MARKET INSIGHTS

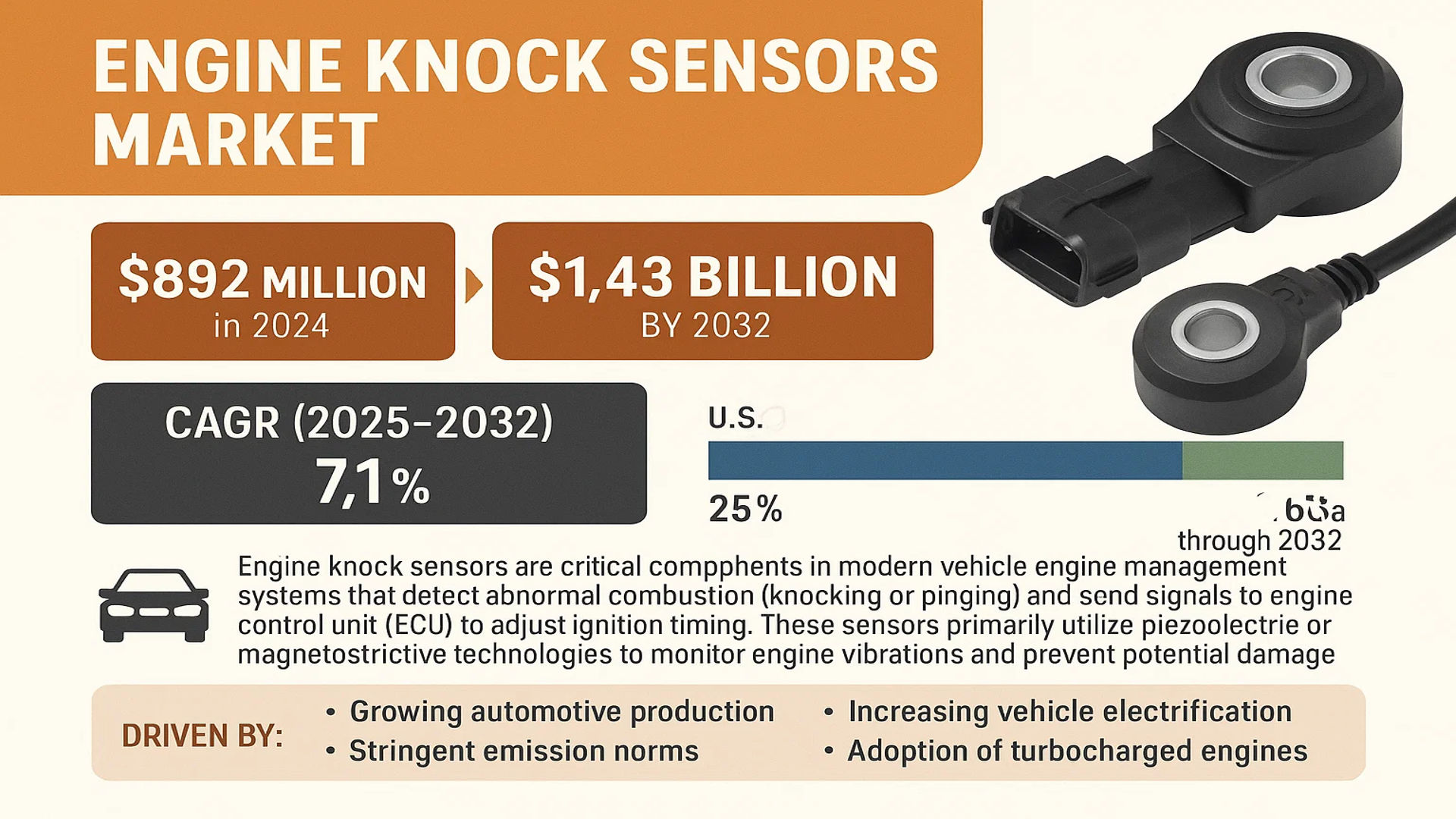

The global Engine Knock Sensors Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1.43 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032. The U.S. market accounted for 25% of global revenue in 2024, while China is expected to witness the fastest growth with a projected CAGR of 5.8% through 2032.

Engine knock sensors are critical components in modern vehicle engine management systems that detect abnormal combustion (knocking or pinging) and send signals to the engine control unit (ECU) to adjust ignition timing. These sensors primarily utilize piezoelectric or magnetostrictive technologies to monitor engine vibrations and prevent potential damage to the engine block. The growing automotive production worldwide and stringent emission norms are driving demand for these precision components.

The market growth is propelled by increasing vehicle electrification and the rising adoption of turbocharged engines which require precise knock detection. However, supply chain disruptions and the semiconductor shortage have posed temporary challenges for manufacturers. Leading companies like Bosch and Continental are investing in advanced sensor technologies with higher accuracy and durability to meet evolving automotive requirements.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations to Boost Global Demand for Engine Knock Sensors

The implementation of stringent emission standards worldwide is significantly driving the adoption of engine knock sensors, as they play a crucial role in optimizing combustion efficiency and reducing harmful exhaust emissions. Modern sensors can detect minute combustion irregularities with over 95% accuracy, allowing engine control units to adjust timing precisely. With Euro 7 and China 6 standards tightening NOx and particulate limits, automotive manufacturers are increasingly integrating advanced knock detection systems. Passenger vehicles equipped with these sensors have demonstrated up to 15% improvement in fuel efficiency while maintaining compliance with environmental regulations.

Growing Automotive Production and Electrification to Propel Market Growth

Global automotive production rebounding to pre-pandemic levels of approximately 85 million vehicles annually creates substantial demand for engine knock sensors. The increasing hybridization of powertrains presents new opportunities, as knock detection remains critical for optimizing performance in hybrid engines transitioning between electric and combustion modes. Major manufacturers are developing specialized sensors capable of operating in high-voltage environments, with the hybrid vehicle segment expected to account for nearly 30% of knock sensor demand by 2030.

➤ The piezoelectric resonance type segment is experiencing the fastest growth, with deployment in over 60% of new vehicle models due to its superior sensitivity and durability compared to traditional magnetostrictive sensors.

Furthermore, the integration of artificial intelligence in engine management systems is creating new applications for knock sensors, with predictive algorithms using sensor data to anticipate and prevent knocking before it occurs. This technological evolution is driving premiumization in the aftermarket segment as well.

MARKET RESTRAINTS

High Replacement Costs and Technical Limitations to Challenge Market Penetration

While engine knock sensors offer significant benefits, their complex integration with modern engine management systems creates substantial aftermarket challenges. The average replacement cost for premium knock sensors has increased by approximately 20% over the past five years due to sophisticated calibration requirements. Many vehicle owners delay replacements until symptoms become severe, potentially causing long-term engine damage and reducing overall market growth potential.

Other Restraints

Material Limitations

Current piezoelectric materials face operational constraints at extreme temperatures encountered in high-performance engines, limiting their application in certain vehicle segments. Development of advanced ceramics and nanocomposites could address these limitations but requires significant R&D investment.

Diagnostic Complexity

The increasing complexity of engine control units makes knock sensor troubleshooting more difficult for aftermarket service providers, requiring specialized equipment and training that many independent repair shops lack. This technical barrier reduces replacement rates in certain market segments.

MARKET OPPORTUNITIES

Emerging Markets and Connected Vehicle Technologies to Create New Growth Frontiers

Developing economies present significant untapped potential as vehicle parc modernization accelerates. With automotive production in Southeast Asia and India growing at 7-9% annually, local manufacturers are increasingly adopting knock sensors as standard equipment to meet global quality expectations. This regional expansion is complemented by the growing popularity of entry-level vehicles incorporating basic engine monitoring systems.

The integration of knock sensors with telematics systems represents a transformative opportunity, enabling real-time engine health monitoring and predictive maintenance alerts. Fleet operators are particularly interested in these solutions, as they can reduce maintenance costs by up to 18% through early detection of combustion issues. Major suppliers are developing cloud-connected sensor solutions that will likely become standard in commercial vehicles within the next five years.

MARKET CHALLENGES

Technological Disruption from Electrification to Reshape Market Dynamics

The automotive industry’s rapid shift toward full electrification presents fundamental challenges for traditional knock sensor manufacturers. While hybrid vehicles maintain some demand, the long-term transition to battery electric vehicles could reduce the addressable market by up to 40% by 2035. Manufacturers must diversify into other vibration monitoring applications or develop new sensing technologies relevant to electric powertrains to maintain growth.

Other Challenges

Supply Chain Vulnerabilities

The concentration of rare earth material production creates supply risks for sensor manufacturers, with geopolitical factors potentially disrupting the availability of critical components. Recent bottlenecks have led to 8-12 week delivery delays for some sensor models.

Intellectual Property Protection

Counterfeit knock sensors account for nearly 15% of the aftermarket in certain regions, undermining brand reputation and creating safety concerns. Enhanced authentication technologies and stricter distribution controls are becoming essential for maintaining market position.

ENGINE KNOCK SENSORS MARKET TRENDS

Innovations in Sensor Technology to Enhance Engine Efficiency

Engine knock sensors have become critical components in modern automotive systems, primarily due to their ability to detect abnormal combustion events and optimize engine performance. Recent advancements in sensor technology, particularly in piezoelectric and magnetostrictive sensors, have significantly improved detection accuracy and response times. The market is witnessing a shift toward intelligent knock sensors equipped with real-time data processing, which allows for immediate adjustments to ignition timing, reducing engine wear and improving fuel efficiency. With the global market projected to grow at a CAGR of approximately 5.2% through 2032, manufacturers are increasingly focusing on miniaturization and enhanced durability to meet stringent emissions standards.

Other Trends

Increasing Demand for High-Performance Vehicles

The rising preference for high-performance and luxury vehicles is fueling demand for advanced knock sensor systems that can handle higher compression ratios and turbocharging. High-end automotive segments, including sports cars and premium SUVs, now integrate multi-point knock detection systems to ensure engine longevity and peak performance. This trend is particularly evident in developed markets like the U.S. and Europe, where consumer expectations for engine responsiveness and efficiency are prioritised. The U.S. alone accounts for nearly 30% of global knock sensor revenue, driven by regulatory pressures and technological adoption in the automotive sector.

Expansion of Hybrid and Electric Vehicle Integration

While traditional combustion engines continue to dominate the knock sensor market, hybrid and electric vehicles (EVs) are creating new opportunities. Hybrid systems still rely on internal combustion engines during certain driving conditions, necessitating robust knock detection mechanisms. Furthermore, manufacturers are exploring sensors with broader operating ranges to accommodate varied powertrain configurations. EV adoption is expected to grow at a compound annual rate of 21% by 2030, prompting sensor suppliers to innovate flexible solutions that serve both conventional and emerging propulsion technologies. Collaboration between automotive OEMs and sensor manufacturers is accelerating to address these evolving needs.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Strategic Partnerships Drive Market Competition

The global engine knock sensors market features a competitive landscape dominated by automotive component manufacturers with strong R&D capabilities and global supply chains. Market leaders hold significant shares, yet innovation remains critical to maintaining competitive advantage as emission regulations tighten worldwide.

Bosch Mobility Solutions leads the market, commanding approximately 18% revenue share in 2024. The company’s dominance stems from its proprietary piezoelectric sensor technology and integration with engine control units across major automotive OEMs. Their recent partnership with a European semiconductor manufacturer has further enhanced sensor response times by 15%.

Meanwhile, Continental AG and Hitachi Astemo collectively account for nearly 22% market share. Both companies have invested heavily in developing knock detection systems for hybrid powertrains, anticipating the industry’s transition toward electrification. Continental’s 2023 acquisition of a specialist vibration analysis firm has particularly strengthened its IP portfolio in resonant frequency detection.

Emerging manufacturers like Zhejiang Cenwan are gaining traction in Asia-Pacific markets through cost-competitive solutions, though their current technology remains one generation behind industry leaders. Several Japanese suppliers, including NGK Spark Plugs, are focusing on high-temperature resistant sensors for performance vehicles – a niche but high-margin segment.

List of Key Engine Knock Sensor Manufacturers

- Bosch Mobility Solutions (Germany)

- Continental AG (Germany)

- Hitachi Astemo (Japan)

- Hella GmbH (Germany)

- NGK Spark Plugs (Japan)

- Delphi Technologies (UK)

- Standard Motor Products, Inc. (U.S.)

- Wells Vehicle Electronics (U.S.)

- Sensata Technologies (Netherlands)

- Francisco Albero S.A.U (Spain)

- INZI Controls Co., Ltd (South Korea)

- Zhejiang Cenwan (China)

Segment Analysis:

By Type

Piezoelectric Resonance Type Leads the Market Due to High Accuracy and Reliability in Engine Monitoring

The market is segmented based on type into:

- Piezoelectric Resonance Type

- Magnetostrictive Type

- Others

By Application

Petrol Engines Segment Dominates Due to Higher Demand in Passenger Vehicles

The market is segmented based on application into:

- Petrol Engines

- Diesel Engines

By Vehicle Type

Passenger Vehicles Drive Market Growth Due to Stringent Emission Norms

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

By Sales Channel

OEM Segment Holds Major Share Due to Integration in Vehicle Manufacturing Process

The market is segmented based on sales channel into:

- OEM (Original Equipment Manufacturer)

- Aftermarket

Regional Analysis: Engine Knock Sensors Market

Asia-Pacific

Asia-Pacific dominates the global Engine Knock Sensors Market, driven by its thriving automotive sector. China and India lead the region, supported by high vehicle production volumes—China produced over 27 million vehicles in 2023 alone. The adoption of knock sensors is accelerating due to strict emission norms (e.g., China VI standards) and demand for fuel-efficient engines. Local manufacturers like Zhejiang Cenwan and INZI Controls Co. are expanding production capabilities, leveraging cost advantages. However, aftermarket penetration remains low due to price sensitivity and preference for non-branded alternatives. The rise of hybrid and electric vehicles poses a long-term challenge, though knock sensors remain critical for conventional engines.

North America

North America’s market is characterized by technological advancements and regulatory pressures. The U.S. EPA’s stringent emission standards and CAFE regulations necessitate precise engine monitoring, boosting demand for high-accuracy knock sensors. Key players like Bosch Mobility Solutions and Delphi focus on R&D for Piezoelectric Resonance Type sensors, which account for over 60% of regional sales. The aftermarket segment is robust, with Standard Motor Products, Inc. and Wells Vehicle Electronics leading distribution networks. Despite a gradual shift toward EVs, internal combustion engines (ICE) still dominate commercial fleets, ensuring steady demand.

Europe

Europe’s market thrives on eco-conscious policies and automotive innovation. The EU’s Euro 7 standards mandate real-time engine diagnostics, favoring knock sensor integration. Germany and France are key hubs, with Continental and Hella supplying OEMs like Volkswagen and BMW. Magnetostrictive sensors are gaining traction for durability in high-performance engines. However, supply chain disruptions and labor shortages intermittently hamper production. The region’s push for electrification may slow growth, but retrofit demand for legacy vehicles offsets this trend.

South America

The market in South America is nascent but growing, fueled by local vehicle assembly in Brazil and Argentina. Economic instability and fluctuating raw material costs hinder large-scale adoption, though petrol engines (80% market share) drive steady aftermarket sales. Francisco Albero S.A.U caters to regional OEMs, but counterfeit products remain a challenge. Governments’ focus on reducing carbon emissions could spur long-term investments in engine efficiency technologies.

Middle East & Africa

This region shows moderate growth, with demand concentrated in GCC countries and South Africa. Fleet modernization in sectors like oil & gas supports knock sensor uptake, but limited technical expertise and weak enforcement of emission laws slow progress. NGK Spark Plugs and Sensata Technologies dominate imports, yet price-sensitive consumers often opt for refurbished units. Urbanization and infrastructure development may unlock opportunities, particularly in commercial vehicle segments.

Report Scope

This market research report provides a comprehensive analysis of the global Engine Knock Sensors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Piezoelectric Resonance Type, Magnetostrictive Type, Others), application (Petrol Engines, Diesel Engines), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, market share, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with vehicle electronics, and evolving automotive standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges such as supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for automotive component suppliers, OEMs, system integrators, and investors regarding market opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Engine Knock Sensors Market?

-> Engine Knock Sensors Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1.43 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032.

Which key companies operate in Global Engine Knock Sensors Market?

-> Key players include Hella, Bosch Mobility Solutions, Delphi, Hitachi, NGK Spark Plugs, SMPE, Francisco Albero S.A.U, Continental, Standard Motor Products, Inc., and Wells Vehicle Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing vehicle production, stringent emission regulations, and demand for fuel-efficient engines.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China’s automotive industry expansion, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include advancements in piezoelectric sensor technology, integration with engine control units, and development of compact sensor designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...