Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market Insights

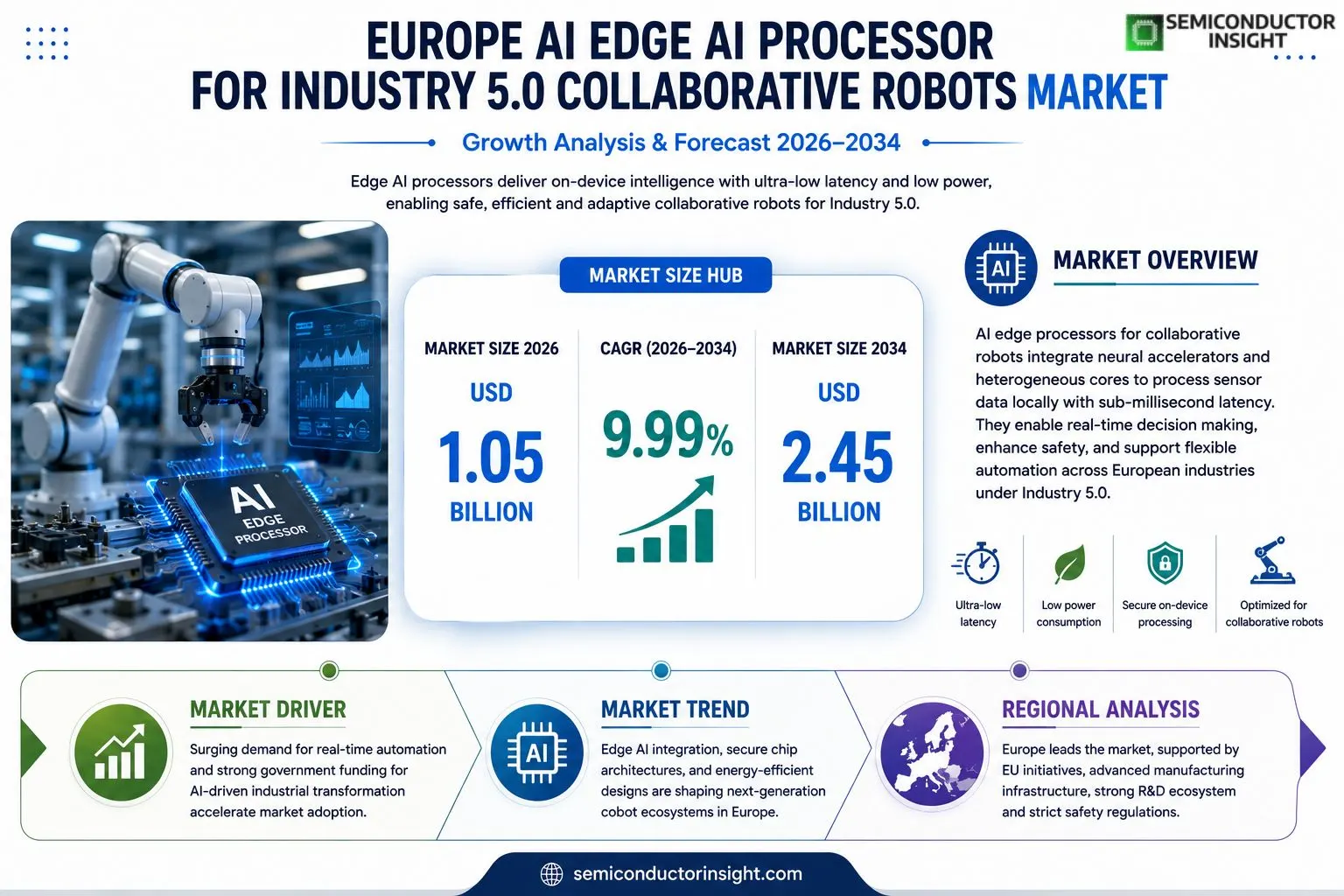

Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.05 billion in 2025 to USD 2.4545 billion by 2034, exhibiting a CAGR of 9.99% during the forecast period.

Edge AI processors designed for collaborative robots are compact semiconductor solutions that deliver on‑device inference with sub‑millisecond latency while consuming minimal power.These chips integrate neural‑network accelerators, heterogeneous cores and secure enclaves, enabling cobots to process sensor data locally and adapt actions in real timekey requirements of Industry 5.0 where humans and machines work side‑by‑side.The market is experiencing rapid growth because European manufacturers are accelerating digital transformation through initiatives such as Horizon Europe and the European Chips Act.Furthermore, rising demand for flexible automation in sectors like automotive, electronics and logistics drives adoption of edge‑enabled cobots.However

MARKET DRIVERS

Increasing Demand for Real‑Time Automation

European manufacturers are accelerating adoption of Industry 5.0 principles, driving a sharp rise in collaborative robot deployments that require edge AI processors capable of sub‑millisecond decision making. Over 40 % of Tier‑1 automotive plants have integrated edge‑enabled cobots to enhance flexible assembly lines.

Government Incentives and Standards

EU funding programs such as Horizon Europe allocate €2 billion annually to AI‑enabled automation, encouraging manufacturers to invest in low‑latency processors. New safety standards also favor on‑device inference, reducing reliance on cloud connectivity.

➤ Edge AI processors deliver up to 30 % lower energy consumption compared with centralized GPU solutions, extending robot uptime in high‑throughput facilities.

These drivers collectively shape a robust growth trajectory for Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market.

MARKET CHALLENGES

Integration Complexity

Deploying edge AI chips within existing cobot architectures requires redesign of power and thermal budgets. Many OEMs report 15‑20 % longer development cycles due to firmware compatibility issues.

Other Challenges

Supply Chain Vulnerability

Semiconductor shortages have limited the availability of advanced nodes, constraining volume production and driving lead times beyond six months for critical edge modules.

MARKET RESTRAINTS

High Capital Expenditure

Edge AI processor platforms command premium pricing, often exceeding €1,500 per unit, which deters small‑scale manufacturers from immediate adoption. The total cost of ownership can be 30 % higher than legacy controller solutions.Regulatory certification processes for safety‑critical cobots add further expense, extending project budgets by an average of 12 months for full compliance.Limited availability of skilled engineers proficient in both robotics and low‑level AI optimization slows scale‑up, creating a talent‑supply restraint across the region.

MARKET OPPORTUNITIES

Smart Factory Expansion

Projected investment of €12 billion in smart factory projects across Germany, France, and the Nordics creates a sizable market for edge AI processors that can be embedded in collaborative robots for on‑site quality inspection and predictive maintenance.Emerging niche applicationssuch as collaborative robots for pharmaceutical aseptic handlingrequire ultra‑low latency inference, opening a 15 % growth niche for specialized edge processors.Partnerships between semiconductor firms and system integrators are accelerating the launch of modular AI processor kits, offering a fast‑track route to market and a potential 10 % market share gain for early adopters.

Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market Trends

Policy‑Driven Expansion of Edge AI Processors

European governments are leveraging the European Chips Act and Horizon Europe programmes to subsidise the design and qualification of edge AI processors that are optimised for collaborative robots. This policy momentum creates a predictable supply chain for manufacturers and lowers total cost of ownership, encouraging OEMs to integrate AI‑enabled cobots on existing production lines. As a result, Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market is seeing a wave of pilot projects in automotive assembly, high‑mix electronics, and logistics hubs where sub‑millisecond inference and ultra‑low power consumption are critical.

Other Trends

Security‑Centric Architectures

Recent releases from European chip designers include hardware‑based secure enclaves and encrypted model‑loading pathways. These features address stringent GDPR‑compliant data handling requirements and protect proprietary AI models from tampering. By embedding security primitives directly into the silicon, cobot operators can process visual and tactile sensor streams on‑device without exposing raw data to external networks, a capability that aligns closely with Industry 5.0’s emphasis on safe human‑machine collaboration.

Sector‑Specific Adoption Accelerates

Manufacturers in the automotive sector are adopting edge AI processors to enable real‑time quality inspection and adaptive torque control, while logistics providers employ them for dynamic path planning around human workers. In the electronics arena, flexible assembly stations rely on the low‑latency decision‑making afforded by these processors to switch between product variants within seconds. Across these verticals, Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market benefits from an ecosystem of specialized software stacks that translate domain‑specific algorithms into optimized firmware, shortening time‑to‑value for end users.

COMPETITIVE LANDSCAPE

Key Industry Players

Europe AI Edge Processors Powering Industry 5.0 Cobots

The European edge‑AI processor market for collaborative robots is anchored by a handful of large semiconductor firms that combine deep automotive and industrial experience with dedicated AI accelerators. STMicroelectronics leads the segment with its “STAI” family, offering sub‑millisecond inference and low‑power operation that fit the tight form‑factor of cobots. Infineon Technologies follows closely, leveraging its secure enclave technology to meet stringent Industry 5.0 safety standards. NXP Semiconductors’ EdgeLock‑AI solutions provide heterogeneous cores that enable real‑time sensor fusion, while Graphcore’s IPU‑based modules bring high‑throughput neural‑network processing to European factories. This tiered structure creates a clear hierarchy: multinational chipmakers control the high‑volume, safety‑critical space, while specialized AI‑centric startups occupy niche performance‑focused niches.Beyond the dominant tier, a vibrant ecosystem of niche players enriches the competitive landscape. CEVA’s DSP‑AI cores are adopted by midsize robot integrators seeking cost‑effective compute. Arm’s Cortex‑M55 with Ethos‑U55 accelerators offers a scalable pathway for OEMs to embed intelligence without redesigning hardware. Finnish startup Bittium delivers secure edge processors for human‑machine collaboration, and France’s Lattice Semiconductor supplies low‑power FPGA‑based AI engines for modular cobot designs. German firm dSPACE provides development platforms that integrate edge AI with real‑time testing, while UK‑based GrapheneOS focuses on secure firmware for AI processors. These companies collectively deepen the technology pool, fostering rapid innovation and regional diversification.

List of Key AI Edge Processor Companies Profiled

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Graphcore

- CEVA DSP

- Arm Ltd.

- Bittium

- Lattice Semiconductor

- dSPACE GmbH

- GrapheneOS

- Flex Logix Technologies

- Silicon Valley AI (European Hub)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neural‑Accelerator Based Processors are emerging as the preferred architecture for collaborative robots because they deliver ultra‑low latency inference while maintaining minimal power draw.

|

| By Application |

|

Automotive Assembly drives the most sophisticated edge‑AI processor requirements as cobots must synchronize with human workers on complex assembly lines.

|

| By End User |

|

Original Equipment Manufacturers (OEMs) prioritize edge AI processors that can be tightly integrated into robot hardware platforms, facilitating seamless firmware and AI model co‑development.

|

| By Deployment Model |

|

On‑Premise Edge Nodes dominate the European cobot landscape because manufacturers aim to keep data processing local for latency, security and compliance reasons.

|

| By Industry Vertical |

|

Automotive remains the flagship vertical where edge AI processors in collaborative robots unlock new levels of flexibility and safety.

|

Regional Analysis: Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market

Europe

Rising demand for flexible automation, coupled with EU initiatives promoting digital transformation, fuels adoption of edge AI processors. Manufacturers seek low‑latency, high‑reliability solutions that empower collaborative robots to operate safely alongside human workers in complex tasks.

Harmonised safety standards under the Machinery Directive and emerging AI governance frameworks provide clear pathways for deployment, reducing compliance uncertainty for vendors and end‑users alike.

Edge computing architectures are being integrated with 5G connectivity, enabling collaborative robots to process sensor data locally, enhance response times, and minimise reliance on centralized cloud resources.

European chipmakers and system integrators are forming alliances to co‑develop processor‑robot platforms, positioning themselves against incumbents through localized expertise and tailored solutions.

North America

North America remains a strong adopter of collaborative robotics, yet its edge AI processor market is characterised by a focus on scale and cloud integration rather than localized edge solutions. Companies are leveraging extensive data‑center ecosystems to support robot fleets, which contrasts with Europe’s emphasis on on‑premise processing for latency‑critical tasks. The region’s regulatory environment is less prescriptive, allowing faster market entry but also presenting challenges around data sovereignty and interoperability. Investment in advanced semiconductor manufacturing sustains a robust supply chain, but the strategic push toward sustainability lags behind European initiatives. Consequently, North America plays a complementary role, providing complementary technologies that can be integrated with European edge‑centric deployments.

Asia‑Pacific

Asia‑Pacific exhibits rapid growth in industrial automation, driven by large‑scale manufacturing hubs in China, Japan, and South Korea. While the region excels in high‑volume production of AI chips, its approach to edge processing for collaborative robots often prioritises cost efficiency over stringent safety standards. Government programmes such as “Made in China 2025” accelerate adoption, yet divergent regulatory frameworks can create fragmentation. Partnerships between Asian semiconductor firms and European robot manufacturers are emerging, enabling technology transfer that supports Europe’s edge‑focused strategies while offering Asian markets access to advanced safety‑compliant solutions.

South America

South America’s industrial sector is undergoing gradual digital transformation, with emerging interest in collaborative robots to address labour shortages and enhance productivity. Edge AI processor adoption is still nascent, constrained by limited local chip production and reliance on imported technologies. Regional trade agreements are facilitating access to European processor modules, and pilot projects in Brazil and Argentina demonstrate the potential for localized edge computing to improve real‑time decision making on the factory floor. However, the market remains small, and growth will depend on investment in infrastructure and skill development.

Middle East & Africa

The Middle East & Africa region is leveraging its strategic position in supply chains to explore advanced automation. Gulf states are investing in smart‑factory initiatives that require robust edge AI capabilities to meet energy‑efficiency targets. In Africa, early‑stage deployments focus on modular collaborative robots that can operate in remote locations with limited connectivity, making edge processing essential. Regulatory environments are evolving, with emerging standards that align closely with European safety guidelines, offering a pathway for technology alignment and cross‑regional collaboration.

Report Scope

This market research report provides a comprehensive analysis of the Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market?

-> Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market was valued at USD 1.05 billion in 2025 and is expected to reach USD 2.45 billion by 2034.

Which key companies operate in Europe AI Edge AI Processor for Industry 5.0 Collaborative Robots Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...