MARKET INSIGHTS

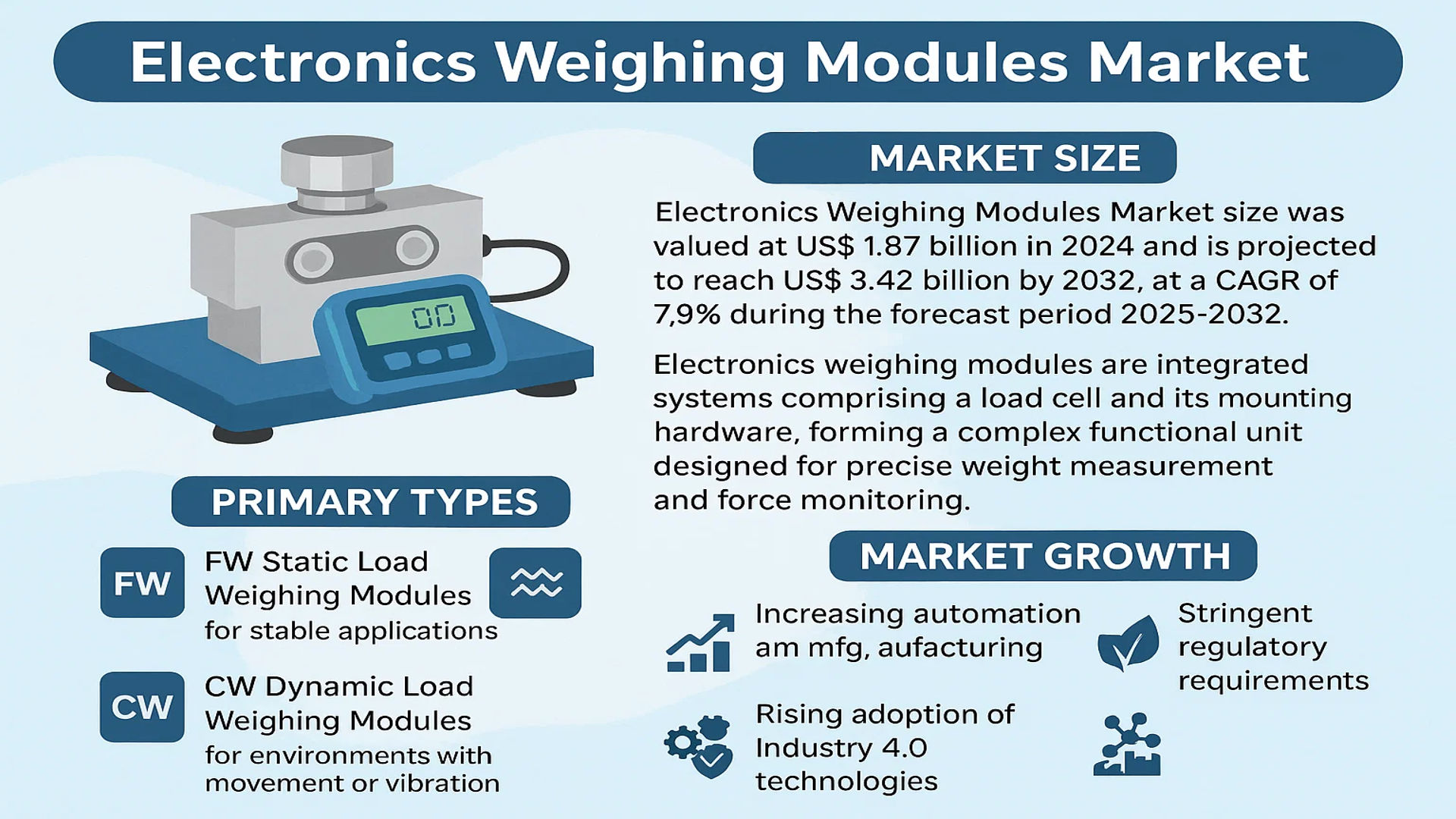

The global Electronics Weighing Modules Market size was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 3.42 billion by 2032, at a CAGR of 7.9% during the forecast period 2025-2032.

Electronics weighing modules are integrated systems comprising a load cell and its mounting hardware, forming a complex functional unit designed for precise weight measurement and force monitoring. These modules are engineered to provide high accuracy and reliability in demanding industrial environments, facilitating processes such as material metering, level indication, and feeding quantity control. The primary types include FW Static Load Weighing Modules for stable applications and CW Dynamic Load Weighing Modules for environments with movement or vibration.

The market growth is driven by increasing automation across manufacturing and logistics sectors, stringent regulatory requirements for accurate weighing, and the rising adoption of Industry 4.0 technologies. Furthermore, advancements in sensor technology and the integration of IoT for real-time data analytics are significant contributors. Key players like HBM, METTLER TOLEDO, and Siemens are continuously innovating, with recent developments focusing on enhanced connectivity and ruggedized designs for harsh conditions, thereby expanding their application scope and fueling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Automation in Manufacturing and Logistics to Drive Electronics Weighing Modules Demand

The global push towards automation across manufacturing, logistics, and process industries is a primary catalyst for the electronics weighing modules market. Industries are increasingly integrating automated weighing systems for tasks such as batching, filling, and quality control to enhance precision, reduce human error, and improve operational efficiency. The manufacturing sector’s adoption of Industry 4.0 principles, which emphasize interconnected and smart systems, relies heavily on accurate data acquisition—a core function provided by weighing modules. This trend is particularly strong in regions with high industrial output, where even a marginal improvement in weighing accuracy can translate to significant cost savings and product quality enhancements. The demand for seamless integration with PLCs and SCADA systems further solidifies the role of these modules in modern automated environments.

Stringent Regulatory Standards for Weighing Accuracy to Boost Market Growth

Globally, industries such as pharmaceuticals, food and beverage, and chemicals operate under strict regulatory frameworks that mandate precise weighing and measurement. Regulations often require documented proof of weighing accuracy for compliance, quality assurance, and safety. This necessitates the use of certified and highly reliable weighing systems. Electronics weighing modules, with their advanced load cell technology and digital signal processing, provide the necessary accuracy and data integrity. For instance, in pharmaceutical manufacturing, even minute deviations in ingredient weights can compromise product efficacy and safety, leading to regulatory non-compliance and potential recalls. This regulatory pressure compels companies to invest in high-performance weighing solutions, directly driving market growth.

Furthermore, international standards for trade and commerce require verified and calibrated weighing systems. The enforcement of these standards by metrological institutes worldwide ensures a continuous replacement and upgrade cycle for outdated mechanical scales, creating a steady demand for modern electronic modules.

➤ For instance, non-compliance with weighing regulations in the food sector can result in penalties exceeding significant financial thresholds and damage to brand reputation, making investment in accurate modules a strategic necessity.

The expansion of global trade also fuels this driver, as cross-border shipments require weight verification for pricing, tariffs, and logistics planning, further embedding the need for reliable electronic weighing systems in the supply chain.

MARKET RESTRAINTS

High Initial Investment and Integration Costs to Deter Market Penetration

While electronics weighing modules offer superior accuracy and integration capabilities, their adoption is tempered by significant upfront costs. A complete system involves not just the module itself but also associated components like indicators, junction boxes, and sophisticated software, alongside the engineering costs for system integration and calibration. For small and medium-sized enterprises (SMEs), this capital expenditure can be prohibitive, especially when replacing functional mechanical systems. The total cost of ownership extends beyond purchase to include regular calibration, maintenance, and potential downtime during installation. This financial barrier slows down market penetration in price-sensitive segments and emerging economies, where budget constraints are a major consideration in capital equipment decisions.

Technical Complexity and Vulnerability to Environmental Factors to Hinder Adoption

Electronics weighing modules are sophisticated instruments that are sensitive to their operating environment. Factors such as temperature fluctuations, humidity, dust, vibration, and electrical noise can significantly impact their accuracy and performance. Installing these systems in harsh industrial environments—like foundries, chemical plants, or outdoor logistics yards—requires additional protective measures and robust housing, which adds to the cost and complexity. Furthermore, achieving optimal performance often requires expert installation and precise calibration to compensate for these environmental variables. The technical expertise needed for troubleshooting and maintenance is not always readily available, leading to longer resolution times for issues and potential operational disruptions. This complexity can deter facilities without dedicated technical staff from adopting these advanced systems.

Additionally, the risk of cyber vulnerabilities in networked weighing systems is an emerging concern. As modules become integrated into broader IoT and Industry 4.0 architectures, they represent potential entry points for security breaches, requiring investments in cybersecurity measures that further increase the total cost of ownership.

MARKET CHALLENGES

Intense Market Competition and Price Pressure to Challenge Manufacturer Margins

The global electronics weighing modules market is characterized by the presence of several established players and numerous regional competitors, leading to intense price competition. While high-end, precision modules from leading brands command premium prices, there is growing pressure from lower-cost alternatives that compete primarily on price. This forces manufacturers to continuously innovate to justify their value proposition while also optimizing production costs to maintain profitability. The challenge is exacerbated by the fact that weighing modules are often perceived as a commodity component within a larger system, leading to procurement decisions focused heavily on initial cost rather than long-term value or total cost of ownership. Navigating this competitive landscape requires significant investment in R&D for product differentiation and efficient global supply chain management.

Other Challenges

Rapid Technological Obsolescence

The pace of technological advancement in electronics and sensor technology is relentless. New communication protocols, improved materials for load cells, and enhanced software features are constantly being developed. This creates a challenge for both manufacturers and end-users. Manufacturers must invest heavily in R&D to keep their products current, while end-users face the dilemma of investing in technology that may become obsolete quickly, potentially complicating future expansion or integration plans.

Supply Chain Vulnerabilities

The reliance on specialized electronic components and raw materials makes the market susceptible to global supply chain disruptions. Events such as trade disputes, geopolitical tensions, or pandemics can lead to shortages of critical components like semiconductors, causing production delays and increased costs. This volatility challenges manufacturers’ ability to meet demand consistently and maintain stable pricing.

MARKET OPPORTUNITIES

Expansion of IoT and Predictive Maintenance to Unlock New Growth Avenues

The integration of Internet of Things (IoT) capabilities into industrial weighing systems presents a substantial growth opportunity. Smart weighing modules equipped with sensors and connectivity can transmit real-time data on weight, equipment health, and usage patterns to centralized monitoring systems. This enables predictive maintenance, where potential failures can be identified and addressed before they cause unplanned downtime. For industries where continuous operation is critical, such as chemical processing or bulk material handling, the value proposition of minimizing downtime far exceeds the additional cost of smart modules. The data collected can also be used for advanced analytics to optimize processes, improve inventory management, and enhance overall operational efficiency, creating a new revenue stream for module manufacturers offering integrated data solutions.

Growth in Emerging Economies and New Application Sectors to Offer Lucrative Potential

Emerging economies are witnessing rapid industrialization and infrastructure development, which directly fuels demand for industrial automation and weighing equipment. As these regions modernize their manufacturing and logistics sectors, the replacement of outdated mechanical scales with electronic modules represents a significant market opportunity. Furthermore, new application areas are continually emerging. The renewable energy sector, for example, requires precise weighing in the production of components like solar panels and batteries. The aerospace industry uses high-precision modules for testing and assembly. The expansion into these non-traditional sectors diversifies the market base and reduces dependency on cyclical industries, providing a stable path for long-term growth.

Additionally, the increasing focus on waste management and recycling creates new demand for weighing systems in sorting and processing facilities, further expanding the addressable market for electronics weighing modules beyond traditional industrial boundaries.

ELECTRONICS WEIGHING MODULES MARKET TRENDS

Integration of IoT and Industry 4.0 to Emerge as a Dominant Trend

The proliferation of Industry 4.0 and smart manufacturing initiatives is fundamentally reshaping the electronics weighing modules landscape. These advanced modules are increasingly being embedded with IoT sensors and connectivity features, enabling real-time data acquisition, remote monitoring, and predictive maintenance. This integration allows for seamless communication between weighing systems and central control units, facilitating automated data logging and process optimization. The demand for such intelligent systems is particularly high in sectors like pharmaceuticals and food & beverage, where stringent regulatory compliance and traceability are paramount. Furthermore, the ability to integrate weighing data directly into Enterprise Resource Planning (ERP) and Manufacturing Execution Systems (MES) is eliminating manual data entry errors and enhancing overall operational efficiency. This trend is a key driver behind the projected market growth, supporting the transition from standalone weighing instruments to interconnected, data-driven components of a larger automated ecosystem.

Other Trends

Demand for High-Precision in Laboratory and Research Applications

There is a growing and unwavering demand for ultra-high precision weighing modules in laboratory, research, and quality control environments. Applications in pharmaceutical R&D, chemical analysis, and biotechnology require measurements with accuracies reaching microgram and even nanogram levels. This necessitates modules with exceptional metrological performance, often certified to standards like OIML R60 and NTEP. Manufacturers are responding by developing modules with advanced features such as automatic temperature compensation, robust immunity to environmental disturbances like vibrations and air currents, and enhanced signal processing algorithms. The shift towards miniaturization in electronics manufacturing also fuels the need for precise weighing of tiny components, a trend that is expected to continue as technology advances.

Expansion in Food Processing and Packaging Industries

The global food processing and packaging industry represents a massive and steadily growing end-user segment for electronics weighing modules. These modules are critical for applications including checkweighing, portion control, filling, and batching. The drive towards automation in food production to improve hygiene, increase throughput, and reduce labor costs is a significant market catalyst. Modern weighing modules designed for these environments are built with durable, easy-to-clean materials, often boasting IP69K ratings for protection against high-pressure washdowns. Additionally, the rise of e-commerce has increased the demand for automated fulfillment centers, where dynamic weighing modules are essential for sorting and shipping processes. This expansion is directly linked to broader macroeconomic trends in consumer behavior and supply chain logistics.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Leadership

The global electronics weighing modules market exhibits a semi-consolidated competitive structure, characterized by the presence of established multinational corporations, specialized medium-sized enterprises, and niche regional players. METTLER TOLEDO stands as a dominant force, commanding a significant market share estimated at approximately 18-22% in 2024. This leadership is anchored in its comprehensive portfolio of high-precision weighing solutions, robust global distribution network spanning over 40 countries, and sustained investment in R&D, which exceeded $150 million in the last fiscal year.

HBM (Hottinger Brüel & Kjær) and BLH Nobel (VPG) are also pivotal contenders, collectively holding a substantial portion of the market. HBM’s strength lies in its advanced sensor technology and strong foothold in the European industrial sector, while BLH Nobel leverages its expertise in custom-engineered solutions for harsh environments, particularly in the process weighing industry. Their growth is further propelled by strategic initiatives; for instance, HBM’s recent launch of the PW15 single-point weighing module series targeted the expanding logistics and packaging automation sector.

Furthermore, companies are aggressively pursuing growth through geographic expansion and mergers & acquisitions. Hardy (Amphenol Corporation) and Rice Lake Weighing Systems have strengthened their positions in North America through channel partner programs and the introduction of IoT-enabled weighing systems. Hardy’s Process Weighting Solutions segment reported a revenue increase of 12% year-over-year, underscoring the success of these strategies.

Meanwhile, technology giants like Siemens and ABB are integrating weighing modules into broader industrial automation and process control ecosystems. Their market presence is bolstered by offering fully integrated solutions, from the load cell to the control software, which appeals to clients seeking streamlined operational technology. This approach, coupled with significant R&D budgets focused on digitalization, ensures their continued influence and growth within the competitive landscape.

List of Key Electronics Weighing Modules Companies Profiled

- METTLER TOLEDO (Switzerland / Global)

- HBM (Germany)

- BLH Nobel (VPG) (U.S.)

- Wipotec (Germany)

- Hardy (Amphenol Corporation) (U.S.)

- Rice Lake Weighing Systems (U.S.)

- Eilersen (Denmark)

- Siemens (Germany)

- ABB (Switzerland)

- Carlton Scale (U.K.)

- SCAIME (France)

- A&D Engineering (U.S.)

Segment Analysis:

By Type

CW Dynamic Load Weighing Module Segment Leads Due to High Demand in Conveyor and Filling Applications

The market is segmented based on type into:

- FW Static Load Weighing Module

- Subtypes: Single-ended beam, Double-ended beam, and others

- CW Dynamic Load Weighing Module

- Subtypes: Conveyor belt scales, Filling systems, and others

By Application

Material Metering Segment Dominates Owing to Critical Role in Industrial Process Control

The market is segmented based on application into:

- Material Metering

- Level Indication and Control

- Feeding Quantity Control

- Others

By End-User Industry

Food and Beverage Industry Represents Largest End-User Segment Due to Strict Quality Control Requirements

The market is segmented based on end-user industry into:

- Food and Beverage

- Chemical and Pharmaceutical

- Logistics and Warehousing

- Manufacturing

- Others

Regional Analysis: Electronics Weighing Modules Market

Asia-Pacific

The Asia-Pacific region dominates the global electronics weighing modules market, accounting for over 45% of total market share by volume in 2024. This leadership position is driven by massive manufacturing expansion, particularly in China, Japan, and South Korea, where industries such as automotive, electronics, and food processing require precise weighing solutions for quality control and automation. China’s “Made in China 2025” initiative continues to fuel industrial modernization, creating sustained demand for high-accuracy weighing modules in automated production lines. However, the market is highly competitive and price-sensitive, leading to a significant presence of local manufacturers offering cost-effective alternatives to international brands. While adoption of advanced dynamic load weighing modules is growing in pharmaceutical and chemical sectors, static load modules remain prevalent in bulk material handling applications due to their lower cost and simplicity.

North America

North America represents a mature but steadily growing market characterized by stringent regulatory requirements and high adoption of advanced weighing technologies. The region’s market is driven by strict compliance standards in pharmaceutical manufacturing (following FDA guidelines) and food processing industries, where traceability and accuracy are paramount. The United States, in particular, shows strong demand for both static and dynamic weighing modules integrated with Industry 4.0 solutions. Recent infrastructure investments under the Infrastructure Investment and Jobs Act have also stimulated demand in construction and logistics sectors. The market is characterized by preference for high-precision, connected weighing solutions from established players like METTLER TOLEDO and Hardy, though price competition is increasing with the entry of Asian manufacturers.

Europe

Europe maintains a sophisticated market for electronics weighing modules with emphasis on precision engineering, certification compliance, and sustainability. Stringent EU regulations regarding weighing instruments (MID 2014/32/EU) and quality standards in pharmaceutical and chemical industries drive demand for certified, high-accuracy modules. Germany remains the technological leader, with strong presence of specialized manufacturers like HBM and Siemens serving advanced manufacturing sectors. The market shows growing integration of weighing modules with IoT platforms and cloud connectivity for data analytics and predictive maintenance. While Western European markets are mature with replacement demand dominating, Eastern European countries show growth potential as manufacturing facilities expand into these regions with lower operating costs.

South America

The South American market for electronics weighing modules is emerging but faces challenges due to economic volatility and infrastructure limitations. Brazil represents the largest market in the region, driven primarily by mining, agriculture, and food processing industries. However, market growth is constrained by currency fluctuations, import dependencies, and limited domestic manufacturing capabilities. Most high-end weighing modules are imported from North America and Europe, while basic static load modules are increasingly sourced from Asian manufacturers. The market shows potential in mining and agricultural sectors where weighing systems are essential for inventory management and process control, but adoption of advanced dynamic weighing solutions remains limited to multinational corporations and large domestic players.

Middle East & Africa

This region represents the smallest but growing market for electronics weighing modules, driven primarily by infrastructure development and industrial diversification efforts. The UAE and Saudi Arabia lead demand due to their focus on developing manufacturing capabilities and logistics hubs. The oil and gas industry remains a significant consumer of weighing modules for custody transfer and inventory management applications. However, market growth is hampered by reliance on imports, limited technical expertise, and preference for basic weighing solutions over advanced integrated systems. South Africa maintains the most developed market in sub-Saharan Africa, particularly in mining and manufacturing applications. While the market shows long-term growth potential, current adoption rates remain modest compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the global Electronics Weighing Modules market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronics Weighing Modules Market?

->Electronics Weighing Modules Market size was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 3.42 billion by 2032, at a CAGR of 7.9% during the forecast period 2025-2032.

Which key companies operate in Global Electronics Weighing Modules Market?

-> Key players include HBM, BLH Nobel (VPG), METTLER TOLEDO, Wipotec, Hardy, Rice Lake Weighing Systems, Eilersen, Siemens, ABB, Carlton Scale, SCAIME, and A&D Engineering, among others.

What are the key growth drivers?

-> Key growth drivers include increased automation in manufacturing, stringent quality control requirements across industries, and the integration of Industry 4.0 and IoT technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by manufacturing expansion in China and India, while North America and Europe remain significant markets due to advanced industrial automation.

What are the emerging trends?

-> Emerging trends include development of wireless and smart weighing modules, integration with cloud-based data analytics platforms, and increased adoption in pharmaceutical and food processing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...