MARKET INSIGHTS

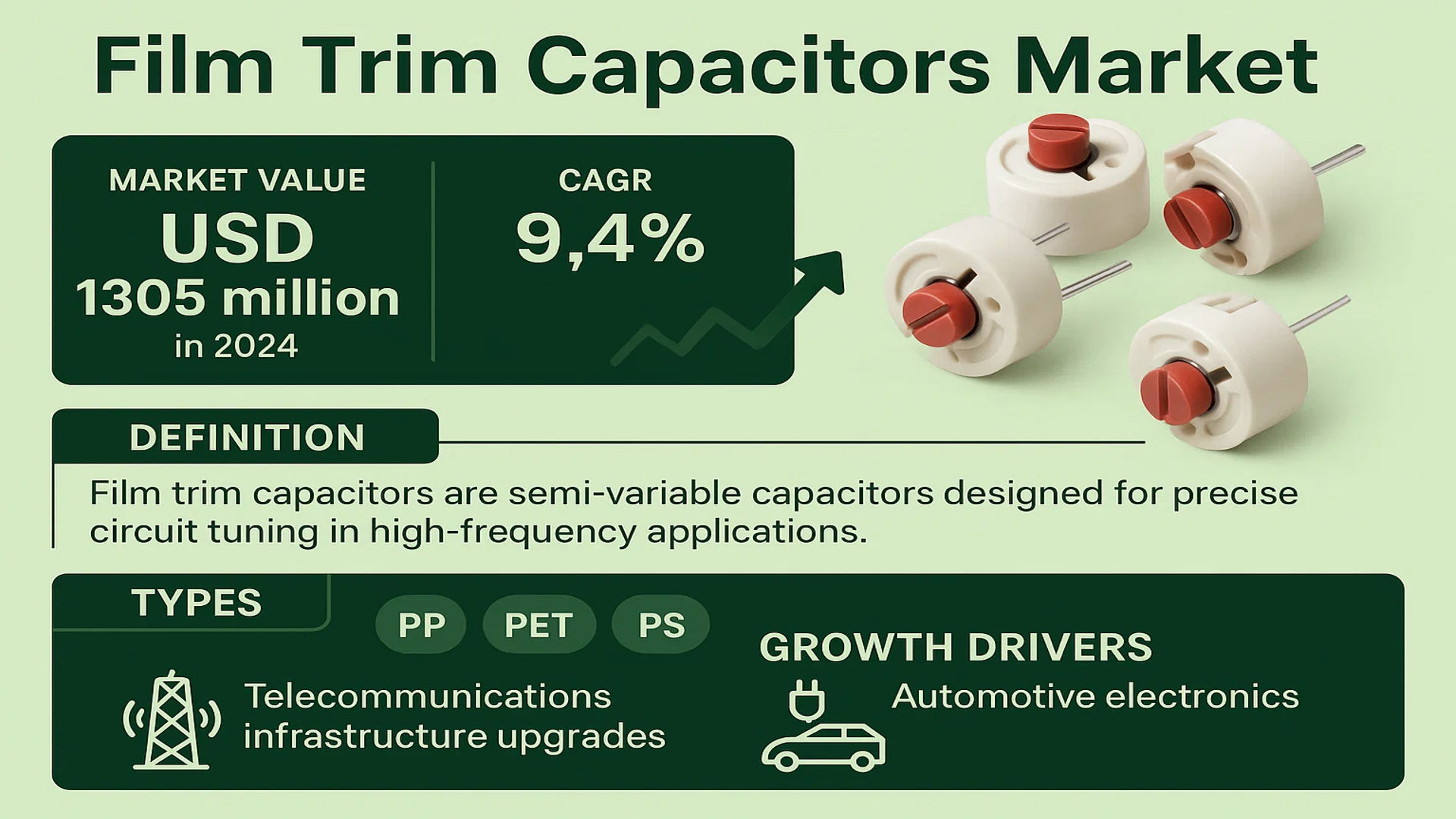

The global Film Trim Capacitors Market was valued at 1305 million in 2024 and is projected to reach US$ 2435 million by 2032, at a CAGR of 9.4% during the forecast period.

Film trim capacitors are semi-variable capacitors designed for precise circuit tuning in high-frequency applications. These components feature stacked or wound metal electrodes separated by plastic film dielectrics, allowing mechanical adjustment of capacitance values typically ranging from picofarads to tens of picofarads. Key variants include polypropylene (PP), polyester (PET), polystyrene (PS), and polycarbonate (PC) film types, each offering distinct stability and performance characteristics for applications requiring fine-tuning of resonance, filtering, or impedance matching.

Market growth is driven by increasing demand in telecommunications infrastructure upgrades and automotive electronics, where 5G deployment and electric vehicle adoption respectively create new tuning requirements. However, supply chain constraints for specialty films and miniaturization challenges present hurdles. Recent developments include Murata’s 2023 launch of ultra-compact PP film trimmers for IoT devices, reflecting industry efforts to address space constraints in modern electronics.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Consumer Electronics Sector Accelerates Demand for Film Trim Capacitors

The global consumer electronics industry has witnessed exponential growth in recent years, with market valuation projected to exceed $1.5 trillion by 2025. This surge directly fuels demand for precision electronic components like film trim capacitors, which are essential for tuning circuits in smartphones, wearables, and IoT devices. High-frequency applications in modern electronics require components with exceptional stability and low loss characteristics – exactly what film trim capacitors deliver. As manufacturers push for higher performance in smaller form factors, the need for reliable miniature tuning solutions intensifies. Leading smartphone brands now incorporate 20-30 trim capacitors per device for RF signal optimization, demonstrating the component’s critical role in product performance.

Automotive Electrification Trend Creates New Application Frontiers

Electric vehicle production is forecast to grow at 24% CAGR through 2030, creating unprecedented demand for advanced electronic components. Film trim capacitors play vital roles in EV power management systems, onboard chargers, and battery monitoring circuits where precise capacitance adjustment is required. Their excellent temperature stability and voltage resistance make them particularly suited for harsh automotive environments. The transition to 800V architectures in premium EVs further drives the need for high-voltage trim capacitors capable of withstanding demanding operating conditions while maintaining precise tuning capabilities.

Defense Modernization Programs Boost Military Applications

Global defense spending reached record levels exceeding $2.2 trillion in 2024, with significant allocations for electronic warfare and communication systems. Film trim capacitors are crucial components in radar systems, secure radios, and electronic countermeasure equipment where they provide reliable tuning in mission-critical applications. Military-grade requirements for shock resistance, wide temperature operation (-55°C to +125°C), and long-term stability align perfectly with the inherent strengths of film-based trimmer capacitors. Recent geopolitical tensions have accelerated replacement cycles for defense electronics, creating sustained demand for high-reliability components.

MARKET RESTRAINTS

Component Miniaturization Challenges Limit Performance Margins

While demand for smaller electronic devices grows, the physical limitations of film trim capacitors present significant engineering challenges. Reducing component size below certain thresholds compromises tuning resolution and stability – critical parameters for many precision applications. As device footprints shrink below 3mm x 3mm, maintaining the required capacitance range and adjustment precision becomes increasingly difficult without sacrificing reliability. This trade-off forces designers to either accept performance compromises or explore alternative tuning solutions in space-constrained applications.

Other Restraints

Supply Chain Vulnerabilities

The film capacitor industry faces material supply constraints for specialty polymer films like polypropylene and polytetrafluoroethylene (PTFE). These high-performance dielectric materials have limited production capacity globally, creating potential bottlenecks during demand surges. Recent geopolitical tensions have further complicated supply chains, with some key raw materials facing export restrictions or allocation controls.

Price Pressure from Digital Alternatives

The rise of digitally programmable capacitors in some application segments threatens traditional film trimmer markets. While digital solutions offer certain advantages in automated production environments, their higher cost and lower high-frequency performance still limit widespread adoption. However, ongoing improvements in digital capacitor technology continue to close the performance gap.

MARKET CHALLENGES

Maintaining Quality While Reducing Environmental Impact Presents Technical Hurdles

The electronics industry faces increasing pressure to eliminate hazardous substances and reduce environmental footprint, challenging traditional capacitor manufacturing processes. New EU regulations restrict certain dielectric materials and plating processes previously used in trimmer capacitors. Developing halogen-free, RoHS-compliant alternatives that match the electrical performance of established materials requires significant R&D investment. Performance parameters like temperature coefficient, dielectric absorption, and aging characteristics must be maintained while meeting stringent environmental standards – a complex balancing act for materials engineers.

Other Challenges

Skilled Labor Shortages

Precision capacitor manufacturing demands technicians with specialized skills in materials science and process engineering. The industry faces a growing talent gap as experienced workers retire without sufficient replacements entering the field. Training new personnel in the nuances of dielectric film processing and precision assembly requires substantial time and resources, slowing production ramp-ups during periods of high demand.

Quality Consistency at Scale

Maintaining tight capacitance tolerances (often ±0.1pF) across high-volume production runs presents ongoing quality control challenges. Variations in film characteristics, electrode deposition, and assembly processes can significantly impact final performance. Implementing statistical process control for these sensitive parameters demands continuous monitoring and adjustment throughout the manufacturing workflow.

MARKET OPPORTUNITIES

5G Infrastructure Rollout Creates New High-Frequency Applications

The global 5G infrastructure market is projected to grow at 40% CAGR through 2030, requiring innovative solutions for RF circuit tuning. Film trim capacitors with low loss characteristics at millimeter-wave frequencies (>24GHz) are finding new applications in 5G base stations, small cells, and beamforming antennas. Advanced polymer formulations with stable dielectric properties at these elevated frequencies command premium pricing, offering manufacturers higher-margin opportunities. The transition to Open RAN architectures further expands the addressable market by decentralizing radio unit components.

Medical Electronics Innovation Drives Specialty Demand

Medical device manufacturers increasingly incorporate wireless connectivity and implantable electronics, creating specialized requirements for reliable passive components. Film trim capacitors with biocompatible materials and hermetically sealed packaging enable new applications in diagnostic equipment and therapeutic devices. The medical electronics segment typically commands higher ASPs while requiring rigorous quality documentation and traceability – areas where established capacitor manufacturers can differentiate themselves.

Industrial IoT Expansion Broadens Application Scope

The growing adoption of industrial IoT solutions across manufacturing, energy, and logistics sectors presents significant growth potential for ruggedized electronic components. Film trim capacitors designed for extended temperature ranges and vibration resistance are finding increasing use in condition monitoring sensors, edge computing nodes, and industrial communication gateways. These applications often require specialized certifications (ATEX, UL Class I Div 2) that create barriers to entry while offering stable, long-term revenue streams for qualified suppliers.

FILM TRIM CAPACITORS MARKET TRENDS

Growing Demand for High-Frequency Applications Drives Market Expansion

The global film trim capacitors market has witnessed robust growth, reaching a valuation of $1.305 billion in 2024, with projections estimating a rise to $2.435 billion by 2032 at a 9.4% CAGR. This surge is primarily driven by increasing demand for high-frequency applications in telecommunications, RF circuits, and precision electronics. Film trim capacitors, known for their low loss, high stability, and excellent voltage resistance, are becoming indispensable in industries requiring fine-tuning of circuit parameters. The push toward miniaturization in electronics has further amplified their adoption, particularly in compact devices where space efficiency is critical.

Other Trends

Rising Adoption in Automotive Electronics

As the automotive industry accelerates toward electrification and advanced driver-assistance systems (ADAS), the need for reliable passive components like film trim capacitors has surged. These capacitors are essential in stabilizing high-frequency signals in automotive infotainment systems, radar modules, and electric vehicle (EV) power management systems. With the global EV market expected to grow at a CAGR of over 21% from 2024 to 2030, demand for film trim capacitors, particularly polypropylene (PP) film variants, is anticipated to rise significantly. Their ability to withstand temperature fluctuations and mechanical stress makes them ideal for harsh automotive environments.

Technological Innovations in Material Science

Advancements in dielectric materials, such as polypropylene (PP) and polyethylene terephthalate (PET) films, are enhancing capacitor performance while reducing footprint. Manufacturers are focusing on thin-film deposition techniques to improve capacitance stability and reduce losses at higher frequencies. The development of multi-layer film trim capacitors has enabled tighter capacitance tolerances, meeting the stringent requirements of 5G infrastructure and IoT devices. Leading suppliers, including Vishay Intertechnology and Murata Manufacturing, have introduced compact, high-reliability variants tailored for next-gen communication systems, further fueling market competitiveness.

While Asia-Pacific dominates production due to its electronics manufacturing hub, North America remains a key innovator, driven by defense and aerospace applications. However, supply chain disruptions and raw material price volatility pose challenges, prompting manufacturers to explore localized production strategies and alternative materials. The convergence of these trends underscores the film trim capacitor market’s pivotal role in enabling modern electronic advancements.

COMPETITIVE LANDSCAPE

Key Industry Players

Advancements in Precision Electronics Drive Innovation Among Capacitor Manufacturers

The global Film Trim Capacitors market features a dynamic competitive environment, blending established multinational corporations with specialized regional manufacturers. The market is moderately fragmented, with the top five players accounting for approximately 32% market share in 2024. Leading this segment, Vishay Intertechnology dominates through its extensive product portfolio featuring both PP and PET film capacitors, along with a strong distribution network spanning over 20 countries.

Murata Manufacturing has emerged as a formidable competitor, particularly in Asian markets, by focusing on miniaturized trimmer capacitor solutions for consumer electronics. Their recent development of ultra-compact PET-based capacitors (2.5mm x 2.0mm) has given them an edge in smartphone and wearable applications. Similarly, Knowles Precision Devices has strengthened its position by specializing in high-reliability capacitors for defense and aerospace applications, where precision and durability are paramount.

Meanwhile, several companies are adopting distinct strategies to enhance market presence:

- Passive Plus is expanding its U.S. production capacity by 35% to meet growing demand from the automotive sector

- JB Capacitors has introduced a new line of moisture-resistant trim capacitors specifically designed for industrial automation applications

- Hongming Electronic Science And Technology is leveraging cost advantages in the Chinese market to supply budget-sensitive OEMs

The competitive intensity is further amplified by technological collaborations, such as the recent partnership between RF Microwave and a major semiconductor manufacturer to develop integrated capacitor solutions for 5G infrastructure. This trend toward system-level integration is reshaping product development strategies across the industry.

List of Key Film Trim Capacitor Manufacturers

- Vishay Intertechnology (U.S.)

- Murata Manufacturing (Japan)

- Knowles Precision Devices (U.S.)

- Passive Plus (U.S.)

- JB Capacitors (China)

- RF Microwave (U.S.)

- Suntan Technology (Hong Kong)

- Kingtronics International (Hong Kong)

- Hongming Electronic Science And Technology (China)

- Arco Electronics (Taiwan)

Segment Analysis:

By Type

PP Film Segment Leads the Market Due to High Thermal Stability and Low Dielectric Loss

The market is segmented based on type into:

- PP Film

- Subtypes: Metallized PP, Non-metallized PP

- PET Film

- PS Film

- PC Film

- Others

By Application

Consumer Electronics Segment Dominates Due to Rising Demand for Compact and High-Performance Devices

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphones, Wearables, Laptops

- Automobile Industry

- Industrial Application

- National Defense and Military

- Others

By End User

Electronics Manufacturers Hold Largest Share Due to Widespread Use in Circuit Design

The market is segmented based on end user into:

- Electronics Manufacturers

- Automotive OEMs

- Defense Contractors

- Research Institutions

Regional Analysis: Film Trim Capacitors Market

Asia-Pacific

The Asia-Pacific region dominates the global Film Trim Capacitors market, accounting for the largest share of both revenue and volume in 2024. This leadership position stems from the region’s booming electronics manufacturing sector, particularly in China, Japan, and South Korea. China alone contributes over 40% of global production, fueled by massive investments in 5G infrastructure, IoT devices, and automotive electronics. The region benefits from strong local supply chains, cost-competitive manufacturing, and increasing R&D expenditure in advanced capacitor technologies. While PP film capacitors remain the dominant product type due to their cost-effectiveness, there’s growing demand for high-performance PET film variants in precision applications. Local players like Hongming Electronic Science and Technology compete closely with global leaders, creating a dynamic market landscape. However, intellectual property protection remains a concern affecting technology transfer in some markets.

North America

North America represents the second-largest market for Film Trim Capacitors, characterized by high-value applications in aerospace, defense, and telecommunications. The U.S. leads regional demand, with stringent quality standards driving adoption of premium-grade capacitors from manufacturers like Passive Plus and Vishay Intertechnology. The market shows strong preference for PP and PC film capacitors that meet MIL-spec requirements for military applications. Recent developments include increased R&D investments in space-grade capacitors by NASA contractors. While manufacturing has declined relative to Asia, the region maintains technological leadership in specialty capacitors, with the medical electronics sector emerging as a key growth driver. Trade policies and semiconductor supply chain realignment may significantly impact future market dynamics.

Europe

Europe’s Film Trim Capacitors market emphasizes sustainability and precision engineering, with Germany and the UK being the largest consumers. EU regulations on RoHS and REACH have accelerated development of eco-friendly capacitor technologies, creating opportunities for PET film variants. The automotive sector drives significant demand, particularly for capacitors used in electric vehicle power electronics and ADAS systems. European manufacturers like Farnell focus on high-reliability applications, competing through quality rather than price. The market faces challenges from energy cost volatility and the gradual relocation of electronics manufacturing outside the region. However, strong collaboration between academia and industry continues to yield innovations in capacitor materials and miniaturization techniques.

South America

South America represents a developing market for Film Trim Capacitors, with Brazil accounting for nearly 60% of regional demand. Growth is primarily driven by consumer electronics assembly and industrial automation projects, though market expansion faces obstacles from economic instability and import dependency. Local production remains limited, with most capacitors sourced from Asian suppliers. The telecommunications sector shows promising growth potential as countries upgrade their network infrastructure. Price sensitivity favors PP film capacitors, though this is gradually changing with the expansion of Brazil’s automotive electronics sector. Supply chain disruptions and currency fluctuations continue to challenge market stability across the region.

Middle East & Africa

The Middle East & Africa region presents a nascent but growing market, with development focused primarily on GCC countries and South Africa. Demand stems from infrastructure projects, oil & gas equipment, and limited electronics manufacturing. The market relies heavily on imports, particularly from Asia and Europe. While current volumes remain modest relative to other regions, long-term growth prospects appear strong as countries diversify their economies and invest in smart city initiatives. The defense sector represents a key niche market for high-reliability capacitors. Lack of local manufacturing capabilities and limited technical expertise currently constrain more rapid market expansion, though several free trade zones are attempting to attract capacitor producers through incentives.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Film Trim Capacitors markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Film Trim Capacitors market was valued at USD 1,305 million in 2024 and is projected to reach USD 2,435 million by 2032, growing at a CAGR of 9.4%.

- Segmentation Analysis: Detailed breakdown by product type (PP Film, PET Film, PS Film, PC Film), application (Consumer Electronics, Automobile Industry, Industrial Application, National Defense & Military, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Passive Plus, Vishay Intertechnology, Murata Manufacturing, Knowles Precision Devices, and others, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging capacitor technologies, material advancements, and evolving industry standards for high-frequency applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for precision electronics, along with challenges like supply chain constraints and raw material price volatility.

- Stakeholder Analysis: Insights for component manufacturers, OEMs, system integrators, and investors regarding strategic opportunities in the evolving electronics ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, manufacturer data, and verified market intelligence to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Film Trim Capacitors Market?

-> Film Trim Capacitors Market was valued at 1305 million in 2024 and is projected to reach US$ 2435 million by 2032, at a CAGR of 9.4% during the forecast period.

Which key companies operate in Global Film Trim Capacitors Market?

-> Key players include Passive Plus, Vishay Intertechnology, Murata Manufacturing, Knowles Precision Devices, JB Capacitors, and RF Microwave, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for precision electronics, expansion of 5G infrastructure, and increasing adoption in automotive electronics.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by electronics manufacturing in China, Japan, and South Korea, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include development of high-frequency capacitors, miniaturization of components, and adoption of advanced dielectric materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...