MARKET INSIGHTS

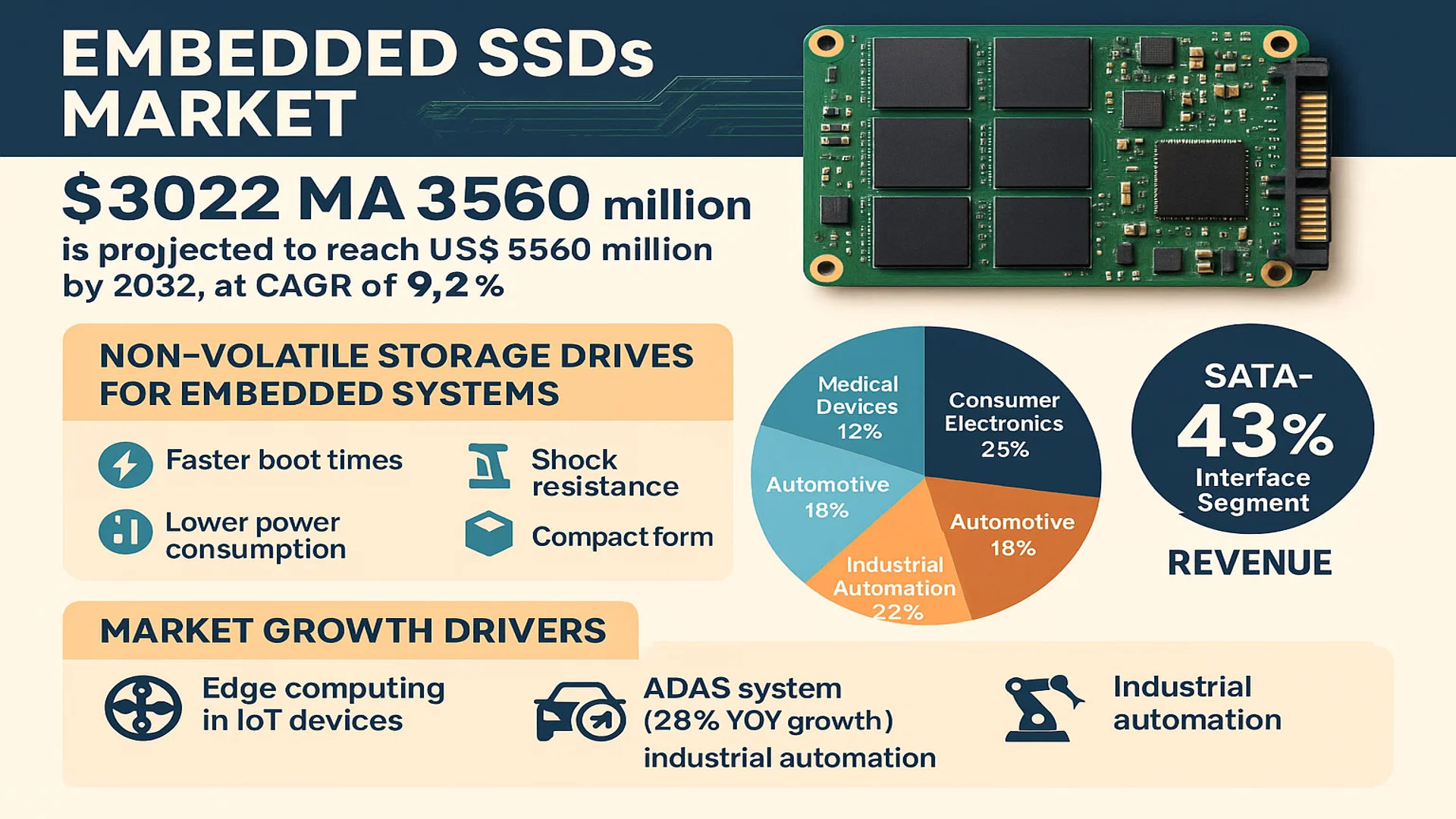

The global Embedded SSDs Market was valued at 3022 million in 2024 and is projected to reach US$ 5560 million by 2032, at a CAGR of 9.2% during the forecast period.

Embedded SSDs (Solid-State Drives) are non-volatile storage devices specifically designed for embedded systems applications across industries. These flash memory-based solutions replace traditional HDDs with superior performance characteristics including faster boot times, shock resistance, lower power consumption, and compact form factors. The technology finds applications in industrial automation (22% market share), automotive (18%), consumer electronics (25%), and medical devices (12%), with SATA-based SSDs currently dominating 43% of interface segment revenue.

Market growth is driven by increasing demand for edge computing in IoT devices, automotive ADAS systems requiring robust storage (projected 28% YOY growth in automotive sector), and industrial automation deployments. However, challenges include NAND flash price volatility and write cycle limitations in high-intensity applications. Recent developments include Samsung’s 2024 launch of high-endurance Z-NAND SSDs for industrial use and Western Digital’s strategic partnerships with automotive Tier 1 suppliers for next-gen infotainment systems.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Performance Storage in Automotive and Industrial Applications to Fuel Market Expansion

The automotive sector’s increasing adoption of advanced driver assistance systems (ADAS) and autonomous driving technologies is accelerating demand for reliable, high-speed embedded storage solutions. As vehicles become more data-intensive with features like real-time navigation and predictive maintenance, the need for rugged, low-latency storage grows exponentially. Embedded SSDs offer superior vibration resistance and thermal tolerance compared to traditional HDDs, making them ideal for harsh automotive environments where traditional storage would fail. The global connected car market is projected to exceed 95 million units by 2030, creating substantial opportunities for embedded SSD manufacturers to provide mission-critical data storage solutions.

Proliferation of IoT and Edge Computing Devices Driving Adoption

Edge computing deployments are growing at a compound annual growth rate exceeding 30% as organizations seek to process data closer to its source. This architectural shift requires robust, energy-efficient storage solutions capable of operating in remote environments. Embedded SSDs with ultra-low power consumption profiles meet these requirements perfectly while providing the necessary speed and reliability for processing large volumes of IoT-generated data. Smart city infrastructure projects alone are expected to deploy over 7 billion IoT sensors by 2025, each potentially requiring high-endurance embedded storage solutions for data logging and processing at the network edge.

➤ Industrial automation systems increasingly depend on embedded SSDs for real-time data acquisition, with modern manufacturing facilities generating over 1 terabyte of production data daily from IoT-enabled equipment.

Furthermore, the medical device industry’s digital transformation creates additional momentum for embedded SSD adoption. Modern diagnostic equipment such as MRI machines and ultrasound systems require high-capacity, high-reliability storage to handle increasingly complex imaging data sets while complying with strict medical device regulations regarding data integrity.

MARKET CHALLENGES

Endurance and Reliability Concerns in Mission-Critical Applications Pose Adoption Barriers

While embedded SSDs offer numerous advantages, their limited write endurance compared to industrial-grade HDDs remains a significant challenge for certain applications. High-temperature environments common in industrial automation and automotive applications can accelerate NAND flash degradation, potentially reducing drive lifespan by up to 50%. Manufacturers must implement advanced wear-leveling algorithms and over-provisioning techniques to extend product lifecycles, but these solutions increase development costs and complexity. Continuous data recording applications such as black box recorders in transportation or industrial process monitoring may require specialized enterprise-grade embedded SSDs with endurance ratings exceeding standard consumer offerings.

Other Challenges

Supply Chain Variability

The global semiconductor shortage continues impacting embedded SSD availability and pricing, particularly for specialized industrial-grade components. Lead times for certain controller chips remain extended by 30-50 weeks, forcing manufacturers to redesign products around available components or delay production schedules.

Certification Requirements

Medical and automotive applications demand compliance with stringent industry certifications like ISO 26262 for functional safety or IEC 60601 for medical devices. These certification processes add 9-18 months to product development cycles while increasing validation costs by 25-40%, creating barriers for smaller manufacturers without established certification expertise.

MARKET RESTRAINTS

Cost Sensitivity in Emerging Markets Limits Commercial Expansion

Despite performance advantages, embedded SSD adoption faces resistance in price-sensitive emerging markets where system cost optimization remains paramount. Industrial automation projects in developing economies frequently prioritize initial acquisition cost over total cost of ownership considerations, favoring conventional storage solutions with lower upfront prices. Automotive OEMs face similar price pressures as they expand into emerging vehicle markets where consumers demonstrate less willingness to pay for advanced technology features requiring premium storage solutions.

Additionally, the custom integration requirements for embedded solutions create additional cost barriers. Unlike standardized storage components, embedded SSDs often require customized firmware and mechanical interfaces tailored to specific OEM applications. These customization requirements can increase per-unit costs by 15-30% compared to off-the-shelf alternatives while extending development timelines, making embedded SSDs less attractive for low-margin, high-volume applications.

MARKET OPPORTUNITIES

AI and Machine Learning Workloads at the Edge Create New Demand for High-Performance Embedded Storage

The proliferation of artificial intelligence applications in edge devices presents significant growth opportunities for embedded SSD manufacturers. Modern AI inference workloads require high-throughput, low-latency storage to handle model parameters and real-time data streams efficiently. Next-generation embedded SSDs featuring advanced NVMe interfaces and ultra-low latency controllers can deliver the necessary performance for real-time AI processing in applications ranging from industrial quality inspection to autonomous mobile robots. Edge AI deployments in manufacturing alone are expected to grow at over 35% CAGR through 2030, creating substantial demand for specialized embedded storage solutions that can withstand industrial environments while delivering enterprise-grade performance.

Advancements in 3D NAND technology enable higher capacities in compact form factors, with leading manufacturers now offering embedded SSDs exceeding 2TB in M.2 2280 footprints. These developments open new possibilities for data-intensive applications in sectors like medical imaging and aerospace, where space constraints previously limited storage capacity. Furthermore, emerging non-volatile memory technologies like Z-NAND and XL-FLASH promise to address endurance challenges in write-intensive industrial applications while maintaining the cost benefits of flash storage.

EMBEDDED SSDS MARKET TRENDS

Expanding Automotive Applications Drive Market Growth

The automotive sector is emerging as a key growth driver for embedded SSDs, fueled by the increasing integration of advanced infotainment systems, autonomous driving technologies, and connected vehicle platforms. Modern vehicles now require robust, high-speed data storage solutions capable of handling complex algorithms and real-time processing. Embedded SSDs, particularly NVMe-based variants, are becoming essential for applications ranging from autonomous navigation systems to over-the-air (OTA) updates, due to their superior read/write speeds and shock-resistant properties. The shift toward electric vehicles (EVs) and smart mobility solutions is further accelerating demand, with market forecasts predicting automotive applications to account for over 25% of total embedded SSD revenue by 2032.

Other Trends

Adoption in Industrial IoT and Edge Computing

Industrial automation and IoT deployments are increasingly relying on embedded SSDs for edge computing applications, where low latency and high reliability are critical. These drives enable real-time data processing in manufacturing equipment, robotics, and smart infrastructure, reducing dependency on cloud-based systems. The industrial sector’s demand for ruggedized storage solutions—capable of withstanding extreme temperatures and vibrations—has led to specialized SSD designs with enhanced durability. As Industry 4.0 initiatives gain momentum globally, industrial applications are projected to grow at a CAGR of over 11% through 2032.

Consumer Electronics Push for Higher Capacities

The consumer electronics segment continues to dominate embedded SSD demand, driven by the proliferation of smart devices, wearables, and portable gaming systems. Manufacturers are prioritizing compact form factors with higher storage capacities—now reaching up to 2TB in some embedded solutions—to accommodate 4K/8K content and advanced applications. The transition from eMMC to UFS-based SSDs in smartphones has significantly improved performance, with sequential write speeds surpassing 1,200 MB/s in latest-generation devices. This shift is reshaping product development cycles, with major OEMs increasingly embedding storage directly into system-on-chip (SoC) designs to optimize space and power efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on High-Performance Solutions to Drive Market Expansion

The global embedded SSDs market is characterized by a mix of established storage giants and specialized manufacturers competing across different segments. Samsung Electronics leads the market with its vertically integrated NAND flash production and diverse portfolio spanning SATA, NVMe, and UFS solutions. The company’s technological edge in 3D NAND architecture gives it significant cost and performance advantages, particularly in automotive and industrial applications.

Western Digital (through its SanDisk brand) and KIOXIA (formerly Toshiba Memory) maintain strong positions, leveraging their flash memory fabrication capabilities and established distribution networks. These players are particularly competitive in the consumer electronics and data center segments, where price-to-performance ratios are critical.

While the top five companies accounted for approximately 58% of global revenue in 2024, the market also features dynamic competition from specialized players like ATP Electronics in industrial applications and Greenliant in aerospace-grade solutions. These niche players compete through reliability certifications, extended temperature ranges, and customized firmware for mission-critical environments.

Several trends are reshaping competitive dynamics: the transition from SATA to PCIe/NVMe interfaces is accelerating, creating opportunities for companies with controller expertise like Phison and Silicon Motion. Meanwhile, the emerging market for automotive-grade embedded storage is prompting partnerships between SSD manufacturers and automotive Tier 1 suppliers, with companies like Micron and Kingston making strategic moves in this space.

List of Key Embedded SSD Manufacturers Profiled

- Samsung Electronics (South Korea)

- Western Digital (U.S.)

- Kingston Technology (U.S.)

- KIOXIA Corporation (Japan)

- Transcend Information (Taiwan)

- Advantech (Taiwan)

- Phison Electronics (Taiwan)

- Silicon Motion (Taiwan)

- ATP Electronics (U.S.)

- Greenliant (U.S.)

- BIWIN Storage Technology (China)

- Kimtigo (China)

Segment Analysis:

By Type

NVMe-based Embedded SSDs Segment Leads Due to High-Performance Demands in Modern Applications

The market is segmented based on type into:

- SATA-based Embedded SSDs

- NVMe-based Embedded SSDs

- eMMC Embedded SSDs

- UFS Embedded SSDs

By Application

Automotive Segment Experiences Rapid Growth with Increasing Demand for Advanced In-Vehicle Systems

The market is segmented based on application into:

- Industrial Automation

- Medical

- Automotive

- Consumer Electronics

- Aerospace and Defense

By Capacity

128GB-512GB Range Dominates Due to Ideal Balance Between Performance and Cost-Efficiency

The market is segmented based on capacity into:

- Below 128GB

- 128GB-512GB

- Above 512GB

By Form Factor

BGA SSDs Gain Popularity for Space-Constrained Embedded Systems

The market is segmented based on form factor into:

- M.2

- BGA

- U.2

- Others

Regional Analysis: Embedded SSDs Market

The Asia-Pacific region dominates the global Embedded SSDs market, driven by rapid industrialization and technological advancements in countries like China, Japan, and South Korea. China, in particular, is a major hub for consumer electronics and automotive manufacturing, creating substantial demand for high-performance embedded storage solutions. The region benefits from strong semiconductor supply chains and cost-efficient production capabilities, with companies like Samsung and KIOXIA Corporation leading innovation. Growth in IoT, smart devices, and 5G infrastructure further accelerates adoption. However, market fragmentation and price competition remain challenges, particularly in emerging economies where cost-sensitive buyers prioritize affordability over cutting-edge technology.

North America

North America is a key market for Embedded SSDs, with the U.S. contributing significantly due to its advanced industrial automation, aerospace, and healthcare sectors. High-performance NVMe-based SSDs are gaining traction in data centers and enterprise applications. The region’s emphasis on technological R&D and early adoption of AI-driven embedded systems ensures steady demand. Companies such as Western Digital and Intel are at the forefront, focusing on innovations in endurance and power efficiency. While regulatory compliance adds complexity, the region’s mature supply chain and high purchasing power support premium SSD adoption.

Europe

Europe demonstrates strong growth in the Embedded SSDs market, propelled by automotive electrification and Industry 4.0 initiatives. Germany leads the charge with its robust automotive sector integrating SSDs for infotainment and autonomous driving systems. Strict EU data regulations emphasize secure, high-reliability storage solutions, boosting demand for embedded SSDs with enhanced encryption. Companies like Infineon and STMicroelectronics play a pivotal role in shaping regional advancements. However, slower adoption in Eastern Europe, due to budget constraints in industrial upgrades, tempers overall growth rates.

South America

South America presents a developing market for Embedded SSDs, where Brazil and Argentina show promising potential in automotive and medical applications. Economic instability and inconsistent infrastructure investment, however, hinder large-scale adoption. Local manufacturers prioritize cost-effective eMMC and SATA-based solutions, limiting the uptake of advanced NVMe SSDs. As regional industries modernize, demand is expected to rise gradually, though price sensitivity will remain a key constraint.

Middle East & Africa

The Middle East & Africa region is in the early stages of Embedded SSD adoption, with growth concentrated in GCC countries like the UAE and Saudi Arabia. Increasing smart city initiatives and digital transformation in oil & gas industries drive niche demand. Limited local manufacturing capabilities mean heavy reliance on imports, creating supply chain bottlenecks. While long-term potential exists, the market’s growth is contingent on sustained investment in technological infrastructure and industrial diversification.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Embedded SSDs market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Embedded SSDs market was valued at USD 3,022 million in 2024 and is projected to reach USD 5,560 million by 2032, growing at a CAGR of 9.2% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (SATA-based, NVMe-based, eMMC, UFS), application (Industrial Automation, Medical, Automotive, Consumer Electronics, Aerospace and Defense), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market is a key contributor in North America, while China leads growth in Asia-Pacific.

- Competitive Landscape: Profiles of leading market participants including Samsung, Western Digital, Kingston, Transcend, and KIOXIA Corporation, analyzing their product portfolios, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging storage technologies, NAND flash advancements, interface protocols (PCIe 5.0), and power efficiency improvements in embedded solutions.

- Market Drivers & Restraints: Evaluation of factors such as increasing IoT adoption, automotive electronics demand, and industrial automation growth, balanced against challenges like NAND flash pricing volatility and write-cycle limitations.

- Stakeholder Analysis: Strategic insights for OEMs, system integrators, component suppliers, and investors regarding emerging opportunities in edge computing, automotive ADAS, and medical imaging applications.

Primary and secondary research methodologies were employed, including analysis of industry reports, company financials, and interviews with key opinion leaders to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Embedded SSDs Market?

-> Embedded SSDs Market was valued at 3022 million in 2024 and is projected to reach US$ 5560 million by 2032, at a CAGR of 9.2% during the forecast period.

Which key companies operate in Global Embedded SSDs Market?

-> Key players include Samsung, Western Digital, Kingston, KIOXIA Corporation, Transcend, BIWIN Storage Technology, and Silicon Motion, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for edge computing, automotive electrification, industrial IoT adoption, and increasing data storage requirements in medical devices.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by electronics manufacturing in China, South Korea, and Taiwan, while North America leads in high-performance applications.

What are the emerging trends?

-> Emerging trends include QLC NAND adoption, PCIe 5.0 interface implementation, automotive-grade SSD solutions, and increasing capacities in small form factors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...