MARKET INSIGHTS

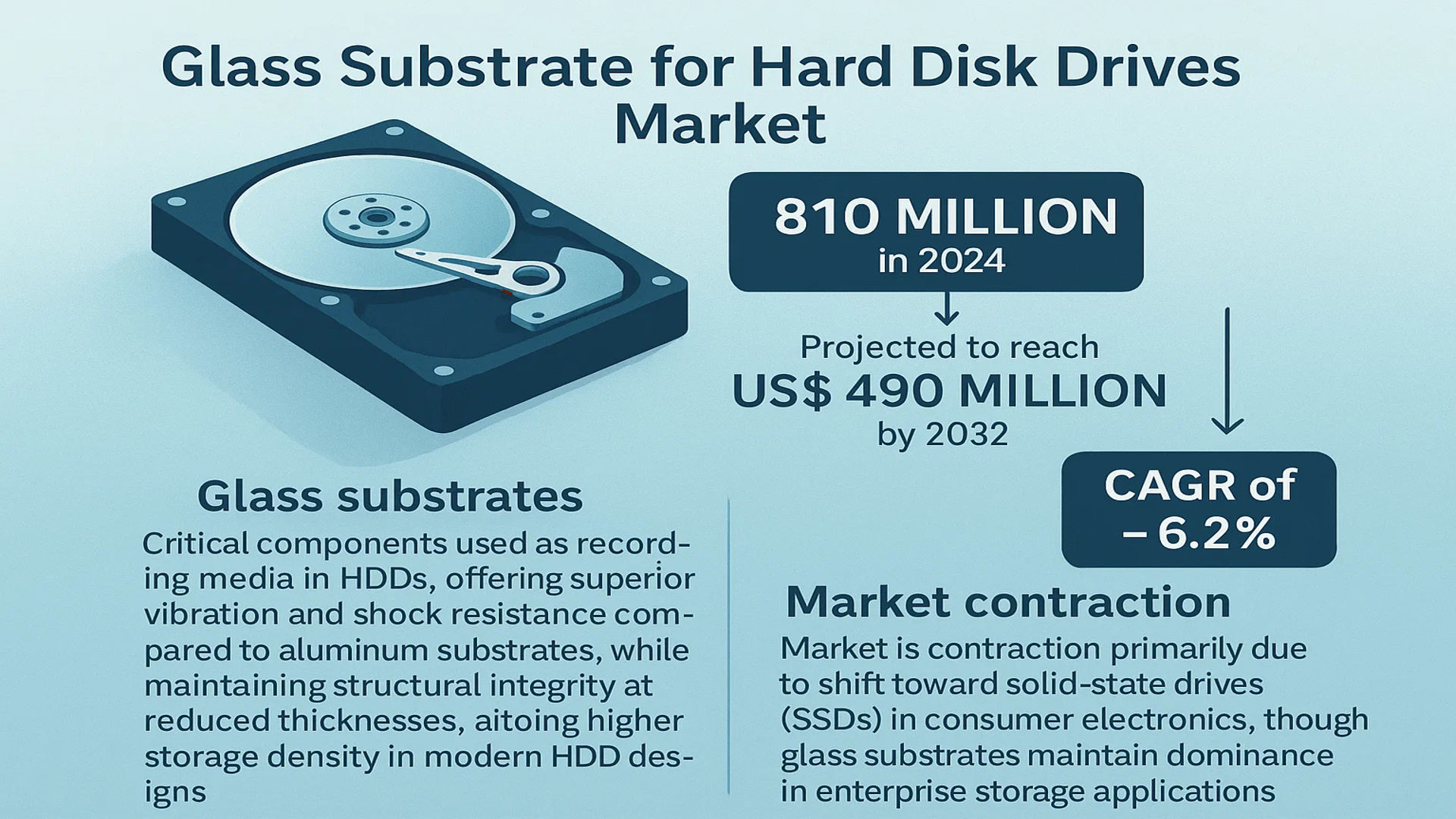

The global Glass Substrate for Hard Disk Drives Market was valued at 810 million in 2024 and is projected to reach US$ 490 million by 2032, at a CAGR of -6.2% during the forecast period.

Glass substrates are critical components used as recording media in hard disk drives (HDDs). These substrates offer superior vibration and shock resistance compared to traditional aluminum substrates, while maintaining structural integrity even at reduced thicknesses. This enables higher storage density and increased capacity in modern HDD designs.

The market is facing contraction primarily due to the shift toward solid-state drives (SSDs) in consumer electronics, though glass substrates maintain dominance in enterprise storage applications. Hoya Corporation currently holds 100% market share in 2.5-inch glass substrates while competing with aluminum substrates in the 3.5-inch segment. The growing demand for high-capacity storage in data centers and cloud infrastructure continues to sustain demand for glass-based HDD solutions, particularly for near-line storage applications where cost-per-terabyte remains crucial.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Demand in Data Centers to Drive Glass Substrate Adoption

The exponential growth of cloud computing and data storage requirements is accelerating demand for high-capacity hard disk drives (HDDs), where glass substrates play a crucial role. As global data generation surpasses 150 zettabytes annually, enterprises are expanding their data center infrastructure, with HDDs remaining the preferred solution for cost-efficient, bulk storage. Glass substrates offer superior stability compared to traditional aluminum, enabling higher areal density and improved vibration resistance—critical factors for enterprise-grade storage solutions. While SSDs dominate high-speed applications, the cost-per-terabyte advantage of HDDs ensures sustained demand in data centers, where over 90% of nearline storage still relies on hard disk technology.

Technological Advancements in Substrate Manufacturing to Boost Market Growth

Recent innovations in glass substrate manufacturing are addressing key challenges in HDD capacity scaling. Advanced polishing techniques now achieve sub-nanometer surface roughness, allowing for tighter head-disk spacing and increased data density. The market leader has demonstrated 2TB platters using next-generation glass substrates, representing a 25% density improvement over previous generations. Such advancements are critical as HDD manufacturers target 50TB+ capacities by 2030. Furthermore, the development of thermal-assist recording (TAR) and microwave-assist recording (MAMR) technologies creates complementary demand for glass substrates that can withstand higher operational temperatures without deformation.

MARKET RESTRAINTS

Accelerating SSD Adoption in Consumer Electronics to Constrain Market Growth

The rapid displacement of HDDs by SSDs in consumer devices presents significant headwinds for glass substrate demand. With SSD prices declining approximately 15% annually and capacities exceeding 4TB in mainstream laptops, the traditional 2.5-inch HDD market—which accounts for nearly 100% of glass substrate usage in consumer devices—is shrinking rapidly. The notebook HDD market has contracted at a 22% CAGR since 2020, while gaming consoles and premium PCs have almost completely transitioned to flash storage. This shift reduces the addressable market for glass substrate manufacturers, particularly as consumer electronics represented over 30% of global HDD shipments just five years ago.

MARKET OPPORTUNITIES

Emerging Heat-Assisted Magnetic Recording Technologies to Create New Growth Avenues

The transition to heat-assisted magnetic recording (HAMR) presents a transformative opportunity for glass substrate manufacturers. HAMR technology requires substrates with exceptional thermal stability—a characteristic where glass outperforms aluminum by maintaining structural integrity at the 400-450°C operating temperatures. As major HDD manufacturers begin volume production of 30TB+ drives using HAMR, the technology is projected to capture over 60% of the high-capacity HDD market by 2028. The specialized requirements of HAMR allow glass substrate producers to command premium pricing, with current prototypes demonstrating 30% higher thermal resistance than conventional materials.

MARKET CHALLENGES

Monopolistic Market Structure Creates Supply Chain Vulnerabilities

The glass substrate market faces unique challenges due to its concentrated supply base, with a single manufacturer controlling 100% of the 2.5-inch substrate supply. This creates significant supply chain risks, as any disruption in production could impact the entire HDD industry. The technical complexity of manufacturing ultra-flat, defect-free glass substrates requires specialized facilities with an average construction cost exceeding $500 million, creating high barriers to new market entry. Additionally, the three-year qualification process for new substrates means HDD manufacturers maintain limited flexibility to switch suppliers, exacerbating supply chain rigidity.

Other Challenges

Material Science Limitations

Current glass formulations approach physical limits in thickness reduction, with 0.5mm substrates representing the practical minimum for maintaining mechanical stability. This constrains future capacity gains that require thinner platters for increased platter counts per drive.

Skilled Labor Shortages

The niche expertise required for precision glass manufacturing creates talent acquisition challenges, particularly as the semiconductor industry competes for similar materials engineering specialists. Regional workforce development programs struggle to keep pace with the specialized training requirements.

GLASS SUBSTRATE FOR HARD DISK DRIVES MARKET TRENDS

Growing Demand for High-Capacity Storage Solutions Drives Market Growth

The global glass substrate for hard disk drives (HDDs) market is witnessing a shift in demand dynamics, primarily fueled by the exponential growth in data generation. With cloud computing, big data analytics, and enterprise storage solutions requiring larger and more reliable storage mediums, glass substrates are increasingly favored for their superior mechanical stability and thin-profile capabilities. Data centers alone consume over 60% of global HDD production, with the trend toward higher areal density storage solutions accelerating adoption. While the market faces competition from SSDs in consumer electronics, the cost-efficiency and capacity advantages of HDDs sustain demand, particularly in nearline and archival storage applications.

Other Trends

Monopoly of Hoya in the Supply Chain

Hoya Corporation remains the sole global supplier of glass substrates for HDDs, controlling 100% of the niche 2.5-inch HDD segment. However, the 3.5-inch HDD market, which constitutes a larger share of enterprise storage and data center applications, still predominantly uses aluminum substrates. The concentration of supply with a single manufacturer introduces supply chain risks, but Hoya’s advanced glass fabrication technologies—such as improved thermal resistance and vibration damping—reinforce its market dominance. Manufacturers are evaluating alternative materials, but no viable alternatives currently match glass’s performance in high-performance HDDs.

Technological Innovations in Substrate Design

The push for higher areal density (expected to exceed 5TB per platter by 2030) is driving innovations in glass substrate manufacturing. Thinner glass substrates (below 0.5mm thickness) reduce weight and enable multi-platter HDD designs, increasing storage capacity per unit. Additionally, advancements in surface polishing and coating technologies enhance magnetic layer adhesion, improving data reliability. Recent developments also focus on integrating glass substrates with heat-assisted magnetic recording (HAMR) and microwave-assisted magnetic recording (MAMR) technologies, which demand substrates capable of withstanding higher operational temperatures without deformation.

COMPETITIVE LANDSCAPE

Key Industry Players

HOYA Dominates the Market While Aluminum Substitutes Pose Challenges

The global glass substrate for HDD market exhibits a highly concentrated competitive landscape, with Japan’s HOYA Corporation maintaining an undisputed monopoly position. According to industry analysis, HOYA commands 100% market share in 2.5-inch glass substrates – a remarkable dominance stemming from its proprietary manufacturing technologies and decades-long expertise in precision glass engineering.

The competitive dynamics are shaped by the gradual transition from aluminum to glass substrates in 3.5-inch HDDs. While aluminum remains the dominant material in this segment due to cost advantages, glass substrates are gaining traction in high-value applications where vibration resistance and data density are paramount. This shift presents both opportunities and challenges for market players.

Emerging competitive pressure comes from alternative storage technologies rather than direct competitors. The rapid adoption of SSDs in consumer electronics has compelled HDD manufacturers to focus on the enterprise segment where glass substrates demonstrate superior value. Consequently, HOYA has intensified its R&D investments to develop next-generation glass substrates with enhanced thermal stability and thinner profiles to maintain its competitive edge.

List of Key Glass Substrate Companies Profiled

- HOYA Corporation (Japan) – The sole manufacturer of glass substrates for HDDs globally

- Western Digital (U.S.) – Major HDD manufacturer utilizing glass substrates

- Seagate Technology (Ireland) – Key consumer of glass substrates for enterprise HDDs

- Toshiba Electronic Devices & Storage Corporation (Japan) – Significant player in the HDD ecosystem

- Showa Denko Materials (Japan) – Supplier of aluminum substrates competing with glass solutions

The market’s future competitiveness will likely be determined by technological innovations in substrate materials and the ongoing battle between HDDs and SSDs for different storage applications. While HOYA’s position appears unshakable in the near term, the company must continue to innovate to maintain relevance as the storage industry evolves.

Segment Analysis:

By Type

2.5-Inch Segment Dominates Market Due to High Adoption in Portable Storage Devices

The market is segmented based on type into:

- 2.5 inch

- Subtypes: Standard thickness, Ultra-thin variants

- 3.5 inch

- Subtypes: Enterprise-grade, High-capacity variants

By Application

Data Center Segment Leads Due to Growing Demand for Bulk Storage Solutions

The market is segmented based on application into:

- Data Center

- Enterprise Storage Solutions

- PCs and Consumer Electronics

- Subtypes: Laptops, Gaming consoles, External storage devices

By Manufacturing Process

Polished Glass Substrates Gain Traction for Enhanced Magnetic Layer Adhesion

The market is segmented based on manufacturing process into:

- Polished Glass Substrates

- Textured Glass Substrates

- Coated Glass Substrates

By Storage Capacity

High-Capacity Variants See Increased Demand for Enterprise Applications

The market is segmented based on storage capacity into:

- Below 1TB

- 1TB – 5TB

- Above 5TB

Regional Analysis: Glass Substrate for Hard Disk Drives Market

Asia-Pacific

Asia-Pacific dominates the glass substrate for HDDs market, accounting for the largest revenue share due to the high concentration of data centers, enterprise storage providers, and electronics manufacturing hubs. Countries like China, Japan, and South Korea drive demand, supported by their strong semiconductor industries and advanced HDD manufacturing capabilities. Japan’s dominance is reinforced by Hoya Corporation, the sole global manufacturer of glass substrates for HDDs. Meanwhile, China’s expanding cloud computing sector fuels long-term demand for high-capacity storage solutions. While SSD adoption is growing in consumer electronics, HDDs remain crucial for cost-sensitive data centers and enterprise storage applications in the region.

North America

North America represents a significant market for glass substrates in HDDs, primarily due to the strong presence of hyperscale data centers and enterprise storage providers. The U.S. leads the region, with companies like Seagate and Western Digital relying on glass substrates for high-performance storage solutions. Demand is bolstered by cloud computing expansion and AI-driven data storage needs, though SSDs continue gaining traction in consumer devices. While aluminum substrates dominate 3.5-inch HDD production, glass substrates maintain steady demand for 2.5-inch HDDs used in enterprise applications. Government and private sector investments in data infrastructure further support market stability.

Europe

Europe shows steady but declining demand for glass substrates in HDDs, with demand primarily centered in enterprise storage and data center applications. The region’s strict environmental regulations influence material choices, but HDD manufacturers continue using glass substrates for their durability and performance benefits. The shift toward sustainable data centers and renewable energy-integrated storage solutions poses both challenges and opportunities for HDD adoption. Germany and the U.K. account for the highest demand, though overall market growth is tempered by rising SSD preferences in consumer and commercial sectors.

South America

The market in South America remains nascent, driven mainly by expanding data center investments in Brazil and Argentina. However, economic constraints and limited local HDD manufacturing result in lower glass substrate adoption compared to other regions. Most demand stems from imported enterprise storage solutions, while consumer electronics increasingly favor SSDs. Despite lower penetration, the long-term outlook remains cautiously optimistic as digital transformation initiatives gain momentum.

Middle East & Africa

The Middle East & Africa exhibit emerging demand for glass substrates in HDDs, primarily driven by data center growth in the UAE, Saudi Arabia, and South Africa. While the market remains small, increasing cloud adoption and smart city developments present growth opportunities. However, infrastructure limitations and SSD preference in high-end electronics restrict broader HDD adoption, keeping glass substrate demand subdued in the near term.

Report Scope

This market research report provides a comprehensive analysis of the global Glass Substrate for Hard Disk Drives market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 810 million in 2024 and is projected to decline to USD 490 million by 2032, reflecting a CAGR of -6.2%.

- Segmentation Analysis: Detailed breakdown by product type (2.5-inch and 3.5-inch substrates), application (data centers, enterprise storage, consumer electronics), and end-user industry to identify niche opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific dominating due to high HDD manufacturing concentration.

- Competitive Landscape: HOYA Corporation holds 100% market share in 2.5-inch glass substrates and partial share in 3.5-inch segments. Analysis covers their production capacity and technological developments.

- Technology Trends: Assessment of substrate thinning technologies, vibration resistance improvements, and material innovations to support higher HDD areal densities.

- Market Drivers & Restraints: Evaluation of cloud storage demand (projected to grow at 19% CAGR) versus SSD substitution in consumer devices (SSD adoption >60% in new laptops).

- Stakeholder Analysis: Strategic insights for HDD manufacturers, substrate suppliers, data center operators, and investors on capacity planning and technology roadmaps.

The report employs primary interviews with HOYA’s technical teams and secondary data from HDD manufacturers like Seagate and Western Digital, ensuring validated market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Glass Substrate for Hard Disk Drives Market?

-> Glass Substrate for Hard Disk Drives Market was valued at 810 million in 2024 and is projected to reach US$ 490 million by 2032, at a CAGR of -6.2% during the forecast period.

Which company dominates the glass substrate market for HDDs?

-> HOYA Corporation maintains a monopoly in 2.5-inch glass substrates (100% share) and partial presence in 3.5-inch segments.

What are the key growth drivers despite market decline?

-> Sustained demand from data centers (growing at 15% annually) and enterprise storage requiring cost-effective high-capacity solutions.

Which application segment uses the most glass substrates?

-> Data centers account for 58% of glass substrate consumption, followed by enterprise storage (32%) in 2024.

What technological trends are shaping the market?

-> Development of ultra-thin substrates (below 0.5mm) and thermal-stable glass formulations to support HAMR (Heat-Assisted Magnetic Recording) technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...