GaN Diodes Market Insights

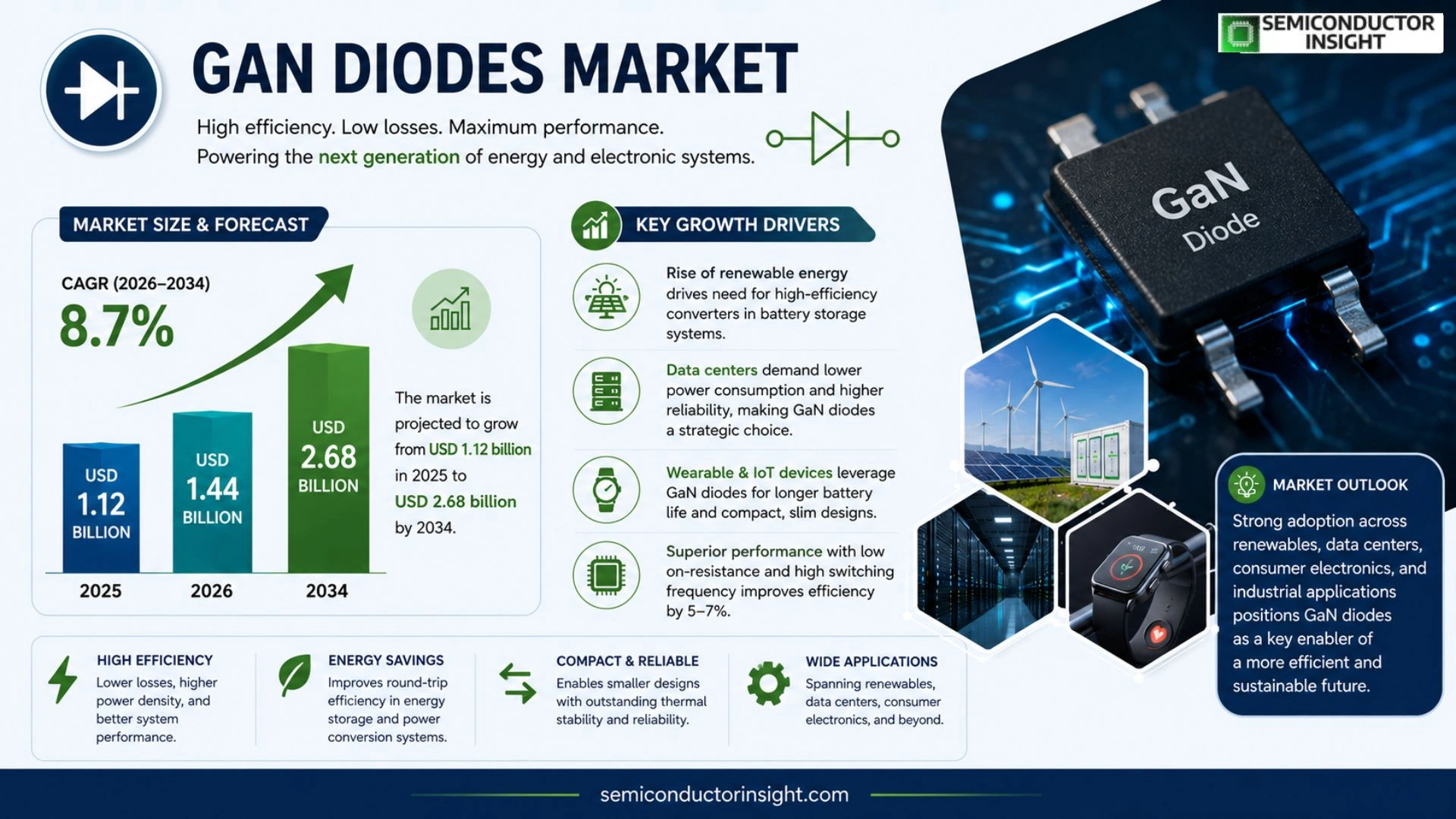

GaN Diodes Market size was valued at USD 1.12 billion in 2025. The market is projected to grow from USD 1.12 billion in 2025 to USD 2.68 billion by 2034, exhibiting a CAGR of 8.7% during the forecast period.

GaN (gallium nitride) diodes are semiconductor components that exploit the wide band‑gap characteristics of gallium nitride to deliver high breakdown voltage, low on‑resistance and ultra‑fast switching speeds, enabling efficient power conversion, RF amplification and high‑frequency operation.

The market is experiencing rapid expansion because automotive electrification, data‑center power‑efficiency goals and the rollout of next‑generation wireless infrastructure are driving demand. Furthermore, cost reductions through advanced substrate technologies and increased production capacity from leading manufacturers such as Infineon Technologies, Navitas Semiconductor, Efficient Power Conversion and Texas Instruments are reinforcing this growth trajectory.

MARKET DRIVER

Rising Demand in Automotive Power Systems

GaN Diodes Market is being propelled by the rapid electrification of vehicles, where manufacturers require compact, high‑efficiency power conversion. GaN technology delivers 30‑40% lower losses compared with traditional silicon devices, enabling longer range and faster charging for electric cars. This efficiency advantage translates into measurable cost savings for OEMs, reinforcing the upward trajectory of the market.

Expansion of 5G Infrastructure

Deployment of 5G networks creates a need for high‑frequency, high‑power RF components. GaN diodes excel in these applications, offering high breakdown voltage and fast switching speeds that support dense antenna arrays and base stations. Analysts forecast that the rollout of 5G will add over $1.2 billion to the total addressable market for GaN diodes by 2028.

➤ GaN Diodes enable up to 40% efficiency gains in DC‑DC converters, driving broader adoption across industrial power supplies.

Overall, the convergence of automotive electrification, 5G rollout, and the push for greener industrial equipment creates a robust foundation for sustained growth GaN Diodes Market.

MARKET CHALLENGES

Technical Integration Barriers

Despite performance benefits, integrating GaN diodes into legacy silicon‑based platforms requires redesign of driver circuits and thermal management solutions. This engineering complexity can extend development cycles, deterring smaller manufacturers from immediate adoption.

Other Challenges

Manufacturing Cost Constraints

The epitaxial growth process for GaN remains capital‑intensive, resulting in unit costs that are 2‑3 times higher than comparable silicon components. This price premium limits entry into cost‑sensitive markets such as consumer electronics.

Supply chain volatility, especially for high‑purity substrates, further complicates scaling production and maintaining competitive pricing.

MARKET RESTRAINTS

High Capital Expenditure

Establishing dedicated GaN fabrication facilities demands significant upfront investment, often exceeding $200 million. This high barrier to entry restricts market participation to a handful of well‑capitalised players, slowing broader diffusion.

The scarcity of skilled engineers familiar with GaN device design adds to the human‑resource restraint, as companies must invest heavily in training programs to build competent teams.

Regulatory scrutiny in aerospace and defense sectors imposes stringent qualification protocols, extending time‑to‑market and increasing compliance costs for GaN diode manufacturers.

MARKET OPPORTUNITIES

Emerging Renewable Energy Storage

The shift toward renewable energy sources creates demand for high‑efficiency power converters in battery storage systems. GaN diodes, with their low on‑resistance and high switching frequency, can improve round‑trip efficiency by 5‑7%, opening lucrative opportunities for vendors.

Data centers are seeking to reduce power consumption, and GaN‑based power supplies present a pathway to significant energy savings while maintaining high reliability, positioning the technology as a strategic choice for cloud operators.

Wearable and IoT devices benefit from the miniaturisation potential of GaN diodes, enabling longer battery life and thinner form factors, which could drive a new wave of consumer‑focused applications for GaN Diodes Market.

GaN Diodes Market Trends

Automotive Electrification Drives Growth

GaN Diodes Market is experiencing a pronounced shift driven by the rapid electrification of vehicles. Gallium nitride diodes provide the high breakdown voltage and low on‑resistance required for onboard chargers and electric‑drive inverters, enabling lighter power‑train designs and higher efficiency. Automakers are integrating GaN‑based converters to meet stricter emissions standards while reducing battery‑load losses. As vehicle platforms move toward higher voltage architectures, the demand for compact, ultra‑fast switching diodes has accelerated, prompting major semiconductor firms to expand dedicated production lines. Cost reductions achieved through silicon‑on‑sapphire and bulk GaN substrates are lowering the price barrier, allowing tier‑1 suppliers such as Infineon and Texas Instruments to offer volume‑priced components for automotive power modules.

Other Trends

Data‑Center Power Efficiency

Data‑center operators are targeting higher power‑density designs to sustain ever‑growing compute workloads. GaN diodes deliver ultra‑fast switching and minimal conduction loss, which translates into lower heat generation and reduced cooling infrastructure. These efficiencies support the transition to higher voltage DC distribution within racks, cutting overall energy consumption. Efficient GaN diodes also reduce cooling requirements, supporting the shift to higher power density racks in hyperscale facilities. Leading manufacturers such as Navitas Semiconductor and Efficient Power Conversion have introduced product families specifically optimized for server‑class power supplies, reinforcing the market’s momentum.

Wireless Infrastructure Expansion

The rollout of 5G and emerging 6G networks relies on GaN’s high‑frequency capability and superior linearity. RF power amplifiers built with GaN diodes enable compact base‑station architectures while meeting stringent efficiency targets, which is critical for dense urban deployments. Cost‑effective substrate advances are making these solutions increasingly accessible to telecom equipment makers. As carriers upgrade to higher bandwidth and lower latency services, the demand for high‑performance GaN diodes is expected to remain robust, further solidifying GaN Diodes Market’s upward trajectory.

COMPETITIVE LANDSCAPE

Key Industry Players

GaN Diodes Market Competitive Landscape Overview

GaN diodes segment is anchored by a handful of large‑scale manufacturers that command the majority of volume and drive technology roadmaps. Infineon Technologies leverages its deep silicon‑carbide heritage to deliver high‑voltage GaN diode families for automotive power‑train and industrial applications, while Navitas Semiconductor has captured fast‑switching RF and data‑center markets through its patented vertical GaN architecture. Efficient Power Conversion (EPC) focuses on ultra‑low‑on‑resistance devices for high‑efficiency power supplies, and Texas Instruments integrates GaN diodes into its broader analog portfolio, providing end‑to‑end design support. These leaders benefit from sizable R&D budgets, vertically integrated production lines, and strategic partnerships that reinforce a moderately concentrated market structure, with the top four firms accounting for roughly 55 % of global shipments.

Beyond the dominant quartet, a diverse set of niche players enriches the ecosystem by targeting specialized applications and emerging segments. GaN Systems and Wolfspeed (Cree) emphasize high‑frequency RF amplifiers for 5G infrastructure, while Qorvo supplies GaN‑based e‑power modules for aerospace and defense. STMicroelectronics and NXP broaden their semiconductor portfolios with GaN diode options for automotive safety and IoT power management. Mitsubishi Electric, Microchip Technology (through its acquisition of Microsemi’s GaN portfolio), and Sumitomo Electric contribute region‑specific solutions, often partnering with foundries to accelerate time‑to‑market. These companies collectively enhance competition, drive incremental innovation, and expand the total addressable market.

List of Key GaN Diodes Companies Profiled

- Infineon Technologies

- Navitas Semiconductor

- Efficient Power Conversion

- Texas Instruments

- GaN Systems

- Wolfspeed (Cree)

- Qorvo

- STMicroelectronics

- NXP Semiconductors

- Mitsubishi Electric

- Microchip Technology

- Sumitomo Electric

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Schottky Diodes dominate due to their inherently low on‑resistance and rapid recovery characteristics, making them ideal for high‑efficiency power conversion.

|

| By Application |

|

Power Conversion leads the application landscape, driven by the need for high‑efficiency, compact converters across multiple industries.

|

| By End User |

|

Automotive emerges as the principal end‑user, valuing the high‑voltage capability and fast switching of GaN diodes for on‑board chargers and traction inverters.

|

| By Voltage Rating |

|

High Voltage segment gains traction as system designers push GaN diodes into higher‑power domains.

|

| By Device Architecture |

|

Vertical architecture is emerging as a key differentiator for high‑current, high‑efficiency applications.

|

Regional Analysis: North America

The automotive sector is a key driver for GaN diodes in North America, with increasing adoption in onboard chargers and power inverters for electric vehicles. The demand for high-power, high-efficiency GaN diodes aligns perfectly with the needs of the rapidly expanding EV market.

The growing deployment of solar and wind power infrastructure in North America is creating significant demand for GaN diodes in power conversion systems, particularly in solar inverters. The higher efficiency of GaN-based inverters contributes to better energy yields and reduced system costs.

Industrial applications, such as motor drives and industrial automation, are increasingly utilizing GaN diodes due to their superior efficiency and power density compared to traditional silicon-based components. This trend is driven by the need for more efficient and compact power supplies in industrial equipment.

Data centers are demanding higher power efficiency, and GaN diodes are being integrated into power supplies and other components to address these needs. Improved efficiency translates to lower operating costs and reduced environmental impact for data center operators in North America.

Europe

The European GaN diodes market is witnessing substantial growth, propelled by stringent energy efficiency regulations and a strong focus on sustainable technologies. The automotive industry in Europe is a significant adopter of GaN diodes for electric vehicle applications. Furthermore, the renewable energy sector, particularly solar power, is a key driver. Government initiatives promoting green energy and energy efficiency are also contributing to market expansion. The region’s strong manufacturing base and research institutions are fostering innovation in GaN technology. The integration of GaN diodes in power supplies for industrial and commercial applications is also gaining momentum. Concerns around supply chain resilience post-pandemic are prompting companies to explore regional manufacturing and sourcing options for GaN diodes.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market for GaN diodes, driven by rapid industrialization, increasing investments in electric vehicles, and a burgeoning renewable energy sector. China, in particular, is a dominant force in the Asia-Pacific GaN diodes market, with significant domestic manufacturing capabilities and a strong government push for advanced semiconductor technologies. The automotive industry in countries like China and South Korea is experiencing rapid adoption of GaN diodes. The region’s large electronics manufacturing base also contributes to the high demand for GaN diodes in power supplies and other electronic devices. The availability of cost-competitive manufacturing and a large pool of skilled labor further strengthens the market potential in Asia-Pacific. The focus on high-power applications in areas like 5G communication also supports GaN diode adoption.

South America

The South American market for GaN diodes is relatively nascent but poised for growth. The increasing adoption of electric vehicles in Brazil and Argentina, coupled with investments in renewable energy projects, are key drivers. The industrial sector in countries like Brazil and Chile is also expected to benefit from the improved efficiency offered by GaN diodes in power supplies. While the market currently represents a smaller portion of the global GaN diodes market, the long-term growth potential is significant. Government policies promoting sustainable development and energy efficiency are expected to further stimulate demand.

Middle East & Africa

The Middle East and Africa represent a promising, although currently smaller, market for GaN diodes. The region’s increasing focus on renewable energy, particularly solar power, is a significant driver. Investments in infrastructure projects and the growing automotive sector are also contributing to market growth. The demand for energy-efficient power supplies in industrial and commercial applications is expected to rise with economic development in the region. Government initiatives aimed at diversifying energy sources and promoting sustainable development are creating favorable market conditions for GaN diodes.

Report Scope

This market research report provides a comprehensive analysis of the GaN Diodes Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of GaN Diodes Market?

-> GaN diodes market size is projected to grow from USD 1.12 billion in 2025 to USD 2.68 billion by 2034, exhibiting a CAGR of 8.7%.

Which key companies operate GaN Diodes Market?

-> Key players include Infineon Technologies, Navitas Semiconductor, Efficient Power Conversion, and Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include automotive electrification, data‑center power‑efficiency goals, and the rollout of next‑generation wireless infrastructure.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include advanced substrate technologies, cost‑reduction initiatives, and expanding production capacity by leading manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...