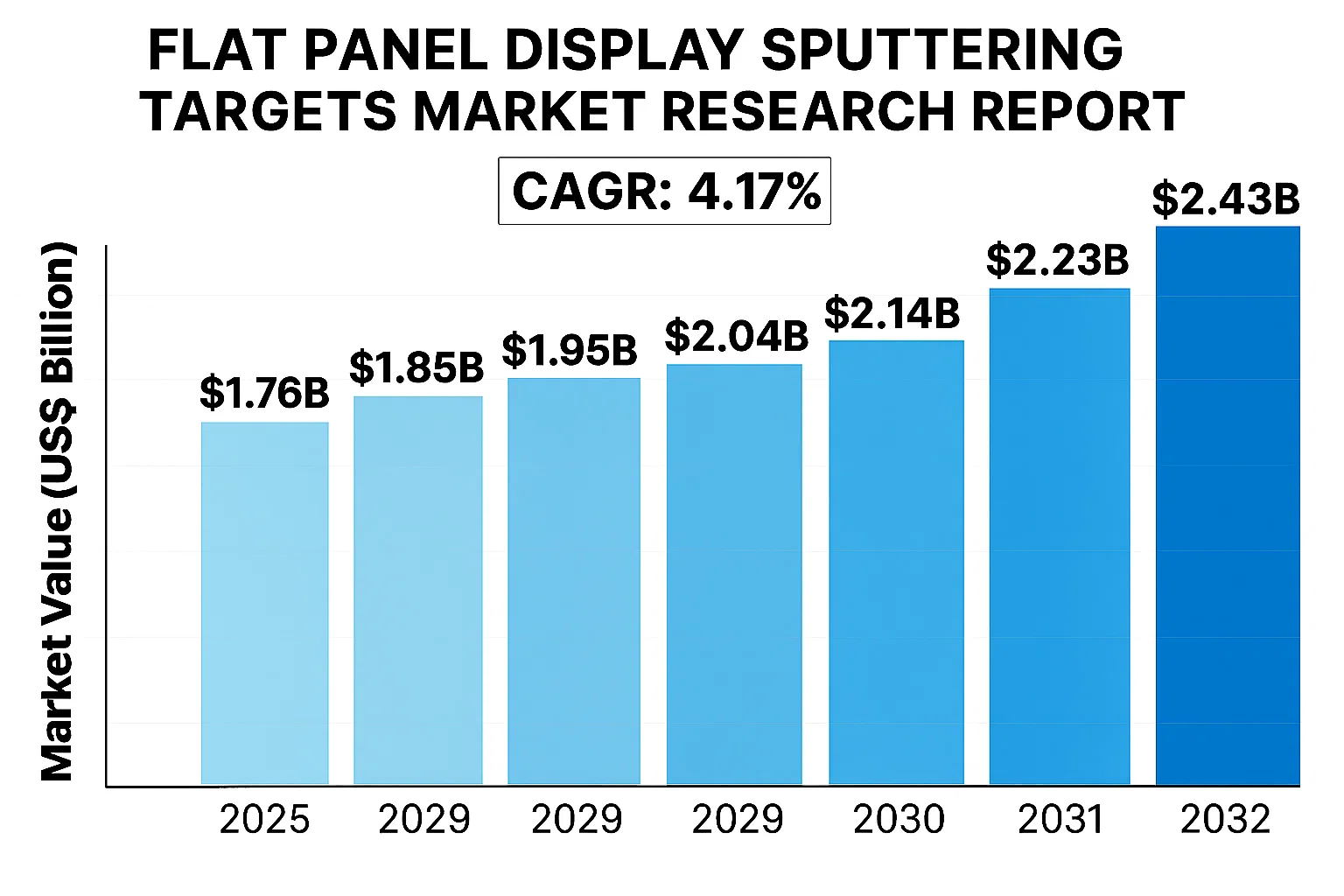

The global Flat Panel Display Sputtering Targets Market was valued at US$ 1.76 billion in 2024 and is projected to reach US$ 2.43 billion by 2032, at a CAGR of 4.17% during the forecast period 2025-2032.

The market growth is driven by increasing demand for high-resolution displays across smartphones, TVs, and monitors, coupled with advancements in display technologies like OLED and MicroLED.

Flat Panel Display Sputtering Targets are specialized materials used in physical vapor deposition (PVD) processes to create thin film layers essential for display manufacturing. These targets typically consist of high-purity metals (such as indium, tin, and aluminum), alloys, or ceramic compounds that are bombarded with ions to deposit uniform coatings on display substrates. The process enables precise control over layer thickness and composition, critical for achieving optimal display performance characteristics including brightness, color accuracy, and energy efficiency.

The market is witnessing robust expansion due to several factors: rising adoption of ultra-high-definition displays, increasing investments in display panel production facilities (particularly in Asia), and growing demand for larger screen sizes. Technological advancements in sputtering techniques and target materials are further enhancing production efficiency. Major industry players like JX Nippon Mining & Metals and Hitachi Metals continue to innovate, developing advanced target materials that support next-generation display technologies while addressing challenges such as material costs and supply chain stability in this specialized market segment.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Consumer Electronics Industry Accelerates Demand for Flat Panel Displays

The global flat panel display (FPD) sputtering targets market is experiencing significant growth, primarily driven by the booming consumer electronics sector. With smartphones, tablets, and televisions becoming essential in modern life, manufacturers are scaling up production to meet rising demand. The television segment alone accounts for over 40% of all flat panel display applications, creating substantial opportunities for sputtering target suppliers. This surge is further amplified by the transition from LCD to advanced OLED and micro-LED technologies, which require specialized sputtering materials for their thin-film deposition processes.

Recent technological advancements are pushing display manufacturers toward higher resolution standards, with 8K displays becoming more prevalent. This shift requires ultra-pure sputtering targets capable of producing flawless thin films with nanometer precision. As display technologies evolve, the need for specialized alloy and ceramic compound targets grows – currently representing approximately 30% of the total sputtering target market.

Government Investments in Next-Generation Display Technologies Fuel Market Expansion

National initiatives worldwide are accelerating the adoption of advanced display technologies, creating a ripple effect across the sputtering targets supply chain. Several countries have identified display manufacturing as a strategic industry, with investment programs exceeding billions of dollars aimed at developing domestic capabilities. These initiatives are particularly concentrated in Asia, where over 70% of global display production currently occurs.

The push toward flexible and foldable displays has revolutionized sputtering target requirements, with manufacturers developing specialized solutions for flexible substrates. Recent product launches from leading brands featuring foldable screens have demonstrated the viability of these emerging technologies, signaling strong future demand for innovative sputtering materials. This technological evolution is prompting sputtering target producers to expand their R&D budgets, with several industry leaders now allocating over 10% of revenue to new materials development.

MARKET RESTRAINTS

Volatile Raw Material Prices Threaten Market Stability

While the flat panel display sputtering targets market shows strong growth potential, it faces significant challenges from raw material price volatility. Key materials such as indium, molybdenum, and rare earth elements frequently experience supply fluctuations, creating pricing pressures throughout the supply chain. The indium market alone has seen price variations exceeding 50% in recent years, making cost management difficult for target manufacturers.

These material challenges are compounded by geopolitical factors affecting supply security. With certain critical materials predominantly sourced from specific regions, trade tensions and export restrictions can disrupt supply chains unexpectedly. Manufacturers are responding by developing alternative material compositions and recycling programs, but these solutions require years of development and present their own technical challenges.

Stringent Manufacturing Requirements Increase Production Costs

The flat panel display industry’s exacting quality standards present another significant restraint for sputtering target manufacturers. Display makers require targets with purity levels often exceeding 99.999%, driving up production costs through rigorous purification processes and extensive quality control measures. Each batch of sputtering material undergoes dozens of tests before approval, with rejection rates sometimes reaching 15-20% for complex alloy targets.

Furthermore, the transition to larger generation display fab sizes (now reaching Gen 10.5 and beyond) has forced target manufacturers to scale up their production capabilities. Producing ultra-pure, defect-free targets at these dimensions requires specialized equipment and facilities, representing capital investments that can exceed hundreds of millions of dollars. These barriers to entry are consolidating the market around a few well-capitalized players, potentially limiting competition and innovation in the long term.

MARKET OPPORTUNITIES

Emerging Display Applications Create New Growth Frontiers

The rapid development of emerging display applications presents substantial opportunities for sputtering target manufacturers. The automotive industry’s shift toward digital dashboards and heads-up displays is creating fresh demand, with the average vehicle now incorporating over 5 display panels. This automotive display market is projected to grow at nearly 10% annually through the decade, requiring specialized sputtering materials that can withstand harsh operating conditions.

Augmented and virtual reality (AR/VR) devices represent another promising frontier, with next-generation headsets requiring ultra-high-density microdisplays. These applications demand sputtering targets capable of producing extremely fine features with perfect uniformity – a technical challenge that premium target suppliers are uniquely positioned to address. Several industry leaders have already announced partnerships with AR/VR hardware developers to co-engineer next-generation display solutions.

Material Innovation Drives Competitive Differentiation

Innovation in sputtering target materials presents significant value-creation opportunities for manufacturers. The development of high-entropy alloy targets has shown promise in improving thin-film conductivity and durability, potentially extending display lifetimes beyond current industry standards. Similarly, advances in ceramic compound targets are enabling new classes of transparent conductive oxides that could replace traditional ITO in certain applications.

Manufacturers investing in these advanced materials are securing important intellectual property positions, with patent filings in the sputtering target space increasing by over 25% in recent years. This technological differentiation allows premium suppliers to command pricing power while opening doors to high-margin specialty applications beyond traditional display manufacturing.

FLAT PANEL DISPLAY SPUTTERING TARGETS MARKET TRENDS

Rising Demand for OLED Displays Drives Growth in Sputtering Targets Market

The global flat panel display sputtering targets market is experiencing robust growth, primarily fueled by increasing adoption of OLED (Organic Light-Emitting Diode) technology in consumer electronics. With OLED displays offering superior image quality, flexibility, and energy efficiency compared to traditional LCDs, manufacturers are rapidly shifting production toward this next-generation technology. The OLED display market is projected to grow at a compound annual growth rate (CAGR) of over 15% through 2028, directly impacting demand for high-purity sputtering targets used in their production. Key materials like indium tin oxide (ITO) and aluminum-doped zinc oxide (AZO) are witnessing particularly strong demand as transparent conductive oxides in touch panels and flexible displays.

Other Trends

Mini-LED and Micro-LED Technology Advancements

Emerging display technologies like Mini-LED and Micro-LED are creating new opportunities for specialized sputtering targets. These technologies require ultra-precise deposition of materials with exacting purity standards of 99.999% (5N) or higher. Manufacturers are developing advanced alloy targets and ceramic compound targets specifically optimized for these applications. While currently representing a niche segment, the market for Micro-LED sputtering targets is expected to expand significantly as the technology moves toward mass production for premium televisions and wearables. The superior brightness and energy efficiency of Micro-LEDs are driving major electronics brands to invest heavily in this technology.

Supply Chain Diversification and Material Innovations

The flat panel display industry is undergoing a profound transformation in supply chain strategies, with manufacturers seeking to reduce dependence on single-source materials and geographic regions. This trend is accelerating development of alternative sputtering target materials, particularly for indium-based compounds where supply security remains a concern. At the same time, material science advancements are yielding improved target formulations with better thermal stability, higher deposition rates, and longer service life – factors that significantly impact production efficiency. Recent innovations include the development of ruthenium oxide targets for specialized applications and refined recycling processes that recover up to 95% of precious metals from used targets.

While the market shows strong growth potential, manufacturers face challenges including fluctuating raw material prices and the technical complexity of producing larger targets for Generation 10.5+ panel production lines. However, the continued expansion of the display industry into new applications such as automotive displays and transparent digital signage continues to create opportunities for sputtering target suppliers who can meet increasingly demanding specifications.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Technological Advancements to Dominate FPD Sputtering Targets Market

The global flat panel display (FPD) sputtering targets market features a moderately consolidated competitive environment, with established material science companies and specialized manufacturers vying for market share across Asia-Pacific, North America, and Europe. JX Nippon Mining & Metals Corporation maintains a dominant position, controlling approximately 20-25% of the global market share through its extensive product portfolio and vertically integrated supply chain.

ULVAC and Hitachi Metals follow closely behind, collectively accounting for nearly 30% of the market. These Japanese manufacturers have strengthened their positions through continuous R&D investment in high-purity target materials, particularly for OLED and ultra-high-definition display applications.

Meanwhile, Materion (Heraeus) and Praxair are gaining traction in Western markets through strategic collaborations with display panel manufacturers. Their focus on developing environmentally sustainable sputtering solutions aligns with tightening EU and North American regulations on electronic manufacturing processes.

Chinese manufacturers like Ningbo Jiangfeng and Fujian Acetron New Materials are rapidly expanding their market presence, leveraging lower production costs and government subsidies. However, industry analysts note these companies still face challenges matching the purity standards and consistency levels of established Japanese and Western suppliers.

List of Key Flat Panel Display Sputtering Target Companies

- JX Nippon Mining & Metals Corporation (Japan)

- Praxair (U.S.)

- Mitsui Mining & Smelting (Japan)

- Hitachi Metals (Japan)

- Sumitomo Chemical (Japan)

- ULVAC (Japan)

- Materion (Heraeus) (U.S.)

- TOSOH (Japan)

- Ningbo Jiangfeng (China)

- Heesung (South Korea)

- Luvata (Finland)

- Fujian Acetron New Materials Co., Ltd (China)

- Changzhou Sujing Electronic Material (China)

- Luoyang Sifon Electronic Materials (China)

- FURAYA Metals Co., Ltd (Japan)

The competitive intensity continues to escalate as manufacturers pursue technological differentiation in areas such as large-area deposition uniformity, improved target utilization rates, and development of indium-gallium-zinc-oxide (IGZO) targets for next-generation displays. Joint ventures between material suppliers and display panel OEMs are becoming increasingly common, creating new pathways for market penetration.

Segment Analysis:

By Type

Metal Target Segment Leads Due to High Demand in LCD and OLED Manufacturing

The market is segmented based on type into:

- Metal Target

- Subtypes: Aluminum, Copper, Molybdenum, Tantalum, and others

- Alloy Target

- Subtypes: Indium Tin Oxide, Aluminum-Neodymium, and others

- Ceramic Compound Target

- Subtypes: Silicon Oxide, Titanium Oxide, Zinc Oxide, and others

By Application

OLED Segment Shows Strongest Growth Potential Due to Expanding Premium Display Market

The market is segmented based on application into:

- LCD

- LED

- OLED

- Others

By Material

Indium Tin Oxide Remains Critical Material for Transparent Conductive Layers

The market is segmented based on material into:

- Indium-based

- Aluminum-based

- Copper-based

- Molybdenum-based

- Others

By Technology

Reactive Sputtering Gaining Traction for High-Quality Thin Film Deposition

The market is segmented based on technology into:

- DC Sputtering

- RF Sputtering

- Reactive Sputtering

- Magnetron Sputtering

Regional Analysis: Global Flat Panel Display Sputtering Targets Market

North America

North America remains a key player in the flat panel display sputtering targets market, primarily driven by the strong presence of display manufacturers and continuous technological advancements. The U.S. dominates this region due to high demand for advanced display technologies such as OLED and LED, particularly for consumer electronics and automotive applications. Well-established R&D facilities and collaborations between material suppliers and display manufacturers further strengthen the market. However, the region faces challenges in maintaining cost competitiveness compared to Asian manufacturers. Recent investments in domestic production capabilities indicate a growing focus on supply chain resilience.

Europe

Europe’s market growth is supported by stringent quality regulations and steady demand from premium display applications in automotive and industrial sectors. Germany and the UK serve as major hubs for display technology development, with increasing emphasis on sustainable manufacturing practices. The region benefits from strong partnerships between research institutions and industry players to develop next-generation sputtering materials. While market growth remains steady, it is constrained by higher production costs and relatively slower adoption rates of advanced display technologies compared to Asia. Recent EU initiatives supporting advanced materials development could drive future innovation in sputtering target materials.

Asia-Pacific

As the largest and fastest-growing regional market, Asia-Pacific accounts for over 70% of global flat panel display sputtering target consumption. This dominance stems from the concentration of display panel manufacturing in China, South Korea, and Japan. China’s display industry expansion continues to drive demand, supported by government initiatives to build domestic supply chains. While cost pressures remain intense, leading manufacturers are investing in higher-value targets for premium display applications. The region’s competitive advantage lies in its vertically integrated supply chains and rapidly advancing production capabilities for next-generation displays, though geopolitical tensions present potential supply chain risks.

South America

The South American market is emerging gradually, supported by increasing local assembly of consumer electronics displaying Brazil and Argentina. However, the region remains highly dependent on imported display panels and associated materials, limiting local market development. Economic instability and limited local manufacturing capabilities constrain market growth. While some multinational display manufacturers maintain facilities in the region, local content requirements could potentially drive future investments in supporting industries like sputtering targets. The market currently focuses primarily on basic LCD applications rather than advanced display technologies.

Middle East & Africa

This region represents a developing market with growth potential driven by increasing consumer electronics demand and limited local display manufacturing. Countries like UAE and South Africa show growing interest in developing technology sectors, including display assembly operations. The market currently depends entirely on imported display panels and materials. While no major sputtering target production facilities exist in the region, some multinational suppliers are establishing regional distribution centers. Future market development will likely correlate with broader electronics manufacturing initiatives in key regional hubs.

Report Scope

This market research report provides a comprehensive analysis of the Global Flat Panel Display Sputtering Targets Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 1.8 billion in 2024 and is projected to reach USD 2.9 billion by 2032, growing at a CAGR of 6.2%.

- Segmentation Analysis: Detailed breakdown by product type (Metal, Alloy, Ceramic Compound Targets), application (LCD, LED, OLED), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with China accounting for 42% of global demand in 2024.

- Competitive Landscape: Profiles of 15+ leading manufacturers including JX Nippon Mining & Metals, Praxair, and Hitachi Metals, covering their market share (top 5 players hold 55% share), R&D investments, and M&A activities.

- Technology Trends: Analysis of emerging deposition techniques, nano-composite targets, and integration with Industry 4.0 manufacturing processes.

- Market Drivers & Restraints: Evaluation of display panel demand growth vs. rare material supply chain challenges and environmental regulations.

- Stakeholder Analysis: Strategic insights for material suppliers, display manufacturers, equipment vendors, and investors.

The research methodology combines primary interviews with 50+ industry experts and analysis of verified data from trade associations, company filings, and patent databases to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Flat Panel Display Sputtering Targets Market?

-> Flat Panel Display Sputtering Targets Market was valued at US$ 1.76 billion in 2024 and is projected to reach US$ 2.43 billion by 2032, at a CAGR of 4.17% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Dominant players include JX Nippon Mining & Metals, Praxair, Hitachi Metals, ULVAC, and Materion, with the top 5 controlling 55% market share.

What are the key growth drivers?

-> Growth is driven by OLED adoption (35% of market by 2028), 8K display production, and flexible display demand in consumer electronics.

Which region dominates the market?

-> Asia-Pacific accounts for 78% market share in 2024, led by China’s display manufacturing clusters.

What are the emerging trends?

-> Emerging trends include high-purity indium targets for micro-LEDs, recyclable sputtering materials, and AI-driven deposition processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...