MARKET INSIGHTS

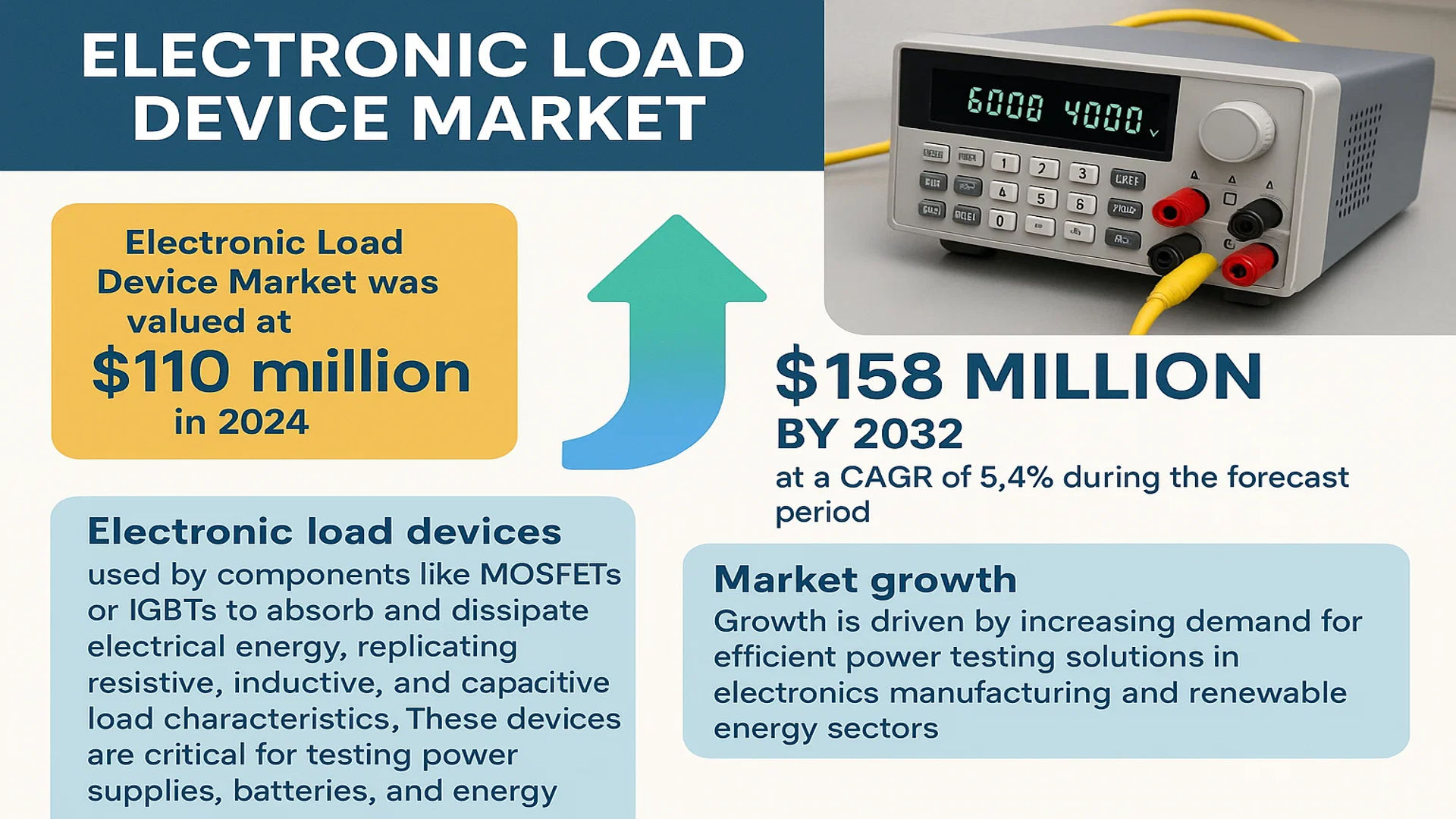

The global Electronic Load Device Market was valued at 110 million in 2024 and is projected to reach US$ 158 million by 2032, at a CAGR of 5.4% during the forecast period.

Electronic load devices are power supply testing instruments that simulate real-world load conditions. They utilize electronic components like MOSFETs or IGBTs to absorb and dissipate electrical energy, replicating resistive, inductive, and capacitive load characteristics. These devices are critical for testing power supplies, batteries, and energy systems across multiple industries.

Market growth is driven by increasing demand for efficient power testing solutions in electronics manufacturing and renewable energy sectors. The DC segment dominates current applications, while AC capabilities are gaining traction. Regional leaders include the U.S. and China, with major manufacturers like Keysight Technologies, National Instruments, and ITECH holding significant market share. Recent technological advancements in high-power testing and energy regeneration features are further propelling adoption across automotive and telecommunications industries.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Electronics Manufacturing Industry Accelerates Demand

The global electronics manufacturing sector continues to experience robust growth, with production volumes increasing significantly across regions. This expansion is driving substantial demand for electronic load devices, which are critical for testing power supplies, batteries, and other electronic components during manufacturing. Asia-Pacific dominates this growth, accounting for over 60% of global electronics production, creating concentrated demand for testing equipment. The proliferation of consumer electronics, coupled with Industry 4.0 initiatives, has intensified quality control requirements, making electronic load devices indispensable for production line validation and reliability testing.

Renewable Energy Sector Growth Fuels Market Expansion

The renewable energy revolution is creating significant opportunities for electronic load device manufacturers. As solar panel production increases by approximately 8% annually and battery storage installations grow at 30% CAGR, the need for precise testing solutions has become paramount. Electronic load devices play a crucial role in evaluating the performance and efficiency of photovoltaic systems and energy storage components. The transition toward green energy solutions worldwide has prompted governments and private entities to invest heavily in testing infrastructure, directly benefiting the electronic load device market.

➤ For instance, recent policy initiatives in the European Union mandate rigorous testing protocols for all grid-connected renewable energy systems, creating a consistent demand for advanced electronic load testing solutions.

Advancements in Electric Vehicle Infrastructure Drive Adoption

The electric vehicle market’s exponential growth is generating substantial secondary demand for electronic load devices. With global EV sales projected to reach 40 million units annually by 2030, manufacturers require sophisticated testing solutions for power electronics, charging systems, and battery management systems. Modern electronic load devices with programmable capabilities and high power ratings have become essential for developing and validating EV components. The automotive industry’s stringent quality standards and safety requirements further amplify the need for precise, reliable load testing equipment throughout the supply chain.

MARKET RESTRAINTS

High Equipment Costs Limit Market Penetration

While demand for electronic load devices grows, the market faces significant price sensitivity challenges. Advanced electronic load systems with high power ratings and precision measurement capabilities can cost between $5,000-$50,000 per unit, making them prohibitively expensive for small manufacturers and research institutions. Many potential customers, particularly in developing markets, opt for lower-cost alternatives or second-hand equipment despite compromised accuracy and functionality. This pricing barrier significantly limits market expansion in price-sensitive segments, where customers prioritize initial cost over long-term testing capabilities.

Other Restraints

Technical Complexity

Modern electronic load devices require specialized knowledge for optimal operation and maintenance. The increasing sophistication of programmable loads with advanced features creates a steep learning curve for technicians and engineers, discouraging adoption among organizations with limited technical expertise.

Supply Chain Constraints

The global semiconductor shortage continues to impact electronic load device manufacturing, leading to extended lead times and production bottlenecks. Critical components like high-power MOSFETs and precision ADCs remain in short supply, constraining manufacturers’ ability to meet growing demand.

MARKET CHALLENGES

Rapid Technological Obsolescence Pressures Manufacturers

The electronic load device market faces significant challenges from the pace of technological change. Power electronics evolve constantly, requiring testing equipment to keep pace with new voltage ranges, switching frequencies, and communication protocols. Manufacturers must continuously invest in R&D to develop devices capable of testing next-generation power semiconductors, creating substantial financial pressure. Many companies struggle to recoup development costs before their products become technologically obsolete, particularly in segments testing advanced wide-bandgap semiconductors.

Standardization and Compliance Hurdles Impede Growth

The lack of global standards for power electronics testing creates significant challenges for electronic load device manufacturers. Varying regional certification requirements and industry specifications force companies to develop multiple product variants, increasing production complexity and costs. Compliance with evolving safety standards, such as IEC 61010 for electrical equipment, requires continuous product redesigns and recertification. These regulatory complexities particularly affect smaller manufacturers who lack the resources to navigate diverse international compliance landscapes efficiently.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Creates New Application Potential

The global rollout of 5G networks presents significant growth opportunities for the electronic load device market. Telecom infrastructure requires extensive power system testing, particularly for base station power supplies and backup systems. 5G’s higher power requirements and stringent reliability standards necessitate advanced testing solutions that can simulate complex load profiles and transient conditions. With over 1 million 5G base stations expected to be deployed worldwide in the next three years, the resulting demand for specialized testing equipment could drive a new wave of market expansion.

Cloud-Based Testing Solutions Open New Revenue Streams

The integration of cloud computing with electronic load devices creates transformative opportunities for market players. Network-connected smart load devices enable remote testing, data logging, and predictive maintenance capabilities that appeal to geographically distributed engineering teams. Many manufacturers are developing subscription-based testing services that complement hardware sales, creating recurring revenue models. This shift toward connected test solutions aligns with broader Industry 4.0 trends and could fundamentally transform traditional electronic load device business models.

Semiconductor Industry Expansion Drives Specialized Testing Needs

The booming semiconductor industry, particularly for power devices, requires increasingly sophisticated test solutions. Wide-bandgap semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) demand testing at higher voltages and switching frequencies than traditional silicon devices. This creates opportunities for electronic load device manufacturers to develop specialized solutions tailored for next-generation semiconductor validation. With the power semiconductor market growing at over 10% annually, manufacturers who can address these specialized testing requirements stand to capture significant market share.

ELECTRONIC LOAD DEVICE MARKET TRENDS

Rising Demand for DC Electronic Load Devices in Renewable Energy Applications

The increasing adoption of renewable energy solutions is significantly influencing the electronic load device market, particularly for DC-based applications. With the global renewable energy capacity expected to grow by over 60% by 2030, the need for efficient power testing solutions for solar panels, wind turbines, and battery storage systems has surged. Electronic loads play a critical role in validating the performance of DC power systems by simulating real-world conditions, ensuring stability and reliability in energy output. Furthermore, manufacturers are integrating advanced features such as dynamic load testing and programmable current profiles to meet the evolving requirements of clean energy infrastructure.

Other Trends

Growth in 5G and Telecom Infrastructure Development

The rapid deployment of 5G networks and modern telecom infrastructure has heightened the demand for precise power testing solutions. Communication equipment, including base stations and small cells, requires rigorous validation of power supplies, driving the adoption of AC/DC electronic load devices. The global 5G infrastructure market is projected to exceed $180 billion by 2027, further accelerating investments in testing tools. Advanced electronic loads now incorporate real-time data logging and high-frequency switching capabilities to ensure seamless power delivery in next-generation networks.

Automotive Electrification Drives Market Expansion

The shift toward electric vehicles (EVs) and hybrid vehicles is a major catalyst for the electronic load device market. Automakers and battery manufacturers rely on these systems for testing high-voltage battery packs, onboard chargers, and power electronics. As EV production is expected to grow at a CAGR of 25% through 2030, the need for high-power electronic loads with regenerative capabilities is increasing. Manufacturers are now prioritizing modular and scalable solutions to accommodate varying voltage levels and provide precise thermal management features, ensuring long-term reliability in automotive applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Competition

The global electronic load device market is moderately fragmented, characterized by the presence of established multinational corporations and emerging regional players. Keysight Technologies and National Instruments dominate the market, leveraging their extensive product portfolios and strong foothold in North America and Europe. These companies have consistently invested in R&D to develop high-precision load testing solutions, making them preferred choices for industrial and commercial applications.

Meanwhile, Kikusui and GW Instek have strengthened their positions through strategic collaborations and expansion in Asia-Pacific markets, particularly in China and Japan, where demand for energy-efficient testing equipment is rising. Their emphasis on modular and programmable electronic loads has allowed them to cater to diverse applications, from electric vehicle testing to renewable energy systems.

Smaller but agile players such as Shenzhen Maynuo Electronic and Nanjing Maynuo Electronics are gaining traction by offering cost-competitive solutions tailored to regional needs. However, challenges like supply chain disruptions and raw material price volatility have forced many mid-tier manufacturers to reassess their operational strategies.

The market’s competitive intensity is further heightened by mergers and acquisitions, with companies like TDK-Lambda expanding their technological capabilities through strategic buyouts. In 2024, vertical integration became a key trend as manufacturers sought to secure component supplies and reduce dependency on third-party vendors.

List of Key Electronic Load Device Companies Profiled

- Keysight Technologies (U.S.)

- National Instruments (U.S.)

- Kikusui Electronics Corporation (Japan)

- GW Instek (Taiwan)

- TDK-Lambda (Japan)

- ITECH Electronics (China)

- Shenzhen Maynuo Electronic (China)

- Nanjing Maynuo Electronics (China)

- Goodwill Instruments (Taiwan)

- Changzhou Dingchen Electronics (China)

Segment Analysis:

By Type

DC Segment Dominates the Market Due to High Adoption in Power Electronics Testing

The market is segmented based on type into:

- DC

- Subtypes: Modular, Benchtop, and others

- AC

- Subtypes: Regenerative, Non-regenerative, and others

By Application

Electronic Manufacturing Industry Segment Leads Due to Growing Need for Quality Testing

The market is segmented based on application into:

- Electronic Manufacturing Industry

- New Energy Field

- Communication Industry

- Others

By Power Rating

Medium Power Range (100W-10kW) Segment Dominates Due to Versatile Applications

The market is segmented based on power rating into:

- Low Power (Below 100W)

- Medium Power (100W-10kW)

- High Power (Above 10kW)

By End-User

Industrial Segment Leads Due to Increasing Automation and Manufacturing Requirements

The market is segmented based on end-user into:

- Industrial

- Commercial

- Government & Defense

- Research & Academia

Regional Analysis: Electronic Load Device Market

Asia-Pacific

The Asia-Pacific region dominates the global electronic load device market, driven by rapid industrialization, expansion of the electronics manufacturing sector, and substantial investments in renewable energy projects. China and Japan lead the market due to their strong semiconductor and automotive industries, which extensively utilize electronic load testing for quality assurance. The region benefits from cost-competitive manufacturing capabilities, enabling high-volume production of DC and AC electronic load devices. Additionally, government initiatives promoting local R&D, such as China’s “Made in China 2025” plan, accelerate technological advancements. However, market fragmentation and price competition among regional players remain challenges.

North America

North America represents a technologically mature market for electronic load devices, with the U.S. contributing the majority of demand. The region’s focus on cutting-edge applications—such as electric vehicle (EV) battery testing, 5G infrastructure validation, and aerospace power systems—drives the need for high-precision devices. Established manufacturers like Keysight Technologies and National Instruments lead innovation, particularly in modular and programmable load solutions. Strict regulatory compliance, especially for energy efficiency and safety standards, further propels the adoption of advanced testing equipment. However, high product costs and reliance on imports for certain components may restrain market expansion.

Europe

Europe’s market growth is bolstered by its emphasis on renewable energy integration and automotive electrification. Countries like Germany and France prioritize testing solutions for wind/solar inverters and EV charging systems, supported by EU-wide sustainability directives. The presence of leading automotive OEMs and stringent product certification requirements fosters demand for reliable electronic load devices. While innovation thrives—particularly in energy-recycling load technologies—the market faces slower growth compared to Asia-Pacific due to higher operational costs and saturation in some industrial segments.

Middle East & Africa

The MEA region exhibits nascent but promising growth, driven by diversification into renewable energy and telecommunications infrastructure. Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the UAE, invest heavily in solar energy projects, creating demand for load testing equipment. Limited local manufacturing capabilities result in reliance on imports, though partnerships with global suppliers are gradually strengthening the supply chain. Economic volatility and underdeveloped industrial bases in parts of Africa hinder widespread adoption, but long-term potential exists with increasing foreign investments.

South America

South America’s market is emerging, with Brazil and Argentina being primary adopters due to their growing electronics and automotive sectors. Economic instability and currency fluctuations remain barriers, but localized production initiatives and rising renewable energy projects offer opportunities. The lack of standardized testing protocols and lower technological penetration compared to other regions results in slower market maturation, though gradual industrialization is expected to fuel demand over the forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Global Electronic Load Device market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Electronic Load Device market was valued at USD 110 million in 2024 and is projected to reach USD 158 million by 2032, growing at a CAGR of 5.4%.

- Segmentation Analysis: Detailed breakdown by product type (DC, AC), application (Electronic Manufacturing Industry, New Energy Field, Communication Industry, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants, including National Instruments, Kikusui, Keysight Technologies, GW Instek, TDK-Lambda, and others, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in power semiconductor devices (MOSFET, IGBT) and their integration in electronic load devices.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronic Load Device Market?

-> Electronic Load Device Market was valued at 110 million in 2024 and is projected to reach US$ 158 million by 2032, at a CAGR of 5.4% during the forecast period.

Which key companies operate in Global Electronic Load Device Market?

-> Key players include National Instruments, Kikusui, Keysight Technologies, GW Instek, TDK-Lambda, ITECH, Shenzhen Maynuo Electronic, and Nanjing Maynuo Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for power supply testing, growth in renewable energy sectors, and advancements in semiconductor technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to rapid industrialization, while North America remains a significant market due to technological advancements.

What are the emerging trends?

-> Emerging trends include adoption of modular electronic loads, integration of IoT in testing devices, and development of high-power density solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...