MARKET INSIGHTS

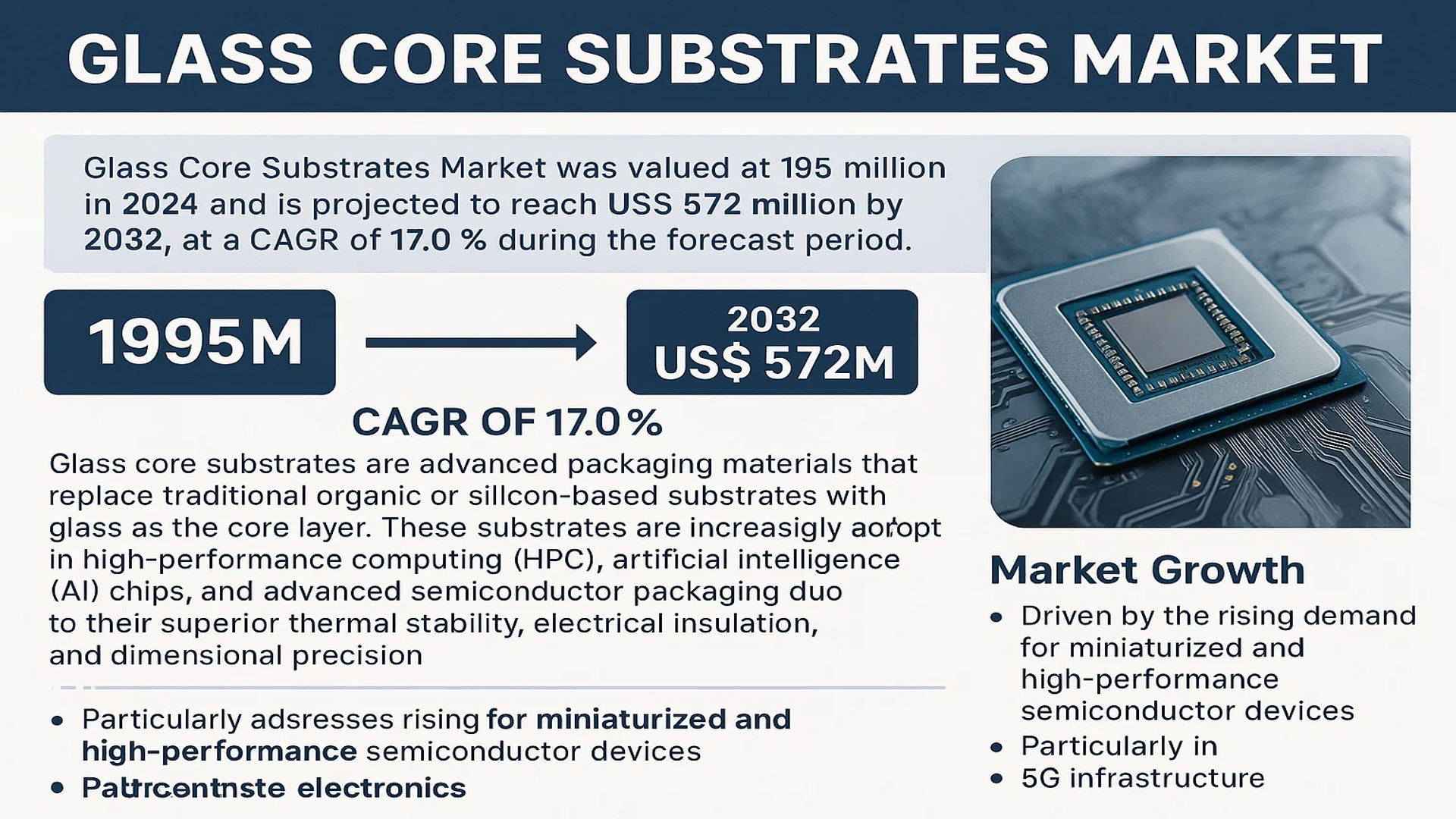

The global Glass Core Substrates Market was valued at 195 million in 2024 and is projected to reach US$ 572 million by 2032, at a CAGR of 17.0% during the forecast period.

Glass core substrates are advanced packaging materials that replace traditional organic or silicon-based substrates with glass as the core layer. These substrates are increasingly adopted in high-performance computing (HPC), artificial intelligence (AI) chips, and advanced semiconductor packaging due to their superior thermal stability, electrical insulation, and dimensional precision.

The market growth is driven by the rising demand for miniaturized and high-performance semiconductor devices, particularly in data centers, 5G infrastructure, and automotive electronics. Additionally, technological advancements in wafer-level packaging (WLP) and panel-level packaging (PLP) further accelerate adoption. The Asia-Pacific region dominates the market, accounting for approximately 80% of global demand, while North America and Europe hold shares of 16% and 3%, respectively. Key players such as AGC, Schott, and Corning collectively control nearly 90% of the market, leveraging their expertise in glass manufacturing and semiconductor applications.

MARKET DYNAMICS

MARKET DRIVERS

Booming Demand for High-Performance Computing and AI Chips Accelerates Adoption

The rapid expansion of artificial intelligence (AI), machine learning, and cloud computing is creating unprecedented demand for advanced semiconductor packaging solutions. Glass core substrates, with their superior thermal stability and electrical insulation properties, are emerging as critical enablers for next-generation chip designs. The global AI chip market is projected to grow at over 30% CAGR through 2030, driving parallel growth in specialized packaging materials. Leading chip manufacturers are increasingly adopting glass substrates to overcome the limitations of organic materials in high-frequency applications, particularly for processors powering data centers and edge computing devices.

Advancements in Wafer-Level Packaging Technology Fuel Market Expansion

Wafer-level packaging (WLP) now accounts for approximately 60% of glass substrate applications, as this approach enables higher integration density and better performance for advanced semiconductors. The transition to panel-level packaging, while still emerging, presents additional growth potential with potential cost reductions of 20-30% compared to traditional methods. Recent developments include the introduction of ultra-thin glass substrates below 100μm thickness, enabling more compact chip designs without compromising mechanical stability. Major Asian semiconductor manufacturers are investing heavily in WLP capabilities, with several new facilities coming online in 2024 specifically designed for glass substrate integration.

5G Infrastructure Deployment and IoT Proliferation Create Sustained Demand

The global rollout of 5G networks and rapid IoT adoption are driving significant demand for radio frequency (RF) components that benefit from glass substrates’ low dielectric loss characteristics. With over 2 billion 5G connections expected by 2025, component manufacturers require packaging solutions that can handle higher frequencies while minimizing signal interference. Glass substrates demonstrate up to 50% better high-frequency performance compared to organic alternatives, making them ideal for 5G front-end modules and millimeter-wave applications. Furthermore, the automotive sector’s growing adoption of connected vehicle technologies presents additional opportunities, particularly for radar and V2X communication systems.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes Limit Adoption

While glass core substrates offer technical advantages, their adoption faces challenges due to substantially higher production costs compared to conventional organic substrates. The specialized manufacturing process requires precision glass handling equipment and cleanroom facilities that can add 30-40% to overall packaging costs. Precision via formation in glass remains particularly challenging, with current laser drilling techniques being both time-consuming and equipment-intensive. These cost factors make glass substrates economically viable primarily for high-end applications, leaving mid-range semiconductor products still reliant on traditional materials.

Supply Chain Constraints and Material Availability Pose Challenges

The glass substrate market is currently constrained by limited supplier diversity, with fewer than ten major manufacturers worldwide capable of producing semiconductor-grade materials. This concentration creates potential supply bottlenecks, especially as demand accelerates across multiple industries. Certain specialty glass formulations require rare earth elements and high-purity raw materials that face periodic shortages. The industry also faces logistical challenges in handling fragile glass panels during transportation, which increases both costs and the risk of yield losses throughout the value chain.

Technical Hurdles in Integration with Existing Packaging Infrastructure

Adopting glass substrates requires significant changes to established semiconductor packaging workflows. The different thermal expansion characteristics of glass compared to silicon create challenges in maintaining reliable interconnects during temperature cycling. Current bonding technologies often require additional interface layers or modified processes that increase complexity. Furthermore, the brittle nature of glass demands specialized handling equipment throughout assembly lines, requiring substantial capital investment from manufacturers transitioning from organic substrates. These integration challenges slow adoption rates despite the technology’s performance benefits.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging Architectures Present Growth Potential

The development of 3D IC packaging and chiplet architectures creates significant opportunities for glass substrate innovation. These advanced approaches benefit from glass’s dimensional stability and ability to support high-density interconnects. Several leading semiconductor companies are prototyping glass interposers for heterogenous integration, potentially doubling the addressable market for substrates by 2030. Additionally, the push toward co-packaged optics in data centers opens new avenues, as glass substrates can seamlessly integrate optical and electronic components on a single platform.

Geographic Expansion in Semiconductor Manufacturing Creates New Demand Centers

Government initiatives worldwide to strengthen domestic semiconductor capabilities are driving new substrate demand. Major investment programs in regions such as North America and Europe aim to reduce reliance on Asian supply chains. For example, recent semiconductor fabrication plant announcements include specific provisions for advanced packaging facilities that could utilize glass substrates. This geographic diversification helps mitigate regional supply risks while opening new customer bases for substrate manufacturers.

Material Science Breakthroughs Enable New Performance Frontiers

Ongoing research into glass compositions with tunable properties presents long-term growth opportunities. Innovations such as ultra-low CTE glass formulations and photosensitive varieties could enable entirely new packaging applications. Recent developments in strength enhancement techniques have shown promise in addressing glass’s brittleness concerns. These material advancements, coupled with improved manufacturing processes, could substantially expand the addressable market by making glass substrates viable for more mainstream semiconductor products.

MARKET CHALLENGES

Standardization Gaps and Intellectual Property Barriers Hinder Market Development

The emerging nature of glass substrate technology means industry standards for specifications and testing methodologies remain under development. This lack of standardization creates uncertainty for both suppliers and adopters. Additionally, key manufacturing processes are often protected by patents, limiting technology transfer and slowing industry-wide innovation. Resolving these standardization and IP challenges will be crucial for achieving broader market acceptance.

Competition from Alternative Advanced Substrate Technologies

While glass substrates offer distinct advantages, they face competition from emerging organic-inorganic hybrid materials and improved silicon-based solutions. Some alternatives claim comparable performance at lower cost points. The rapid innovation in composite materials poses a continuing challenge for glass substrate adoption, particularly in price-sensitive applications. Manufacturers must continually demonstrate superior total cost of ownership to maintain market position.

Workforce Development and Skills Shortage Impacts Implementation

The specialized nature of glass substrate manufacturing and integration requires a workforce with unique skills spanning materials science, semiconductor physics, and precision engineering. Currently, few academic programs specifically address glass substrate technology, creating a talent gap. Companies face challenges in recruiting and training personnel capable of managing the full production workflow. Addressing this skills shortage through targeted education programs and industry collaboration will be essential for sustained market growth.

GLASS CORE SUBSTRATES MARKET TRENDS

Demand for High-Performance Computing (HPC) Drives Glass Core Substrates Adoption

The global glass core substrates market is witnessing robust growth, propelled by the increasing demand for high-performance computing (HPC) and artificial intelligence (AI) chips. With the market valued at $195 million in 2024 and projected to reach $572 million by 2032, glass core substrates are emerging as a critical component in next-generation semiconductor packaging. Unlike conventional organic or silicon-based substrates, glass offers superior thermal stability, lower signal loss, and enhanced dimensional stability, making it ideal for high-frequency applications. Leading manufacturers like AGC, Schott, and Corning are accelerating product innovations to meet the surging demand, particularly in the Asia-Pacific region, which holds an 80% market share.

Other Trends

Advanced Packaging Technologies Fueling Market Expansion

The shift toward advanced packaging solutions, including wafer-level packaging (WLP) and panel-level packaging (PLP), is a key growth driver. Wafer-level packaging alone accounts for about 60% of the total market share as it enables higher integration density and improved performance for AI processors and 5G communication devices. Glass core substrates with a Coefficient of Thermal Expansion (CTE) above 5 ppm/°C dominate the market (65% share) due to superior compatibility with silicon-based die. Meanwhile, the rising complexity of IC designs is pushing manufacturers toward glass-based solutions that minimize warpage and enable finer pitch interconnections.

Material Innovations and Sustainability Initiatives Gain Momentum

Leading suppliers are intensifying R&D efforts to develop eco-friendly glass core substrates that reduce environmental impact without compromising performance. For example, Corning’s ultra-low-loss glass substrates are being adopted in high-speed data centers, while AGC has introduced thinner glass solutions with improved mechanical strength. With semiconductor companies committing to net-zero emissions, recyclable glass substrates are gaining preference over traditional epoxy-based laminates, further shaping the competitive landscape. Additionally, collaborations between substrate manufacturers and foundries aim to optimize glass integration in 3D-IC and heterogeneous packaging architectures, unlocking new growth avenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance by Established Glass Technology Giants with Expanding Semiconductor Applications

The global glass core substrates market exhibits a highly consolidated structure, where AGC, Schott, Corning, Hoya, and Ohara collectively control approximately 90% of market share as of 2024. This dominance stems from their technological expertise in precision glass manufacturing and established relationships with semiconductor packaging leaders. AGC (Asahi Glass Company) leads the segment through proprietary glass formulations specifically engineered for advanced chip packaging, while Corning leverages its Gorilla Glass brand recognition to penetrate the emerging glass substrate segment.

Schott AG maintains a strong foothold through its TEMPAX® high-performance borosilicate glass series, preferred for thermal stability in wafer-level packaging. The company’s 2023 partnership with TSMC to develop next-generation glass substrates for 3D IC packaging demonstrates its commitment to technology leadership. Meanwhile, Hoya Corporation continues to gain traction with its low-CTE glass cores that minimize silicon die stress during high-temperature packaging processes.

Regional dynamics significantly influence competition, with Asia-Pacific housing 80% of glass substrate demand due to concentration of semiconductor packaging facilities. This geographic advantage benefits Japanese players like Ohara Corporation and Dai Nippon Printing, who have optimized supply chains serving Taiwanese, Korean and Chinese OSAT (outsourced semiconductor assembly and test) providers. Recent capacity expansions by these firms in Southeast Asia aim to reduce lead times for major clients like ASE Group and Amkor Technology.

List of Key Glass Core Substrate Manufacturers

- AGC Inc. (Japan)

- Schott AG (Germany)

- Corning Incorporated (U.S.)

- Hoya Corporation (Japan)

- Ohara Corporation (Japan)

- Dai Nippon Printing Co., Ltd. (Japan)

- Nippon Electric Glass (NEG) (Japan)

- CrysTop Glass (China)

- WGTech (South Korea)

Segment Analysis:

By Type

Coefficient of Thermal Expansion (CTE) Above 5 ppm/°C Segment Leads Due to Superior Compatibility with Semiconductor Packaging

The market is segmented based on type into:

- Coefficient of Thermal Expansion (CTE), above 5 ppm/°C

- Coefficient of Thermal Expansion (CTE), below 5 ppm/°C

By Application

Wafer Level Packaging Segment Dominates Owing to High Demand in Advanced Semiconductor Manufacturing

The market is segmented based on application into:

- Wafer Level Packaging

- Panel Level Packaging

By End User

Semiconductor Manufacturers Lead Adoption Due to Need for High-Performance Packaging Solutions

The market is segmented based on end user into:

- Semiconductor manufacturers

- Electronics component producers

- Research and development institutions

- Others

By Technology

Advanced Packaging Segment Grows Rapidly Due to Increasing Demand for Miniaturization

The market is segmented based on technology into:

- Advanced packaging

- Traditional packaging

Regional Analysis: Glass Core Substrates Market

Asia-Pacific

Asia-Pacific dominates the global glass core substrates market, accounting for approximately 80% of the total market share in 2024. This dominance is driven by massive semiconductor manufacturing activities in countries like China, South Korea, Japan, and Taiwan. The region benefits from strong government support, with China’s $150 billion semiconductor investment plan accelerating domestic production capabilities. Japan and South Korea lead in innovation, with major players like AGC and Hoya headquartered there. While wafer-level packaging drives most demand, panel-level packaging adoption is gaining traction. The region’s cost-competitive manufacturing ecosystem and proximity to leading semiconductor fabs like TSMC and Samsung make it the preferred location for glass substrate production.

North America

North America holds the second-largest market share at 16%, primarily fueled by advanced semiconductor R&D and high-performance computing applications in the U.S. The CHIPS and Science Act, allocating $52 billion for domestic semiconductor manufacturing, is creating new opportunities for glass substrate adoption. Major technology companies in Silicon Valley are driving demand for advanced packaging solutions to support AI and data center applications. However, higher production costs compared to Asia and limited local manufacturing capacity restrain faster growth. Collaborations between material suppliers like Corning and semiconductor giants aim to overcome these challenges.

Europe

Europe accounts for approximately 3% of the global market, with growth centered in Germany, France, and the Nordic countries. The region focuses on specialized applications in automotive and industrial semiconductors, where glass substrates’ thermal stability is critical. EU initiatives like the European Chips Act are boosting investments in next-generation packaging technologies. While adoption lags behind Asia, European research institutions and companies like Schott are pioneering novel glass compositions with ultra-low CTE for niche applications. The market faces challenges from high energy costs and competition from established Asian suppliers.

South America

South America represents an emerging market with limited current adoption of glass core substrates. Brazil shows the most potential due to its growing electronics manufacturing sector, but infrastructure limitations and reliance on imported semiconductors hinder market development. The region currently lacks local production capabilities, with most substrates sourced from Asia or North America. However, increasing foreign investments in Mexican semiconductor assembly plants could create downstream demand in the coming years. Economic volatility remains a key challenge for technology adoption across the region.

Middle East & Africa

This region has minimal involvement in the glass core substrates market today. While countries like Israel have advanced semiconductor design capabilities, they lack manufacturing scale. The UAE and Saudi Arabia’s investments in technology infrastructure could generate future demand, particularly for data center applications. However, absence of local supply chains and limited technical expertise in advanced packaging technologies create barriers to adoption. The market is expected to remain dependent on imports from Asia and Europe for the foreseeable future.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Glass Core Substrates markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Glass Core Substrates Market?

-> Glass Core Substrates Market was valued at 195 million in 2024 and is projected to reach US$ 572 million by 2032, at a CAGR of 17.0% during the forecast period..

Which key companies operate in Global Glass Core Substrates Market?

-> Key players include AGC, Schott, Corning, Hoya, Ohara, Dai Nippon Printing (DNP), NEG, CrysTop Glass, and WGTech, among others. The top five players hold approximately 90% of the market share.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance computing (HPC) and AI chips, advancements in semiconductor packaging technologies, and increasing adoption of wafer-level packaging solutions.

Which region dominates the market?

-> Asia-Pacific is the largest market, accounting for 80% of global demand, driven by semiconductor manufacturing hubs in China, Japan, and South Korea. North America and Europe hold 16% and 3% shares, respectively.

What are the emerging trends?

-> Emerging trends include development of ultra-thin glass substrates, integration of advanced thermal management solutions, and growing R&D investments in next-generation semiconductor packaging.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...