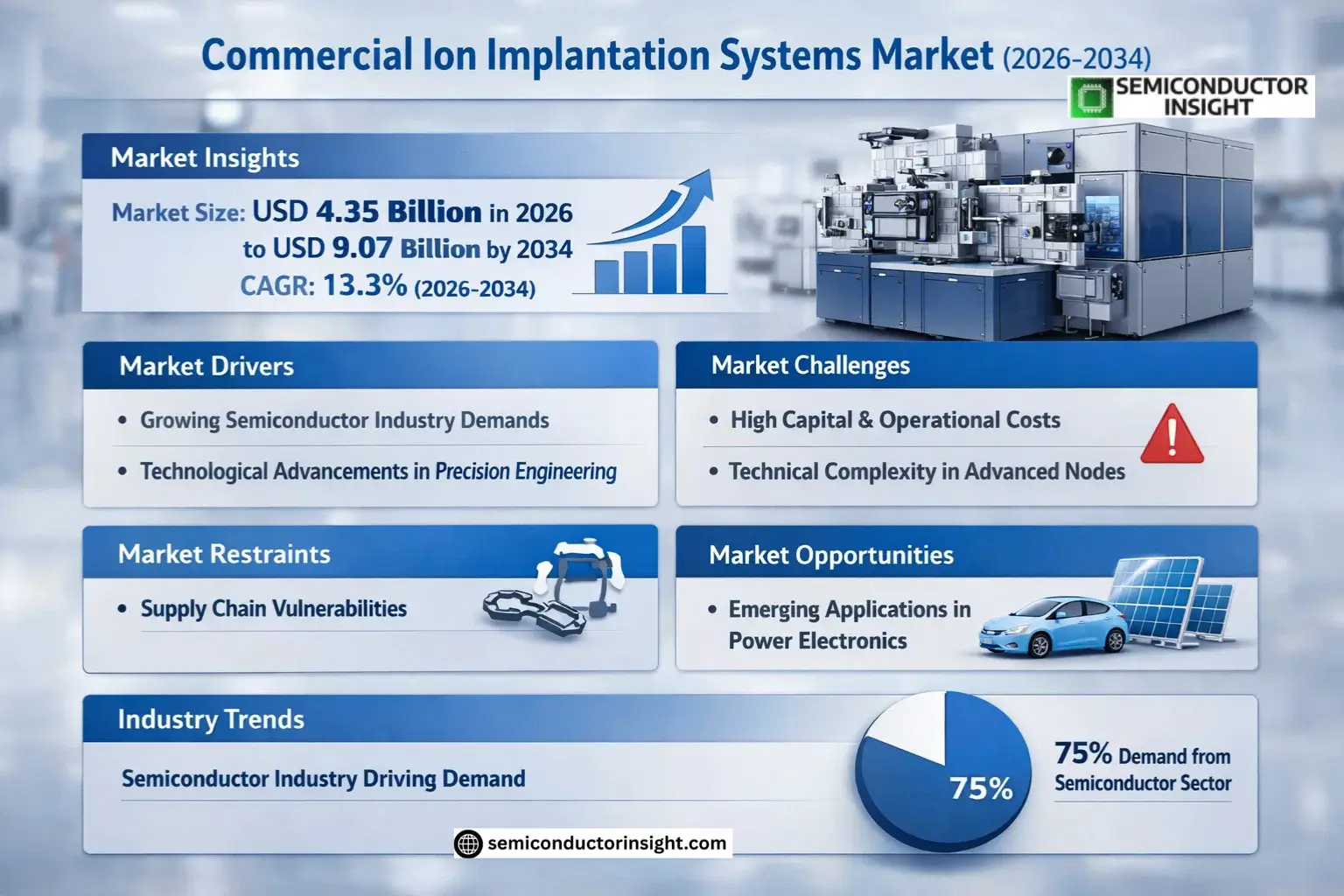

Market Insights

Global Commercial Ion Implantation Systems Market size was valued at USD 3.86 billion in 2025. The market is projected to grow from USD 4.35 billion in 2026 to USD 9.07 billion by 2034, exhibiting a CAGR of 13.3% during the forecast period.

Commercial ion implantation systems are specialized semiconductor manufacturing equipment used to modify the electrical properties of materials by implanting ions into substrates such as silicon wafers. These systems play a critical role in semiconductor fabrication, enabling precise doping processes essential for integrated circuits, MEMS devices, and photovoltaic cells.

The market growth is driven by increasing demand for advanced semiconductor devices, particularly in applications like AI, IoT, and 5G technologies. While the U.S. remains a key market due to its strong semiconductor manufacturing base, China’s rapid expansion in chip production is creating significant opportunities. However, supply chain constraints and high capital costs pose challenges for smaller manufacturers looking to adopt these systems.

MARKET DRIVERS

Growing Semiconductor Industry Demands

Global semiconductor industry’s rapid expansion is a key driver for the Commercial Ion Implantation Systems Market. With semiconductor manufacturers requiring precise doping processes for advanced chip fabrication, demand for ion implantation systems has grown by approximately 18% annually. The need for high-performance chips in AI, 5G, and IoT applications further accelerates this trend.

Technological Advancements in Precision Engineering

Recent innovations in beam current stability and dose control have enhanced the capabilities of commercial ion implantation systems. Manufacturers are investing in cluster tool compatibility and single-wafer processing solutions, with system accuracy now reaching sub-nanometer precision levels. The market has seen a 25% increase in demand for multi-species implantation systems since 2022.

Government initiatives supporting domestic semiconductor production in the U.S., EU, and Asia-Pacific are creating additional growth opportunities for commercial ion implantation system providers.

MARKET CHALLENGES

High Capital and Operational Costs

Commercial ion implantation systems represent a significant capital expenditure, with advanced systems costing between USD 3-10 million per unit. The operational costs, including maintenance and specialized operator training, add to the total cost of ownership. This creates a high barrier to entry for smaller semiconductor fabrication facilities.

Other Challenges

Technical Complexity in Advanced Nodes

As semiconductor nodes shrink below 5nm, ion implantation systems face increasing challenges in maintaining uniformity and preventing wafer damage. The precision requirements for ultra-shallow junctions and 3D structures push the limits of current technology.

MARKET RESTRAINTS

Supply Chain Vulnerabilities

Commercial Ion Implantation Systems Market faces supply chain constraints for critical components like ion sources and high-voltage power supplies. Lead times for certain systems have extended to 9-12 months due to semiconductor component shortages, impacting market growth projections by an estimated 8-10% annually.

MARKET OPPORTUNITIES

Emerging Applications in Power Electronics

The growing demand for power semiconductors in electric vehicles and renewable energy systems is creating new opportunities for commercial ion implantation systems. These applications require specialized doping profiles for SiC and GaN devices, driving a 30% increase in system customization requests since 2023.

Commercial Ion Implantation Systems Market Trends

Semiconductor Industry Driving Demand

The semiconductor industry remains the primary driver for Commercial Ion Implantation Systems, accounting for over 75% of total demand. These systems are critical for doping semiconductors with precise ion concentrations to modify electrical properties. Leading manufacturers are investing in advanced systems capable of handling smaller node processes below 7nm.

Other Trends

Medium-Current Implanter Segment Growth

Medium-current implanters are gaining market share due to their versatility in handling multiple doping applications across different semiconductor types. This segment is particularly favored for memory chip production where balanced implantation depth and dose control are essential.

Regional Market Shifts

Asia-Pacific continues to dominate the Commercial Ion Implantation Systems market, with China, Taiwan and South Korea representing over 60% of global demand. The region’s semiconductor manufacturing expansion and government support for domestic chip production are key growth factors. Meanwhile, North America maintains strong R&D investments in next-generation implantation technologies.

Other Trends

Equipment Innovation Focus

Major players like Applied Materials and Axcelis Technologies are developing implantation systems with improved beam uniformity and energy efficiency. Recent advancements include hybrid systems combining multiple implantation technologies to address diverse semiconductor manufacturing requirements.

Supply Chain Optimization

Commercial Ion Implantation Systems Market is seeing increased vertical integration as manufacturers seek to secure critical components. This trend responds to semiconductor industry demands for more stable equipment supply chains and shorter lead times for system maintenance and upgrades.

COMPETITIVE LANDSCAPE

Key Industry Players

Global ion implantation systems market dominated by semiconductor equipment giants and specialized manufacturers

Commercial Ion Implantation Systems Market is consolidated, with the top five players accounting for a significant revenue share in 2025. Applied Materials (AMAT) and Axcelis Technologies lead the market with their comprehensive product portfolios and strong presence across semiconductor fabrication facilities worldwide. These market leaders have maintained dominance through continuous R&D investments in advanced implantation technologies for sub-7nm nodes and emerging memory applications.

Specialized manufacturers like Nissin Ion Equipment and Advanced Ion Beam Technology (AIBT) compete through niche high-energy implantation solutions, particularly for power devices and MEMS applications. Chinese players such as CETC Electronics Equipment and Kingstone Semiconductor are gaining traction in domestic semiconductor fabs, supported by government initiatives to strengthen local semiconductor supply chains. The market also features several Japanese precision engineering firms with strong capabilities in ion beam technologies.

List of Key Commercial Ion Implantation Systems Companies Profiled

- AMAT (Applied Materials)

- Axcelis Technologies

- Sumitomo Heavy Industries

- Nissin Ion Equipment

- Advanced Ion Beam Technology (AIBT)

- CETC Electronics Equipment

- ULVAC Technologies

- Kingstone Semiconductor

- Intevac

- IBS (Ion Beam Services)

- Semequip

- AccuBeam

- Rena Technologies

- Innovion Corporation

- Pegasus Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Medium-Current Implanter dominates with superior adoption in mainstream semiconductor manufacturing:

|

| By Application |

|

Semiconductor Industry drives extensive adoption with critical process requirements:

|

| By End User |

|

Foundries represent the core demand segment with intensive production needs:

|

| By Technology Node |

|

Advanced Nodes (<28nm) show strongest growth potential:

|

| By System Configuration |

|

Cluster Systems gain prominence in advanced fabs:

|

Regional Analysis: Global Commercial Ion Implantation Systems Market

China’s SMIC and Taiwan’s TSMC lead in adopting cluster tool architectures combining implantation with etch and deposition modules, driving demand for advanced systems with sub-10nm process capabilities and AI-based beam control.

Korea’s semiconductor belt spanning Pyeongtaek to Hwaseong concentrates over 40% of regional implantation capacity, with Samsung deploying self-calibrating implanters featuring real-time dopant profile monitoring through integrated machine learning algorithms.

Japan’s collaboration between equipment makers like Nissin Electric and material suppliers develops novel beamline designs optimized for silicon carbide and gallium nitride power devices, addressing automotive electrification needs.

Southeast Asia emerges as secondary hub with Singapore and Malaysia hosting backend implantation services and specialty foundries utilizing refurbished mid-range implanters for analog and mixed-signal IC production.

North America

The North American Commercial Ion Implantation Systems Market thrives on advanced research facilities and specialized compound semiconductor production. The U.S. leads in developing plasma doping technologies for 3D IC packaging, with major fabless companies driving demand for ultra-low energy implanters. Defense applications stimulate needs for radiation-hardened implantation processes, while national semiconductor initiatives encourage equipment upgrades among domestic IDMs. Canada’s photonics industry creates niche demand for precise dopant placement in optoelectronic devices.

Europe

Europe maintains strong positions in automotive and industrial power semiconductors requiring robust ion implantation solutions. Germany’s automotive chipmakers favor high-voltage implanters for silicon carbide devices, while France’s research institutes pioneer quantum computing applications using single-ion implantation techniques. The EU Chips Act accelerates equipment investments, particularly in MEMS and sensor manufacturing clusters across the Dresden-Nanterre innovation corridor.

Middle East & Africa

The region shows emerging potential with Saudi Arabia’s semiconductor initiatives and Israel’s specialized foundries focusing on medical device applications. Investments in technology transfer programs facilitate localized maintenance capabilities for implantation systems, while sovereign wealth funds explore partnerships with major equipment manufacturers to establish regional service hubs.

South America

Brazil leads regional adoption through its electronics manufacturing incentives, primarily utilizing mid-range implantation systems for discrete semiconductors. Argentina’s nuclear technology sector drives specialized demand for high-energy implanters in radiation detector production, while regional universities collaborate on developing compact ion sources for research applications.

Report Scope

This market research report provides a comprehensive analysis of the Commercial Ion Implantation Systems Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of ion implantation systems in powering advancements across industries such as semiconductors, photovoltaics, and electronic devices.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Commercial Ion Implantation Systems Market?

-> Commercial Ion Implantation Systems Market size was valued at USD 3.86 billion in 2025. The market is projected to grow from USD 4.35 billion in 2026 to USD 9.07 billion by 2034, exhibiting a CAGR of 13.3% during the forecast period.

Which key companies operate in Commercial Ion Implantation Systems Market?

-> Key players include AMAT (Applied Materials), Axcelis Technologies, Sumitomo Heavy Industries, Nissin Ion Equipment, Advanced Ion Beam Technology (AIBT), CETC Electronics Equipment, ULVAC Technologies, Kingstone Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for semiconductors, advancements in photovoltaic technology, and increasing adoption of electronic devices.

Which region dominates the market?

-> Asia is the dominant market, with China leading in terms of market size and growth potential.

What are the emerging trends?

-> Emerging trends include development of high-current and high-energy implanters, integration of AI in semiconductor manufacturing, and sustainable fabrication techniques.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...