MARKET INSIGHTS

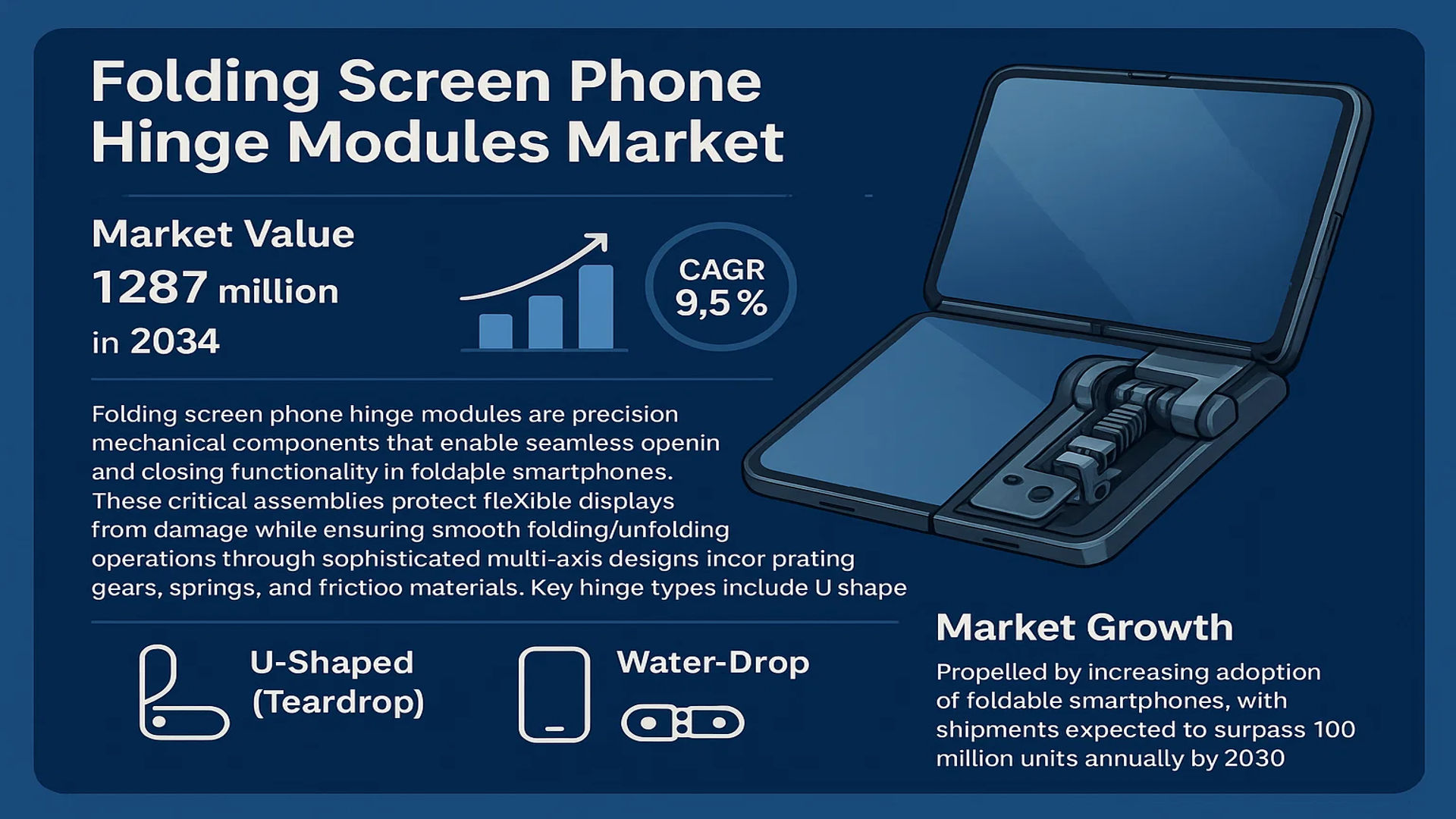

The global Folding Screen Phone Hinge Modules Market was valued at 1287 million in 2024 and is projected to reach US$ 2601 million by 2032, at a CAGR of 9.5% during the forecast period.

Folding screen phone hinge modules are precision mechanical components that enable seamless opening and closing functionality in foldable smartphones. These critical assemblies protect flexible displays from damage while ensuring smooth folding/unfolding operations through sophisticated multi-axis designs incorporating gears, springs, and friction materials. Key hinge types include U-shaped (teardrop) and water-drop variants, each offering distinct durability and form factor advantages.

The market growth is propelled by increasing adoption of foldable smartphones, with shipments expected to surpass 100 million units annually by 2030. While Samsung dominates current production, Chinese manufacturers like Huawei and Xiaomi are accelerating market expansion through competitive pricing. However, technical challenges around hinge durability (typically rated for 200,000+ folds) and manufacturing precision continue influencing R&D investments among key players including Amphenol, KH Vatec, and AAC Technologies.

MARKET DYNAMICS

MARKET DRIVERS

Growing Popularity of Foldable Smartphones to Accelerate Market Growth

The global folding screen phone hinge modules market is witnessing robust growth due to increasing consumer demand for foldable smartphones. Shipments of foldable phones are projected to grow from approximately 16.3 million units in 2024 to over 35 million units by 2027, representing a compound annual growth rate of 28%. Leading smartphone manufacturers are investing heavily in foldable display technology, with major brands collectively allocating over $2.5 billion annually in R&D. As the form factor becomes more mainstream, component suppliers are scaling up production capacities, creating significant demand for high-quality hinge modules that can withstand repeated folding cycles.

Technological Advancements in Hinge Designs to Fuel Market Expansion

Breakthroughs in hinge module engineering are enabling thinner, lighter, and more durable folding mechanisms. Recent innovations include multi-link hinge systems that reduce stress on flexible displays, allowing for folding radii as tight as 1.8mm without screen damage. Water drop-style hinge designs, which accounted for nearly 60% of hinge module shipments in 2024, help minimize creasing on foldable displays. Major manufacturers are developing hinge modules rated for over 300,000 folding cycles while maintaining module thickness below 4mm. These technological improvements are critical for enhancing user experience and driving consumer adoption of foldable devices.

Expanding Ecosystem of Foldable Devices to Create New Opportunities

The application of folding screen technology is expanding beyond smartphones into tablets, laptops, and wearable devices. This diversification is creating additional demand for hinge modules across multiple product categories. Industry projections suggest that non-smartphone applications could account for around 25% of the hinge module market by 2027. The convergence of foldable technology with features like rollable displays and multi-fold configurations is opening new avenues for innovation. Some manufacturers are already developing hinge solutions compatible with next-generation materials like ultra-thin glass substrates and transparent conductive films.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes to Limit Market Penetration

The sophisticated nature of folding screen hinge modules results in production costs that are significantly higher than conventional hinges, with some premium hinge modules costing manufacturers over $50 per unit. The manufacturing process involves precision machining, specialized alloys, and complex assembly that requires cleanroom environments. These factors contribute to device prices that remain nearly 70-80% higher than comparable traditional smartphones, limiting mass-market adoption. Additionally, the industry faces challenges in scaling production to meet potential demand while maintaining strict quality standards for fold endurance and durability.

Materials Science Challenges to Impact Hinge Module Performance

Developing hinge materials that balance strength, thickness, and fatigue resistance remains a significant technical challenge. Current hinge modules require specialized alloys and lubricants to prevent wear over thousands of folding cycles, but these solutions add weight and complexity. The industry is also grappling with compatibility issues between hinge materials and evolving display technologies. Some manufacturers have reported failure rates of up to 3-5% in initial hinge module batches, primarily due to material fatigue and component misalignment issues. These technical hurdles increase warranty costs and may delay product launches.

MARKET CHALLENGES

Supply Chain Vulnerabilities to Affect Market Stability

The folding screen hinge module market faces significant supply chain challenges due to the specialized nature of components and manufacturing processes. The industry relies on a limited number of suppliers for critical materials like specialized bearings and ultra-thin stainless steel alloys, creating potential bottlenecks. Geopolitical factors and trade restrictions have caused fluctuations in the availability of key materials, with some manufacturers experiencing lead times extending beyond 6 months for certain components. This fragile supply chain situation could hinder the industry’s ability to scale up production in response to growing demand.

Intellectual Property Conflicts to Slow Down Innovation

The rapid development of folding screen hinge technology has led to an increasingly complex patent landscape, with over 1,200 active patents related to hinge mechanisms filed in the past five years. Several high-profile intellectual property disputes have emerged between major manufacturers, resulting in legal battles that have delayed product launches. Smaller players face particular challenges in navigating this competitive environment, as licensing costs for essential hinge technologies can account for up to 15% of component costs. This situation creates barriers to entry and may slow the pace of innovation in the market.

MARKET OPPORTUNITIES

Emerging Material Technologies to Enable Next-Generation Hinge Solutions

Breakthroughs in material science present significant opportunities for the folding screen hinge module market. Researchers are developing new composite materials that could reduce hinge weight by 30-40% while maintaining strength. Shape-memory alloys and self-lubricating materials show promise for significantly extending hinge lifespans beyond current standards. Some manufacturers are experimenting with integrated sensor systems within hinge modules to enable new device functionalities. These advancements could lead to hinge solutions that are not only more durable but also enable innovative form factors and user interactions with foldable devices.

Expansion into Emerging Markets to Drive Volume Growth

As the technology matures and production costs decline, emerging markets present significant opportunities for market expansion. Manufacturers are developing cost-optimized hinge solutions specifically for price-sensitive markets, with some Asian suppliers offering hinge modules at 40-50% lower costs than premium alternatives. Localization of production in regions like Southeast Asia and India is expected to reduce logistics costs and improve supply chain resilience. Some analysts project that emerging markets could account for over 35% of foldable device shipments by 2027, creating substantial opportunities for hinge module suppliers to capitalize on this growth.

FOLDING SCREEN PHONE HINGE MODULES MARKET TRENDS

Increasing Adoption of Foldable Smartphones Drives Market Expansion

The global folding screen phone hinge modules market is experiencing substantial growth, fueled by the rising demand for foldable smartphones among consumers seeking innovative and portable devices. The market was valued at $1.28 billion in 2024 and is projected to reach $2.6 billion by 2032, growing at a compound annual growth rate (CAGR) of 9.5%. This surge is primarily driven by advancements in hinge technology, which enhances durability and seamless folding mechanisms. Key manufacturers are leveraging high-precision engineering to minimize creasing, reduce wear-and-tear, and improve hinge longevity beyond 200,000 folds—addressing a critical consumer concern.

Other Trends

Shift Toward Water Drop-Type Hinges

The preference for water drop-type hinges is growing due to their ability to create wider folding radii, reducing stress on flexible displays. Unlike traditional U-shape hinges, these designs eliminate visible creases while maintaining device slimness—a key selling point for premium brands. By 2032, water drop hinges are anticipated to capture over 45% of the market share, with U-shape variants gradually declining in dominance. Additionally, these hinges enable slimmer device profiles, aligning with consumer demand for portability without compromising screen size.

Automation and Material Innovations Enhance Production Efficiency

Manufacturers are increasingly adopting automated assembly lines to meet the precision demands of hinge production while reducing costs. The integration of ultra-thin stainless steel alloys and ceramics has improved hinge resilience against dust and mechanical fatigue, addressing early-generation reliability issues. Collaborative R&D efforts between display panel producers and hinge manufacturers are accelerating the development of hybrid materials that balance flexibility with structural integrity. These innovations are critical as foldable phone shipments are forecasted to exceed 100 million units annually by 2030, necessitating scalable and cost-effective production solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Competition in Foldable Hinge Module Market

The global Folding Screen Phone Hinge Modules market features a highly competitive landscape with key players primarily concentrated in Asia, given the region’s dominance in consumer electronics manufacturing. While the market remains semi-consolidated, technological differentiation has become a critical battleground as companies compete to develop more durable and slim-profile hinge solutions. Amphenol and Asia Vital Components (AVC) currently lead the market share, benefiting from early-mover advantage in supplying hinge modules for flagship foldable devices from Samsung and Huawei.

Chinese manufacturers like Dongguan Huanli Intelligent Technology and AAC Technologies are rapidly gaining ground through aggressive R&D investments and cost-competitive manufacturing. These companies have particularly strengthened their position by developing Water Drop Type hinge mechanisms that minimize screen creasing – a persistent challenge in foldable devices. Meanwhile, South Korea’s KH Vatec maintains technological leadership in ultra-thin hinge designs through patented nano-level precision engineering techniques.

The market is witnessing intensified competition in material science innovations, with companies like NBTM New Materials developing specialized alloys that combine lightweight properties with extreme durability. Strategic partnerships with display manufacturers have become crucial, as hinge performance directly impacts flexible screen longevity. JARLLYTEC recently secured a multi-year supply agreement with a leading Chinese smartphone maker by demonstrating a hinge lifespan exceeding 300,000 folds in testing.

List of Key Folding Screen Hinge Module Manufacturers

- Amphenol (U.S.)

- Asia Vital Components (AVC) (Taiwan)

- KH Vatec (South Korea)

- JARLLYTEC (China)

- NBTM New Materials (China)

- AAC Technologies (China)

- Dongguan Huanli Intelligent Technology (China)

- Shanghai TOMI Electronic Material (China)

- S-Connect (South Korea)

- FINE M-TEC (Japan)

- Jiangsu Gian Technology (China)

- DONG GUAN JINFENG ELECTRON (China)

- Kunshan Kersen Science & Technology (China)

Segment Analysis:

By Type

U Shape Hinge Segment Holds Major Market Share Due to Its Wide Adoption in Foldable Phones

The market is segmented based on type into:

- U Shape

- Water Drop Type

- Others

By Application

Foldable Inward/Outward Phone Segment Leads Due to Increasing High-End Smartphone Demand

The market is segmented based on application into:

- Foldable Clamshell Phone

- Foldable Inward/Outward Phone

By Material

Stainless Steel Segment Dominates Due to High Durability Requirements

The market is segmented based on material into:

- Stainless Steel

- Titanium Alloy

- Others

By Sales Channel

OEM Segment Accounts for Majority Share Due to Direct Integration with Smartphone Manufacturers

The market is segmented based on sales channel into:

- OEM (Original Equipment Manufacturer)

- Aftermarket

Regional Analysis: Folding Screen Phone Hinge Modules Market

Asia-Pacific

The Asia-Pacific region dominates the Folding Screen Phone Hinge Modules market, accounting for the largest revenue share in 2024, driven primarily by China, South Korea, and Japan. This leadership stems from the region’s concentration of smartphone manufacturers (Samsung, Huawei, Xiaomi) and hinge component suppliers (AAC Technologies, KH Vatec). China alone contributes over 60% of global production, supported by aggressive R&D investments in flexible display technologies. South Korea’s Samsung Display and its proprietary Ultra Thin Glass (UTG) technology further strengthen the region’s supply chain. However, intense competition among local manufacturers has led to price pressures, forcing companies to focus on innovation in hinge durability (tested for 200,000+ folds) and slimness (<1.4mm thickness) to differentiate offerings.

North America

North America represents the second-largest market, fueled by consumer willingness to adopt premium foldable devices (average selling price >$1,200) and the presence of technology giants like Motorola (Razr series). The U.S. market benefits from collaborations between hinge module specialists (Amphenol) and Silicon Valley firms developing next-gen foldable designs. Regulatory standards for material safety and electromagnetic interference (FCC compliance) add production costs but ensure product reliability. Though trailing Asia in manufacturing scale, the region excels in patent filings for novel hinge mechanisms (174 U.S. patents granted in 2023), particularly for dust-resistance solutions addressing a key industry pain point.

Europe

Europe’s market growth is tempered by cautious consumer adoption of foldable phones (just 3.2% of total smartphone sales in 2024) but shows promise in B2B applications like foldable tablets for healthcare and field services. EU regulations on conflict minerals and e-waste recycling (WEEE Directive) require hinge manufacturers to implement sustainable material sourcing—16% of European hinges now use recycled stainless steel. German engineering firms lead in precision tooling for hinge assembly lines, while UK-based startups pioneer graphene-enhanced hinges that reduce weight by 30%. The region’s focus on product longevity aligns with hinge durability enhancements but faces cost barriers against Asian imports.

South America

South America remains a nascent market where foldable phone adoption is limited to affluent urban consumers (Brazil accounts for 68% of regional demand). Economic instability discourages local production—most hinges are imported from China, with tariffs adding 12-18% to final device costs. However, Mexico’s proximity to the U.S. has attracted some hinge module assembly plants serving the North American market. The lack of standardized testing facilities for hinge fatigue (most devices imported) creates quality concerns, though Chile and Colombia are establishing certification centers to boost consumer confidence. The region shows potential for mid-range foldables if localized assembly can reduce prices below $800.

Middle East & Africa

The MEA market is emerging through luxury-focused demand in UAE (where foldables constitute 7% of premium smartphone sales) and enterprise adoption in South Africa (mining and oilfield rugged devices). Hinge suppliers face challenges from extreme climate conditions—sand resistance is a key design requirement in GCC countries, while humidity resistance drives specifications in coastal Africa. Israel’s tech ecosystem contributes innovative hinge locking mechanisms (32 related patents filed in 2023). Though infrastructure gaps hinder widespread adoption, the region’s young demographic and 5G rollout present long-term opportunities—hinge module sales are projected to grow at 11.2% CAGR through 2032 as disposable incomes rise.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Folding Screen Phone Hinge Modules markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Folding Screen Phone Hinge Modules market was valued at USD 1,287 million in 2024 and is projected to reach USD 2,601 million by 2032, growing at a CAGR of 9.5%.

- Segmentation Analysis: Detailed breakdown by product type (U Shape, Water Drop Type, Others) and application (Foldable Clamshell Phone, Foldable Inward/Outward Phone) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. China and the U.S. are key growth markets.

- Competitive Landscape: Profiles of leading market participants including Amphenol, Asia Vital Components (AVC), KH Vatec, JARLLYTEC, and NBTM New Materials, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging hinge technologies, material advancements, and durability improvements for foldable displays.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for foldable smartphones versus challenges in hinge durability and manufacturing complexity.

- Stakeholder Analysis: Insights for component suppliers, smartphone OEMs, investors, and policymakers regarding the evolving foldable device ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Folding Screen Phone Hinge Modules Market?

-> Folding Screen Phone Hinge Modules Market was valued at 1287 million in 2024 and is projected to reach US$ 2601 million by 2032, at a CAGR of 9.5% during the forecast period.

Which key companies operate in Global Folding Screen Phone Hinge Modules Market?

-> Key players include Amphenol, Asia Vital Components (AVC), KH Vatec, JARLLYTEC, NBTM New Materials, AAC Technologies, and Dongguan Huanli Intelligent Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of foldable smartphones, technological advancements in hinge mechanisms, and increasing investments by major smartphone manufacturers.

Which region dominates the market?

-> Asia-Pacific is the largest market, led by China and South Korea, while North America shows strong growth potential.

What are the emerging trends?

-> Emerging trends include development of ultra-thin hinge modules, multi-axis hinge systems, and integration of advanced materials for enhanced durability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...