MARKET INSIGHTS

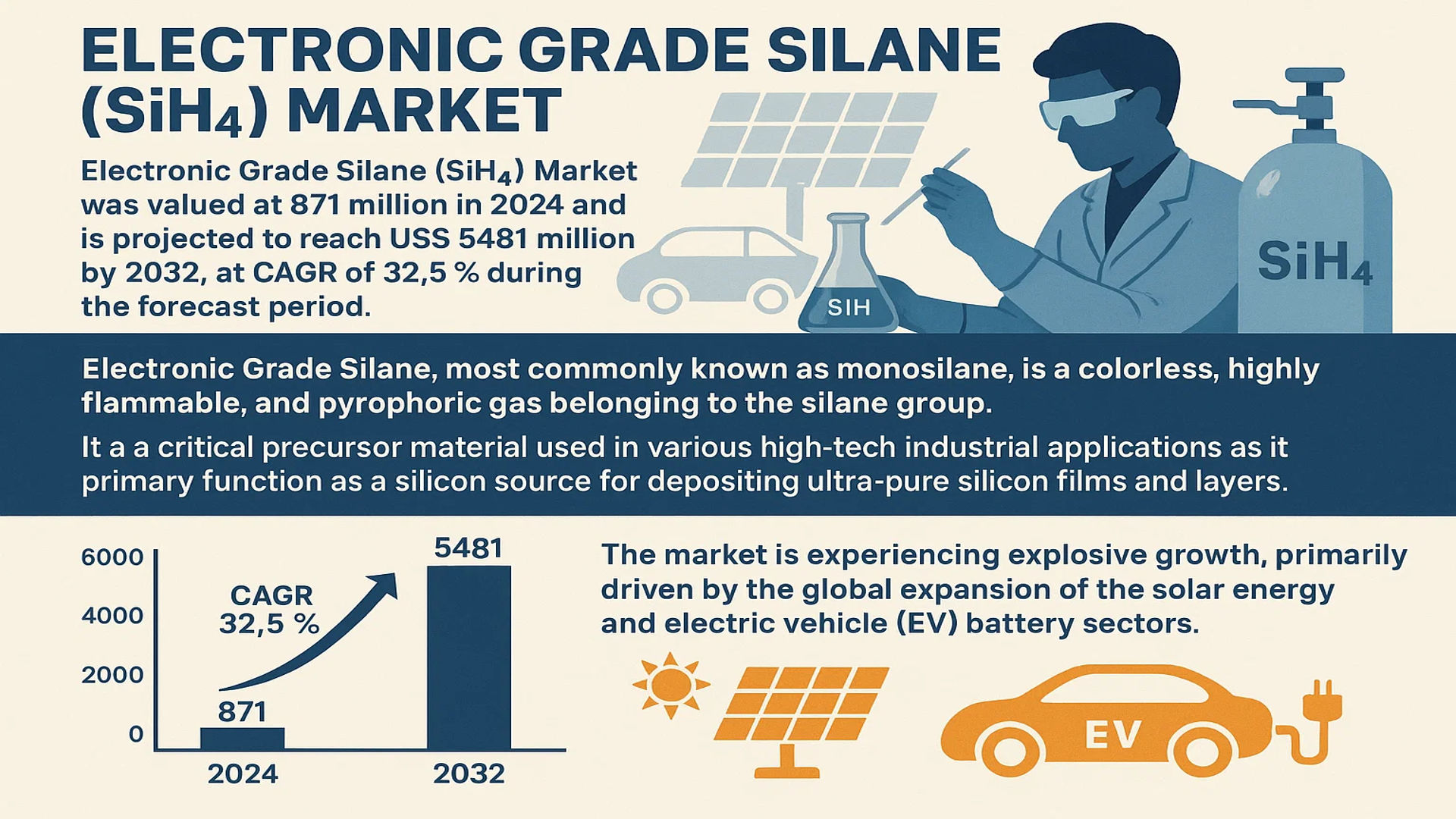

The global Electronic Grade Silane (SiH4) Market was valued at 871 million in 2024 and is projected to reach US$ 5481 million by 2032, at a CAGR of 32.5% during the forecast period.

Electronic Grade Silane, most commonly known as monosilane, is a colorless, highly flammable, and pyrophoric gas belonging to the silane group. It is a critical precursor material used in various high-tech industrial applications because of its high reactivity and purity. Its primary function is as a silicon source for depositing ultra-pure silicon films and layers.

The market is experiencing explosive growth, primarily driven by the global expansion of the solar energy and electric vehicle (EV) battery sectors. In solar cell manufacturing, monosilane is essential for producing high-efficiency crystalline silicon panels. Furthermore, its use in creating silicon anode materials for next-generation lithium-ion batteries is a major growth driver, with this application segment already accounting for approximately 35% of the market. China dominates global consumption, holding a 74% market share, due to its massive manufacturing base for both photovoltaics and batteries. Key players like REC Silicon, Air Liquide, and Linde lead the market, focusing on producing high-purity grades (above 6N), which constitute over 90% of the market, to meet the stringent requirements of these advanced industries.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Solar Energy and Semiconductor Industries Driving Market Growth

The global push toward renewable energy and advanced electronics is creating unprecedented demand for electronic grade silane. Solar energy capacity additions reached approximately 350 gigawatts globally in 2023, representing a 35% year-over-year increase, with China accounting for over 60% of new installations. This massive solar expansion directly fuels demand for silane in thin-film solar cell production, where it serves as a crucial precursor for amorphous silicon layers. Simultaneously, the semiconductor industry’s growth, particularly in advanced nodes below 7nm, requires increasing amounts of high-purity silane for chemical vapor deposition processes. The semiconductor market is projected to exceed $1 trillion by 2030, with foundries investing over $200 billion in new capacity between 2024 and 2026. These parallel expansions in both sectors create a powerful synergistic effect on silane demand.

Electric Vehicle Battery Revolution Accelerating Silane Consumption

The transition to electric mobility represents a transformative driver for electronic grade silane markets. Silicon-based anode materials are becoming increasingly critical for next-generation lithium-ion batteries, offering up to 10 times higher theoretical capacity than traditional graphite anodes. Global electric vehicle sales surpassed 14 million units in 2023 and are projected to reach 45 million by 2030, creating enormous demand for advanced battery technologies. Major battery manufacturers are investing over $150 billion in new production facilities worldwide, with silicon anode technology expected to capture approximately 25% of the anode market by 2030. This technological shift requires substantial quantities of high-purity silane for silicon deposition processes, positioning the battery sector as the fastest-growing application segment.

Technological Advancements in Display Manufacturing Boosting Demand

Advanced display technologies are creating new opportunities for electronic grade silane applications. The global display panel market, valued at approximately $180 billion in 2024, increasingly relies on silane for thin-film transistor production and surface passivation layers. Organic light-emitting diode (OLED) display shipments grew by over 28% in 2023, with flexible and foldable displays requiring specialized silicon-based coatings that utilize high-purity silane. Furthermore, the emergence of microLED technology, projected to reach $10 billion by 2028, incorporates sophisticated deposition processes that depend on electronic grade silane for precise layer formation. Display manufacturers are investing heavily in new fabrication facilities, particularly across Asia, creating sustained demand growth for high-purity silane products.

MARKET CHALLENGES

High Production Costs and Complex Manufacturing Processes Impeding Market Accessibility

The electronic grade silane market faces significant challenges related to its complex production economics. Manufacturing high-purity silane requires sophisticated purification systems capable of achieving parts-per-billion impurity levels, with production costs approximately 40-50% higher than industrial grade alternatives. The capital expenditure for a new electronic grade silane production facility typically exceeds $300 million, creating substantial barriers to market entry. Additionally, energy consumption accounts for nearly 60% of operational costs, making production highly sensitive to electricity price fluctuations. These economic factors particularly impact smaller manufacturers and emerging markets where cost sensitivity is more pronounced.

Other Challenges

Supply Chain Vulnerabilities

Global supply chain disruptions continue to challenge silane market stability. Transportation restrictions for hazardous materials, particularly across international borders, create logistical complexities and increase delivery costs by 25-30%. Specialty cylinder requirements for silane storage and transport add another layer of complexity, with lead times for certified containers extending to 12-18 months. These supply chain issues are exacerbated by geopolitical tensions and trade restrictions affecting key manufacturing regions.

Technical Specification Stringency

Increasing purity requirements present ongoing technical challenges. The transition from 6N to 7N purity standards demands additional purification stages that reduce yield rates by approximately 15-20%. Meeting evolving customer specifications for specific metallic impurities, particularly in semiconductor applications, requires continuous process optimization and substantial quality control investments. These technical hurdles particularly affect manufacturers transitioning from industrial to electronic grade production capabilities.

MARKET RESTRAINTS

Safety Concerns and Regulatory Compliance Limiting Market Expansion

Electronic grade silane’s highly pyrophoric nature presents significant safety challenges that restrain market growth. Spontaneous combustion risks require specialized handling equipment and safety protocols that increase operational costs by 20-25%. Regulatory compliance with hazardous material regulations across different jurisdictions creates complex operational frameworks, particularly for multinational suppliers. Insurance premiums for silane production and transportation are approximately three times higher than for conventional industrial gases, reflecting the elevated risk profile. These safety considerations particularly impact market penetration in regions with stringent environmental and safety regulations.

Technological Substitution Threats Creating Market Uncertainty

Emerging alternative technologies pose potential threats to traditional silane applications. Developments in atomic layer deposition techniques utilizing alternative precursors could reduce silane consumption in certain semiconductor processes by 30-40%. Research into silicon-free anode materials for lithium-ion batteries, while still in early stages, represents a long-term challenge to silane demand growth in the battery sector. Additionally, advancements in display manufacturing technologies exploring alternative deposition materials could potentially impact silane consumption patterns in the display industry. These technological evolution trends create market uncertainty and may restrain investment decisions in production capacity expansion.

Geographic Concentration Creating Supply Chain Vulnerabilities

The extreme geographic concentration of both production and consumption creates systemic market vulnerabilities. China’s dominance as both a producer and consumer, accounting for over 74% of global consumption, creates supply chain risks during regional disruptions. Production capacity concentration among five major manufacturers controlling nearly half the market increases vulnerability to facility-specific disruptions. This geographic and corporate concentration creates challenges for diversifying supply sources and may restrain market growth in regions seeking to develop local supply capabilities. The situation is particularly challenging for markets outside Asia, where transportation costs and lead times create competitive disadvantages.

MARKET OPPORTUNITIES

Next-Generation Semiconductor Technologies Opening New Application Frontiers

Advanced semiconductor manufacturing processes are creating substantial opportunities for electronic grade silane. The transition to 3nm and smaller process nodes requires increasingly sophisticated deposition techniques that utilize higher purity silane specifications. Silicon nitride deposition processes for gate spacers and isolation layers are consuming growing volumes of electronic grade silane, with leading foundries projecting 40% increased consumption per wafer at advanced nodes. Additionally, emerging memory technologies including 3D NAND and DRAM applications are incorporating new silane-based processes that could increase market demand by 25-30% over the next five years. These technological advancements create opportunities for suppliers capable of meeting increasingly stringent purity requirements.

Energy Storage Innovation Driving New Market Segments

The energy storage revolution presents transformative opportunities for electronic grade silane. Beyond electric vehicle batteries, grid-scale energy storage applications are emerging as a significant growth segment. Global energy storage deployments are projected to increase fifteenfold by 2030, creating massive demand for advanced battery technologies. Silicon anode technology, enabled by high-purity silane deposition processes, offers particular advantages for grid storage applications where cycle life and energy density are critical parameters. Additionally, emerging solid-state battery technologies incorporate silicon-based components that require electronic grade silane, potentially creating entirely new application segments worth approximately $5 billion annually by 2030.

Geographic Expansion and Supply Chain Diversification Creating Strategic Opportunities

Current market concentration patterns create significant opportunities for geographic expansion and supply chain diversification. North American and European initiatives to develop local semiconductor and battery supply chains are driving investments in regional electronic grade silane production. Government incentives totaling over $100 billion across various jurisdictions are accelerating capacity development outside traditional manufacturing regions. This geographic diversification presents opportunities for both existing manufacturers expanding globally and new entrants developing regional capabilities. Additionally, supply chain security concerns are driving demand for diversified supply sources, creating opportunities for suppliers capable of establishing reliable production and delivery capabilities in multiple regions.

ELECTRONIC GRADE SILANE (SIH4) MARKET TRENDS

Explosive Growth in Silicon Anode Batteries to Emerge as a Dominant Trend

The most significant trend shaping the Electronic Grade Silane market is its rapidly expanding application in next-generation lithium-ion batteries, specifically as a precursor for silicon anode materials. While the solar industry has historically been the largest consumer, accounting for approximately 47% of demand, the battery sector is projected to become the primary driver. This shift is fueled by the automotive industry’s relentless pursuit of higher energy density to extend electric vehicle range. Silicon anodes offer a theoretical capacity nearly ten times that of traditional graphite, and silane gas is the critical raw material deposited via chemical vapor deposition to create high-purity silicon coatings. This demand is reflected in the market’s projected compound annual growth rate of 32.5%, with battery applications expected to capture the largest market share in the coming years, potentially exceeding 50% by the end of the forecast period. Major battery manufacturers and automotive OEMs are securing long-term supply agreements with silane producers, creating a robust and predictable demand pipeline that is fundamentally altering the market’s structure.

Other Trends

Technological Advancements in Purification and Production

Concurrent with demand growth, significant advancements in production technology are emerging as a critical trend. The market for ultra-high purity silane, specifically grades at 6N (99.9999%) and above, which already commands over 90% market share, is pushing manufacturers to innovate. Traditional purification methods are being augmented with sophisticated adsorption and distillation techniques to reduce metallic impurities to parts-per-trillion levels, a necessity for advanced semiconductor nodes below 5nm and high-efficiency solar cells. Furthermore, the industry is moving towards larger-scale, more energy-efficient production reactors to improve economies of scale and reduce the carbon footprint of manufacturing. This focus on technological refinement is not only about meeting purity specifications but also about enhancing safety protocols for handling this highly pyrophoric gas, thereby reducing operational risks and insurance costs for end-users.

Geographic Supply Chain Consolidation and Regional Policies

A clear trend of geographic supply chain consolidation is underway, heavily influenced by regional industrial policies and energy costs. China’s dominance as a consumer, with over 74% of the global market, is driving massive domestic production investments. This is largely supported by government policies aimed at securing the supply chain for both the photovoltaic and electric vehicle industries. However, this concentration also presents a risk, prompting other regions like North America and Europe to reassess their strategic dependencies. The U.S. Inflation Reduction Act, for instance, is incentivizing local production of battery components, which indirectly stimulates investment in domestic silane capacity. This trend is creating a more fragmented global supply landscape, where logistics and regional pricing disparities become increasingly important factors for market participants. While global trade continues, the push for regional self-sufficiency in key technology supply chains is a powerful force shaping investment and long-term planning for all major silane producers.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Capacity Expansions and Technological Purity Advancements Define Market Competition

The global Electronic Grade Silane (SiH4) market exhibits a semi-consolidated structure, dominated by a handful of major international corporations that command significant production capacity and technological expertise. REC Silicon is the unequivocal market leader, holding a 12.89% share of the global market in 2024. This preeminence is largely due to its vertically integrated operations, which span from polysilicon production to high-purity monosilane gas, and its established supply agreements with major solar and semiconductor manufacturers.

Air Liquide and Linde plc are other pivotal players, leveraging their vast global industrial gas infrastructure and deep expertise in gas purification and handling to secure a strong foothold. Their growth is heavily driven by the burgeoning demand from the semiconductor industry, where ultra-high purity gases are non-negotiable. Because these companies operate on a global scale, they are exceptionally well-positioned to serve multinational clients and navigate complex international supply chains.

Meanwhile, Chinese manufacturers are asserting immense influence on the global supply dynamics. Inner Mongolia Xingyang Technology Co., Ltd. and China National Silicon Industry Group (CNS) have rapidly expanded their capacity to cater to the domestic market, which consumes over 74% of the world’s monosilane. Their competitive strategy often revolves around cost leadership and securing long-term contracts within the massive Chinese solar PV and battery anode material sectors. Furthermore, these companies are aggressively investing in R&D to achieve higher purity levels, aiming to compete directly with established Western players in the more demanding semiconductor segment.

The intense competition is compelling all key players to prioritize significant capital expenditure towards capacity expansion and purity enhancement. For instance, achieving and maintaining purity levels above 6N (99.9999%), which constitutes over 90% of the market by type, requires sophisticated purification technology and represents a major barrier to entry. Consequently, strategic partnerships, long-term offtake agreements, and continuous innovation in production processes are critical for sustaining market position and capitalizing on the projected 32.5% CAGR growth.

List of Key Electronic Grade Silane (SiH4) Companies Profiled

- REC Silicon ASA (Norway)

- Air Liquide S.A. (France)

- Linde plc (U.K.)

- Inner Mongolia Xingyang Technology Co., Ltd. (China)

- China National Silicon Industry Group Co., Ltd. (CNS) (China)

- SK Materials Co., Ltd. (South Korea)

- Taiyo Nippon Sanso Corporation (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- Henan Silane Technology Development Co., Ltd. (China)

Segment Analysis:

By Purity Grade

Ultra-High Purity Segment Dominates the Market Due to Critical Requirements in Semiconductor and Photovoltaic Manufacturing

The market is segmented based on purity grade into:

- Purity ≥6N

- Subtypes: 6N, 6.5N, 7N, and others

- Purity <6N

By Application

Solar Cell Manufacturing Segment Leads Due to Massive Global Expansion of Photovoltaic Production Capacity

The market is segmented based on application into:

- Solar cell manufacturing

- Battery silicon anode material

- Semiconductor manufacturing

- Display panel production

- Others

By End-User Industry

Renewable Energy Sector Commands Largest Share Fueled by Global Transition to Sustainable Power Sources

The market is segmented based on end-user industry into:

- Renewable energy

- Electronics and semiconductor

- Energy storage

- Display technologies

- Others

Regional Analysis: Electronic Grade Silane (SiH4) Market

Asia-Pacific

This region is unequivocally the dominant force in the global Electronic Grade Silane market, accounting for over 74% of global consumption, with China as its undisputed epicenter. This overwhelming market share is driven by the country’s colossal manufacturing base for solar panels and lithium-ion batteries. The nation’s “14th Five-Year Plan” explicitly supports the expansion of renewable energy and high-tech industries, creating immense, sustained demand for monosilane. While cost sensitivity has historically favored domestic producers offering competitive pricing, there is a marked and accelerating shift towards higher purity grades (above 6N) to meet the stringent requirements of next-generation semiconductor fabrication and premium silicon anode materials for electric vehicle batteries. This trend is further fueled by rapid urbanization, government mandates for clean energy, and the strategic importance of securing the domestic semiconductor supply chain.

North America

The North American market, while smaller in volume than Asia-Pacific, is characterized by its focus on high-value, technologically advanced applications. Demand is primarily driven by the robust semiconductor industry in the United States, supported by legislation like the CHIPS and Science Act, which allocates billions in funding to bolster domestic chip manufacturing. This necessitates a reliable supply of ultra-high-purity Electronic Grade Silane. Furthermore, the growing electric vehicle sector is spurring investment in domestic battery production, creating a new and significant demand stream for silicon anode materials. The market is dominated by technologically sophisticated players, and stringent safety and environmental regulations govern the handling and use of this highly pyrophoric gas, ensuring high operational standards.

Europe

The European market is shaped by a dual focus on technological innovation and regulatory compliance. Strict environmental, health, and safety directives under the EU’s REACH regulation govern the production and use of chemicals like SiH4, pushing manufacturers towards developing safer handling technologies and sustainable production processes. Demand is anchored by a strong automotive sector that is rapidly electrifying, necessitating advanced battery materials, and a well-established semiconductor industry, particularly in Germany and France. The European Green Deal, which aims for climate neutrality, also indirectly supports the solar energy sector, a traditional consumer of silane. However, high production costs and energy prices present ongoing challenges for local manufacturers competing with imported materials.

Middle East & Africa

This region represents an emerging market with significant long-term potential, though current consumption volumes remain relatively low. Growth is primarily linked to strategic economic diversification initiatives undertaken by nations like Saudi Arabia and the UAE, which include investments in renewable energy infrastructure and smart city technologies. These projects will gradually drive demand for solar panels and, consequently, the silane used in their production. However, the market’s development is currently constrained

Report Scope

This market research report provides a comprehensive analysis of the global and regional Electronic Grade Silane (SiH4) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronic Grade Silane (SiH4) Market?

-> Electronic Grade Silane (SiH4) Market was valued at 871 million in 2024 and is projected to reach US$ 5481 million by 2032, at a CAGR of 32.5% during the forecast period.

Which key companies operate in Global Electronic Grade Silane (SiH4) Market?

-> Key players include REC Silicon, Air Liquide, Linde, Inner Mongolia Xingyang Technology, and CNS, which collectively hold approximately 47% of the global market share.

What are the key growth drivers?

-> Key growth drivers include the expansion of the solar energy sector, rising demand for silicon anode batteries in electric vehicles, and advancements in semiconductor manufacturing processes.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China alone accounting for over 74% of global consumption due to its massive solar panel and electronics manufacturing base.

What are the emerging trends?

-> Emerging trends include the shift toward higher purity grades (above 6N), increasing adoption in lithium-ion battery silicon anode production, and development of safer handling and transportation protocols for this highly pyrophoric material.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...