MARKET INSIGHTS

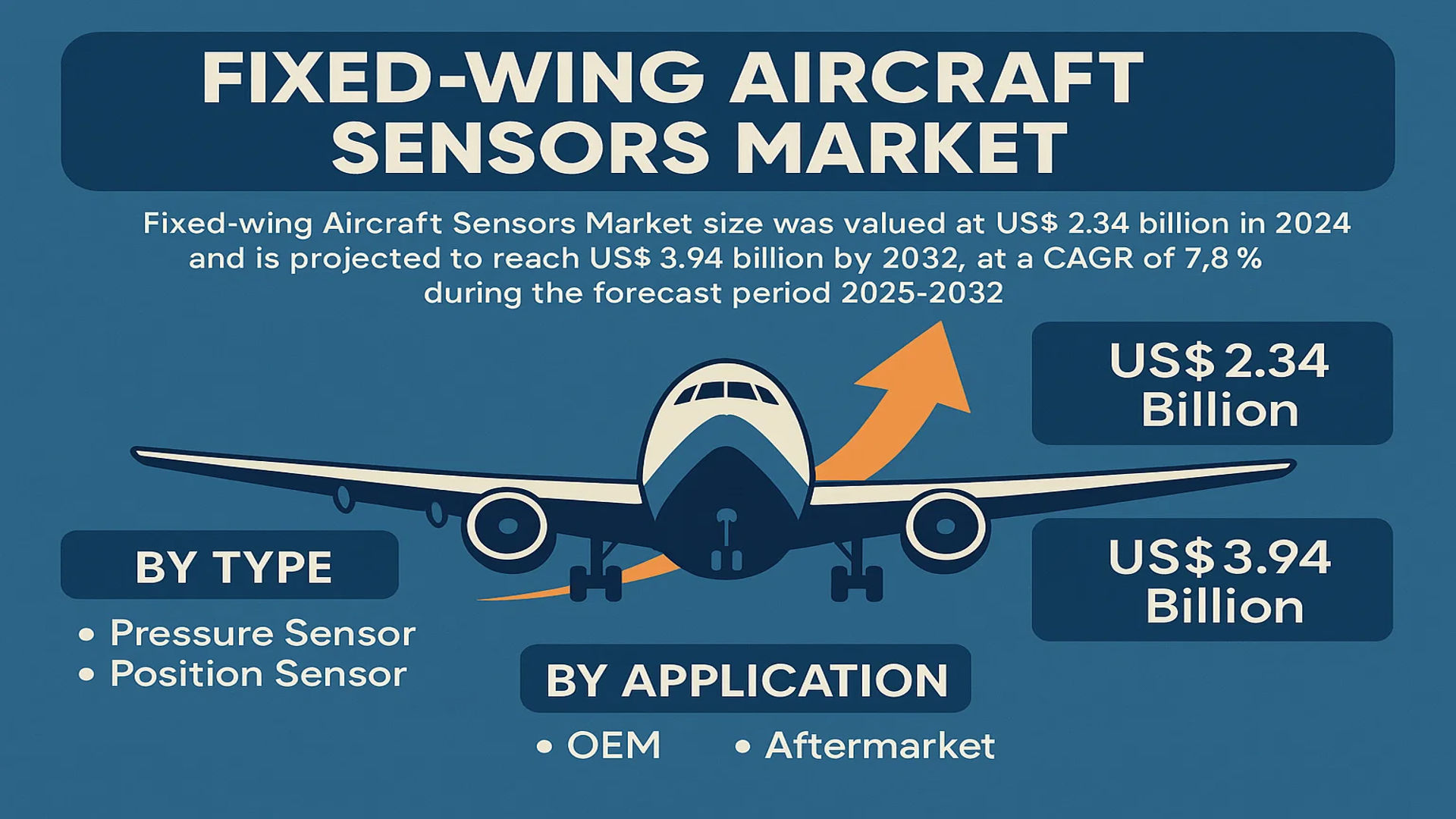

The global Fixed-wing Aircraft Sensors Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 3.94 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032. While North America currently holds the largest market share (38%), Asia-Pacific is expected to witness the fastest growth at 6.1% CAGR, driven by increasing defense budgets and commercial aviation expansion in China and India.

Fixed-wing aircraft sensors are critical components that monitor and measure various flight parameters including altitude, airspeed, temperature, vibration, and pressure. These systems encompass multiple sensor types such as pressure sensors, position sensors, radar sensors, and vibration sensors that collectively ensure operational safety, performance optimization, and regulatory compliance. Advanced MEMS (Micro-Electro-Mechanical Systems) technology is increasingly being adopted for these sensors due to their compact size and reliability.

The market growth is propelled by rising aircraft deliveries, with Boeing projecting demand for 42,600 new commercial aircraft by 2042. However, supply chain disruptions and stringent certification processes pose challenges. Key players like Honeywell International and TE Connectivity are investing in next-generation sensor technologies, with recent developments including AI-integrated predictive maintenance systems. The aftermarket segment is particularly dynamic, accounting for 32% of total revenues in 2024, as airlines prioritize sensor upgrades for fleet modernization.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Aircraft Fleet Expansion to Drive Market Growth

The global fixed-wing aircraft market is witnessing robust growth due to increasing air passenger traffic and fleet expansion. With commercial aviation demand projected to grow at over 4% annually, airlines are investing heavily in new aircraft equipped with advanced sensor technologies. Sensor systems play a critical role in flight operations, monitoring parameters from engine performance to environmental conditions. For instance, modern aircraft incorporate over 5,000 sensors generating data points that enable predictive maintenance and enhance operational efficiency. This growing adoption of sensor-enabled aircraft systems is expected to drive significant demand in the coming years.

Stringent Aviation Safety Regulations Fueling Sensor Adoption

Regulatory mandates for enhanced flight safety are compelling aircraft manufacturers to integrate sophisticated sensor systems. Aviation authorities worldwide are implementing stricter requirements for real-time monitoring of critical flight parameters, driving the need for accurate pressure, temperature and vibration sensors. While mechanical systems traditionally dominated aircraft monitoring, the shift toward digital solutions with embedded sensors is accelerating. These regulatory pressures coupled with the aviation industry’s zero-tolerance approach to safety lapses are creating strong market momentum for advanced sensor technologies.

MARKET RESTRAINTS

High Development Costs and Certification Challenges Impeding Growth

Aircraft sensor manufacturers face significant financial and technical barriers to entry due to stringent certification requirements. The aviation industry’s rigorous safety standards necessitate extensive testing protocols that can extend development cycles by 18-24 months. Furthermore, the certification process for new sensor technologies often requires multi-million dollar investments in testing facilities and compliance documentation. These high barriers discourage smaller players from entering the market while forcing established manufacturers to carefully evaluate return on investment for new product development.

Supply Chain Disruptions Affecting Sensor Component Availability

The global semiconductor shortage has emerged as a critical challenge for sensor manufacturers, with lead times for specialized components extending beyond 52 weeks in some cases. Aircraft sensors require high-reliability semiconductors and electronic components that must meet stringent aerospace qualifications. These specialized parts often have limited alternate sources, making the supply chain vulnerable to disruptions. While manufacturers are working to mitigate these challenges through strategic stockpiling and supplier diversification, component availability remains a persistent constraint on market growth.

MARKET OPPORTUNITIES

Emergence of Predictive Maintenance Creating New Growth Avenues

The aviation industry’s transition toward predictive maintenance models presents significant opportunities for sensor manufacturers. Airlines are increasingly adopting condition-based monitoring systems that leverage sensor data to predict component failures before they occur. This approach can reduce unscheduled maintenance events by up to 35% while improving aircraft utilization rates. As predictive analytics capabilities advance, demand is growing for sensors with enhanced data acquisition features and wireless connectivity. Manufacturers that can deliver integrated sensor solutions combining measurement accuracy with data analytics functionality stand to benefit substantially from this market shift.

Military Modernization Programs Driving Specialized Sensor Demand

Defense spending on next-generation aircraft is creating new opportunities in the military aviation segment. Modern combat aircraft incorporate sophisticated sensor arrays for flight control, threat detection and mission systems. With global defense budgets exceeding $2 trillion annually, military aviation programs represent a high-growth segment for specialized sensor technologies. Requirements for enhanced survivability and mission capabilities are driving demand for sensors with improved resistance to electromagnetic interference and harsh environmental conditions. This trend is particularly evident in fifth-generation fighter programs and unmanned combat aerial vehicle development initiatives.

MARKET CHALLENGES

Technical Complexity of Next-Generation Sensor Integration

While demand for advanced sensing capabilities grows, integrating new sensor technologies into aircraft systems presents significant technical hurdles. Modern avionics architectures require seamless interoperability between diverse sensor types while meeting strict weight and power consumption limits. The challenge is particularly acute for retrofit applications, where new sensors must interface with legacy aircraft systems. These integration complexities can delay product development timelines and increase engineering costs, presenting ongoing challenges for market participants.

Cybersecurity Risks in Connected Sensor Systems

The growing connectivity of aircraft sensor networks introduces new cybersecurity vulnerabilities that must be addressed. As sensor systems become more interconnected and data-driven, they present potential entry points for cyber threats. Ensuring the security of sensor data transmission and protecting against unauthorized access requires sophisticated encryption and authentication protocols. These security requirements add development complexity while potentially limiting the implementation of cost-effective commercial off-the-shelf components in aircraft sensor systems.

FIXED-WING AIRCRAFT SENSORS MARKET TRENDS

Smart Sensor Integration Emerges as a Key Growth Driver

The fixed-wing aircraft sensors market is witnessing rapid advancements in smart sensor technology, driven by the aviation industry’s increasing demand for real-time data monitoring and predictive maintenance. Modern sensors now incorporate Internet of Things (IoT) capabilities, enabling wireless connectivity and automated data transmission to ground control systems. Major manufacturers are investing heavily in miniaturized, lightweight sensors that offer higher accuracy while reducing fuel consumption. The global adoption of these advanced sensors is expected to grow at a compound annual growth rate (CAGR) of over 6% in the next five years, with pressure sensors and vibration sensors leading the segment due to their critical role in flight safety.

Other Trends

Increasing Demand for Aftermarket Sensor Upgrades

The aftermarket segment is experiencing substantial growth as airlines and defense agencies retrofit aging fleets with modern sensor systems. Regulatory mandates for improved flight data monitoring, especially in commercial aviation, have accelerated the replacement of legacy sensors with next-generation alternatives. Fixed-wing aircraft in service for more than 15 years are increasingly being fitted with upgraded temperature and position sensors to comply with evolving safety standards. Furthermore, the rise of predictive maintenance solutions has pushed demand for vibration and radar sensors that can preemptively alert maintenance crews.

Military Aviation Fuels High-Performance Sensor Development

The defense sector continues to be a dominant end-user in the fixed-wing aircraft sensors market, accounting for nearly 40% of total revenue in 2024. Unmanned aerial vehicles (UAVs) and next-generation fighter jets require specialized sensor suites with enhanced resistance to electromagnetic interference and extreme environments. Manufacturers are innovating in multi-spectral imaging sensors and AI-powered radar systems, with applications ranging from surveillance to electronic warfare. Government investments in modernizing air defense fleets across North America and Asia-Pacific are expected to sustain this demand, particularly for force sensors and advanced navigation systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Drive Market Position

The global fixed-wing aircraft sensors market remains competitive, with a mix of established aerospace giants and specialized sensor manufacturers vying for market share. Honeywell International dominates as the market leader, leveraging its integrated avionics systems and cutting-edge sensor technology that accounts for a significant portion of its aerospace segment revenue. Their recent development of MEMS-based pressure sensors for next-gen aircraft exemplifies their technological edge.

TE Connectivity Corporation and UTC Aerospace Systems (now part of Raytheon Technologies) hold robust positions, particularly in commercial aviation sensors, where reliability and precision are paramount. TE Connectivity’s 2023 launch of their Ultra-Low Noise Vibration Sensors demonstrates how companies are addressing the industry’s need for enhanced flight data accuracy. Meanwhile, UTC’s acquisition strategy has expanded its sensor capabilities across multiple aircraft systems.

The market sees intense competition in innovation, with Safran Electronics & Defense making significant strides in fiber optic sensor technology, while Thales Group focuses on integrated sensor suites for next-generation flight management systems. These European players are gaining traction through their specialization in military and high-performance aircraft applications.

What makes this market particularly dynamic is how mid-sized players like Ametek and Curtiss-Wright Corporation compete through niche expertise—Ametek in extreme environment sensors and Curtiss-Wright in mission-critical military aircraft systems. Their targeted approach allows them to maintain strong positions despite competing with larger conglomerates.

List of Key Fixed-Wing Aircraft Sensor Manufacturers

- Honeywell International (U.S.)

- TE Connectivity Corporation (U.S.)

- UTC Aerospace Systems (U.S.)

- Zodiac Aerospace (France)

- Ametek (U.S.)

- Safran Electronics & Defense (France)

- Curtiss-Wright Corporation (U.S.)

- Thales Group (France)

- Raytheon Company (U.S.)

- General Electric (U.S.)

Segment Analysis:

By Type

Pressure Sensor Segment Dominates Due to Critical Role in Flight Control Systems

The market is segmented based on type into:

- Pressure Sensor

- Subtypes: Absolute, differential, and gauge pressure sensors

- Position Sensor

- Force Sensor

- Temperature Sensor

- Vibration Sensor

- Radar Sensor

- Others

By Application

OEM Segment Leads with Increasing Aircraft Production Rates

The market is segmented based on application into:

- OEM

- Aftermarket

By Aircraft Type

Commercial Aviation Segment Drives Demand for Advanced Sensor Technologies

The market is segmented based on aircraft type into:

- Commercial Aviation

- Military Aviation

- General Aviation

By Technology

MEMS Technology Gains Traction for Miniaturization Benefits

The market is segmented based on technology into:

- MEMS-based Sensors

- Fiber Optic Sensors

- Traditional Electronic Sensors

- Others

Regional Analysis: Fixed-wing Aircraft Sensors Market

North America

The North American fixed-wing aircraft sensors market is highly advanced, driven by strong demand from commercial aviation and defense sectors. The U.S. dominates regional growth, accounting for over 70% of market share, supported by substantial defense budgets exceeding $800 billion annually and an active commercial aviation sector. Key manufacturers like Honeywell International and Raytheon Company are investing heavily in next-generation sensor technologies, particularly for UAVs and next-gen fighter jets. Regulatory emphasis on aviation safety (FAA Part 25 standards) and modernization of aging fleets creates steady demand for pressure, temperature, and position sensors. However, supply chain disruptions and component shortages occasionally challenge market stability.

Europe

Europe maintains a mature yet innovation-driven sensors market, with stringent EASA certification processes influencing product development. The region sees growing adoption of MEMS-based sensors and fiber optic technologies to enhance aircraft performance monitoring. Airbus’ production ramp-up and defense modernization programs in France, Germany, and the UK create sustained demand, especially for vibration and radar sensors. Environmental regulations pushing for fuel efficiency are accelerating sensor integration in engine monitoring systems. While Brexit created temporary supply chain complexities, the market remains resilient due to strong OEM-supplier partnerships across EU nations.

Asia-Pacific

As the fastest-growing regional market, Asia-Pacific benefits from expanding commercial fleets in China and India, plus increasing defense expenditures. China’s aviation sector alone is projected to account for 40% of new aircraft deliveries globally through 2030, driving sensor demand. Japan and South Korea lead in precision sensor manufacturing, while Southeast Asia emerges as a maintenance hub creating aftermarket opportunities. Price sensitivity pushes local manufacturers to offer cost-effective solutions, though global players maintain dominance in advanced avionics. The lack of standardized regional certification frameworks occasionally slows technology adoption compared to Western markets.

South America

Market growth in South America remains moderate but volatile, influenced by economic conditions and fluctuating defense budgets. Brazil’s Embraer creates steady demand for OEM sensors, while other nations primarily focus on fleet maintenance. The aftermarket segment shows promising growth as airlines extend aircraft service life. Challenges include limited local manufacturing capabilities and dependence on imports, though trade agreements are gradually improving component availability. Political instability in some countries creates unpredictable procurement cycles, particularly for military applications.

Middle East & Africa

This region presents contrasting growth patterns – Gulf nations drive premium sensor demand through fleet expansions (Etihad, Emirates, Qatar Airways), while African markets remain underdeveloped due to funding constraints. The UAE and Saudi Arabia are investing heavily in aerospace manufacturing capabilities, attracting sensor suppliers. Defense applications grow steadily due to geopolitical tensions, particularly for surveillance and radar systems. Though infrastructure limitations persist in some areas, the region’s strategic aviation hub status ensures long-term market potential, especially for temperature and pressure sensors compatible with extreme operating environments.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Fixed-wing Aircraft Sensors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Pressure Sensor, Position Sensor, Force Sensor, etc.), application (OEM, Aftermarket), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, and recent developments such as mergers and acquisitions.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration of AI/ML, and evolving aviation safety standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and regulatory hurdles.

- Stakeholder Analysis: Insights for component suppliers, aircraft manufacturers, MRO providers, and investors regarding strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Fixed-wing Aircraft Sensors Market?

-> Fixed-wing Aircraft Sensors Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 3.94 billion by 2032, at a CAGR of 7.8% during the forecast period 2025-2032.

Which key companies operate in Global Fixed-wing Aircraft Sensors Market?

-> Key players include Honeywell International, TE Connectivity Corporation, UTC Aerospace Systems, Zodiac Aerospace, Ametek, Safran Electronics & Defense, Curtiss-Wright Corporation, Thales Group, Raytheon Company, and General Electric.

What are the key growth drivers?

-> Key growth drivers include increasing aircraft production, modernization of existing fleets, stringent aviation safety regulations, and rising demand for fuel-efficient aircraft systems.

Which region dominates the market?

-> North America currently holds the largest market share (38.5% in 2024), while Asia-Pacific is expected to witness the highest growth rate (6.2% CAGR) during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, development of smart sensor networks, integration of predictive maintenance capabilities, and adoption of fiber optic sensing technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...