MARKET INSIGHTS

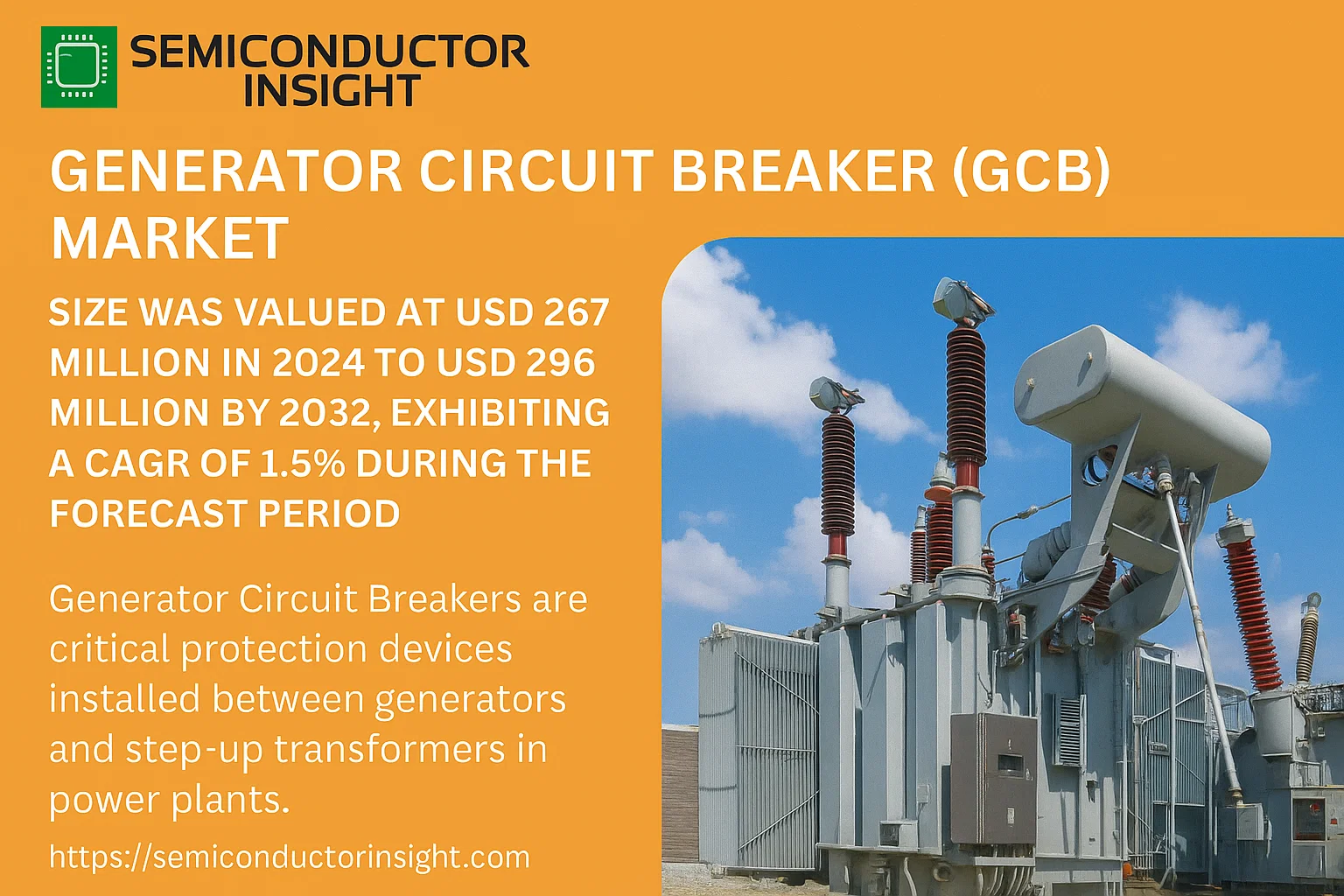

Global Generator Circuit Breaker (GCB) Market size was valued at USD 267 million in 2024 to USD 296 million by 2032, exhibiting a CAGR of 1.5% during the forecast period.

Generator Circuit Breakers are critical protection devices installed between generators and step-up transformers in power plants. These specialized circuit breakers are designed to handle the unique challenges of generator protection, including high continuous currents, asymmetrical short-circuit currents, and demanding transient recovery voltage conditions. The main types include vacuum circuit breakers, SF6 circuit breakers, and other emerging technologies.

The market is experiencing steady growth driven by increasing investments in power generation infrastructure, particularly in renewable energy projects and grid modernization initiatives. Europe dominates the global landscape with approximately 80% market share, while North America follows with about 12% share. The market is highly concentrated, with the top three manufacturers ABB, Siemens, and Schneider Electric collectively holding around 81% of the market. Recent developments include technological advancements in vacuum interruption technology and the phase-out of SF6 gas in some regions due to environmental concerns.

MARKET DRIVERS

Rising Global Demand for Uninterrupted Power Supply

The increasing global demand for reliable electricity, particularly from critical sectors like data centers, healthcare, and industrial manufacturing, is a primary driver for the Generator Circuit Breaker (GCB) Market. These sectors require highly reliable backup power systems to prevent costly downtime, directly increasing the need for robust generator protection equipment like GCBs.

Expansion of Renewable Energy Integration

As power grids incorporate more intermittent renewable sources such as wind and solar, the role of standby and peaking generators has become more critical. GCBs are essential for safely synchronizing and isolating these generators from the grid, ensuring stability and safety during fluctuations in renewable power generation.

Furthermore, stricter regulations and standards for electrical safety and equipment performance are compelling power plant operators and industries to upgrade their older switching and protection systems to modern, more reliable GCBs.

MARKET CHALLENGES

High Capital and Maintenance Costs

Generator Circuit Breakers represent a significant capital investment. Their complex design, which must handle high short-circuit currents and frequent switching, leads to higher initial costs compared to standard circuit breakers. Additionally, specialized maintenance and testing requirements contribute to a high total cost of ownership, which can be a barrier for some end-users.

Other Challenges

Technical Complexity and Skilled Labor Shortage

The installation, commissioning, and maintenance of GCBs require highly skilled technicians with specific expertise in high-voltage systems. A global shortage of such specialized labor can lead to project delays and increased service costs.

Supply Chain Constraints for Critical Components

The production of GCBs relies on specialized materials and components, such as specific interrupting chamber technologies and high-performance contacts. Disruptions in the supply chain for these critical parts can lead to extended lead times and increased prices.

MARKET RESTRAINTS

Economic Volatility and Fluctuating Investment in Power Infrastructure

Capital-intensive projects in the power generation sector are highly sensitive to economic cycles. During periods of economic uncertainty or recession, investments in new power plants or major upgrades to existing facilities, which drive GCB demand, are often deferred or cancelled. This cyclical nature of investment acts as a significant restraint on market growth.

Competition from Alternative Protection Schemes

In some applications, particularly for smaller generators, utilities and industries may opt for alternative protection schemes that use a combination of generator contactors and low-voltage circuit breakers. While potentially less robust, these alternatives can offer a lower-cost solution, posing a competitive restraint to the adoption of dedicated GCBs in certain market segments.

MARKET OPPORTUNITIES

Growing Investments in Data Center Infrastructure

The exponential growth of cloud computing, big data, and digitalization is fueling massive investments in data centers globally. These facilities require absolute power reliability, often supported by multiple large backup generators. This creates a substantial and growing market for high-performance GCBs to protect these critical assets.

Modernization and Replacement of Aging Fleet

A significant portion of the existing installed base of generator protection equipment, particularly in developed regions, is aging and nearing the end of its operational life. The need to replace these systems with more efficient and digitally enabled GCBs presents a major aftermarket and retrofit opportunity for manufacturers.

Adoption of SF6-Free and Eco-Friendly Technologies

With increasing regulatory pressure to phase out SF6 gas due to its high global warming potential, there is a significant opportunity for the development and adoption of alternative interruption technologies, such as vacuum circuit breakers or those using environmentally friendly gases. Companies leading in this innovation are poised to capture new market share.

Generator Circuit Breaker (GCB) Market Trends

Steady Market Growth Driven by Power Generation Investments

Global Generator Circuit Breaker (GCB) Market is on a path of steady, measured growth. Valued at an estimated USD 267 million in 2024, the market is projected to reach USD 296 million by 2032, reflecting a compound annual growth rate (CAGR) of 1.5%. This growth is primarily supported by ongoing investments in power generation infrastructure across various global regions. Generator Circuit Breakers are critical protection devices installed between a generator and a step-up voltage transformer, safeguarding both assets from electrical faults. The persistent need for reliable electricity and the modernization of aging power plants are key factors underpinning market demand, ensuring a stable outlook for the foreseeable future.

Other Trends

Dominance of SF6 and Vacuum Technologies

The market is segmented by breaker type into Vacuum Circuit Breakers, SF6 Circuit Breakers, and others. SF6 circuit breakers have traditionally held a significant market share due to their excellent arc-quenching properties and high reliability for heavy-duty applications. However, environmental concerns regarding SF6 gas, which is a potent greenhouse gas, are driving increased adoption of Vacuum Circuit Breaker technology. Vacuum breakers offer a more environmentally friendly alternative with minimal maintenance requirements, and their share is expected to grow as regulations on SF6 emissions tighten globally.

Regional Market Concentration

Europe stands as the dominant force in the Generator Circuit Breaker market, commanding approximately 80% of the global market share. This is largely attributed to a high concentration of power generation facilities, stringent safety and reliability standards, and ongoing grid modernization projects. The United States follows as the second-largest market, accounting for about 12% of the global share, driven by its substantial power generation capacity and infrastructure renewal initiatives. The Asian market, while currently holding a smaller share, presents significant growth potential due to rapid industrialization and expanding energy needs.

Consolidated Competitive Landscape with Emphasis on Innovation

The competitive environment is highly concentrated, with the top three companies ABB, Siemens, and Schneider collectively occupying approximately 81% of the market. Other key players include General Electric, Mitsubishi Electric, Eaton, Hitachi, Chinatcs, and NHVS. This high level of market share concentration indicates significant barriers to entry, driven by the need for advanced engineering expertise, rigorous safety certifications, and long-standing relationships with major power utilities. Competition is largely based on technological innovation, product reliability, service support, and the development of environmentally sustainable solutions, particularly alternatives to SF6 gas.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Dominated by a Select Few in Power Infrastructure

Global Generator Circuit Breaker (GCB) Market is characterized by a high level of concentration, with the top three players ABB, Siemens, and Schneider Electric collectively commanding approximately 81% of the total market share as of 2024. This dominance is a testament to their extensive product portfolios, strong global distribution networks, and deep-rooted relationships with major power generation utilities across nuclear, thermal, and hydraulic power plants. These established giants leverage their expertise in high-voltage equipment and long-standing reputations for reliability to secure large-scale contracts, creating significant barriers to entry for smaller players and reinforcing a mature, oligopolistic market structure. Technological innovation, particularly in SF6 and vacuum circuit breaker technologies, remains a key competitive differentiator among these leaders.

Beyond the dominant trio, several other significant players maintain strong positions in specific regional markets or product niches. Companies like Mitsubishi Electric, General Electric, and Eaton hold considerable expertise and offer robust GCB solutions, often competing for major projects, especially in the North American and Asian markets. Furthermore, specialized manufacturers such as Hitachi, NHVS, and Chint (also known as Chinatcs) have carved out substantial roles, frequently focusing on cost-competitive offerings and catering to specific application needs in emerging economies. These companies contribute to a dynamic competitive environment, ensuring a diversity of options for power plant operators worldwide while collectively addressing the global demand for critical generator protection systems.

List of Key Generator Circuit Breaker (GCB) Companies Profiled

- ABB

- Siemens

- Schneider Electric

- General Electric

- Mitsubishi Electric

- Eaton

- Hitachi

- Chint (Chinatcs)

- NHVS

- Hyosung Heavy Industries

- Toshiba Infrastructure Systems & Solutions

- Larsen & Toubro

- Fuji Electric

- Bharat Heavy Electricals Limited (BHEL)

- CG Power and Industrial Solutions

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

SF6 Circuit Breaker has traditionally been the dominant technology due to its exceptional dielectric strength and superior arc-quenching capabilities, which are critical for the high fault currents associated with large generators. However, the Vacuum Circuit Breaker segment is experiencing a notable uptrend, driven by increasing environmental regulations concerning SF6 gas emissions and the advantages of vacuum technology, including minimal maintenance requirements, longer operational life, and enhanced safety. The evolution towards more sustainable and maintenance-friendly solutions is a key factor influencing technology adoption in this market. |

| By Application |

|

Thermal Power Plants represent the most significant application segment, as they constitute a large portion of the global baseload power generation infrastructure and require robust protection systems for their massive generators. The demand in this segment is characterized by the need for high reliability and the ability to handle substantial electrical loads. Meanwhile, the Nuclear Power Plants segment demands GCBs with the utmost reliability and safety certifications, creating a specialized, high-value niche. The hydraulic power segment also presents steady demand, particularly in regions with significant investments in hydropower infrastructure. |

| By End User |

|

Utility Companies are the primary end users, driving the bulk of market demand due to their ownership of large-scale power generation assets. Their procurement decisions are heavily influenced by long-term reliability, lifecycle costs, and adherence to stringent grid codes. Independent Power Producers (IPPs) represent a dynamic segment, often more agile in adopting newer technologies to optimize the efficiency and profitability of their plants. The Industrial Self-Generators segment, including large manufacturing and mining operations, requires GCBs for captive power plants, with a strong focus on minimizing operational downtime and ensuring continuous process power supply. |

| By Voltage Rating |

|

High Voltage GCBs are the leading segment, as they are predominantly used in the majority of large-scale power generation facilities, including thermal and nuclear plants, where generators are typically connected to the grid at high voltage levels. The technical complexity and performance requirements for these breakers are substantial, creating a high-barrier segment dominated by established global players. The Medium Voltage segment caters to smaller generators and specific industrial applications, while Extra High Voltage applications are more niche, associated with the largest power plants and interconnections, demanding cutting-edge technology and exceptional reliability. |

| By Installation |

|

Outdoor installation is the conventional and most widely adopted method, especially for large power plants where space is less constrained. The key driver for this segment is the straightforward installation and accessibility for maintenance. However, the GIS (Gas-Insulated Switchgear) segment is gaining significant traction in regions with space limitations or harsh environmental conditions, as it offers a compact, reliable, and environmentally protected solution. The indoor installation segment is typically reserved for specific industrial settings or smaller generating units where environmental protection is already provided by the building infrastructure. |

Regional Analysis: Generator Circuit Breaker (GCB) Market

The relentless growth of manufacturing and the establishment of hyperscale data centers across Southeast Asia and East Asia require uninterrupted power, creating a massive, continuous demand for generator sets and their protective circuit breakers. This industrial backbone is a primary driver for the GCB market, necessitating advanced protection solutions for mission-critical operations.

National policies focused on electrification, particularly in developing economies like India and Indonesia, are leading to substantial investments in new power plants and grid infrastructure. These projects, often incorporating both conventional and renewable sources, specify the use of high-performance GCBs to meet reliability standards, ensuring steady market demand from the public sector.

A concentration of electrical component manufacturers in countries such as China provides a significant advantage in terms of production capacity and cost-efficiency. This localized supply chain reduces lead times and costs for GCBs, making advanced protection more accessible for regional power projects and enhancing the competitiveness of the entire market.

As the region aggressively adopts solar and wind power, there is a growing need for GCBs that can handle bidirectional power flow and the unique fault currents associated with inverter-based resources. This technological shift is driving innovation and the adoption of next-generation GCBs, securing the region’s leadership in the evolving energy landscape.

North America

The North American GCB market is characterized by a strong emphasis on reliability, replacement of aging infrastructure, and stringent regulatory standards. The region’s mature power grid requires continuous upgrades and maintenance, creating a steady demand for high-quality GCBs for both utility-scale power plants and critical backup systems in sectors like healthcare and data centers. A key driver is the need to enhance grid resilience against extreme weather events, leading to investments in more robust protection systems. Furthermore, the ongoing energy transition, including the integration of natural gas plants and renewables, necessitates advanced GCBs that offer greater control and monitoring capabilities, supporting the region’s focus on operational excellence and safety.

Europe

Europe’s GCB market is driven by the ambitious decarbonization goals of the European Green Deal, which is accelerating the phase-out of conventional power plants and the integration of renewable energy sources. This transition creates a demand for specialized GCBs that can manage complex grid interactions and ensure stability with a high penetration of renewables. There is also a significant market for upgrading existing thermal power plants with more efficient and environmentally compliant GCBs. The presence of leading international electrical equipment manufacturers in the region fosters innovation, particularly in developing smart and digitally enabled circuit breakers that align with Europe’s focus on a digitalized and interconnected energy system.

Middle East & Africa

The GCB market in the Middle East & Africa is primarily fueled by massive investments in power generation infrastructure to support economic diversification and address energy access challenges. In the Middle East, large-scale desalination plants, industrial cities, and ongoing construction projects rely heavily on backup power, driving demand for robust GCBs. In Africa, the focus is on expanding electrification and developing independent power projects, which require reliable generator protection. The market is also influenced by the need to maintain uninterrupted power for the oil and gas sector, a critical economic driver in the region, ensuring a consistent need for high-performance circuit protection solutions.

South America

South America’s GCB market is influenced by the region’s reliance on hydropower and the growing investment in diversifying its energy mix with thermal, solar, and wind power. The need to protect large hydroelectric generators and the increasing number of distributed generation systems creates opportunities for GCB suppliers. Infrastructure development projects, particularly in the mining and industrial sectors in countries like Chile and Brazil, are key demand drivers. However, market growth can be uneven, often correlating with national economic stability and the pace of energy sector reforms, which influence investment in new power generation assets and their associated protection equipment.

Report Scope

This market research report provides a comprehensive analysis of the Generator Circuit Breaker (GCB) Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Generator Circuit Breaker (GCB) Market?

-> Generator Circuit Breaker (GCB) Market size was valued at USD 267 million in 2024 to USD 296 million by 2032, exhibiting a CAGR of 1.5% during the forecast period.

Which key companies operate in Generator Circuit Breaker (GCB) Market?

-> Key players include ABB, Siemens, Schneider, General Electric, Mitsubishi Electric, Eaton, Hitachi, Chinatcs, NHVS, among others. The top 3 companies occupy about 81% market share.

What are the key growth drivers?

-> Global demand for reliable power generation and expansion of power plants are key growth drivers for the GCB market.

Which region dominates the market?

-> Europe is the largest Generator Circuit Breaker (GCB) Market with about 80% market share. The US is a follower, accounting for about 12% market share.

What are the emerging trends?

-> Emerging trends include product development and innovation in vacuum and SF6 circuit breaker technologies for enhanced protection and reliability in power generation applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...