Gallium Nitride (GaN) Power Semiconductor Market Insights

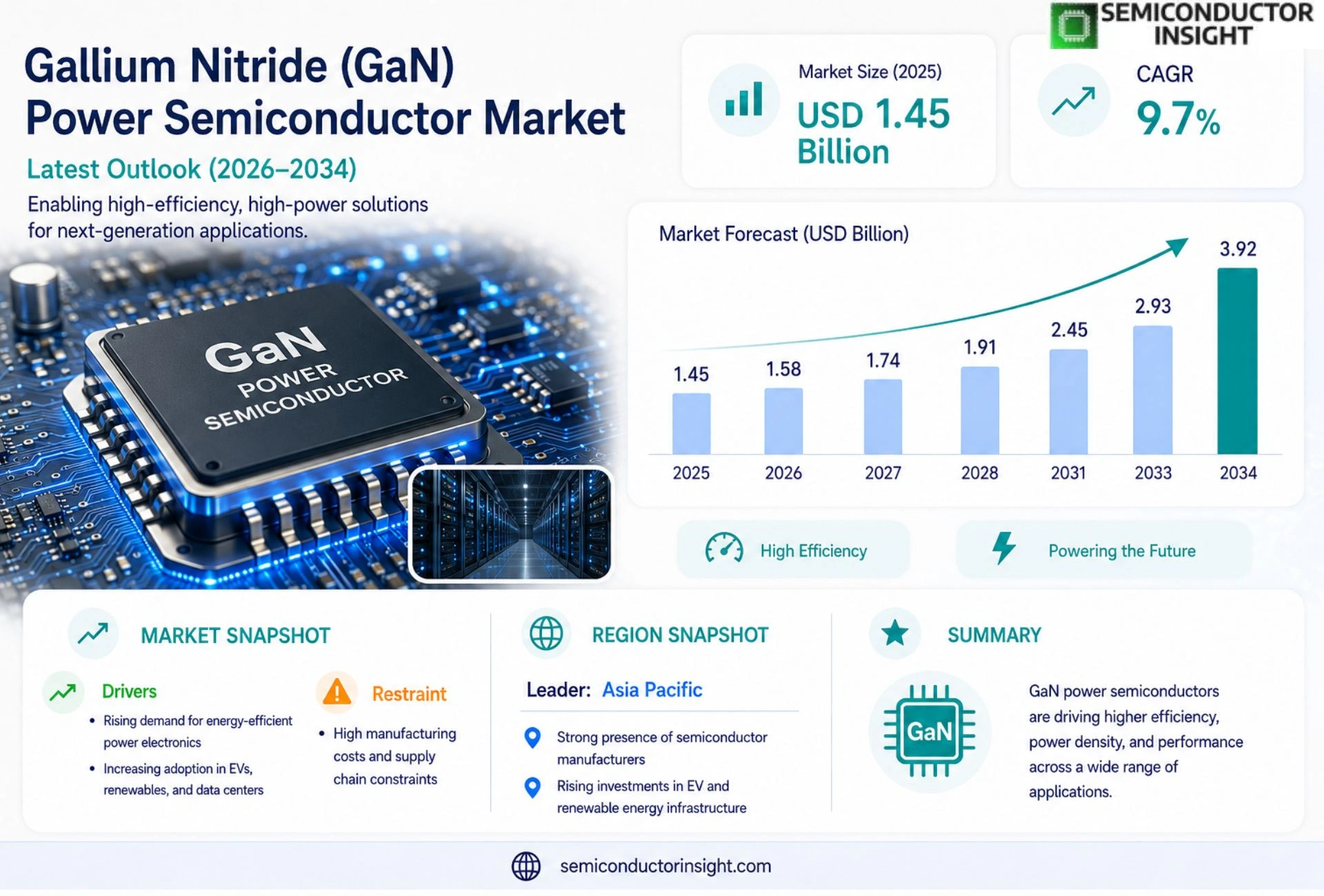

Global Gallium Nitride (GaN) Power Semiconductor Market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.92 billion by 2034, exhibiting a CAGR of 9.7% during the forecast period.

Gallium Nitride power semiconductors are wide‑bandgap devices that enable high‑efficiency voltage conversion, fast switching speeds, and superior thermal performance compared with traditional silicon counterparts. These attributes make GaN ideal for applications such as electric vehicle chargers, data‑center power supplies, RF amplifiers, and aerospace systems.

The market is experiencing rapid expansion driven by rising demand for energy‑efficient solutions, aggressive electrification targets across automotive sectors, and increasing adoption of renewable‑energy infrastructure that requires compact high‑power converters. Furthermore, advancements in substrate technology,particularly silicon‑on‑insulator (SOI) and sapphire wafers,are lowering production costs and accelerating volume adoption. Key players such as Infineon Technologies AG, Texas Instruments Inc., Navitas Semiconductor Corp., ON Semiconductor (onsemi), STMicroelectronics NV, and Efficient Power Conversion Corp are actively investing in next‑generation GaN platforms; for example, in March 2024 Navitas announced a strategic partnership with Samsung Electronics to co‑develop advanced GaN wafer processes aimed at scaling production capacity beyond one million wafers per year.

MARKET DRIVERS

Rising Demand for High‑Efficiency Power Conversion

Gallium Nitride (GaN) Power Semiconductor Market is being propelled by rapid adoption of electric vehicles and data‑center infrastructure, where efficiency gains of up to 30 % over silicon devices translate into lower operating costs and reduced carbon emissions. OEMs are increasingly specifying GaN converters for on‑board chargers, creating a robust pipeline of volume orders.

Policy Support and Energy‑Saving Regulations

Government initiatives worldwide,such as stricter energy‑consumption standards for consumer electronics and incentive programs for renewable‑energy integration,are encouraging manufacturers to transition to GaN technology. These policies accelerate market penetration by offering tax credits and subsidized R&D funding.

➤ Analysts project that cumulative GaN shipments will exceed 1.2 million units by 2028, driven by the convergence of efficiency mandates and rising power‑density requirements.

Collectively, these drivers create a favorable environment for sustained growth, positioning GaN as the preferred choice for next‑generation power electronics.

MARKET CHALLENGES

Manufacturing Complexity and Cost

Despite performance advantages, GaN power semiconductor market faces significant hurdles due to intricate epitaxial growth processes and tight tolerance requirements, which keep production costs above those of mature silicon fabs. Small‑volume manufacturers struggle to achieve economies of scale.

Other Challenges

Supply‑Chain Constraints

Limited availability of high‑purity substrates and specialized processing equipment leads to longer lead times, affecting the ability of OEMs to meet accelerated product roadmaps.

Reliability concerns in high‑temperature and high‑voltage environments also demand extensive qualification, adding to development cycles and capital outlays.

MARKET RESTRAINTS

High Initial Capital Expenditure

Establishing GaN production lines requires substantial upfront investment in MOCVD reactors and clean‑room facilities, deterring smaller entrants and slowing overall market expansion.

Additionally, the current design ecosystem lacks mature simulation tools and standardized footprints, compelling engineers to allocate extra resources for custom layout development.

Thermal management remains a technical restraint; although GaN devices operate at higher frequencies, their heat‑dissipation characteristics demand advanced packaging solutions that are not yet widely available.

MARKET OPPORTUNITIES

Expansion into 5G Infrastructure

The rollout of 5G networks creates a sizable opportunity for GaN power amplifiers and DC‑DC converters, where high power density and fast switching are essential for base‑station efficiency and compact form factor.

Growth in renewable‑energy systems, particularly solar‑inverter and wind‑turbine applications, benefits from GaN’s ability to operate at higher voltages with reduced losses, enabling lighter and more reliable power conversion modules.

Emerging automotive power‑train architectures, such as silicon‑carbide‑GaN hybrid systems, present a frontier for innovation, offering manufacturers a pathway to meet stringent range‑extension targets while maintaining thermal performance.

Gallium Nitride (GaN) Power Semiconductor Market Trends

Growing Adoption in EV Charging Infrastructure

Gallium Nitride (GaN) Power Semiconductor Market is being reshaped by the accelerating electrification of road transport. Vehicle manufacturers are committing to higher percentages of fully electric models, creating a sustained demand for fast‑charge stations that can deliver high power in a compact footprint. GaN converters meet this need by offering faster switching speeds, lower on‑resistance, and superior thermal management compared with silicon alternatives, which directly translates into reduced charger size, lighter weight, and lower installation costs. Recent product roadmaps from leading suppliers such as Infineon, Texas Instruments and ON Semiconductor highlight dedicated EV‑charging modules that promise up to 30 % efficiency gains, encouraging OEMs to integrate GaN‑based power stages across new charging networks worldwide.

Other Trends

Advancements in Substrate Technology

Substrate innovations are a critical enabler for broader market acceptance. The shift toward silicon‑on‑insulator (SOI) and high‑purity sapphire wafers has improved device yield and lowered per‑unit cost, making large‑scale production economically viable. In March 2024 Navitas announced a strategic collaboration with Samsung Electronics to co‑develop advanced wafer processes designed to exceed one million wafers per year, a milestone that signals a transition from niche applications to mainstream adoption. These manufacturing improvements also reduce defect density, allowing designers to push voltage ratings higher while maintaining the intrinsic reliability required for automotive and aerospace deployments.

Expansion into Data‑Center Power Supplies

Data‑center operators are turning to GaN power solutions to address the twin challenges of rising energy consumption and limited floor space. The high‑frequency operation of GaN devices enables power‑density improvements of 40 % or more, which in turn diminishes the size of magnetic components and heat‑sink infrastructure. Operators report measurable operational‑expense reductions because the enhanced thermal performance cuts cooling loads and extends equipment lifespan. Moreover, as renewable‑energy integration intensifies, the need for efficient, high‑speed converters that can quickly adapt to fluctuating input conditions makes GaN an attractive choice for next‑generation data‑center power architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

GaN Power Semiconductor Competitive Landscape 2024‑2034

GaN power semiconductor market is currently dominated by a handful of globally diversified firms that combine deep R&D resources with mature silicon‑based foundry capabilities. Infineon Technologies AG and Texas Instruments Inc. lead the segment by offering integrated GaN platforms for automotive chargers and data‑center power supplies, leveraging their extensive supply‑chain networks to achieve economies of scale. Navitas Semiconductor Corp., backed by strategic alliances such as its 2024 partnership with Samsung Electronics, accelerates wafer‑level production and targets high‑growth niches in fast‑charging and RF power. ON Semiconductor (onsemi) and STMicroelectronics NV contribute complementary product families that emphasize reliability for aerospace and industrial automation, while Efficient Power Conversion Corp. focuses on niche high‑frequency converters that deliver superior thermal performance. Collectively, these leaders account for more than 70 % of the forecasted market revenue through integrated solutions, aggressive cost‑reduction programs, and roadmap‑driven architecture upgrades that align with the market’s projected CAGR of 9.7 %.

Beyond the primary tier, a vibrant set of specialist manufacturers expands the competitive fabric of the GaN ecosystem. GaN Systems Inc. and Qorvo provide high‑power RF amplifiers for 5G infrastructure, whereas NXP Semiconductors and Analog Devices are integrating GaN devices into mixed‑signal portfolios for automotive and IoT applications. Mitsubishi Electric and Rohm Co., Ltd. emphasize silicon‑on‑insulator (SOI) and sapphire substrate innovations that lower unit costs for mass‑market converters. GeneSiC Semiconductor, Panasonic, and Toshiba round out the landscape with niche offerings in power‑dense modules for renewable‑energy converters and aerospace‑grade power supplies. These companies, while smaller in revenue share, drive differentiation through proprietary substrate technologies, customized packaging, and vertical integration strategies that challenge incumbents and broaden the overall market choice.

List of Key GaN Power Semiconductor Companies Profiled

- Infineon Technologies AG

- Texas Instruments Inc.

- Navitas Semiconductor Corp.

- ON Semiconductor (onsemi)

- STMicroelectronics NV

- Efficient Power Conversion Corp.

- GaN Systems Inc.

- Qorvo

- NXP Semiconductors

- Analog Devices

- Mitsubishi Electric

- Rohm Co., Ltd.

- GeneSiC Semiconductor

- Panasonic

- Toshiba

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GaN HEMT dominates the type landscape because it delivers exceptional switching speeds and low on‑resistance.

|

| By Application |

|

Electric Vehicle Fast Chargers are emerging as the leading application segment due to the drive toward rapid charging infrastructure.

|

| By End User |

|

Automotive OEMs lead the end‑user segment because electrification strategies demand higher efficiency power conversion.

|

| By Technology |

|

Silicon‑on‑Insulator is gaining traction because it leverages mature silicon processing while delivering superior thermal performance.

|

| By Market Driver |

|

Energy‑Efficiency Regulations are the primary catalyst, pushing designers toward technologies that can achieve higher conversion efficiency.

|

Regional Analysis: North America

United States

The automotive sector represents a major driver for GaN adoption in the United States, particularly in electric vehicles. GaN’s high efficiency and power density are crucial for improving EV range and reducing charging times. The increasing number of electric vehicle models hitting the market is directly translating to increased demand for GaN power semiconductors.

In the renewable energy sector, GaN power semiconductors enhance the efficiency of solar inverters and wind power converters. Their ability to handle high voltages and frequencies makes them ideal for optimizing energy conversion in these systems, contributing to greater grid stability and reliability.

The industrial power supply market in the US is benefiting from GaN’s compact size and high efficiency. These characteristics are highly valued in industrial applications where space is limited and energy consumption needs to be minimized. GaN-based power supplies are finding increasing use in various industrial equipment, including motor drives and power tools.

GaN is gradually making inroads into consumer electronics, particularly in laptop and mobile phone chargers. Its smaller size and higher efficiency compared to silicon-based solutions offer design advantages and contribute to lower energy bills.

Europe

The European Gallium Nitride (GaN) Power Semiconductor Market is experiencing steady growth, propelled by stringent energy efficiency regulations and increasing adoption in key sectors. The region is witnessing a surge in demand from electric vehicle manufacturers, as well as advancements in renewable energy infrastructure and industrial automation. Government support for green technologies and a strong focus on sustainable development are further fueling market expansion. Key players in Europe are investing in R&D to develop advanced GaN solutions tailored to the specific needs of European industries. The growing emphasis on power electronics in electric mobility is a significant driver, alongside applications in industrial power supplies and consumer electronics. The emphasis on energy efficiency standards is helping to solidify GaN’s position.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region withGallium Nitride (GaN) Power Semiconductor Market. This growth is largely attributable to the region’s burgeoning automotive industry, particularly in China and India, where electric vehicle adoption is rapidly increasing. Strong government initiatives promoting domestic semiconductor manufacturing and technological innovation are also contributing to market expansion. The Asia-Pacific region is a major manufacturing hub for consumer electronics and industrial equipment, creating significant demand for GaN power semiconductors. The presence of a large and cost-competitive manufacturing base further enhances the region’s attractiveness for GaN production and deployment. The rapid expansion of the electric vehicle market in China is a major catalyst for GaN adoption in the region.

South America

The South American Gallium Nitride (GaN) Power Semiconductor Market is relatively nascent but poised for significant growth in the coming years. The expanding renewable energy sector, particularly in Brazil and Chile, is driving demand for GaN-based power conversion systems. Increasing adoption of electric vehicles and a growing industrial base are also contributing to market potential. While the market currently represents a smaller portion of the global GaN market, the long-term growth prospects are promising, driven by increasing investments in infrastructure and technological advancements. The increasing focus on sustainable energy solutions is expected to accelerate GaN adoption in the region.

Middle East & Africa

The Middle East & Africa Gallium Nitride (GaN) Power Semiconductor Market is in its early stages of development but offers substantial long-term growth potential. The region’s ambitious plans for renewable energy deployment, particularly solar power projects, are driving demand for GaN-based power conversion systems. Expanding industrial sectors and a growing electric vehicle market are also expected to contribute to market expansion. Government initiatives aimed at diversifying energy sources and promoting technological advancement are fostering a favorable environment for GaN adoption. The significant investments in solar energy projects across the Middle East and North Africa are expected to be a key driver of GaN demand.

Report Scope

This market research report provides a comprehensive analysis of the Gallium Nitride (GaN) Power Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Gallium Nitride (GaN) Power Semiconductor Market?

-> Gallium Nitride (GaN) Power Semiconductor Market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.92 billion by 2034.

Which key companies operate Gallium Nitride (GaN) Power Semiconductor Market?

-> Key players include Infineon Technologies AG, Texas Instruments Inc., Navitas Semiconductor Corp., ON Semiconductor (onsemi), STMicroelectronics NV, and Efficient Power Conversion Corp, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy‑efficient solutions, aggressive automotive electrification targets, expanding renewable‑energy infrastructure, and cost‑reduction advances in substrate technologies such as silicon‑on‑insulator and sapphire wafers.

Which region dominates the market?

-> The reference material does not specify a single dominant region; regional performance analysis will be detailed in the full report.

What are the emerging trends?

-> Emerging trends include advancements in GaN substrate technology (SOI and sapphire), strategic partnerships to scale wafer production (e.g., Navitas with Samsung), and the development of next‑generation GaN platforms for high‑power, compact converters.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...