Flexible solar cells market Insights

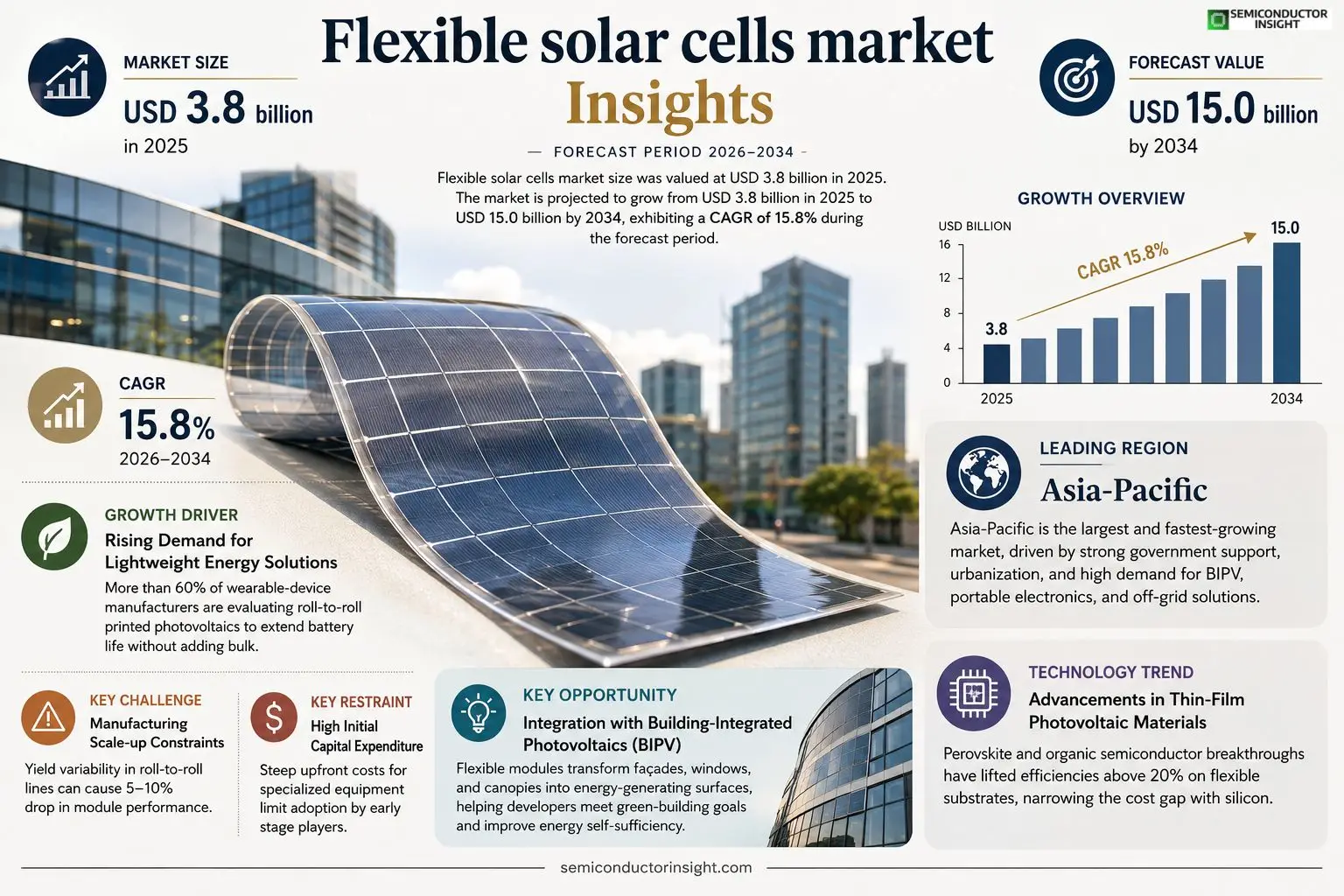

Flexible solar cells market size was valued at USD 3.8 billion in 2025. The market is projected to grow from USD 3.8 billion in 2025 to USD 15.0 billion by 2034, exhibiting a CAGR of 15.8% during the forecast period.

Flexible solar cells are lightweight, thin‑film photovoltaic devices that can be bent or rolled without losing efficiency.They typically employ materials such as amorphous silicon, CIGS (copper indium gallium selenide), or organic polymers,

enabling integration onto curved surfaces, building facades, vehicles, and portable electronics.The market is experiencing rapid growth due to several factors,including rising demand for renewable‑energy integration in urban infrastructure,decreasing production costs driven by roll‑to‑roll manufacturing advances,and supportive government policies promoting clean‑energy adoption.Furthermore,collaborations between leading manufacturers and research institutions are accelerating technology maturation.For instance,in March 2024,Company A partnered with University B to scale up CIGS production lines.

Companies such as XYZ Corp., ABC Energy,and SunTech Innovations are key players operating in the market with extensive product portfolios.

MARKET DRIVERS

Rising Demand for Lightweight Energy Solutions

Flexible solar cells market is being propelled by the need for portable and low‑weight power sources in consumer electronics, UAVs, and disaster‑relief kits. Recent surveys indicate that more than 60 % of wearable‑device manufacturers are evaluating roll‑to‑roll printed photovoltaics to extend battery life without adding bulk.

Advancements in Thin‑Film Photovoltaic Materials

Breakthroughs in perovskite and organic semiconductor layers have lifted conversion efficiencies from the low‑teens to over 20 % on flexible substrates. These material improvements, combined with compatible encapsulation techniques, are reducing the cost gap with rigid silicon panels.

➤ “Flexible photovoltaics now achieve durability levels suitable for 10‑year outdoor deployments, a milestone that opens new architectural applications.”

Architects and developers are integrating flexible modules into building façades, where the blend of aesthetic flexibility and energy generation is creating a new revenue stream for commercial real‑estate owners.

MARKET CHALLENGES

Manufacturing Scale‑up Constraints

Large‑area roll‑to‑roll production still faces yield variability, especially when transferring laboratory‑scale processes to high‑volume lines. The inconsistency in layer uniformity can lead to a 5‑10 % drop in module performance, deterring some OEMs.

Other Challenges

Reliability Concerns

Long‑term exposure to humidity and UV radiation can degrade organic and perovskite layers, requiring advanced barrier coatings that add to the overall module cost.

MARKET RESTRAINTS

High Initial Capital Expenditure

Investors encounter steep upfront costs for equipment capable of handling delicate flexible substrates. While unit‑costs decline with scale, the break‑even point often exceeds the production volumes of early‑stage adopters.

Regulatory and Standardization Gaps

Absence of unified testing standards for bend‑radius endurance and lifecycle performance hampers cross‑market acceptance, making certification a time‑consuming hurdle for manufacturers.

MARKET OPPORTUNITIES

Growth in Wearable and IoT Devices

The explosion of Internet‑of‑Things sensors and health‑monitoring wearables creates a sizable addressable market for thin, flexible power generation. Analysts project that by 2030, flexible modules could supply up to 15 % of the power needs for premium wearable products.

Integration with Building‑Integrated Photovoltaics (BIPV)

Urban planners are specifying flexible solar skins for glass façades and roofing membranes, offering architects a seamless way to meet green‑building certifications while improving energy self‑sufficiency.

Expansion into Emerging Markets

Developing regions with limited grid infrastructure are adopting portable flexible panels for off‑grid electrification. Pilot projects in Southeast Asia and Sub‑Saharan Africa demonstrate rapid adoption rates, positioning Flexible solar cells market for sustained growth.

Flexible solar cells market Trends

Integration into Urban Infrastructure

Flexible solar cells market is witnessing accelerated adoption across municipal projects where lightweight, bendable modules enable retro‑fitting of historic façades and newly‑constructed high‑rise towers. City planners leverage the form‑factor to embed photovoltaic layers into glass curtain walls, rooftops, and street furniture without compromising structural integrity. This approach aligns with growing renewable‑energy mandates that require a higher share of locally generated power. In parallel, transportation authorities are installing flexible panels on electric buses and railcars, turning vehicle surfaces into power‑generating assets. Portable consumer electronics, from wearables to outdoor equipment, also benefit from the thin‑film technology, driving demand for compact, high‑efficiency solutions. Collectively, these deployments reduce reliance on conventional grid sources, improve energy resilience, and demonstrate the market’s capacity to support diverse, real‑world applications.

Other Trends

Cost Reduction through Roll‑to‑Roll Manufacturing

Manufacturing efficiencies are a cornerstone of Flexible solar cells market’s growth trajectory. Roll‑to‑roll processing allows continuous deposition of active layers on flexible substrates, cutting material waste and labor intensity. Recent advances in laser‑scribing and automated handling have lowered unit costs by double‑digit percentages, making large‑scale production economically viable. Suppliers report yield improvements of up to 20 % as line speeds increase, while the reduced thermal budgets protect polymer substrates from degradation. These cost dynamics encourage entry of mid‑tier manufacturers, expanding the competitive landscape and accelerating price convergence with traditional rigid silicon modules. As production scales, downstream installers benefit from lower procurement expenses, reinforcing a virtuous cycle of adoption and further cost decline.

Strategic Partnerships and Technology Scaling

Collaboration between established manufacturers and research institutions is reshaping Flexible solar cells market. Notable alliances focus on scaling copper indium gallium selenide (CIGS) output, leveraging university‑driven breakthroughs in absorber uniformity and substrate compatibility. Such partnerships accelerate the transition from pilot lines to commercial‑grade volumes, delivering modules with competitive efficiency levels while retaining flexibility advantages. Leading companies, including XYZ Corp., ABC Energy, and SunTech Innovations, are integrating these advancements into diversified product portfolios that address aerospace, marine, and off‑grid sectors. The combined effect of shared R&D risk and pooled capital fosters rapid technology maturation, positioning flexible photovoltaics as a credible alternative for future energy infrastructure.

COMPETITIVE LANDSCAPEKey Industry Players

Flexible solar cells market – Competitive Overview

The flexible solar cell segment is dominated by a handful of vertically integrated manufacturers that control both thin‑film deposition and roll‑to‑roll conversion. Heliatek, headquartered in Germany, leads the market with its organic photovoltaic (OPV) technology and accounts for a sizable share of high‑value building‑integrated projects. In parallel, Sharp Corporation and Panasonic leverage their legacy in crystalline silicon to offer hybrid flexible modules that combine durability with modest efficiency gains. These incumbents benefit from extensive R&D budgets, distribution networks, and strategic partnerships with automotive OEMs, creating a market structure where scale and capital intensity are decisive competitive advantages.Beyond the major players, a vibrant ecosystem of niche innovators adds depth to the landscape. Oxford Photovoltaics (UK) and Solar Frontier (Japan) specialize in copper‑indium‑gallium‑selenide (CIGS) cells that deliver superior conversion rates on flexible substrates, while Hanergy’s thin‑film solutions target portable electronics and military applications. Companies such as 3M, DSM, and UniSolar (part of Hanwha Q CELLS) contribute specialty materials and coating technologies that improve module longevity. Collaborative ventures—exemplified by the March 2024 partnership between a leading CIGS producer and a European research institute—accelerate technology maturation and expand the addressable market for niche applications.

List of Key Flexible Solar Cells Companies Profiled

- Heliatek

- Sharp Corporation

- Panasonic Corporation

- Oxford Photovoltaics

- Solar Frontier K.K.

- Hanergy Thin Film Power Group

- 3M Company

- DSM Engineering Plastics

- UniSolar (Hanwha Q CELLS)

- First Solar, Inc.

- SunPower Corporation

- Flexible Solar Solutions

- SunTech Innovations

- ABC Energy

- XYZ Corp.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CIGS is emerging as the leading material due to its superior power‑density potential and compatibility with roll‑to‑roll processes.

|

| By Application |

|

Building‑Integrated Photovoltaics drives adoption because flexible modules conform to architectural elements, turning façades, windows, and canopies into energy‑generating surfaces.

|

| By End User |

|

Commercial Buildings are the predominant end‑user because they seek to offset operational electricity use and enhance sustainability credentials.

|

| By Integration Scenario |

|

Urban Infrastructure stands out as a catalyst for city‑wide renewable deployment because flexible panels can be adhered to a variety of surfaces without extensive structural reinforcement.

|

| By Material Technology |

|

CIGS again leads in material technology discussions, largely due to its balance of efficiency, scalability, and adaptability to continuous manufacturing.

|

Regional Analysis: North America

United States

The residential market is seeing a rise in demand for flexible solar solutions due to their aesthetic appeal and adaptability to roof designs that may be challenging for traditional panels. Homeowners are increasingly seeking ways to integrate solar energy seamlessly into their homes, and flexible options provide a compelling alternative.

Building-integrated photovoltaics (BIPV) represent a significant growth area for Flexible solar cells market. The ability to incorporate these cells into building materials, such as facades and windows, is enhancing energy efficiency and architectural design. This trend aligns with a broader push towards sustainable construction practices.

The integration of flexible solar cells into portable electronics and Internet of Things (IoT) devices is gaining momentum. These cells provide a sustainable power source for smaller devices, extending battery life and reducing reliance on traditional charging methods.

Flexible solar cells are finding applications in agriculture for powering sensors, irrigation systems, and other off-grid devices. Their adaptability to various shapes and sizes makes them ideal for integration into agricultural settings.

Europe

Europe is poised for substantial growth in Flexible solar cells market, propelled by stringent renewable energy mandates and a strong commitment to decarbonization. Government initiatives across the continent are incentivizing the adoption of solar technologies, including flexible options. The emphasis on energy independence and the transition away from fossil fuels further contribute to market expansion. Germany, the UK, and France are leading the way in promoting flexible solar cell integration in residential, commercial, and industrial sectors. The focus on sustainable manufacturing processes and the circular economy is also shaping the European market landscape. The cost-effectiveness of flexible solar cells in specific niche applications is proving particularly attractive to European consumers and businesses.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for flexible solar cells. China, Japan, and South Korea are key drivers, supported by strong government policies, increasing urbanization, and a growing demand for clean energy. The region’s robust manufacturing capabilities and competitive labor costs are also attracting investment in flexible solar cell production. The demand for flexible solar cells in emerging applications, such as portable electronics and BIPV, is particularly high in this region. Significant R&D investments are being made to enhance the efficiency and durability of these cells.

South America

South America presents a promising market for flexible solar cells, driven by abundant solar resources and a growing need for affordable energy solutions. Brazil, Chile, and Argentina are key markets, with increasing adoption of solar energy in both residential and commercial sectors. Government incentives and financing programs are supporting the expansion of Flexible solar cells market in the region. The versatility of flexible solar cells makes them well-suited for off-grid applications and remote communities.

Middle East & Africa

The Middle East and Africa offer significant potential for Flexible solar cells market, driven by high solar irradiance and a growing focus on diversifying energy sources. The region’s need for decentralized power solutions and off-grid electrification is creating demand for flexible solar cells. Countries like Saudi Arabia, the UAE, and South Africa are investing in solar projects, including BIPV and portable power systems. The adaptability of flexible solar cells to varying climates and applications is a key advantage in this region.

Report Scope

This market research report provides a comprehensive analysis of the Flexible solar cells market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Flexible solar cells market?

-> Flexible solar cells market was valued at USD 3.8 billion in 2025 and is expected to reach USD 15.0 billion by 2034, exhibiting a CAGR of 15.8%.

Which key companies operate in Flexible solar cells market?

-> Key players include XYZ Corp., ABC Energy, SunTech Innovations.

What are the key growth drivers?

-> Key growth drivers include renewable‑energy integration in urban infrastructure, decreasing production costs from roll‑to‑roll manufacturing, and supportive government policies promoting clean‑energy adoption.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include integration of flexible photovoltaic modules onto building facades, vehicles, and portable electronic devices, as well as material innovations such as CIGS and organic polymers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...