MARKET INSIGHTS

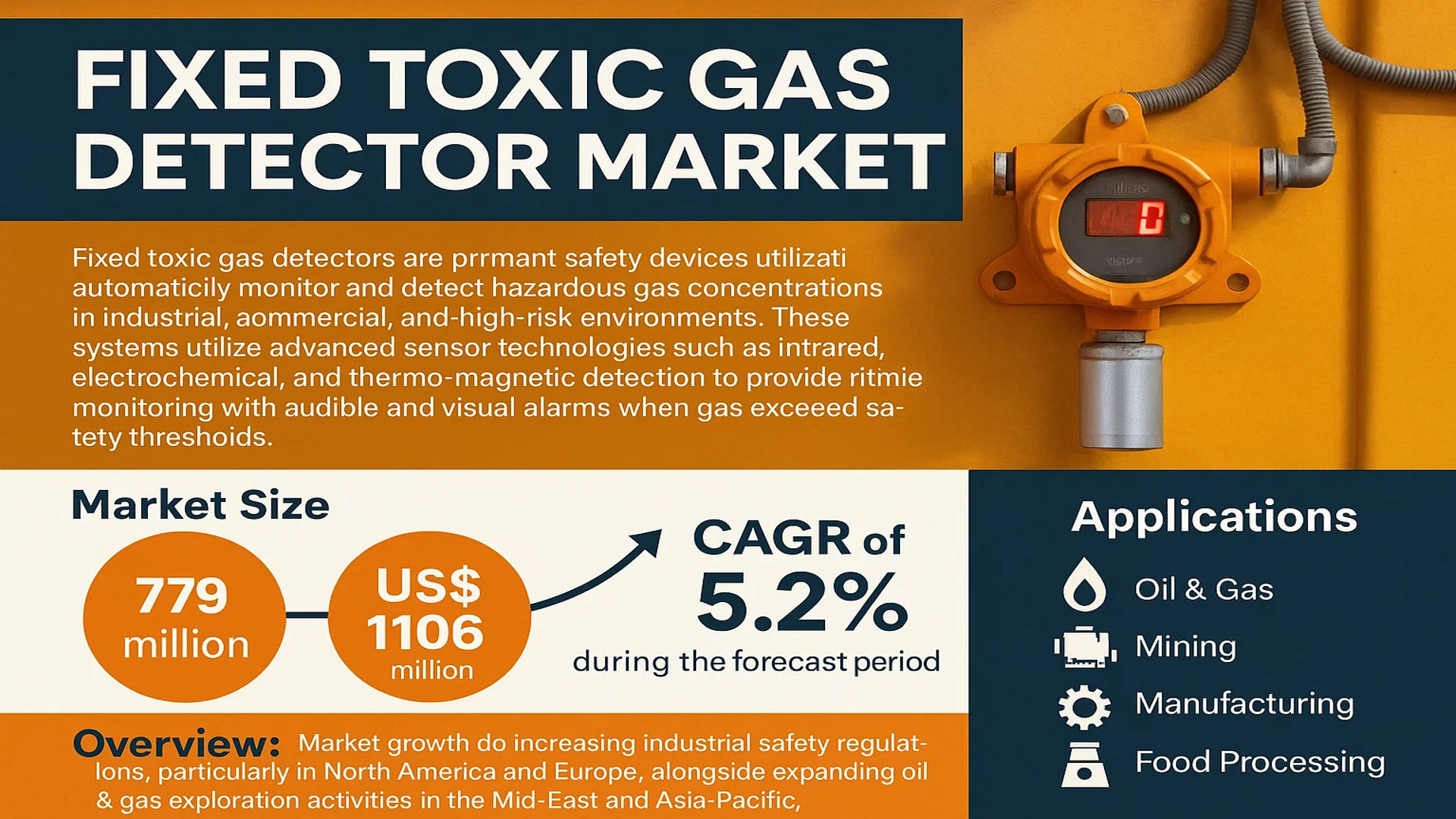

The global Fixed Toxic Gas Detector Market was valued at 779 million in 2024 and is projected to reach US$ 1106 million by 2032, at a CAGR of 5.2% during the forecast period.

Fixed toxic gas detectors are permanent safety devices designed to continuously monitor and detect hazardous gas concentrations in industrial, commercial, and high-risk environments. These systems utilize advanced sensor technologies such as infrared, electrochemical, and thermo-magnetic detection to provide real-time monitoring with audible and visual alarms when gas levels exceed safety thresholds. Major applications span oil & gas, mining, manufacturing, and food processing industries where worker safety regulations mandate their use.

Market growth is driven by increasing industrial safety regulations, particularly in North America and Europe, alongside expanding oil & gas exploration activities in the Middle East and Asia-Pacific. The infrared gas detector segment is gaining traction due to its long lifespan and minimal maintenance requirements, while electrochemical sensors remain dominant for their high accuracy in detecting low-concentration toxic gases. Key players like Honeywell, Drager, and MSA are investing in IoT-enabled smart detectors with cloud connectivity, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Workplace Safety Regulations Driving Adoption of Fixed Toxic Gas Detectors

Global occupational safety standards are becoming increasingly rigorous, compelling industries to invest in advanced gas detection systems. The International Labor Organization estimates toxic gas exposure causes over 2.4 million work-related deaths annually, prompting governments worldwide to implement stricter compliance measures. In 2024 alone, regulatory bodies across North America and Europe introduced 17 new workplace safety amendments specifically addressing toxic gas monitoring. These regulations mandate real-time gas detection in hazardous environments, directly fueling demand for fixed systems as they provide continuous monitoring – a critical requirement under modern safety protocols. Fixed detectors now account for over 60% of industrial gas detection installations globally, reflecting their essential role in regulatory compliance.

Expansion of Oil & Gas Industry Accelerating Market Growth

The global oil and gas sector, which represents the largest end-user of fixed toxic gas detectors, continues to expand with new refinery projects and pipeline networks. With energy demand projected to grow by 15% through 2032, major operators are investing heavily in safety infrastructure including gas detection systems. Recent data shows offshore platform installations incorporating 20-30 fixed detectors per facility, while large refineries deploy over 200 units each. This sector’s compound annual growth rate of 4.8% directly correlates with increased detector deployments, particularly in emerging markets where energy infrastructure development is most active. Major projects in the Middle East and Southeast Asia alone account for 35% of current fixed detector demand.

Technological Advancements Enhancing System Capabilities

Modern fixed gas detectors now incorporate artificial intelligence-enabled predictive analytics, wireless connectivity, and improved sensor technologies that boost reliability while reducing false alarms. The latest electrochemical sensors demonstrate 99.9% accuracy with lifespans exceeding 5 years, addressing historical maintenance challenges. Infrared-based systems have seen particular advancement, with newer models detecting parts-per-billion concentrations of toxic gases like hydrogen sulfide. These innovations reduce total cost of ownership while improving safety outcomes, making fixed systems increasingly attractive. Industry leaders report that 75% of new installations now specify these advanced features, driving replacement cycles and premium pricing opportunities.

MARKET RESTRAINTS

High Installation and Maintenance Costs Limiting Widespread Adoption

While essential for safety, fixed gas detection systems require significant capital expenditure for proper installation and calibration. A comprehensive fixed detection network for a medium-sized chemical plant can exceed $250,000 in initial costs, with annual maintenance adding 15-20% of initial investment. This pricing creates adoption barriers for small and medium enterprises, particularly in developing regions. Additionally, specialized personnel are needed for calibration and servicing, with technician shortages in some markets leading to 30% longer downtime periods between servicing. These cost factors currently restrict market penetration in price-sensitive segments despite the clear safety benefits offered.

Regulatory Approval Processes Slowing Product Launches

Stringent certification requirements for fixed gas detectors create lengthy approval timelines that can delay market entry by 9-18 months. The certification process often requires extensive field testing across different environmental conditions, with some jurisdictions demanding localized validation studies. This regulatory fragmentation complicates global product strategies and increases development costs. Recently introduced standards like IEC 60079 for explosive atmospheres have added new testing requirements, extending time-to-market for next-generation systems. While these standards improve safety, they temporarily constrain manufacturers’ ability to quickly deploy new technologies in response to emerging gas detection needs.

MARKET CHALLENGES

False Alarm Rates Remain Persistent Industry Challenge

Despite technological improvements, false alarms continue to plague approximately 15% of fixed gas detection installations annually, eroding user confidence. Environmental factors like humidity fluctuations or chemical interference account for 60% of these incidents, while sensor drift contributes another 25%. The consequences extend beyond nuisance alarms – facilities may implement costly emergency shutdowns in response to false readings. Some industries report spending up to $50,000 per false alarm event when factoring in lost productivity. Manufacturers face ongoing pressure to enhance sensor specificity while maintaining the rapid response times necessary for life safety applications.

Workforce Shortages Impacting Installation and Service Capabilities

The specialized nature of fixed gas detection system installation and maintenance has created a skills gap, with trained technicians in short supply globally. Industry surveys indicate a 22% vacancy rate for certified gas detection specialists, with the problem most acute in rapidly industrializing regions. This shortage leads to delayed system commissioning and extended maintenance intervals, potentially compromising safety. The complexity of modern networked systems exacerbates the issue, requiring technicians to possess both traditional gas detection knowledge and IT networking skills. Training programs have struggled to keep pace with industry demand, creating a bottleneck for market growth.

MARKET OPPORTUNITIES

Smart Factory Initiatives Creating New Application Areas

Industry 4.0 adoption is driving integration of fixed gas detectors with plant-wide monitoring systems, opening new value opportunities. Modern detectors equipped with Industrial IoT capabilities now represent 40% of new installations, up from just 15% five years ago. These connected systems enable predictive maintenance, remote calibration and centralized data analytics – features that improve safety while reducing operational costs. The smart factory market’s projected 11% CAGR through 2030 suggests substantial growth potential for intelligent gas detection solutions. Early adopters report 30% reductions in maintenance costs and 50% faster incident response times when using these integrated systems.

Emerging Economies Present Untapped Growth Potential

Developing nations undergoing rapid industrialization currently represent less than 20% of the fixed gas detector market despite accounting for over 60% of global industrial growth. Increasing safety awareness combined with tightening regulations in countries like India, Vietnam and Brazil is creating new demand. The Middle East alone plans to invest $120 billion in new oil and chemical facilities by 2030, all requiring comprehensive gas detection systems. Localized manufacturing and distribution partnerships are proving essential to capitalize on these opportunities, with regional players gaining market share through cost-competitive offerings tailored to local conditions.

Green Energy Transition Driving New Detection Requirements

The shift toward renewable energy and hydrogen economies is creating demand for specialized gas detection capabilities. Hydrogen fuel applications require detectors capable of sensing low concentrations with extreme precision, as hydrogen’s flammable range is four times wider than methane. Similarly, battery manufacturing facilities need systems to monitor toxic off-gassing during production. These emerging applications currently represent nearly $150 million in annual detector sales, growing at 18% yearly as clean energy investments accelerate. Manufacturers investing in application-specific sensor technologies stand to gain significant first-mover advantages in these nascent but rapidly expanding market segments.

FIXED TOXIC GAS DETECTOR MARKET TRENDS

Increasing Stringency of Safety Regulations to Drive Market Growth

The global fixed toxic gas detector market is witnessing robust growth, primarily driven by tightening industrial safety regulations worldwide. Governments and regulatory bodies have implemented stringent workplace safety standards, such as OSHA in the U.S. and ATEX directives in Europe, mandating continuous toxic gas monitoring in hazardous environments. Recent expansions in oil & gas infrastructure and chemical manufacturing have further propelled demand for advanced detection systems. The market has responded with smart detectors featuring IoT connectivity, enabling real-time remote monitoring and predictive maintenance capabilities that significantly reduce workplace hazards.

Other Trends

Technological Convergence with Industrial Automation

Integration with industrial IoT platforms has become a game-changer for fixed gas detection systems. Modern detectors now incorporate cloud-based data analytics, providing not just leak detection but also predictive insights about equipment failures. This convergence has been particularly valuable in refinery operations where over 60% of major incidents historically stem from equipment malfunctions. The adoption of wireless sensor networks has eliminated wiring constraints, allowing flexible deployment even in challenging industrial layouts.

Emerging Economies Present High-Growth Opportunities

The rapid industrialization across Asia-Pacific nations is creating substantial demand for fixed gas detection solutions. Countries like China and India are investing heavily in petrochemical complexes and manufacturing hubs, where regulatory frameworks are becoming increasingly aligned with global safety standards. Southeast Asian semiconductor fabrication plants now represent one of the fastest-growing application segments, requiring ultra-sensitive detection systems for specialty gases. Meanwhile, Middle Eastern nations continue to drive demand through ongoing megaprojects in energy infrastructure.

Electrochemical Sensors Gaining Traction

While infrared technology dominates hydrocarbon detection, electrochemical sensors are experiencing accelerated adoption for toxic gas monitoring due to their superior sensitivity at lower concentrations. Recent advancements have extended sensor lifespans beyond 3 years while maintaining accuracy, addressing a longstanding industry challenge. The mining sector has particularly benefited from these developments, as electrochemical detectors can identify noxious gases like hydrogen sulfide at concentrations as low as 1 ppm – well below immediately dangerous levels.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation Through Technology and Strategic Expansion

The global fixed toxic gas detector market features a competitive mix of established multinational corporations and specialized regional players. Honeywell International Inc. dominates the market with its comprehensive portfolio of industrial safety solutions, accounting for a significant share in 2024. The company’s strength lies in its integrated detection systems that combine infrared, electrochemical, and catalytic bead technologies for diverse industry applications.

Dragerwerk AG & Co. KGaA and MSA Safety Incorporated maintain strong positions through continuous innovation in detector accuracy and connectivity features. Both companies have recently introduced IoT-enabled detectors with predictive maintenance capabilities, addressing growing demand for smart safety solutions in oil & gas and chemical industries.

Japanese firm Riken Keiki Co., Ltd. shows particularly strong performance in Asian markets, where its compact detector designs and competitive pricing have captured over 15% of regional sales. Their recent partnership with Chinese manufacturers has further strengthened distribution networks across emerging markets.

Mid-sized competitors like Industrial Scientific Corporation are gaining traction through specialized solutions for mining applications, leveraging wireless network capabilities that outperform traditional fixed systems in underground environments. The company’s recent acquisition of a European sensor technology startup demonstrates its strategy to enhance technical capabilities.

List of Key Fixed Toxic Gas Detector Manufacturers

- Honeywell International Inc. (U.S.)

- Dragerwerk AG & Co. KGaA (Germany)

- MSA Safety Incorporated (U.S.)

- Riken Keiki Co., Ltd. (Japan)

- Industrial Scientific Corporation (U.S.)

- 3M Company (U.S.)

- New Cosmos Electric Co., Ltd. (Japan)

- Shenzhen ExSAF Electronics Co., Ltd. (China)

- United Technologies Corporation (U.S.)

- Johnson Controls International plc (Ireland)

- Emerson Electric Co. (U.S.)

- RKI Instruments, Inc. (U.S.)

Segment Analysis:

By Type

Electrochemical Gas Detector Leads the Market Due to High Accuracy and Versatility

The market is segmented based on type into:

- Infrared Gas Detector

- Thermo-magnetic Gas Detector

- Electrochemical Gas Detector

- Others

By Application

Oil and Gas Sector Holds Maximum Market Share Due to High Safety Regulations

The market is segmented based on application into:

- Oil and Gas

- Mining

- Manufacturing Industry

- Food and Beverage

- Others

By Technology

Fixed Detection Systems Remain Dominant Owing to Continuous Monitoring Needs

The market is segmented based on technology into:

- Fixed Detection Systems

- Portable Detection Devices

By End User

Industrial Sector Accounts for Major Share Due to High Risk of Gas Leakage

The market is segmented based on end user into:

- Industrial Facilities

- Commercial Buildings

- Public Infrastructure

- Residential Complexes

Regional Analysis: Fixed Toxic Gas Detector Market

North America

North America holds a dominant position in the global fixed toxic gas detector market, driven by strict occupational safety regulations, particularly in the U.S. with OSHA standards and the Chemical Safety Board’s guidelines. The oil & gas sector remains the largest end-user, accounting for over 35% of regional demand, followed by manufacturing facilities where OSHA’s Permissible Exposure Limits (PELs) mandate continuous gas monitoring. The recent push for industrial IoT integration has accelerated adoption of smart, networked gas detection systems. However, market maturity leads to slower growth compared to emerging regions, with replacements rather than new installations driving most sales.

Europe

Europe maintains stringent workplace safety directives through ATEX and IECEx certifications, making it the second-largest market for fixed toxic gas detectors. Germany and France lead in adoption due to their robust chemical industries, where electrochemical detectors dominate for precision in low-concentration measurements. The region shows growing interest in multi-gas detection systems, especially in offshore oil platforms following the EU’s Offshore Safety Directive revisions. Sustainability trends drive demand for detectors with lower false alarm rates and reduced maintenance needs, though high compliance costs restrain smaller enterprises.

Asia-Pacific

As the fastest-growing region, Asia-Pacific is propelled by China’s industrial expansion and India’s improving safety norms. China alone represents 42% of regional market value, with coal mining and petrochemical sectors investing heavily in infrared-based detectors for methane monitoring. Southeast Asian countries see increasing demand from electronics manufacturing plants where semiconductor fabrication requires precise toxic gas control. While cost sensitivity favors local manufacturers, international brands maintain premium positioning for critical applications. Emerging smart city projects incorporate gas detection in public infrastructure, creating new growth avenues.

Middle East & Africa

The oil-dependent economies of GCC nations drive most regional demand, particularly in Saudi Arabia and UAE where large refineries require extensive H2S monitoring systems. Infrastructure limitations in African nations restrict market growth, though South Africa’s mining safety improvements and Nigeria’s LNG projects show promise. The region faces challenges with detector calibration frequency and maintenance expertise gaps, prompting suppliers to focus on rugged, low-maintenance designs. Political instability in some areas hinders foreign investment in safety systems, but growing awareness of workplace risks supports gradual market expansion.

South America

Brazil dominates the region’s market, primarily serving its mining and ethanol production sectors where carbon monoxide detection is critical. Argentina’s chemical industry shows steady demand, while Andean countries lag due to inconsistent enforcement of safety regulations. Economic volatility makes long-term safety investments challenging, though multinational operators maintain high standards in oil & gas projects. The region shows potential for growth in wastewater treatment applications, but currency fluctuations and import dependencies create pricing pressures for detector suppliers.

Report Scope

This market research report provides a comprehensive analysis of the Global Fixed Toxic Gas Detector Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 779 million in 2024 and is projected to reach USD 1,106 million by 2032, growing at a CAGR of 5.2%.

- Segmentation Analysis: Detailed breakdown by product type (Infrared, Electrochemical, Thermo-magnetic), application (Oil & Gas, Mining, Manufacturing), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with the U.S. and China as key country markets.

- Competitive Landscape: Profiles of 15+ leading manufacturers including Honeywell, Drager, MSA, and Industrial Scientific, with market share analysis and recent strategic developments.

- Technology Trends: Assessment of emerging detection technologies, IoT integration, smart monitoring systems, and advancements in sensor accuracy and reliability.

- Market Drivers & Restraints: Analysis of industrial safety regulations, increasing energy demand, and urbanization versus high installation costs and maintenance challenges.

- Stakeholder Analysis: Strategic insights for gas detector manufacturers, industrial end-users, safety equipment providers, and regulatory bodies.

The research employs both primary and secondary methodologies, including manufacturer surveys, industry expert interviews, and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Fixed Toxic Gas Detector Market?

-> Fixed Toxic Gas Detector Market was valued at 779 million in 2024 and is projected to reach US$ 1106 million by 2032, at a CAGR of 5.2% during the forecast period.

Which key companies operate in this market?

-> Major players include Honeywell, Drager, MSA Safety, Industrial Scientific, Riken Keiki, and 3M, with the top 5 companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by stringent industrial safety regulations, increasing energy sector investments, and rising awareness of workplace safety across industries.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging technology trends?

-> Emerging trends include wireless monitoring systems, IoT-enabled detectors, AI-based predictive maintenance, and multi-gas detection capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...