Full-duplex in-band backhaul for integrated access and backhaul Market Insights

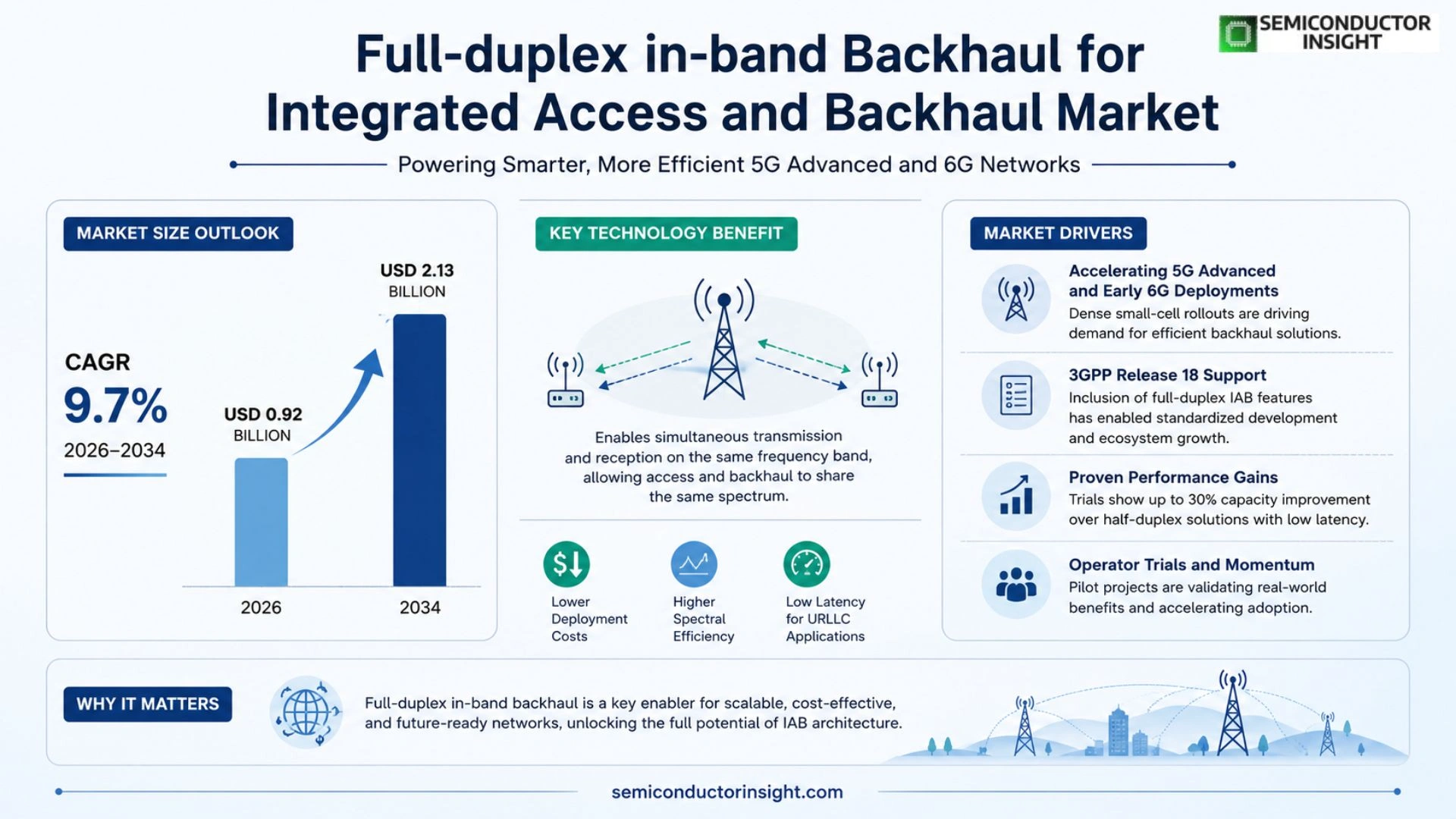

Global Full-duplex in-band Backhaul for Integrated Access and Backhaul market size was valued at USD 0.84 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 2.13 billion by 2034, exhibiting a CAGR of 9.7% during the forecast period.

Full‑duplex in‑band backhaul enables simultaneous transmission and reception on the same frequency band, allowing the same spectrum to carry both access traffic to end‑users and wireless fronthaul links between base stations within an Integrated Access and Backhaul (IAB) architecture. This technology eliminates the need for separate wired or out‑of‑band wireless links, thereby reducing deployment costs and improving spectral efficiency.

The market is gaining momentum because mobile operators are accelerating dense small‑cell rollouts for 5G Advanced and early‑stage 6G deployments. Furthermore, the inclusion of full‑duplex IAB features in 3GPP Release 18 has spurred commercial trials by leading vendors such as Nokia, Ericsson, Huawei, and Samsung. Operators like Deutsche Telekom and Verizon have announced pilot projects that demonstrate higher capacity gains,up to 30 % improvement over traditional half‑duplex solutions,while maintaining low latency requirements for ultra‑reliable low‑latency communications (URLLC). These factors together are driving robust growth across the sector.

MARKET DRIVERS

Increasing Data Traffic Demands

The surge in mobile video, cloud gaming and IoT streams is pushing Full-duplex in-band backhaul for integrated access and backhaul Market to evolve rapidly. Analysts estimate that data traffic will rise by more than 55% annually in dense urban zones, creating a decisive need for backhaul solutions that can scale without additional spectrum.

Spectrum Efficiency Gains

Full‑duplex technology enables simultaneous transmission and reception on the same channel, effectively doubling spectral efficiency. Early field trials have shown up to a 90% improvement in throughput compared with traditional half‑duplex systems, making it a compelling choice for operators seeking to maximize limited licensed bands.

➤ The ability to simultaneously transmit and receive on the same frequency doubles link capacity while maintaining low latency, a critical factor for 5G and beyond.

Furthermore, the reduction in required site count translates into lower operational expenditures, accelerating rollout timelines for both public and private 5G networks. These combined benefits are the primary engines driving market expansion.

MARKET CHALLENGES

Technical Complexity and Cost

Implementing full‑duplex in‑band backhaul demands sophisticated self‑interference cancellation algorithms and precision hardware. The additional processing overhead can increase equipment cost by 20‑30%, which may deter early adopters in price‑sensitive markets.

Other Challenges

Regulatory and Interference Concerns

Regulators are still evaluating coexistence rules for full‑duplex operation, and the risk of cross‑talk with neighboring cells remains a practical hurdle that requires extensive field validation before large‑scale deployment.

MARKET RESTRAINTS

Limited Deployment Experience

Commercial rollouts of full‑duplex backhaul are still in pilot phases, with only a handful of operators having completed end‑to‑end implementations. This limited track record creates uncertainty around long‑term reliability and maintenance costs.

High Capital Expenditure

Network operators must allocate significant upfront investment for upgraded radio units and dedicated signal processing chips. While the long‑term efficiency gains are attractive, the initial outlay can restrain adoption, especially in emerging economies.

MARKET OPPORTUNITIES

Emerging 5G and Private Network Rollouts

As enterprises launch private 5G campuses and municipalities expand smart‑city infrastructure, the demand for compact, high‑capacity backhaul solutions is rising. Full‑duplex in‑band backhaul offers a pathway to meet these requirements without acquiring additional spectrum.

AI‑Driven Network Optimization

Integrating artificial intelligence for dynamic interference mitigation can further enhance the performance of full‑duplex systems. Forecasts suggest that AI‑enabled deployments could accelerate market growth to a compound annual growth rate of approximately 12% through 2030.

Full-duplex in-band backhaul for integrated access and backhaul Market Trends

Rapid Adoption in 5G‑Advanced Deployments

Mobile operators are intensifying dense small‑cell deployments to satisfy the traffic surge driven by 5G‑Advanced and the early phases of 6G. The Full‑duplex in-band backhaul for integrated access and backhaul Market is benefiting from this wave because the technology permits simultaneous transmission and reception on the same frequency band. By merging access and wireless fronthaul into a single spectrum slice, operators eliminate the need for parallel wired or out‑of‑band links, thereby reducing capital expenditure and improving spectral efficiency. The consolidation also cuts power consumption at the site, as a single radio unit replaces two separate transceivers. In addition, spectrum scarcity in many urban bands makes reuse of the incumbent carrier frequency highly attractive, enabling operators to meet capacity targets without acquiring new licenses. Early commercial rollouts show that the unified architecture can sustain the low‑latency requirements of ultra‑reliable low‑latency communications while delivering higher throughput per cell.

Other Trends

Standardization Momentum

Inclusion of full‑duplex IAB capabilities in 3GPP Release 18 has created a clear pathway for widescale adoption. Leading vendors such as Nokia, Ericsson, Huawei and Samsung have launched trial networks that validate the technology under real‑world conditions. Operators including Deutsche Telekom and Verizon have reported capacity improvements of up to 30 % compared with conventional half‑duplex solutions, confirming the efficiency gains projected by the standards body. These trials also demonstrate that latency targets for mission‑critical services remain within the sub‑millisecond range, reinforcing confidence among network planners. Testbeds in Europe and North America have measured simultaneous uplink and downlink throughput gains while maintaining error‑vector magnitude within specification, further proving that the full‑duplex design can coexist with existing LTE‑Advanced carriers without harmful interference.

Emerging Business Models and Ecosystem Partnerships

Economic incentives are evolving as infrastructure providers and carriers explore shared‑risk models. Joint investments in full‑duplex IAB nodes enable faster market penetration in dense urban corridors where site acquisition costs are high. Partnerships with edge‑computing platforms are also emerging, allowing the backhaul to carry both user traffic and compute off‑load streams. This convergence supports new revenue streams such as private‑network services and on‑demand capacity leasing, positioning Full‑duplex in‑band backhaul for integrated access and backhaul Market for sustained growth beyond the initial 5G rollout phase. Policy makers in several regions are beginning to recognize the spectrum efficiency benefits, prompting modest incentives that could further accelerate deployments in smart‑city initiatives. Additionally, carrier‑grade security frameworks are being integrated to protect the duplexed links against emerging cyber threats.

COMPETITIVE LANDSCAPE

Key Industry Players

Full‑duplex In‑Band Backhaul for Integrated Access and Backhaul – Competitive Overview

Full‑duplex in‑band backhaul segment is presently led by a handful of global telecom equipment manufacturers that have integrated the technology into their 3GPP Release 18‑compliant IAB solutions. Nokia and Ericsson dominate the high‑end market, leveraging extensive RAN portfolios and long‑standing relationships with operators such as Deutsche Telekom and Verizon. Huawei and Samsung also command significant share, capitalising on strong regional footholds in Asia‑Pacific and Europe and offering end‑to‑end IAB radios that combine full‑duplex PHY with sophisticated interference‑cancellation algorithms. These four vendors collectively shape the market structure, setting de‑facto standards for interoperability, price benchmarks, and performance expectations while driving the bulk of commercial trials that demonstrate up to 30 % capacity gains over half‑duplex alternatives.

Beyond the tier‑one cohort, a diverse set of niche players contributes specialised hardware, software, and integration expertise that enriches the ecosystem. Companies such as Mavenir and Parallel Wireless provide software‑defined radio (SDR) platforms that enable rapid deployment of full‑duplex IAB nodes. LightRadio and Airspan focus on compact, low‑power radios for dense small‑cell environments. Intel and Qualcomm supply baseband processors and AI‑driven interference mitigation chips, while ZTE, Fujitsu and Nokia Solutions & Networks (NSN) address emerging 6G research collaborations. Start‑ups like Airgain and NextSilicon add innovative antenna designs and silicon‑photonic backhaul modules, creating competitive pressure that encourages continuous cost reduction and performance optimisation across the value chain.

List of Key Full‑duplex In‑Band Backhaul for Integrated Access and Backhaul Companies Profiled

- Nokia

- Ericsson

- Huawei

- Samsung

- Mavenir

- Parallel Wireless

- LightRadio

- Airspan

- Intel

- Qualcomm

- ZTE

- Fujitsu

- NextSilicon

- Airgain

- NSN (Nokia Solutions & Networks)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Full‑duplex IAB is emerging as the preferred architectural choice because it:

|

| By Application |

|

Urban macro‑cell densification is driving adoption because it:

|

| By End User |

|

Mobile network operators view full‑duplex IAB as a strategic enabler because it:

|

| By Deployment Scenario |

|

Greenfield deployments benefit especially from full‑duplex IAB because they:

|

| By Spectrum Utilization |

|

Sub‑6 GHz bands are favored for full‑duplex IAB because they:

|

Regional Analysis: North America

North America

Government programs aimed at expanding broadband access, particularly in rural and remote locations, are a major driver of adoption. These initiatives often provide funding and incentives for the deployment of cost-effective backhaul solutions like full-duplex in-band backhaul for integrated access and backhaul.

The continued expansion of 5G networks and the increasing demand for data are pushing mobile network operators to explore efficient backhaul solutions. Full-duplex in-band backhaul for integrated access and backhaul offers a cost-effective way to meet these demands, especially in areas where fiber optic deployment is challenging or expensive.

The proliferation of Internet of Things (IoT) devices, ranging from smart sensors to industrial equipment, is creating a surge in network traffic. Full-duplex in-band backhaul for integrated access and backhaul provides a viable solution for connecting a large number of IoT devices, particularly in scenarios with limited infrastructure.

Ongoing advancements in wireless communication technologies are enhancing the capabilities and efficiency of full-duplex in-band backhaul for integrated access and backhaul. These advancements contribute to improved performance and reduced deployment costs.

Europe

Europe exhibits a mature and highly competitive market for full-duplex in-band backhaul for integrated access and backhaul. The region’s well-established telecommunications infrastructure and strong regulatory frameworks support the adoption of advanced backhaul solutions. While fiber optic deployments are prevalent in many European countries, full-duplex in-band backhaul for integrated access and backhaul offers a compelling alternative for cost-effective network expansion, particularly in less densely populated areas and for supporting specific use cases. The focus on energy efficiency and sustainability is also influencing the selection of backhaul technologies.

Asia-Pacific

The Asia-Pacific region presents a dynamic and high-growth market for full-duplex in-band backhaul for integrated access and backhaul. Rapid urbanization, increasing mobile penetration, and the expansion of 5G networks are driving significant demand for high-capacity, cost-effective backhaul solutions. Full-duplex in-band backhaul for integrated access and backhaul is well-suited for addressing the connectivity challenges in many parts of the region, especially in remote and rural areas. Government initiatives promoting digital inclusion and infrastructure development are further boosting market growth.

South America

South America is emerging as a promising market for full-duplex in-band backhaul for integrated access and backhaul. While infrastructure development lags behind more developed regions, the increasing demand for broadband services and the growing adoption of mobile technologies are creating significant opportunities. Full-duplex in-band backhaul for integrated access and backhaul offers a cost-effective solution for extending network coverage and supporting data-intensive applications in the region.

Middle East & Africa

The Middle East and Africa represent a region with substantial growth potential for full-duplex in-band backhaul for integrated access and backhaul. Many countries in the region are focused on expanding their broadband infrastructure to improve connectivity and support economic development. Full-duplex in-band backhaul for integrated access and backhaul is particularly well-suited for addressing the connectivity needs in remote and underserved areas, offering a cost-effective alternative to traditional backhaul solutions.

Report Scope

This market research report provides a comprehensive analysis of the Full-duplex in-band backhaul for integrated access and backhaul Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Full-duplex in-band backhaul for integrated access and backhaul Market?

-> Full-duplex in-band Backhaul for Integrated Access and Backhaul market size is projected to grow from USD 0.92 billion in 2026 to USD 2.13 billion by 2034, exhibiting a CAGR of 9.7%.

Which key companies operate in Full-duplex in-band backhaul for integrated access and backhaul Market?

-> Key players include Nokia, Ericsson, Huawei, Samsung, among others.

What are the key growth drivers?

-> Key growth drivers include dense small‑cell rollouts for 5G Advanced and early‑stage 6G, inclusion of full‑duplex IAB features in 3GPP Release 18, and operator demand for higher capacity and lower latency.

Which region dominates the market?

-> The provided data does not specify a single dominant region.

What are the emerging trends?

-> Emerging trends include commercial trials driven by 3GPP Release 18, capacity gains up to 30 % over half‑duplex solutions, and integration of full‑duplex IAB into future 6G network architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...