Market Insights

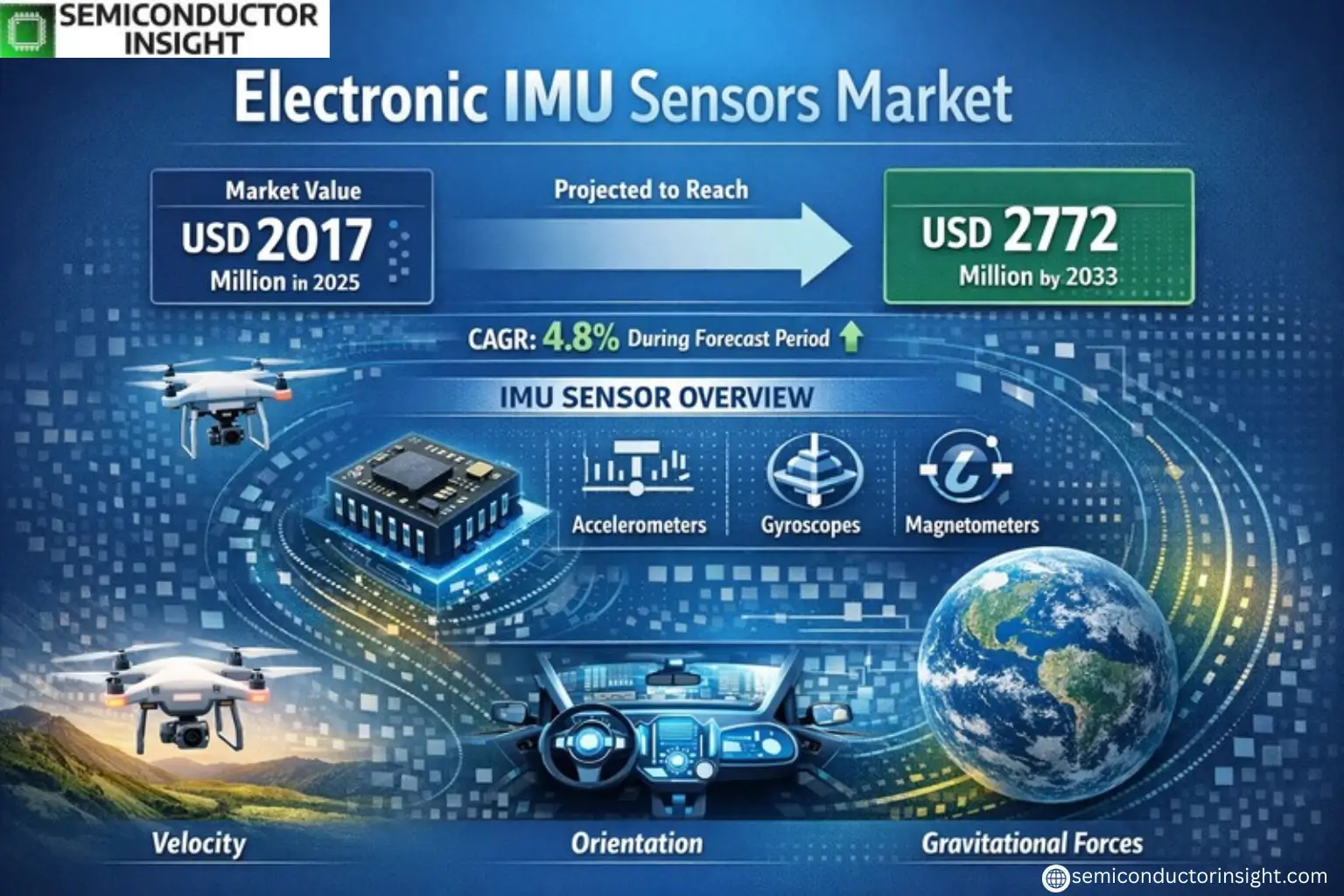

Global Electronic IMU Sensors Market was valued at USD 2017 million in 2025 and is projected to reach USD 2772 million by 2033, exhibiting a CAGR of 4.8% during the forecast period.

An inertial measurement unit (IMU) sensor is an electronic device that measures and reports a craft’s velocity, orientation, and gravitational forces using a combination of accelerometers and gyroscopes, sometimes also magnetometers. These sensors are critical for high-performance applications in aerospace, defense, industrial automation, and naval systems. The market excludes consumer-grade or automotive IMUs, focusing instead on precision-driven sectors where accuracy and reliability are paramount.

The market growth is driven by increasing demand for navigation systems in unmanned aerial vehicles (UAVs), advancements in MEMS technology, and rising defense expenditures globally. North America dominates the market with a 40% share due to strong aerospace and defense sectors, while Europe and China collectively account for approximately 50%. Key players like Honeywell International, Northrop Grumman, and SAFRAN hold about 75% of the market share through innovative product development and strategic partnerships.

MARKET DRIVERS

Growing Demand for Navigation and Stabilization Systems

Electronic IMU Sensors Market is experiencing significant growth due to rising demand in aerospace, defense, and automotive industries. These sensors are critical for navigation, motion tracking, and stabilization in autonomous vehicles, drones, and industrial robotics. Global push towards automation continues to fuel adoption, with an estimated 18% annual growth in industrial applications alone.

Advancements in MEMS Technology

Micro-Electro-Mechanical Systems (MEMS) innovations have enabled smaller, more cost-effective electronic IMU sensors with improved accuracy. This has expanded their use in consumer electronics, including smartphones and wearable devices. The consumer segment now accounts for nearly 27% of total IMU sensor shipments worldwide.

Military modernization programs across major economies continue to drive high-performance IMU sensor development, particularly for missile guidance and unmanned systems.

MARKET CHALLENGES

High Development Costs and Technical Complexities

Manufacturing precision electronic IMU sensors requires specialized facilities and expertise, creating significant barriers to entry. The average R&D cycle for new IMU sensor models exceeds 24 months, with development costs reaching upwards of USD 5 million for aerospace-grade units.

Other Challenges

Calibration and Error Compensation

Maintaining accuracy over time remains a technical hurdle, especially in harsh environments where thermal and mechanical stresses impact sensor performance. Vibration and shock resistance continues to be an area requiring ongoing innovation.

MARKET RESTRAINTS

Export Restrictions in Defense Applications

Stringent international regulations on dual-use technologies limit the global trade of advanced electronic IMU sensors, particularly those with military-grade specifications. This creates fragmented regional markets and complicates supply chains for manufacturers.

MARKET OPPORTUNITIES

Emerging Industrial IoT Applications

The Industrial Internet of Things creates new demand for electronic IMU sensors in predictive maintenance and equipment monitoring systems. This sector is projected to account for 31% of non-military IMU sensor revenue by 2026, growing at a 22% CAGR from current levels.

Electronic IMU Sensors Market Trends

Growing Demand in Aerospace and Defense Applications

Electronic IMU Sensors Market is experiencing steady growth, projected to reach USD 2.77 billion by 2033 at a 4.8% CAGR. Aerospace applications dominate demand, accounting for over 40% of market share, followed by defense systems. This growth stems from increasing adoption in unmanned aerial vehicles, missile guidance systems, and advanced navigation platforms requiring high-precision motion tracking.

Other Trends

Technological Advancements in MEMS-based IMUs

Si/Quartz MEMS and emerging HRG technologies are gaining traction, offering improved accuracy and reliability while reducing size and power consumption. These innovations are particularly valuable for space-constrained applications in both commercial and military sectors.

Regional Market Concentration

North America leads the Electronic IMU Sensors Market with 40% share, driven by substantial defense spending and aerospace innovation. Europe and China collectively hold 50% market share, with China showing the fastest growth rate due to expanding domestic aerospace capabilities and military modernization programs.

Other Trends

Industry Consolidation

The market remains concentrated, with top five players (Honeywell, Northrop Grumman, SAFRAN, Thales, Kearfott) controlling 75% of global sales. Recent years have seen strategic acquisitions as companies seek to expand their technological capabilities and market reach in high-performance IMU segments.

Increasing Industrial Applications

Non-defense industrial applications, particularly in offshore and naval sectors, are emerging as significant growth areas. These applications demand ruggedized IMU sensors for precision positioning and stabilization in harsh environments, creating new opportunities for market expansion beyond traditional aerospace/defense sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Positioning in the High-Performance IMU Sensors Sector

Global Electronic IMU Sensors Market is dominated by a few established aerospace and defense contractors, with Honeywell International and Northrop Grumman collectively controlling nearly 40% of the market share. These leaders specialize in Fiber Optic Gyroscope (FOG) and Ring Laser Gyroscope (RLG) technologies, primarily serving military and commercial aerospace applications. SAFRAN and Thales follow closely, leveraging their European base to cater to Airbus and regional defense programs with advanced MEMS-based IMUs.

Mid-tier players like Kearfott, KVH Industries, and UTC carve out specialized niches Kearfott in precision navigation for missile guidance, KVH in miniature FOG solutions, while UTC excels in ruggedized industrial IMUs. Emerging competitors such as SBG Systems and VectorNav disrupt traditional segments with cost-effective MEMS-IMU fusion for autonomous systems, though they currently hold sub-5% market shares.

List of Key Electronic IMU Sensors Companies Profiled

- Honeywell International

- Northrop Grumman Corp

- SAFRAN

- Thales

- Kearfott

- KVH Industries

- UTC

- Systron Donner Inertial

- IAI Tamam

- Elop

- L-3 Communications

- VectorNav

- Tronics

- SBG systems

- AOSense

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

FOG

|

| By Application |

|

Aerospace

|

| By End User |

|

Military & Defense

|

| By Performance Level |

|

Navigation Grade

|

| By Technology |

|

MEMS-based

|

Regional Analysis: Electronic IMU Sensors Market

North American aerospace manufacturers extensively use electronic IMU sensors for flight control systems and platform stabilization. The region’s stringent safety regulations drive adoption of high-reliability inertial measurement solutions in commercial and military aircraft.

Major automotive OEMs and tech companies in the region are accelerating testing of autonomous vehicles, creating substantial demand for compact, high-performance IMU sensors for navigation and positioning systems in varying environmental conditions.

Growing automation across manufacturing sectors fuels adoption of IMU sensors for robotic positioning and motion control systems. The region’s focus on smart factories and Industry 4.0 initiatives supports long-term market growth.

North America hosts leading research institutions and technology firms developing next-generation IMU solutions, including quantum and fiber-optic gyroscopes, maintaining the region’s technological edge in precision motion sensing applications.

Europe

Europe holds significant position in the Electronic IMU Sensors Market with strong automotive and industrial automation sectors driving demand. The region benefits from well-established aerospace manufacturers and growing investments in satellite navigation technologies. Stringent EU regulations regarding vehicle safety and navigation standards boost adoption rates. Germany leads regional growth with advanced manufacturing capabilities, while France shows strength in defense applications. The increasing deployment of industrial robots across manufacturing facilities creates steady demand for precision motion sensors. European research initiatives focusing on miniaturized IMU solutions for IoT applications present new growth opportunities.

Asia-Pacific

Asia-Pacific emerges as the fastest growing region for Electronic IMU Sensors, fueled by expanding automotive production and defense modernization programs. China dominates the regional market with massive investments in autonomous vehicle technologies and space exploration. Japan maintains technological leadership in MEMS-based sensor manufacturing. India shows accelerating demand driven by defense sector upgrades and growing drone applications. The region benefits from cost-effective manufacturing capabilities and increasing R&D investments. Expanding industrial automation across electronics manufacturing sectors creates new opportunities for IMU sensor adoption.

Middle East & Africa

The Middle East demonstrates growing demand for Electronic IMU Sensors in defense and aerospace applications, supported by substantial military budgets. Gulf countries invest in advanced navigation systems for both military and commercial aircraft. Africa shows emerging potential with increasing adoption in mining and oil & gas exploration equipment. The region benefits from expanding infrastructure projects requiring surveying and positioning technologies. While the market remains relatively smaller compared to other regions, strategic partnerships with global sensor manufacturers are facilitating technology transfer and localized solutions.

South America

South America presents developing opportunities in the Electronic IMU Sensors Market, primarily driven by agricultural automation and defense modernization. Brazil leads regional adoption with applications in aerospace and automotive sectors. The mining industry creates demand for ruggedized IMU solutions for heavy equipment navigation. Challenges include limited local manufacturing capabilities and reliance on imports. However, growing government initiatives to develop domestic technology sectors and partnerships with international sensor providers are gradually improving market conditions across the region.

Report Scope

This market research report provides a comprehensive analysis of the Electronic IMU Sensors Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Electronic IMU Sensors Market?

-> Electronic IMU Sensors Market was valued at USD 2017 million in 2025 and is projected to reach USD 2772 million by 2033, exhibiting a CAGR of 4.8% during the forecast period.

Which key companies operate in Electronic IMU Sensors Market?

-> Key players include Honeywell International, Northrop Grumman Corp, SAFRAN, Thales, Kearfott, KVH Industries, UTC, Systron Donner Inertial, IAI Tamam, Elop, L-3 Communications, VectorNav, Tronics, SBG systems, AOSense, Analog Devices, MEGGITT, Sensonor, EPSON TOYOCOM, JAE, among others. Global top five players hold a share about 75%.

What are the key growth drivers?

-> Key growth drivers include increasing demand in aerospace and defense applications, advancements in MEMS technology, and rising industrial automation.

Which region dominates the market?

-> North America is the largest market with a share of about 40%, followed by Europe and China, having a combined share of 50%.

What are the emerging trends?

-> Emerging trends include development of high-performance MEMS IMUs, integration of AI in inertial navigation systems, and miniaturization of IMU sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...