MARKET INSIGHTS

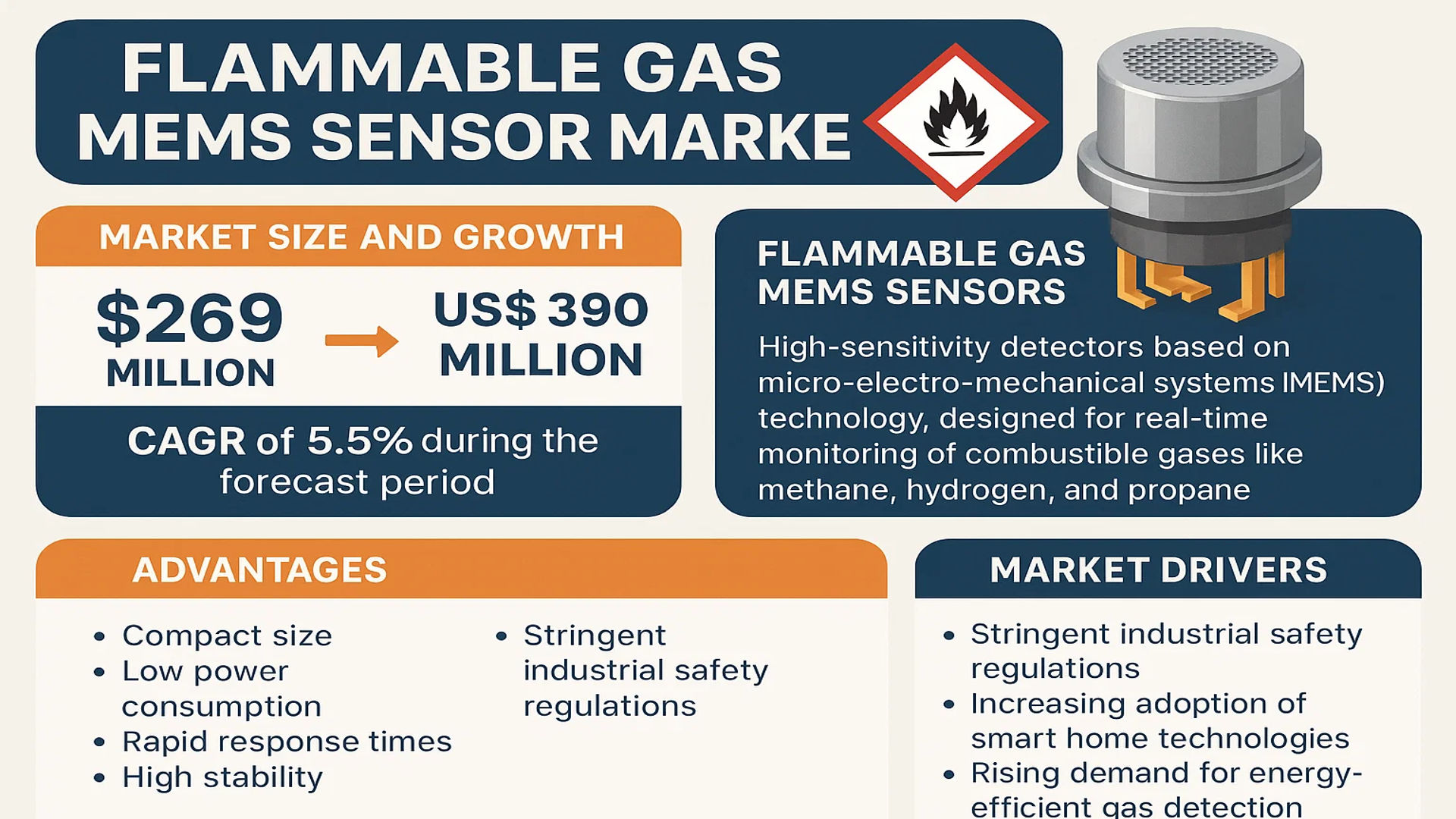

The global Flammable Gas MEMS Sensor Market was valued at 269 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 5.5% during the forecast period.

Flammable gas MEMS sensors are high-sensitivity detectors based on micro-electro-mechanical systems (MEMS) technology, designed for real-time monitoring of combustible gases like methane, hydrogen, and propane. These sensors integrate miniaturized components for superior performance, offering advantages such as compact size, low power consumption, rapid response times, and high stability. They play a critical role in industrial safety systems, residential gas leak detection, and hydrogen monitoring in emerging applications like fuel cell vehicles.

Market growth is primarily driven by stringent industrial safety regulations, increasing adoption of smart home technologies, and rising demand for energy-efficient gas detection solutions. However, challenges persist in achieving high selectivity across multiple gas types while maintaining cost competitiveness. Recent innovations include the development of NDIR (Non-Dispersive Infrared) sensors with enhanced detection ranges and the integration of IoT capabilities for remote monitoring. Key industry players like Amphenol and Figaro are expanding their portfolios through strategic partnerships and technological advancements in MEMS fabrication.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Industrial Safety Regulations Fuel Adoption of Flammable Gas MEMS Sensors

Global industrial safety regulations are becoming increasingly stringent, mandating advanced flammable gas detection systems across high-risk sectors like oil & gas, chemical, and mining. Regulatory bodies worldwide are imposing stricter standards due to rising workplace accidents from gas leaks – recent statistics indicate that industrial gas incidents account for approximately 15% of all workplace fatalities in hazardous environments. MEMS-based sensors are gaining traction as preferred solutions because of their superior sensitivity (detecting gas concentrations as low as 1-5 ppm), compact form factor enabling integration into IoT devices, and lower power consumption compared to conventional detectors. The European Union’s ATEX directive and OSHA standards in North America are driving widespread sensor deployment, with the industrial segment projected to account for over 45% of total flammable gas sensor demand by 2026.

Expansion of Smart City Infrastructure Accelerates Market Growth

Urbanization projects globally are incorporating smart gas monitoring systems as essential infrastructure components, creating substantial demand for MEMS-based flammable gas sensors. Modern cities are deploying networked sensor arrays for real-time air quality and gas leak monitoring, particularly in residential areas with piped natural gas distribution. The global smart city initiative investment surpassed $120 billion in 2023, with environmental monitoring systems constituting nearly 20% of this expenditure. MEMS sensors dominate these deployments due to their wireless connectivity capabilities, with leading manufacturers reporting 30% year-over-year growth in municipal orders. Recent technological advancements in edge computing integration allow these sensors to process data locally, reducing latency in emergency response systems while maintaining energy efficiency.

Transition to Low-GWP Refrigerants Creates New Application Areas

The global phase-out of hydrofluorocarbon (HFC) refrigerants under the Kigali Amendment is driving adoption of flammable gas sensors in HVAC and refrigeration systems. New environmentally-friendly but flammable alternatives like R-32 and R-290 require continuous leak monitoring, with safety standards mandating sensor deployment in commercial refrigeration units. The HVAC industry’s conversion to these refrigerants is progressing at 12-15% annually, creating a parallel growth trajectory for gas detection solutions. MEMS sensors specifically designed for refrigerant detection now account for nearly 25% of the total industrial sensor market, with manufacturers developing specialized variants offering false-alarm immunity to common household vapors while maintaining high sensitivity to target gases.

MARKET RESTRAINTS

High Development Costs and Complex Calibration Requirements Limit Market Penetration

While MEMS technology offers significant advantages, the specialized manufacturing processes and calibration requirements create substantial barriers to entry. Developing gas-specific MEMS sensors involves expensive semiconductor fabrication techniques, with initial R&D investments often exceeding $2-3 million per sensor variant. Additionally, maintaining consistent performance across environmental conditions requires sophisticated calibration protocols – humidity variations of just 10% can alter sensor response curves by up to 15%. These technical complexities restrict adoption in price-sensitive markets, particularly in developing regions where conventional sensors still dominate due to their 30-40% lower upfront costs despite higher long-term maintenance requirements.

Other Restraints

Cross-Sensitivity Challenges

Many MEMS gas sensors exhibit cross-sensitivity to non-target gases, potentially triggering false alarms. For instance, certain metal-oxide semiconductor (MOS) variants may respond similarly to methane and ethanol vapor, complicating deployment in environments like breweries or food processing plants where both might be present. Advanced filtering algorithms can mitigate but not eliminate this issue, requiring redundant sensor arrays that increase system costs by 25-30%.

Extended Development Cycles

The time-to-market for new MEMS sensor variants averages 18-24 months, limiting manufacturers’ ability to quickly respond to emerging gas detection needs. This includes extensive field testing (typically 6-8 months) to validate performance across temperature ranges and potential interference scenarios, creating challenges in keeping pace with evolving industry requirements.

MARKET OPPORTUNITIES

Hydrogen Economy Development Presents Transformative Growth Potential

The global transition to hydrogen energy systems is creating unprecedented demand for specialized gas detection solutions. Fuel cell vehicles and hydrogen fueling stations require continuous monitoring for leaks, as hydrogen’s wide flammability range (4-75% concentration) demands sensors with exceptional responsiveness. MEMS-based hydrogen detectors capable of 500ms response times are becoming standard in next-generation fuel cell systems, with the automotive sector projected to account for 35% of high-end sensor demand by 2028. Recent breakthroughs in palladium-alloy MEMS structures have improved detection thresholds below the 1% LEL (Lower Explosive Limit), meeting stringent safety requirements for confined spaces like vehicle cabins and underground storage facilities.

Integration with AI-Powered Predictive Maintenance Systems

The convergence of MEMS sensor networks with machine learning analytics is enabling predictive gas leak detection before concentrations reach dangerous levels. Advanced systems can now identify equipment deterioration patterns by analyzing subtle changes in baseline sensor readings, allowing maintenance interventions 3-5 times earlier than threshold-based detection. Industrial facilities adopting these AI-enhanced solutions report 60-70% reductions in unplanned downtime related to gas systems. This technological synergy is particularly valuable in aging infrastructure, where MEMS sensor grids provide continuous health monitoring for pipelines and storage tanks that might otherwise require costly physical inspections.

MARKET CHALLENGES

Performance Degradation in Extreme Environments

MEMS gas sensors face significant reliability challenges in harsh operating conditions common to many industrial applications. High ambient temperatures above 85°C can accelerate sensor drift, requiring more frequent recalibration – in refinery environments, this may necessitate maintenance intervals as short as 3 months compared to the typical 12-month cycle. Similarly, sub-zero conditions can increase response times by 200-300%, compromising safety in cold climate operations. While protective enclosures help, they add bulk and cost, negating some of MEMS technology’s inherent advantages. Recent material science advancements have improved high-temperature stability, but widespread adoption of these premium-grade sensors remains limited by costs that are nearly double standard variants.

Other Challenges

Battery Life Constraints in Wireless Installations

While MEMS sensors are power-efficient compared to conventional detectors, continuous wireless operation in IoT networks still presents battery life challenges. In typical configurations, industrial-grade wireless sensors require battery replacement every 6-9 months, creating maintenance logistics issues in large-scale deployments. Emerging energy harvesting solutions show promise but currently add 30-40% to unit costs while introducing reliability concerns in low-light or vibration-limited environments.

Standardization Gaps Across Industries

The lack of unified performance standards for MEMS gas sensors across different verticals complicates product development and certification. Requirements vary significantly between automotive (ISO 26142), industrial (IEC 60079), and consumer applications, forcing manufacturers to maintain multiple product lines. This fragmentation increases development costs by an estimated 15-20% while delaying time-to-market for new innovations.

FLAMMABLE GAS MEMS SENSOR MARKET TRENDS

Rising Industrial Safety Regulations to Drive Market Growth

The global flammable gas MEMS sensor market is witnessing significant growth due to stringent regulatory standards mandating gas leak detection in industrial environments. Governments worldwide are enforcing stricter safety protocols, particularly in oil & gas, chemical, and manufacturing sectors, where exposure to explosive gases poses critical risks. MEMS sensors—known for their compact size, high sensitivity, and low power consumption—are increasingly replacing traditional detectors in compliance with these norms. For example, North America’s Occupational Safety and Health Administration (OSHA) mandates continuous monitoring of hazardous gases in workplaces, directly accelerating the adoption of MEMS-based solutions.

Other Trends

Advancements in Hydrogen Detection for New Energy Vehicles

With the rapid expansion of hydrogen fuel cell vehicles (FCVs), there is a surging demand for high-precision flammable gas MEMS sensors capable of detecting hydrogen leaks in real time. Hydrogen, being highly combustible, requires ultra-sensitive detection systems, and MEMS technology offers faster response rates (under 10 seconds) and superior stability compared to conventional electrochemical sensors. Japan and South Korea, leading adopters of FCVs, are spearheading investments in these sensors, with projections indicating that hydrogen-related applications could account for over 15% of the market’s revenue by 2032. This trend aligns with global shifts toward decarbonization and renewable energy solutions.

Growing Demand for Smart Home Gas Leak Detectors

The residential sector is emerging as a key growth area, driven by increasing consumer awareness of gas safety and smart home integrations. Modern MEMS sensors are now embedded in IoT-enabled detectors that provide instant alerts via smartphones, reducing risks associated with natural gas (methane) and LPG leaks. Europe and North America dominate this segment, with smart gas detectors projected to grow at a CAGR of 7.8% through 2030. Features like self-calibration and wireless connectivity further enhance their appeal, positioning them as critical components of next-generation home safety systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Product Innovations Drive Market Competition

The global flammable gas MEMS sensor market exhibits a moderately competitive landscape, characterized by key players leveraging technological advancements and regional expansions to strengthen their foothold. Amphenol Advanced Sensors holds a significant market share, accounting for approximately 18% of global revenue in 2024, thanks to its diversified product portfolio and strong distribution network across industrial and residential sectors. The company’s latest MEMS-based methane sensors have gained traction in oil & gas monitoring applications.

Meanwhile, Figaro Engineering and senseAir (an Asahi Kasei company) have emerged as formidable competitors, capturing nearly 12% and 15% market share respectively. Figaro’s TGS series MOS sensors demonstrate industry-leading stability in harsh environments, while senseAir’s NDIR sensors dominate the European HVAC monitoring segment. Both companies continue to invest in miniaturization technologies to enhance sensor portability.

Recent industry developments highlight intensifying competition through M&A activities. SmartGAS’s acquisition by Endress+Hauser in 2023 strengthened its position in industrial safety systems, while Cubic Sensor’s strategic partnership with Chinese EV manufacturers reflects the growing importance of hydrogen detection in transportation applications. These moves signal the market’s transition toward integrated safety solutions rather than standalone sensor offerings.

Regional dynamics further influence competition, with Japanese firms like NISSHA leveraging precision manufacturing for high-sensitivity consumer applications, while U.S.-based Veris Industries focuses on IoT-enabled solutions for smart buildings. The convergence of MEMS technology with wireless connectivity presents new opportunities for differentiation, particularly in predictive maintenance systems.

List of Key Flammable Gas MEMS Sensor Manufacturers

- Amphenol Advanced Sensors (U.S.)

- senseAir (Sweden) – subsidiary of Asahi Kasei Microdevices

- smartGAS Mikrosensorik (Germany)

- Figaro Engineering (Japan)

- NISSHA FIS Inc. (Japan)

- Veris Industries (U.S.)

- Dynament Ltd. (UK)

- Cubic Sensor and Instrument (China)

- Siemens AG (Germany)

Segment Analysis:

By Type

NDIR (Non-Dispersive Infrared) Sensors Dominate the Market Owing to High Accuracy and Selectivity in Flammable Gas Detection

The market is segmented based on type into:

- NDIR (Non-Dispersive Infrared) Sensors

- Subtypes: Single-gas NDIR, Multi-gas NDIR

- Metal Oxide Semiconductor Sensors

- Catalytic Sensors

- Electrochemical Sensors

- Others

By Application

Industrial Segment Leads Due to Stringent Safety Regulations and Wide Application in Oil & Gas, Chemical, and Manufacturing Sectors

The market is segmented based on application into:

- Industrial

- Residential

- Commercial

- Automotive

- Others

By Detection Range

0-1000 ppm Range Holds Maximum Share for Monitoring Low Concentration Flammable Gases in Occupational Safety Applications

The market is segmented based on detection range into:

- 0-1000 ppm

- 1000-10000 ppm

- Above 10000 ppm

By Gas Type

Methane Detection Segment Dominates Due to Widespread Use in Industrial and Residential Settings

The market is segmented based on gas type into:

- Methane

- Propane

- Hydrogen

- Butane

- Others

Regional Analysis: Flammable Gas MEMS Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the global Flammable Gas MEMS Sensor market, accounting for over 40% of total revenue in 2024. This leadership position stems from rapid industrialization in China and India, coupled with stringent workplace safety regulations. China’s ambitious hydrogen energy development plan, targeting 50,000 fuel cell vehicles by 2025, is creating substantial demand for hydrogen detection sensors. Japan’s advanced MEMS manufacturing capabilities and South Korea’s growing semiconductor industry further bolster regional market growth. However, price sensitivity remains a challenge, pushing manufacturers to develop cost-optimized solutions without compromising on detection accuracy.

North America

North America represents the second-largest market, driven by strict safety standards from OSHA and increasing adoption in shale gas operations. The U.S. leads regional demand, particularly for methane detection in oil & gas facilities and carbon monoxide monitoring in residential applications. Canada’s focus on industrial automation and Mexico’s expanding manufacturing sector contribute to steady growth. Recent regulatory updates, including enhanced leak detection requirements for LNG facilities, are accelerating sensor replacements with MEMS-based alternatives offering higher reliability and lower maintenance costs.

Europe

Europe’s market growth is propelled by environmental directives like ATEX and IECEx governing hazardous area equipment. Germany and the UK lead in industrial adoption, while Scandinavian countries show high penetration in residential applications. The region’s strong automotive sector is driving innovation in hydrogen sensors for fuel cell vehicles, with several EU-funded projects underway. However, market maturity and lengthy product certification processes somewhat limit growth potential compared to Asia-Pacific. Recent developments include smart sensors with IoT connectivity for remote monitoring in chemical plants.

Middle East & Africa

This emerging market benefits from expanding oil & gas infrastructure and growing awareness of industrial safety. The UAE and Saudi Arabia account for over 60% of regional demand, driven by large-scale energy projects incorporating advanced gas detection systems. Africa presents untapped potential, though adoption rates remain low outside South Africa and Nigeria due to limited regulations. The lack of local manufacturing necessitates imports, creating opportunities for global sensor suppliers with robust distribution networks.

South America

Market growth in South America trails other regions due to economic volatility and inconsistent enforcement of safety standards. Brazil leads in industrial applications, particularly for ethanol production monitoring, while Chile and Argentina show promise in mining sector adoptions. Political instability in some countries hampers foreign investment in safety technologies, though increasing insurance requirements for industrial facilities are gradually driving sensor adoption. Local manufacturers focus on ruggedized designs suited for harsh environmental conditions prevalent in regional industries.

Report Scope

This market research report provides a comprehensive analysis of the Global Flammable Gas MEMS Sensor market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 269 million in 2024 and is projected to reach USD 390 million by 2032, growing at a CAGR of 5.5%.

- Segmentation Analysis: Detailed breakdown by product type (NDIR Sensors, Metal Oxide Semiconductor Sensors) and application (Residential, Commercial, Industrial) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading manufacturers including Amphenol, Senseair, smartGAS, Figaro, and NISSHA, covering their product portfolios, market shares, and strategic developments.

- Technology Trends & Innovation: Analysis of MEMS sensor advancements, integration with IoT platforms, and development of miniaturized, low-power solutions.

- Market Drivers & Restraints: Evaluation of factors such as industrial safety regulations, hydrogen economy growth, and challenges like sensor calibration requirements.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, industrial end-users, and policy makers.

The research methodology combines primary interviews with industry experts and analysis of verified secondary data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Flammable Gas MEMS Sensor Market?

-> Flammable Gas MEMS Sensor Market was valued at 269 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Flammable Gas MEMS Sensor Market?

-> Key players include Amphenol, Senseair, smartGAS, Figaro, NISSHA, Veris Industries, Dynament, and Cubic Sensor and Instrument.

What are the key growth drivers?

-> Primary growth drivers include increasing industrial safety regulations, adoption in hydrogen fuel cell vehicles, and growing demand for smart gas detection systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing market due to industrial expansion, while North America leads in technological adoption.

What are the emerging trends?

-> Emerging trends include integration with IoT platforms, development of multi-gas detection sensors, and miniaturization of sensor components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...