MARKET INSIGHTS

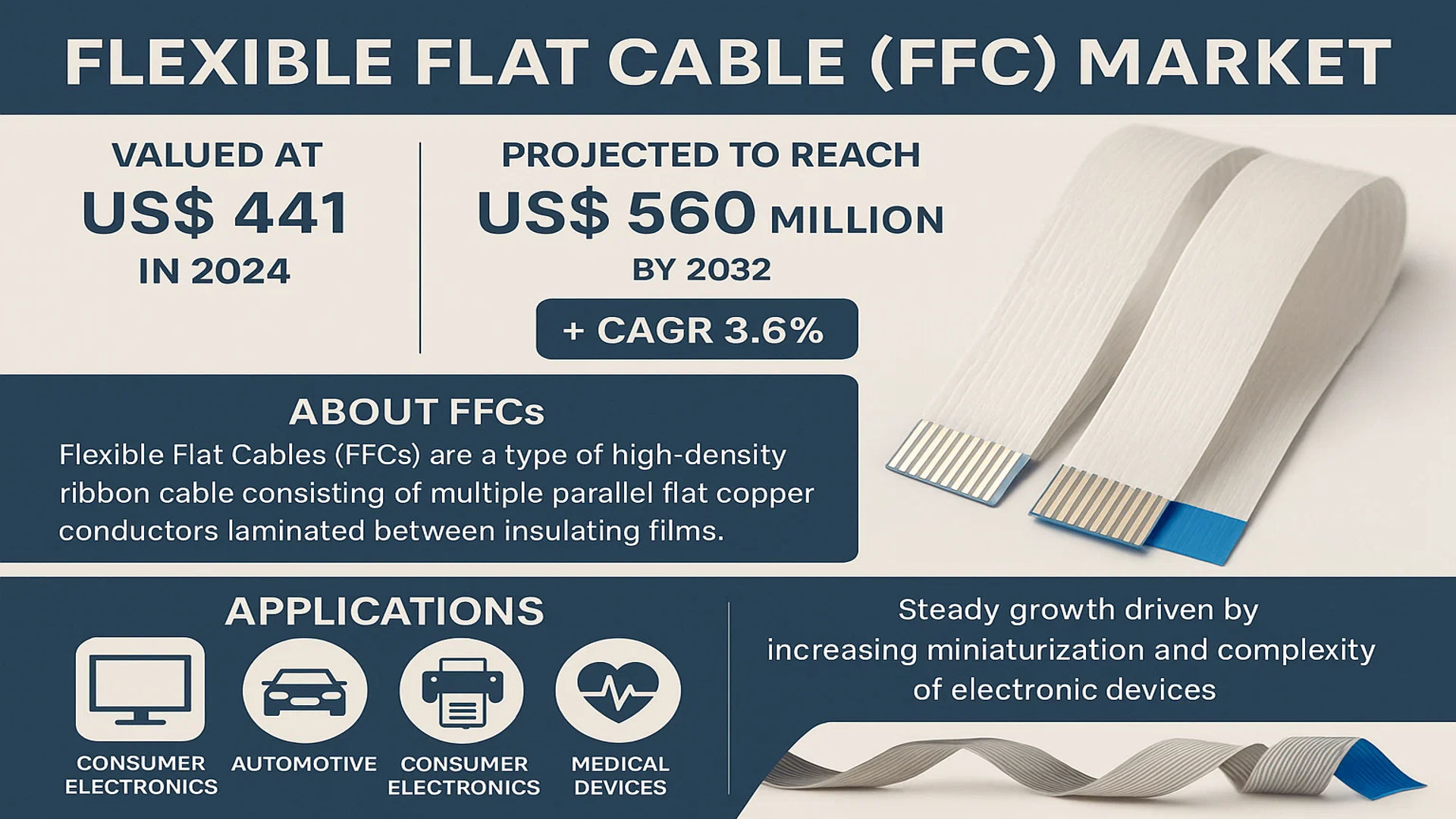

The global Flexible Flat Cable (FFC) Market was valued at 441 million in 2024 and is projected to reach US$ 560 million by 2032, at a CAGR of 3.6% during the forecast period.

Flexible Flat Cables (FFCs) are a type of high-density ribbon cable consisting of multiple parallel flat copper conductors laminated between insulating films. They are primarily used for internal connections in electronic devices to link printed circuit boards (PCBs) to other components, offering advantages such as space savings, flexibility, and improved signal integrity. While widely used in consumer electronics like TVs and printers, their application is also expanding into automotive and medical devices.

The market is experiencing steady growth driven by the increasing miniaturization and complexity of electronic devices across various sectors. However, this growth is tempered by competition from alternative interconnect solutions and pricing pressures. China dominates as the largest regional market, holding over 20% of the global share, while the 0.500 mm pitch segment is the most prominent product type, accounting for more than 30% of the market. Key players such as Sumitomo Electric and Johnson Electric lead a highly consolidated landscape where the top five manufacturers collectively control over 50% of the market.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Consumer Electronics and Automotive Sectors to Propel Market Growth

The global Flexible Flat Cable (FFC) market is experiencing robust growth driven by the expanding consumer electronics and automotive industries. FFCs are integral components in devices such as smartphones, laptops, televisions, and automotive infotainment systems due to their flexibility, space-saving design, and high-speed data transmission capabilities. The consumer electronics sector, valued at over $1 trillion globally, continues to innovate with thinner, lighter, and more powerful devices, necessitating the use of compact and reliable interconnect solutions like FFCs. In the automotive sector, the increasing integration of advanced driver-assistance systems (ADAS), electric vehicles (EVs), and in-car entertainment systems has significantly boosted demand. Automotive electronics now account for approximately 35% of a vehicle’s total cost, up from just 10% two decades ago, underscoring the critical role of components such as FFCs in modern vehicle architecture.

Rising Adoption of High-Density Interconnect Solutions in Industrial Applications

Industrial automation and medical devices represent significant growth avenues for the FFC market. The trend toward Industry 4.0 and smart manufacturing has increased the deployment of robotics, sensors, and control systems that require high-density, flexible cabling for efficient signal transmission and space optimization. FFCs are preferred in these applications because of their ability to withstand repeated flexing, resistance to vibration, and reliability in harsh environments. The global industrial automation market is projected to grow at a compound annual growth rate of nearly 9% over the next five years, directly fueling demand for FFCs. Similarly, the medical device industry, which relies on precision and miniaturization, uses FFCs in equipment such as patient monitors, imaging systems, and portable diagnostic devices. This sector’s expansion, driven by an aging population and increased healthcare spending, further supports market growth.

Technological Advancements and Miniaturization Trends

Technological advancements in electronics manufacturing are key drivers for the FFC market. The ongoing miniaturization of electronic components demands interconnect solutions that offer higher performance in smaller form factors. FFCs, with pitches as fine as 0.3 mm, enable high-density connections essential for modern devices. Innovations in materials, such as the use of high-temperature-resistant polymers and improved shielding techniques, have enhanced the durability and signal integrity of FFCs. Additionally, the rise of 5G technology and the Internet of Things (IoT) has created new applications for FFCs in communication devices and smart infrastructure. The global IoT market is expected to exceed $1.5 trillion by 2030, indicating substantial future demand for reliable, high-speed cabling solutions like FFCs.

MARKET CHALLENGES

Price Volatility of Raw Materials and Intense Market Competition

The FFC market faces challenges related to the volatility of raw material prices and intense competitive pressure. Copper, a primary material in FFC conductors, has experienced significant price fluctuations due to supply chain disruptions, geopolitical tensions, and changing demand patterns. These fluctuations directly impact production costs and profit margins for manufacturers. Additionally, the market is highly competitive, with numerous players, particularly in Asia, offering low-cost alternatives. This competition pressures established manufacturers to reduce prices, often at the expense of quality and innovation. While the top five companies hold over 50% of the market share, smaller players aggressively compete on price, creating a challenging environment for sustainable growth and investment in research and development.

Other Challenges

Technical Limitations in High-Frequency Applications

FFCs face limitations in very high-frequency applications, where signal integrity and electromagnetic interference (EMI) become critical concerns. As data transmission speeds increase, maintaining signal quality over flat cable structures becomes more challenging compared to shielded coaxial or twisted-pair cables. This restricts the use of standard FFCs in certain advanced applications, such as high-speed networking equipment or next-generation automotive systems, requiring additional engineering or alternative solutions.

Supply Chain and Manufacturing Complexities

Manufacturing FFCs involves precise processes to ensure consistent quality, particularly for fine-pitch designs. Variations in alignment, insulation thickness, or conductor spacing can lead to performance issues or failure. Additionally, global supply chain disruptions, as witnessed in recent years, can delay raw material availability and increase logistics costs, affecting production timelines and overall market stability.

MARKET RESTRAINTS

Limitations in High-Power and Extreme Environment Applications

While FFCs excel in many areas, they are less suitable for high-power applications or extreme environmental conditions. Their flat structure and typically thin conductors limit current-carrying capacity compared to round cables with larger cross-sections. In applications requiring significant power delivery, such as industrial motors or power supplies, FFCs may not be the preferred choice. Similarly, exposure to extreme temperatures, chemicals, or mechanical stress beyond specified limits can degrade FFC performance. For instance, in automotive under-the-hood applications or outdoor industrial settings, additional protection or alternative cabling solutions are often necessary, restraining broader adoption in these segments.

Compatibility and Standardization Issues

The lack of universal standards for FFC designs and connectors can create compatibility issues, hindering market growth. While pitches like 0.500 mm, 1.000 mm, and 1.250 mm are common, variations in connector types, locking mechanisms, and termination methods exist across manufacturers. This fragmentation complicates the sourcing and replacement process for end-users, particularly in aftermarket or repair scenarios. It also increases inventory costs for distributors and OEMs who must stock multiple variants. The absence of globally accepted standards slows down innovation and interoperability, potentially limiting the seamless integration of FFCs into diverse applications and systems.

Economic Sensitivity and Cyclical Demand Patterns

The FFC market is sensitive to economic cycles due to its strong ties to consumer electronics and automotive production. During economic downturns, reduced consumer spending on electronics and decreased automotive sales directly impact FFC demand. For example, the global semiconductor shortage recently affected production across multiple industries, highlighting the vulnerability of supply chains. Such cyclical patterns make long-term planning and investment challenging for manufacturers, who must navigate periods of oversupply and undersupply. This economic sensitivity acts as a restraint, particularly for companies heavily reliant on a few key industries or geographic markets.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy and Electric Vehicles

The rapid growth of renewable energy and electric vehicles presents significant opportunities for the FFC market. In solar power systems, FFCs are used in panel connections and monitoring equipment due to their flexibility and reliability. The global solar energy market is expanding at a compound annual growth rate of over 20%, driven by sustainability initiatives and falling technology costs. Similarly, electric vehicles require extensive wiring for battery management, infotainment, and control systems. With EV sales projected to reach 45 million units annually by 2040, the demand for high-performance, lightweight cabling like FFCs is expected to surge, offering substantial growth potential for manufacturers.

Advancements in Flexible Hybrid Electronics (FHE)

Flexible Hybrid Electronics (FHE) represent a cutting-edge opportunity for FFC technology. FHE combines printed electronics with traditional components to create flexible, stretchable, and conformable devices. FFCs are ideal for interconnecting these systems in wearables, health monitors, and smart textiles. The wearable technology market alone is forecast to exceed $100 billion by 2030, with health and fitness applications leading growth. Innovations in FHE require increasingly sophisticated interconnect solutions that can bend, twist, and integrate seamlessly with flexible substrates, positioning FFCs as critical enablers of next-generation electronic devices.

Geographic Expansion and Strategic Partnerships

Geographic expansion into emerging markets and strategic partnerships offer lucrative opportunities for FFC manufacturers. Regions such as Southeast Asia, Latin America, and Eastern Europe are experiencing growing electronics production and automotive manufacturing. Establishing local presence or partnerships in these regions can tap into new customer bases and reduce logistics costs. Additionally, collaborations with technology companies to develop custom FFC solutions for specific applications, such as augmented reality/virtual reality devices or advanced medical equipment, can create high-value niches. Such strategic initiatives allow companies to diversify their portfolios and reduce dependence on traditional, highly competitive market segments.

FLEXIBLE FLAT CABLE (FFC) MARKET TRENDS

Miniaturization and High-Density Interconnects Driving Market Evolution

The relentless push towards smaller, more powerful electronic devices is fundamentally reshaping the Flexible Flat Cable (FFC) market. This trend towards miniaturization necessitates interconnects that occupy minimal space while maintaining high performance, a core strength of FFCs. The demand is particularly pronounced for finer pitch cables, with the 0.500 mm pitch segment commanding over 30% of the market share because it offers the ideal balance of compact design and reliable signal integrity for high-density applications. This is especially critical in consumer electronics like smartphones, laptops, and wearables, where internal real estate is at a premium. Furthermore, the proliferation of high-resolution displays and advanced sensors in automotive and medical devices requires FFCs capable of handling increased data bandwidth without electromagnetic interference, pushing manufacturers to innovate with improved shielding and material compositions.

Other Trends

Automotive Electrification and Advanced Driver-Assistance Systems (ADAS)

The automotive industry’s rapid transition towards electrification and autonomy is a significant growth vector for FFCs. Modern vehicles are becoming increasingly software-defined, incorporating a vast array of electronic control units (ECUs), infotainment systems, and numerous sensors for ADAS functionalities like lane-keeping and automatic emergency braking. These systems rely on a complex network of reliable, lightweight, and durable interconnects. FFCs are ideally suited for this environment because of their flexibility, which allows for routing through tight spaces within a vehicle’s chassis, and their resistance to vibration. The integration of multiple cameras and display screens per vehicle, a number that continues to rise, directly correlates to increased FFC consumption, making the automotive sector a key driver of market expansion beyond traditional consumer electronics.

Geographical Shift and Supply Chain Resilience

While China remains the dominant production and consumption hub, accounting for over 20% of the global market, there is a noticeable strategic trend towards supply chain diversification and regionalization. Recent global disruptions have highlighted the risks of concentrated manufacturing, prompting many OEMs to seek suppliers in other regions like North America and Europe to enhance resilience. This is not just about risk mitigation; it is also about proximity to end-use markets, particularly for the automotive industry. However, this shift faces the challenge of replicating the established, cost-effective manufacturing ecosystems found in Asia. Consequently, leading market players are expanding their production footprints globally, and there is increased investment in automation to maintain competitive pricing and quality standards across different geographical locations, ensuring stable supply for critical industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Geographic Expansion to Maintain Dominance

The global Flexible Flat Cable (FFC) market exhibits a semi-consolidated competitive structure, characterized by the presence of several established multinational corporations alongside numerous specialized regional manufacturers. The top five manufacturers collectively hold over 50% of the global market share, indicating a significant concentration of power among leading players. Sumitomo Electric stands as a preeminent force in this sector, leveraging its extensive expertise in electronic components and formidable global distribution network to secure a leading market position. The company’s strength is particularly evident across key regions including Asia, North America, and Europe.

Johnson Electric and Luxshare-ICT also command substantial portions of the market. Their growth is largely driven by strategic contracts with major consumer electronics OEMs and continuous advancements in high-density, fine-pitch FFC solutions, which are increasingly critical for modern compact devices. Furthermore, these companies benefit from robust manufacturing capabilities in Asia, the largest consuming region which accounts for over 50% of global demand.

Concurrently, the competitive intensity is heightened by the aggressive strategies of other significant players. Companies like Samtec and Würth Elektronik are strengthening their foothold through substantial investments in research and development. Their focus is on creating next-generation FFCs that offer higher data transmission rates, improved flexibility, and enhanced durability for demanding applications in automotive electronics and high-performance computing. This relentless pursuit of innovation is crucial for capturing value in an increasingly technical market.

Meanwhile, several specialized manufacturers are carving out strong niches. Mei Tong Electronics and He Hui Electronics, for instance, have solidified their status as key suppliers by offering cost-competitive and reliable products, particularly for the vast PC and display segment, which represents the largest application area. Their growth is underpinned by deep integration into the Asian supply chain and responsiveness to volume-driven demand.

List of Key Flexible Flat Cable (FFC) Companies Profiled

- Sumitomo Electric Industries, Ltd. (Japan)

- Johnson Electric Holdings Limited (Hong Kong)

- Mei Tong Electronics Co., Ltd. (China)

- He Hui Electronics Co., Ltd. (China)

- Luxshare-ICT Limited (China)

- Samtec, Inc. (U.S.)

- Würth Elektronik GmbH & Co. KG (Germany)

- Sumida-flexcon Co., Ltd. (Japan)

- Cvilux Corporation (Taiwan)

- Axon Cable S.A.S. (France)

- Hitachi Metals, Ltd. (Japan)

- Cicoil Corporation (U.S.)

- Xinfuer Electronics Co., Ltd. (China)

- Hezhi Electronic Technology Co., Ltd. (China)

- VST Electronics (India)

- Nicomatic S.A. (France)

- JSB TECH Co., Ltd. (South Korea)

Segment Analysis:

By Type

0.500 mm Pitches Segment Dominates the Market Due to High Demand in Consumer Electronics and PC Interconnects

The market is segmented based on type into:

- 0.500 mm Pitches

- 1.000 mm Pitches

- 1.250 mm Pitches

- Others

By Application

PC/PC Display Segment Leads Due to Pervasive Use in Laptops, Monitors, and Desktop Computers

The market is segmented based on application into:

- PC or PC Display

- TV

- Printer

- Car Stereo

- Others

Regional Analysis: Flexible Flat Cable (FFC) Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the Flexible Flat Cable (FFC) market, accounting for over 50% of worldwide consumption by volume. This dominance is primarily fueled by China, which alone holds a market share exceeding 20%, making it the single largest national market globally. The region’s supremacy is built on its colossal electronics manufacturing ecosystem, serving both domestic demand and global exports for products like PCs, televisions, and consumer electronics. Countries like Japan and South Korea are hubs for high-end, precision FFC manufacturing, with key players such as Sumitomo Electric and Hitachi Metals operating there. Meanwhile, Southeast Asian nations are experiencing rapid growth due to shifting manufacturing bases and increasing investments in automotive and industrial electronics. The demand is heavily skewed towards the 0.500 mm pitch segment, which holds over 30% market share, driven by the need for miniaturization in modern devices.

North America

North America represents a significant and technologically advanced market for FFCs, holding a collective share of over 30% alongside Japan. The region’s demand is characterized by a strong focus on high-reliability applications in the automotive, medical, and aerospace sectors. The presence of major technology corporations and robust R&D activities drives the need for specialized, high-performance cables that meet stringent quality and safety standards, such as those from the FDA for medical devices. While the overall market volume is less than Asia-Pacific, the value per unit is often higher due to the advanced specifications required. Key players like Samtec have a strong foothold here, supplying to the region’s sophisticated manufacturing and design industries. The market is also influenced by trends like the electrification of vehicles and advancements in medical imaging equipment.

Europe

The European FFC market is driven by its strong automotive industrial base and a well-established consumer electronics sector, particularly in Germany, France, and the U.K. The region has a significant demand for FFCs used in car stereos, GPS systems, and advanced driver-assistance systems (ADAS), aligning with the continent’s leadership in automotive innovation. Furthermore, strict EU regulations, such as RoHS and REACH, compel manufacturers to adopt high-quality, compliant components, creating a market for reliable and environmentally conscious FFC products. Companies like Würth Elektronik are key suppliers within this framework. While the market is mature and stable, growth is sustained by continuous technological upgrades in end-use industries and the region’s emphasis on premium, durable electronic goods.

South America

The South American FFC market is emerging and presents potential for future growth, though it is currently constrained by economic volatility and infrastructural challenges. Brazil and Argentina are the primary markets within the region, with demand stemming from the automotive assembly and consumer electronics sectors. However, the market is highly cost-sensitive, which often limits the adoption of advanced, higher-priced FFC variants. Growth is sporadic and heavily tied to the economic health of these nations and government policies aimed at boosting local manufacturing. While there is a baseline demand for FFCs in products like TVs and printers, the market lacks the robust, innovation-driven demand seen in more developed regions.

Middle East & Africa

The FFC market in the Middle East & Africa is nascent and fragmented. Development is primarily concentrated in more economically developed nations like Israel, Turkey, and the UAE, where there is some local electronics assembly and a growing consumer base. The demand is largely met through imports, as there is limited local manufacturing capacity for these components. The market’s growth is slow and is primarily driven by infrastructure development, urbanization, and the gradual increase in disposable income, which fuels demand for consumer electronics. However, the region’s share of the global FFC market remains minimal, with progress hindered by a reliance on imports and a less developed industrial manufacturing sector compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Flexible Flat Cable (FFC) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Flexible Flat Cable (FFC) Market?

-> Flexible Flat Cable (FFC) Market was valued at 441 million in 2024 and is projected to reach US$ 560 million by 2032, at a CAGR of 3.6% during the forecast period.

Which key companies operate in Global Flexible Flat Cable (FFC) Market?

-> Key players include Sumitomo Electric, Johnson Electric, Mei Tong Electronics, He Hui Electronics, and Luxshare-ICT, among others. The global top five manufacturers hold a combined market share of over 50%.

What are the key growth drivers?

-> Key growth drivers include increasing demand from consumer electronics, automotive applications, and the proliferation of high-density interconnect (HDI) PCBs requiring reliable and space-saving connectivity solutions.

Which region dominates the market?

-> China is the largest market, with a share exceeding 20%, followed by North America and Japan, which together account for over 30% of the global market.

What are the emerging trends?

-> Emerging trends include the development of finer pitch FFCs for miniaturized devices, the integration of FFCs in flexible and foldable displays, and the adoption of advanced materials for improved durability and signal integrity in high-frequency applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...