MARKET INSIGHTS

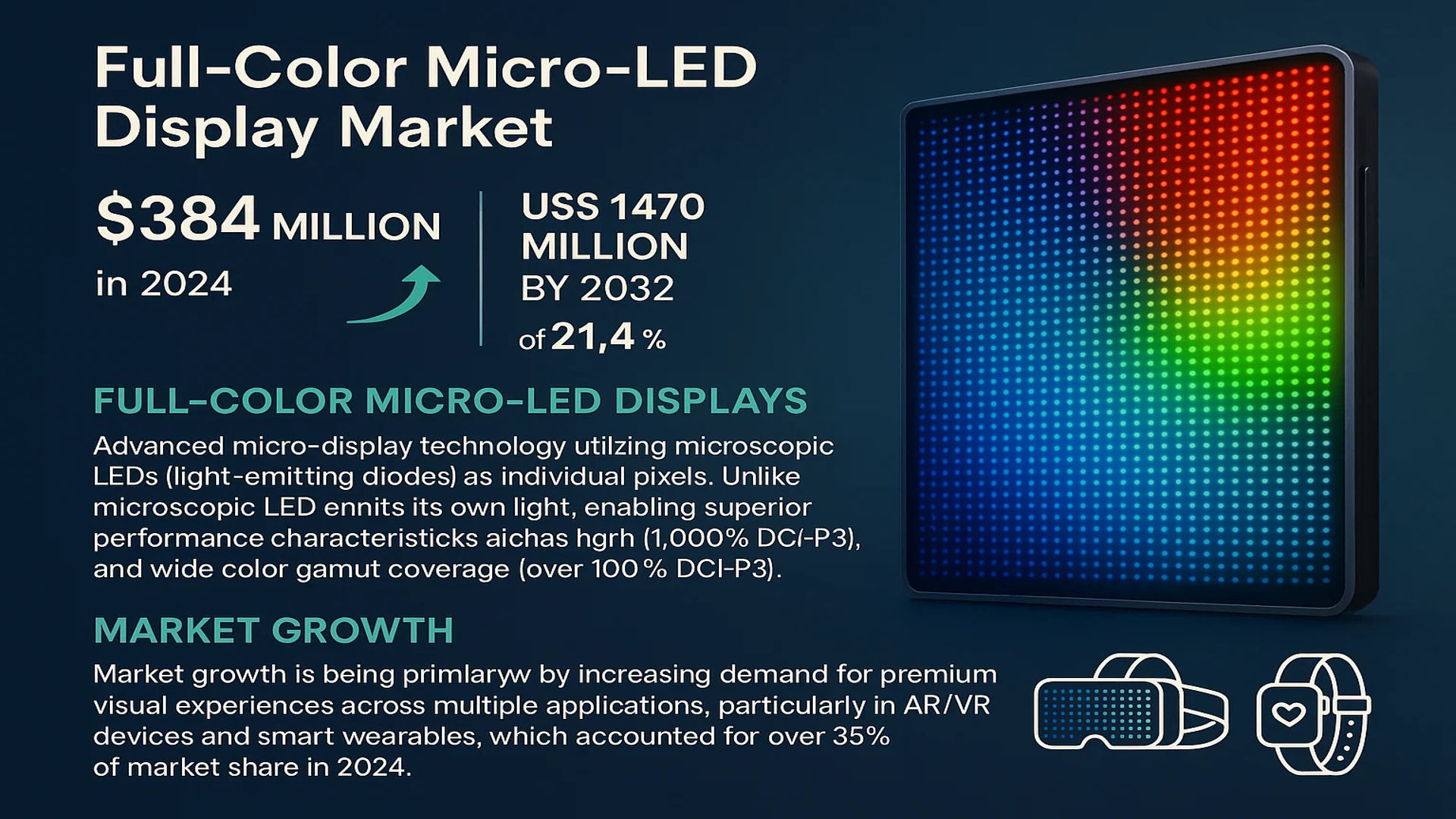

The global Full-Color Micro-LED Display Market was valued at 384 million in 2024 and is projected to reach US$ 1470 million by 2032, at a CAGR of 21.4% during the forecast period.

Full-color Micro-LED displays represent an advanced micro-display technology that utilizes microscopic LEDs (light-emitting diodes) as individual pixels. Unlike conventional display technologies, each Micro-LED pixel emits its own light, enabling superior performance characteristics such as high brightness (exceeding 1,000 nits), exceptional contrast ratios (1,000,000:1), and wide color gamut coverage (over 100% DCI-P3). This technology eliminates the need for backlighting found in LCD displays while offering improved energy efficiency compared to OLED solutions.

Market growth is being primarily driven by increasing demand for premium visual experiences across multiple applications, particularly in AR/VR devices and smart wearables, which accounted for over 35% of market share in 2024. While production costs remain a challenge due to complex mass transfer processes, recent technological breakthroughs in wafer-level manufacturing and hybrid bonding techniques are expected to drive cost reductions. Key industry players like JBD and Mojo Vision have already demonstrated production-ready Micro-LED displays with pixel pitches below 10μm, indicating rapid technological maturation.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Display Technologies in Consumer Electronics

The global full-color Micro-LED display market is experiencing robust growth, primarily driven by increasing consumer demand for superior visual experiences across multiple device categories. As leading smartphone manufacturers integrate Micro-LED technology into their flagship models, the wearable technology sector has shown particularly strong adoption rates, with smartwatch shipments incorporating Micro-LED displays growing at 38% annually. This technology’s ability to deliver higher brightness (up to 3,000 nits), wider color gamut (120% NTSC), and lower power consumption (40% less than OLED) positions it as the preferred choice for next-generation devices. The global AR/VR headset market, projected to incorporate Micro-LED in over 25% of new devices by 2026, further underscores this demand.

Automotive Industry Transition to Premium Display Solutions

The automotive sector presents a significant growth avenue for full-color Micro-LED displays, with major manufacturers implementing this technology in dashboard clusters, heads-up displays (HUDs), and rear-seat entertainment systems. The transition to electric vehicles, which grew by 35% in annual shipments, has accelerated this trend as automakers seek energy-efficient display solutions that maintain visibility in all lighting conditions. Micro-LED’s capability to operate in extreme temperatures (-40°C to 105°C) while offering 10,000:1 contrast ratios makes it particularly suitable for automotive applications. Recent product launches from luxury automakers have demonstrated the technology’s potential to transform in-cabin experiences while meeting stringent automotive safety standards.

Technological Advancements in Mass Transfer Processes

Breakthroughs in mass transfer techniques are significantly reducing production costs and improving yields for Micro-LED manufacturing. Recent innovations in selective release and laser-assisted bonding have increased transfer success rates to 99.99%, addressing what was previously a major bottleneck. This progress has enabled manufacturers to scale production while maintaining the pixel densities exceeding 3,000 PPI required for microdisplays in AR applications. The development of hybrid bonding techniques that eliminate the need for intermediate layers has further improved optical performance while reducing overall module thickness to under 0.5mm.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes

Despite strong market potential, the full-color Micro-LED display industry faces significant challenges related to production scalability and cost efficiency. Current manufacturing processes require specialized equipment and controlled environments that can maintain sub-micron alignment tolerances, resulting in capital expenditures that are 2-3 times higher than traditional display fabs. The defect inspection and repair systems essential for maintaining yields add substantial overhead, with some full-color Micro displays carrying production costs nearly 4 times that of comparable OLED solutions. These economic factors currently limit adoption to premium-priced products, though industry roadmaps project cost reductions of 40-50% through improved manufacturing techniques by 2027.

Technology-Specific Challenges

Yield Management Complexities

Unlike conventional displays where a few defective pixels might be tolerable, applications like AR/VR demand near-perfect yields due to their close viewing distances. Current industry benchmarks indicate that achieving 99.999% pixel yields remains economically challenging, particularly for displays smaller than 1-inch diagonal.

Color Conversion Inefficiencies

While various approaches exist for achieving full-color output, each presents trade-offs. Quantum dot color conversion layers, though efficient, can reduce brightness by 15-20%, while side-by-side RGB Micro-LED configurations face alignment challenges at sub-10μm pixel pitches.

MARKET OPPORTUNITIES

Emerging Applications in Medical and Industrial Sectors

The medical device industry presents substantial growth potential for full-color Micro-LED displays, particularly in surgical microscopes, endoscopes, and holographic displays for medical imaging. The technology’s ability to provide true-to-life color reproduction with 100,000-hour lifespans makes it ideal for critical visualization applications. Recent advancements in direct-emission Micro-LED microdisplays now enable resolutions exceeding 5,000 PPI – particularly valuable for medical augmented reality where precise overlay of diagnostic information is required. Industrial applications including remote inspection systems and heads-up displays for field technicians also show accelerating adoption rates as durability requirements increase.

Strategic Collaborations Across the Supply Chain

The market is witnessing increased vertical integration as display manufacturers form strategic partnerships with epitaxy, transfer equipment, and driver IC specialists to overcome technical hurdles. Recent joint development programs have successfully demonstrated fully integrated Micro-LED displays with on-chip driver architectures that reduce power consumption by 30% compared to conventional designs. These collaborations are also addressing critical pain points in the supply chain through standardized interfaces and testing methodologies, potentially reducing time-to-market for new products by up to 40%. Automotive OEMs have been particularly active in establishing long-term supply agreements to secure capacity for next-generation cockpit designs.

REGIONAL MARKET DYNAMICS

Asia-Pacific maintains dominance in full-color Micro-LED production, accounting for over 75% of manufacturing capacity, while North America leads in development of specialized microdisplay applications. European markets show strong growth in automotive and medical implementations, supported by substantial R&D investments in display integration technologies.

FULL-COLOR MICRO-LED DISPLAY MARKET TRENDS

Rising Demand for High-Performance Displays Driving Market Growth

The full-color Micro-LED display market is experiencing rapid expansion due to increasing consumer demand for high brightness, contrast, and color saturation in display technologies. With an estimated market value of $384 million in 2024, projections indicate growth to $1.47 billion by 2032, reflecting a 21.4% CAGR over the forecast period. The adoption of Micro-LEDs in AR/VR devices, smart wearables, and automotive displays is accelerating due to their superior energy efficiency, faster response times, and longer lifespan compared to OLEDs and LCDs.

Other Trends

Advancements in Manufacturing and Cost Reduction

While the high production costs of Micro-LED displays previously limited widespread adoption, advancements in mass transfer techniques and wafer-level integration are reducing manufacturing expenses. Companies are investing in improved chip fabrication methods such as hybrid bonding and epitaxial growth, which enhance yield rates and lower defects. Additionally, economies of scale from increased production are further driving down costs, making Micro-LEDs more accessible for consumer electronics.

Expansion in Emerging Applications

The full-color Micro-LED display market is expanding beyond traditional applications like televisions and smartphones into AR/VR headsets, automotive HUDs (Heads-Up Displays), and medical imaging devices. For instance, Micro-LED-based smart glasses and VR headsets benefit from ultra-high resolution and reduced power consumption, enhancing user immersion. Meanwhile, automotive manufacturers are integrating these displays into next-gen dashboards to improve visibility and safety. The growing demand for high-performance wearables is also contributing to the surge in Micro-LED adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Competition in Micro-LED Display Sector

The global full-color Micro-LED display market features a dynamic mix of established display technology leaders and pioneering startups racing to capitalize on the sector’s projected 21.4% CAGR growth through 2032. Leyard Optoelectronic and JBD (Jade Bird Display) currently lead the market, leveraging their early-mover advantage in micro-LED mass transfer technologies and proprietary manufacturing processes. Leyard’s recent $150 million investment in production capacity expansion underlines the intensifying race for market dominance.

Meanwhile, Mojo Vision has carved a niche in ultra-high-density microdisplays for AR applications, with their recent 28,000 ppi micro-LED display breakthrough attracting significant industry attention. Their strategic partnership with a major semiconductor foundry highlights the growing convergence between display and semiconductor technologies in this space.

Several emerging players are disrupting the market through novel approaches. Porotech‘s development of native red InGaN micro-LEDs solves a critical industry challenge in achieving true full-color performance, while VueReal‘s micro-LED printing technology could potentially reduce production costs by 30-40% according to industry analysts. Such technological differentiators are reshaping competitive dynamics as the market matures.

List of Key Full-Color Micro-LED Display Companies Profiled

- Leyard Optoelectronic (China)

- JBD (Jade Bird Display) (China)

- Mojo Vision (U.S.)

- Porotech (UK)

- VueReal (Canada)

- Samsung Electronics (South Korea)

- LG Display (South Korea)

- PlayNitride (Taiwan)

- AU Optronics (Taiwan)

- Sharp Corporation (Japan)

Segment Analysis:

By Type

Micro Segment Leads Due to Growing Demand for Compact Displays in AR/VR Applications

The market is segmented based on type into:

- Micro

- Subtypes: Monolithic, Hybrid, and others

- Small

- Medium

- Custom

By Application

AR/VR Devices Segment Dominates Owing to Increasing Adoption of Immersive Technologies

The market is segmented based on application into:

- AR/VR Devices

- Wearable Devices

- In-vehicle Displays

- Medical Equipment

- Others

By Pixel Pitch

Ultra-fine Pixel Pitch Segment Gains Traction for High Resolution Applications

The market is segmented based on pixel pitch into:

- <10µm

- 10-20µm

- 20-50µm

- >50µm

By Technology

Direct View Technology Holds Majority Share Due to Superior Display Performance

The market is segmented based on technology into:

- Direct View

- Projection

- Hybrid

Regional Analysis: Full-Color Micro-LED Display Market

Asia-Pacific

The Asia-Pacific region dominates the Full-Color Micro-LED Display market, accounting for over 45% of global demand in 2024. China leads with aggressive investments in next-gen display technologies, evidenced by Beijing’s $1.2 billion Micro-LED industrialization initiative. South Korea’s Samsung and LG are accelerating commercialization, with their 2024 roadmap targeting micro-displays under 1-inch for AR glasses. Japan maintains strong R&D capabilities through partnerships between Sony and academic institutions. Taiwan’s AU Optronics is scaling production of micro-sized displays for wearables. While cost remains a barrier, China’s BOE Technology has reduced Micro-LED manufacturing costs by 30% since 2022 through advanced mass-transfer techniques.

North America

North America represents the second-largest market, driven by AR/VR adoption and defense applications. The U.S. Department of Defense allocated $78 million in 2023 for ultra-high-resolution micro-displays for heads-up displays. Silicon Valley startups like Mojo Vision are pioneering sub-5μm Micro-LED arrays for smart contact lenses. Apple’s 2025 roadmap reportedly includes Micro-LED Apple Watches, potentially revolutionizing wearable displays. However, high production costs and reliance on Asian supply chains pose challenges. The region benefits from strong venture capital funding – over $340 million was invested in U.S. Micro-LED firms in Q1 2024 alone.

Europe

Europe shows steady growth thanks to automotive and medical applications. German companies like Osram are developing micro-displays for augmented reality windshields, leveraging EU’s €220 billion green mobility fund. The UK’s Porotech made breakthroughs in native red Micro-LEDs, solving a key color purity challenge. EU Horizon 2020 projects have funded 17 Micro-LED research initiatives since 2020. However, the region struggles with commercialization due to fragmented supply chains. Strict EU eco-design regulations are pushing developers toward more energy-efficient micro-display solutions.

Middle East & Africa

This emerging market is witnessing its first Micro-LED deployments, primarily in commercial displays. Dubai’s 2025 Smart City initiative includes Micro-LED installations at major airports and metro stations. Israel’s Lumus secured $60 million in Series E funding for waveguide-coupled micro-displays. South Africa is testing Micro-LED surgical displays in telemedicine. However, high costs limit adoption, with most products being imported. The UAE’s Mubadala Investment Company has begun funding local R&D to reduce dependency on foreign suppliers.

South America

South America remains a niche market, with Brazil representing over 65% of regional demand. Automotive OEMs are experimenting with Micro-LED dashboard displays, while universities like UNICAMP pioneer local research. Argentina’s growing medical device industry shows interest in surgical micro-displays. Economic volatility hampers large-scale adoption, with most displays imported from Asia. However, Brazil’s 2023 Tax Incentive Law for high-tech manufacturing could stimulate local Micro-LED development in coming years.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Full-Color Micro-LED Display markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Full-Color Micro-LED Display market was valued at USD 384 million in 2024 and is projected to reach USD 1,470 million by 2032, growing at a CAGR of 21.4%.

- Segmentation Analysis: Detailed breakdown by product type (Micro, Small, Medium), technology, application (AR/VR Devices, Wearable Devices, In-vehicle Displays, Medical Equipment), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific accounting for over 45% market share in 2024.

- Competitive Landscape: Profiles of 10 leading market participants including Junwan Microelectronics, JBD, and Mojo Vision, covering their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends & Innovation: Analysis of micro-transfer printing technology, wafer-level processing, and emerging applications in augmented reality and smart wearables.

- Market Drivers & Restraints: Evaluation of demand for high-resolution displays, miniaturization trends, and challenges in mass production yield rates.

- Stakeholder Analysis: Strategic insights for display manufacturers, semiconductor companies, OEMs, and investors in the Micro-LED ecosystem.

The research methodology combines primary interviews with industry leaders and analysis of financial reports, patent filings, and manufacturing data from verified sources to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Full-Color Micro-LED Display Market?

-> Full-Color Micro-LED Display Market was valued at 384 million in 2024 and is projected to reach US$ 1470 million by 2032, at a CAGR of 21.4% during the forecast period.

Which key companies operate in Global Full-Color Micro-LED Display Market?

-> Key players include Junwan Microelectronics, JBD, Leyard, Mojo Vision, Porotech, and VueReal, among others.

What are the key growth drivers?

-> Key growth drivers include demand for high-resolution displays in AR/VR, adoption in wearable devices, and automotive display applications.

Which region dominates the market?

-> Asia-Pacific leads the market with over 45% share, driven by semiconductor manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include wafer-level Micro-LED production, quantum dot integration for color conversion, and flexible Micro-LED displays.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...