MARKET INSIGHTS

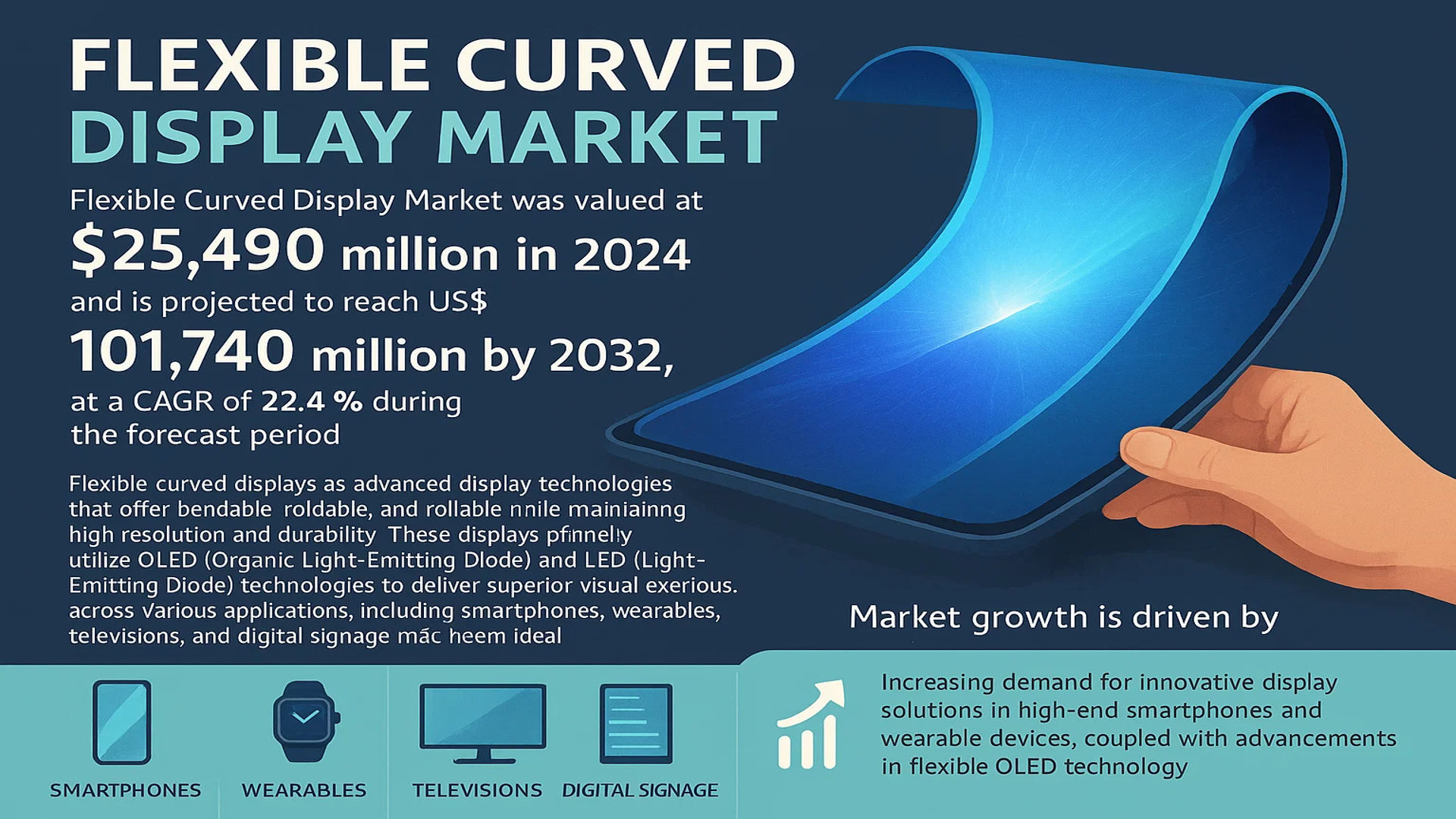

The global Flexible Curved Display Market was valued at 25490 million in 2024 and is projected to reach US$ 101740 million by 2032, at a CAGR of 22.4% during the forecast period.

Flexible curved displays are advanced display technologies that offer bendable, foldable, and rollable characteristics while maintaining high resolution and durability. These displays primarily utilize OLED (Organic Light-Emitting Diode) and LED (Light-Emitting Diode) technologies to deliver superior visual experiences across various applications, including smartphones, wearables, televisions, and digital signage. Their lightweight nature and energy efficiency make them ideal for next-generation consumer electronics.

The market growth is driven by increasing demand for innovative display solutions in high-end smartphones and wearable devices, coupled with advancements in flexible OLED technology. While supply chain disruptions from geopolitical tensions posed challenges, manufacturers are adapting through localized production. Key players like Samsung Electronics and LG Display continue to invest in R&D, with recent product launches such as foldable smartphones accelerating adoption. The Asia-Pacific region dominates production, accounting for over 60% of global output in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption in Smartphones and Wearable Devices to Accelerate Market Expansion

The global flexible curved display market is experiencing robust growth, primarily driven by their increasing integration in smartphones and wearable devices. Major smartphone manufacturers are adopting flexible OLED displays for flagship models to enhance design aesthetics and user experience. Samsung’s Galaxy Z Flip series and Huawei’s Mate X lineup showcase how curvature and flexibility are becoming key differentiators in premium devices. Beyond smartphones, wearable tech like smartwatches and fitness bands benefit from bendable displays that conform to the human body. The wearable display market alone is projected to grow at a compound annual rate of over 25% through 2030, creating substantial demand for flexible screen technologies.

Technological Advancements in OLED Manufacturing to Fuel Market Growth

Breakthroughs in OLED production technologies are significantly lowering manufacturing costs while improving yield rates for flexible displays. The development of more efficient deposition techniques and the introduction of advanced encapsulation methods have reduced material waste by nearly 40% compared to earlier production methods. Leading manufacturers are now achieving bend radii of under 3mm while maintaining display quality, enabling innovative product designs previously impossible with rigid panels. These technological improvements are translating into better profit margins for producers and more affordable end products for consumers.

Growing Demand for Energy-Efficient Displays to Boost Adoption

Flexible OLED displays consume approximately 30% less power than comparable LCD panels, making them increasingly attractive for mobile applications where battery life is paramount. This energy efficiency advantage, combined with their superior contrast ratios and viewing angles, is driving adoption across multiple sectors. Automotive manufacturers are incorporating curved displays in dashboards and infotainment systems, while the medical field is exploring flexible displays for portable diagnostic equipment. The global push toward energy-efficient technologies across industries is expected to sustain long-term demand growth for flexible display solutions.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes Limit Market Penetration

Despite technological advancements, flexible curved displays remain significantly more expensive to produce than conventional flat panels. The specialized materials and precise manufacturing conditions required for flexible OLEDs result in production costs that are approximately 2-3 times higher than standard displays. Establishing new production lines requires investments exceeding $7 billion for advanced Gen 10.5 fabs, creating substantial barriers to market entry. Even leading manufacturers experience yield rates below 70% for particularly complex flexible designs, further driving up unit costs and limiting widespread adoption in mid-range devices.

Durability Concerns Impact Consumer Confidence and Product Lifespan

The inherent flexibility of these displays introduces unique durability challenges not present in rigid panels. Repeated bending can cause micro-cracks in the thin-film transistor layer, with some studies showing noticeable degradation after just 20,000 folding cycles. Advanced encapsulation techniques have improved lifespan, but reliability remains a concern for mission-critical applications. Manufacturers continue to face warranty claims and returns related to display integrity, creating additional costs that hinder market expansion in price-sensitive segments.

MARKET CHALLENGES

Supply Chain Vulnerabilities Create Production Bottlenecks

The flexible display industry faces significant supply chain challenges due to the specialized nature of required materials. Over 80% of the world’s polyimide substrates—a critical component—come from just a handful of suppliers, creating potential bottlenecks. Geopolitical tensions and trade restrictions have periodically disrupted the flow of essential materials, causing production delays. Manufacturers must maintain expensive inventory buffers or develop costly alternative supply chains to mitigate these risks, adding substantial operational complexity.

Technical Hurdles in Large-Scale Display Manufacturing

While flexible technology excels in small to medium-size applications, scaling up to larger formats presents considerable engineering challenges. Current production methods struggle to maintain uniformity across larger panel sizes, with defect rates increasing exponentially beyond 15-inch diagonal measurements. The development of effective roll-to-roll manufacturing processes for large flexible displays remains an unsolved challenge, limiting expansion into promising applications like foldable laptops and rollable TVs.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Medical Sectors Present Growth Potential

The automotive industry’s shift toward digital cockpits creates substantial opportunities for flexible curved displays. Modern vehicle interiors increasingly incorporate wraparound dashboards and curved center stacks where flexible technology offers distinct advantages. Medical device manufacturers are also adopting flexible displays for portable imaging systems and wearable patient monitors, benefiting from their lightweight and rugged characteristics. These emerging verticals are projected to account for over 25% of flexible display demand by 2030.

Advancements in Hybrid Rigid-Flex Display Solutions Open New Markets

Innovative hybrid designs that combine rigid and flexible display elements are enabling cost-effective implementations in new application areas. These solutions provide many benefits of pure flexible displays at significantly lower price points, making the technology accessible to broader market segments. Early success with this approach in mid-range smartphones and industrial HMIs demonstrates considerable potential for value-conscious markets that previously couldn’t justify premium flexible display costs.

Government Support for Advanced Display Technologies Accelerates R&D

Several governments are establishing funding programs to support domestic flexible display development, recognizing its strategic importance. The United States and European Union have allocated over $2 billion combined for display technology research initiatives, with Asia-Pacific nations making even larger investments. These programs are catalyzing cross-industry collaborations between display manufacturers, materials science researchers, and equipment providers, accelerating the pace of innovation and commercialization in flexible display technologies.

FLEXIBLE CURVED DISPLAY MARKET TRENDS

Rising Demand for Foldable Smartphones to Drive Market Expansion

The global flexible curved display market is experiencing rapid growth, largely due to the increasing adoption of foldable smartphones. With major smartphone manufacturers investing heavily in next-generation flexible displays, shipments of foldable devices have surpassed 15 million units in 2023, a significant increase from previous years. The ability of curved displays to offer larger screens without compromising portability has made them particularly appealing in the mobile sector. Moreover, newer iterations of these displays now feature ultra-thin glass layers, improving durability while maintaining flexibility, which has further accelerated consumer adoption.

Beyond smartphones, flexible displays are gaining traction in wearables, with the market for flexible smartwatch displays growing at a CAGR of 25.6% from 2022 to 2025. Innovations such as stretchable OLED panels, capable of conforming to irregular surfaces, are expanding applications in medical devices and automotive dashboards. While some manufacturers face challenges in mass production yields, ongoing improvements in manufacturing techniques are expected to lower costs and further boost market penetration.

Other Trends

Technological Advancements in OLED Manufacturing

OLED technology dominates the flexible curved display market, accounting for over 78% of revenue share in 2024. Continuous improvements in encapsulation techniques have significantly extended the lifespan of flexible OLEDs, reducing burn-in risks that once limited their adoption. Key manufacturers have also introduced hybrid architectures combining rigid and flexible substrates, enhancing structural integrity without sacrificing design versatility. These breakthroughs have enabled displays with bending radii under 3mm, opening new possibilities for compact and foldable consumer electronics.

Expansion into Automotive and Smart Home Applications

The automotive industry is emerging as a major consumer of flexible curved displays, with premium vehicle manufacturers integrating them into dashboards and center consoles. The curved nature of these displays aligns perfectly with modern vehicle interiors, offering enhanced visibility while maintaining sleek aesthetics. In smart homes, flexible displays are being utilized in innovative ways, from rollable TVs to interactive wallpaper applications. Market analysts project that non-consumer electronic applications will account for nearly 30% of the flexible display market by 2030, reflecting diversification beyond traditional mobile devices.

While supply chain disruptions impacted production in recent years, leading manufacturers have significantly ramped up capacity to meet growing demand. South Korean and Chinese manufacturers collectively hold over 85% of the production share, though new entrants are emerging in other regions. Sustainability improvements, including the development of more eco-friendly flexible substrates, are also positioning the technology favorably amid tightening environmental regulations worldwide.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansions Drive Market Competition

The global flexible curved display market is characterized by intense competition, with Samsung Electronics and LG Display dominating the sector due to their early-mover advantage and continuous R&D investments. Samsung leads with approximately 35% market share in 2024, primarily due to its Galaxy Z Fold/Flip series and partnerships with smartphone OEMs. Meanwhile, LG Display maintains strong positioning through its automotive and television display segments.

BOE Technology Group and AU Optronics have emerged as formidable Asian competitors, capturing nearly 28% combined market share through cost-effective manufacturing and government-backed semiconductor initiatives. These companies are accelerating production capacity to meet growing demand from Chinese smartphone brands.

Recent developments show established players are adopting divergent strategies – while Samsung focuses on OLED-based foldables, companies like Royole Corporation and E Ink Holdings are pioneering ultra-thin flexible displays for niche applications including wearables and e-paper devices. The market also sees increasing cross-industry collaborations, such as Corning’s specialty glass partnerships with multiple display manufacturers.

List of Key Flexible Curved Display Companies Profiled

- Samsung Electronics (South Korea)

- LG Display (South Korea)

- BOE Technology Group (China)

- AU Optronics (Taiwan)

- Corning Incorporated (U.S.)

- Japan Display Inc. (Japan)

- Visionox (China)

- Royole Corporation (China)

- E Ink Holdings (Taiwan)

- Sharp Corporation (Japan)

- Huawei Technologies (China)

Segment Analysis:

By Type

OLED Segment Dominates the Market Due to Superior Flexibility and Energy Efficiency

The market is segmented based on type into:

- OLED (Organic Light-Emitting Diode)

- Subtypes: AMOLED, PMOLED, and others

- LED (Light-Emitting Diode)

- Quantum Dot Display

- MicroLED

- Others

By Application

Smartphones Lead the Market Due to High Demand for Premium Display Solutions

The market is segmented based on application into:

- Smartphones

- Televisions

- Wearable Devices

- Subtypes: Smartwatches, Fitness Trackers, and others

- Automotive Displays

- Digital Signage and Advertising Screens

- Others

By End User

Consumer Electronics Sector Drives Market Growth

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Healthcare

- Retail and Advertising

- Others

Regional Analysis: Flexible Curved Display Market

Asia-Pacific

The Asia-Pacific region dominates the global flexible curved display market, accounting for over 45% of total revenue in 2024, driven by strong manufacturing ecosystems in South Korea, China, and Japan. The presence of display technology giants like Samsung Electronics, LG Display, and BOE Technology fuels innovation, particularly in OLED-based flexible displays. China’s aggressive investments in display panel production, including the $5.2 billion BOE plant in Chengdu, underscore its commitment to technology leadership. Regional smartphone manufacturers are early adopters of curved displays, while growing demand for foldable devices in premium consumer electronics segments provides further growth momentum. However, intense price competition among domestic manufacturers creates margin pressures, necessitating continuous technological differentiation.

North America

North America represents the second-largest market for flexible curved displays, primarily driven by premium electronics adoption and strong R&D investments in display technologies. The U.S. market benefits from close collaboration between tech giants like Apple and display manufacturers, with patents for foldable iPhone designs signaling future market expansion. Military and aerospace applications are emerging as significant growth areas, leveraging flexible displays’ durability advantages. While the region lags in panel manufacturing capacity, it leads in material science innovations with companies like Corning developing specialized flexible glass substrates capable of withstanding repeated bending cycles.

Europe

Europe maintains a strong position in flexible display material sciences and niche applications, though it accounts for a smaller share of global production capacity. German chemical companies lead in developing advanced encapsulation materials critical for flexible OLED longevity, while Scandinavian firms pioneer rollable display applications in automotive interiors. The EU’s circular economy regulations are pushing manufacturers toward more sustainable production methods, affecting material choices and recycling processes. Adoption in the region remains concentrated in high-end automotive displays and premium consumer electronics, with growth tempered by conservative consumer preferences for traditional form factors.

Middle East & Africa

The MEA region shows promising growth potential, particularly in digital signage and luxury retail applications across Gulf Cooperation Council countries. Flexible curved displays are gaining traction in high-end commercial installations, though consumer adoption remains limited by premium pricing. Israel’s display technology startups contribute specialist innovations in flexible sensor integration. The region benefits from increasing technology infrastructure investments, with the UAE’s smart city initiatives incorporating next-generation displays in public spaces. However, the market faces challenges around technology distribution networks and after-sales service capabilities for sophisticated display technologies.

South America

South America represents an emerging market with growth concentrated in Brazil and Mexico, where local assembly of consumer electronics incorporating imported display panels creates incremental demand. Economic volatility and import dependency constrain market expansion, though increasing smartphone penetration and digital advertising growth provide opportunities. The region shows particular interest in cost-effective flexible display solutions for point-of-sale systems and digital signage. Local manufacturers face hurdles in establishing display production due to infrastructure limitations and competition from Asian imports, making the market primarily consumption-driven rather than production-oriented.

Report Scope

This market research report provides a comprehensive analysis of the Global Flexible Curved Display market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Flexible Curved Display market was valued at USD 25,490 million in 2024 and is projected to reach USD 101,740 million by 2032, growing at a CAGR of 22.4%.

- Segmentation Analysis: Detailed breakdown by product type (OLED, LED), application (Cell Phone, Digital Camera, Advertising Screen, Computer and TV, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to high smartphone adoption and manufacturing hubs.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in display manufacturing, and evolving industry standards like foldable and rollable displays.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as demand for high-end smartphones and wearable devices, along with challenges like supply chain disruptions and high production costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global Flexible Curved Display Market?

-> Flexible Curved Display Market was valued at 25490 million in 2024 and is projected to reach US$ 101740 million by 2032, at a CAGR of 22.4% during the forecast period.

Which key companies operate in the Global Flexible Curved Display Market?

-> Key players include Samsung Electronics, LG Display, BOE Technology Group Co., Ltd., AU Optronics, and Sharp Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for smartphones, wearable devices, and advancements in OLED technology.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by high production capacity and consumer demand in countries like China, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include foldable displays, rollable screens, and integration with IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...