MARKET INSIGHTS

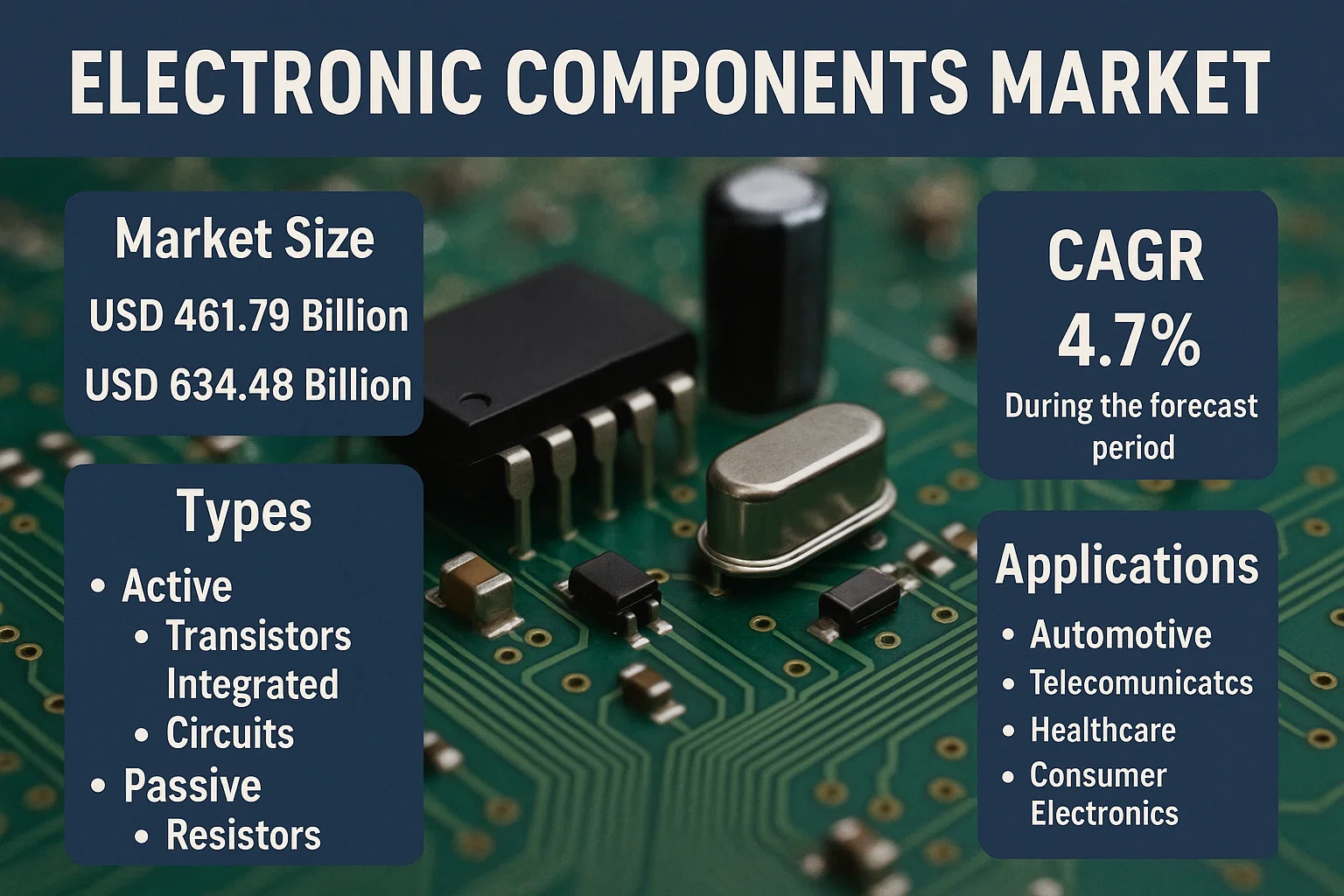

Global Electronic Components Market size was valued at USD 461.79 billion in 2024 to USD 634.48 billion by 2032, exhibiting a CAGR of 4.7% during the forecast period.

Electronic components are fundamental building blocks of electronic circuits, enabling functionalities such as signal processing, amplification, and energy conversion. These components are categorized into active (e.g., transistors, integrated circuits) and passive (e.g., resistors, capacitors) types, with applications spanning industries like automotive, telecommunications, healthcare, and consumer electronics. The increasing demand for miniaturization, energy efficiency, and high-performance devices continues to drive innovation in this sector.

The market is expanding due to the proliferation of IoT devices, 5G adoption, and advancements in automotive electronics. For instance, the growing deployment of electric vehicles (EVs) has significantly boosted demand for power semiconductors and sensors. Additionally, the shift toward Industry 4.0 and smart manufacturing is accelerating the adoption of advanced electronic components. Key players such as Texas Instruments, Murata, and Infineon Technologies are investing in R&D and strategic partnerships to strengthen their market position and cater to emerging technological demands.

MARKET DRIVERS

Rapid Digital Transformation Across Industries

The global push towards Industry 4.0 has accelerated the adoption of electronic components across manufacturing, healthcare, and automotive sectors. Companies are investing heavily in IoT-enabled devices, which require sophisticated semiconductor components to function effectively.

Growth in Electric Vehicle Production

With governments worldwide setting ambitious targets for electric vehicle adoption, the demand for power electronics, sensors, and control modules has surged. Major manufacturers are scaling production, requiring reliable supplies of advanced electronic components.

➤ Automotive industry’s shift towards autonomous driving systems has created unprecedented demand for high-performance processors and sensor arrays

Next-generation vehicles require advanced driver-assistance systems (ADAS), which utilize complex electronic components for real-time data processing and decision-making.

MARKET CHALLENGES

Global Semiconductor Shortage

The ongoing semiconductor shortage continues to disrupt supply chains across multiple industries. Automotive manufacturers have reported production halts due to insufficient chip supplies, while consumer electronics companies face extended lead times exceeding 52 weeks for certain components.

Other Challenges

Supply Chain Disruptions

Logistical challenges and geopolitical tensions have created bottlenecks in the raw material supply chain. Critical raw materials such as rare earth elements face volatile pricing and availability, impacting component manufacturing costs.

MARKET RESTRAINTS

High Research and Development Costs

Developing next-generation electronic components requires substantial investment in research and development. Advanced semiconductor nodes below 7nm require capital expenditures exceeding $20 billion per facility, creating significant barriers to entry for new market participants.

MARKET OPPORTUNITIES

5G Infrastructure Expansion

The global rollout of 5G networks requires massive deployment of new infrastructure components. Base stations, small cells, and network equipment all require advanced electronic components that can handle higher frequencies and data throughput. This creates sustained demand for RF components, power management ICs, and advanced processors.

Artificial Intelligence and Edge Computing

Edge computing deployments are creating new markets for specialized processors and memory components. AI applications require specialized hardware accelerators, creating opportunities for manufacturers of high-performance computing components and custom ASICs.

Space and Defense Applications

Increased government spending on defense and space exploration has created demand for radiation-hardened components, high-temperature electronics, and advanced communication modules. These applications typically command higher profit margins than commercial components.

Electronic Components Market Trends

Miniaturization and Integration Driving Market Evolution

The global electronic components market is experiencing significant transformation driven by the relentless pursuit of miniaturization and higher integration densities. Semiconductor manufacturers are pushing the boundaries of Moore’s Law with advanced packaging technologies like chiplets and 3D stacking, allowing for more functionality in smaller form factors. This trend is particularly crucial for mobile devices, IoT devices, and advanced computing systems where space constraints are paramount. The shift towards System-in-Package (SiP) designs is enabling more complex functionality in compact packages, while advanced substrates and interconnects are improving thermal management and signal integrity at reduced scales.

Advanced packaging technologies such as fan-out wafer-level packaging (FOWLP) and integrated passive devices (IPDs) are becoming standard in high-performance applications. Manufacturers are increasingly adopting heterogeneous integration techniques to combine different chip technologies within single packages. The demand for smaller, more powerful components is driving R&D investments in materials science and manufacturing processes. Leading companies are developing ultra-thin substrates, high-density interconnects, and advanced thermal management solutions to support these trends. The market is also seeing increased adoption of system-level packaging where multiple functions are integrated into single modules, reducing overall system size and improving performance.

Other Trends

Supply Chain Diversification and Regionalization

The electronic components market is experiencing significant supply chain restructuring following recent global disruptions. Companies are diversifying their supplier base across different geographic regions, with particular focus on reducing dependency on single-source suppliers. Many manufacturers are implementing dual-sourcing strategies and increasing their inventory buffers for critical components. The trend towards regional manufacturing clusters is accelerating, with companies establishing production facilities closer to end markets to reduce logistics risks. Countries are implementing policies to strengthen domestic semiconductor and electronics production capabilities, with significant investments in new fabrication plants and testing facilities. Supply chain transparency and traceability have become priority concerns, driving adoption of blockchain and other tracking technologies across the component supply chain.

Rising Demand from Electric Vehicles and Renewable Energy

The rapid growth of electric vehicles (EVs) and renewable energy infrastructure is creating unprecedented demand for advanced electronic components. EV manufacturers require high-performance power semiconductors, advanced battery management systems, and sophisticated sensor networks, all demanding specialized components rated for automotive applications. The shift to electric powertrains is driving demand for high-voltage capacitors, advanced power MOSFETs, and gate driver ICs capable of operating in harsh automotive environments. Solar and wind energy installations require robust power conversion components, grid interface electronics, and advanced monitoring systems, all requiring specialized electronic components designed for high reliability and long service life.

Grid-scale energy storage systems are driving demand for advanced battery management ICs, power converters, and grid interface electronics. The expansion of charging infrastructure for electric vehicles requires specialized power electronics, communication modules, and payment processing components. Wind turbine installations require robust condition monitoring systems, power converters, and pitch control systems, all demanding high-reliability electronic components. The integration of renewable energy sources requires sophisticated grid management electronics, smart inverters, and distributed control systems that continue to drive component innovation.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Electronic Components Manufacturers

The electronic components market is dominated by large multinational corporations with extensive product portfolios and global reach. Texas Instruments leads in analog semiconductors, while Murata Manufacturing dominates in passive components and advanced materials. Japanese and South Korean manufacturers maintain strong positions in high-frequency and high-precision components.

Chinese manufacturers have rapidly expanded their market share in recent years, particularly in the consumer electronics and industrial sectors. Companies like Huawei, ZTE, and several emerging manufacturers are now competing effectively in specific component categories such as connectors, sensors, and power devices. The market remains fragmented with specialized players dominating niche segments.

List of Key Electronic Components Companies

- Texas Instruments Inc.

- Murata Manufacturing Co., Ltd.

- ABB Ltd.

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Kyocera Corporation

- Omron Corporation

- Amphenol Corporation

- Infineon Technologies AG

- Samsung Electro-Mechanics Co., Ltd.

- TDK Corporation

- Analog Devices, Inc.

- Molex, LLC

- Vishay Intertechnology, Inc.

- ON Semiconductor Corporation

- Microchip Technology Inc.

- Panasonic Corporation

- TE Connectivity Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Semiconductors dominate due to their critical role in all modern electronics, from smartphones to industrial automation, while Optoelectronics show strong growth driven by demand for displays and sensors across industries. |

| By Application |

|

Consumer Electronics represents the largest segment due to massive global demand for smartphones and smart devices, while Automotive is the fastest growing segment with increasing electronic content per vehicle for ADAS and connectivity. |

| By End User |

|

OEMs (Original Equipment Manufacturers) lead in consumption as they integrate components into final products, while Distributors and Resellers show strong growth due to the increasing complexity of supply chains and need for specialized component distribution. |

| By Region |

|

Asia Pacific dominates production and consumption with China as the manufacturing hub and India showing rapid growth in both production and adoption of electronic components across industries. |

| By Technology |

|

Silicon-based technologies remain dominant due to maturity and cost-effectiveness, while Compound Semiconductors show exceptional growth for specialized applications requiring higher performance in harsh environments. |

Regional Analysis: Electronic Components Market

Asia-Pacific’s manufacturing ecosystem for electronic components is the most globally integrated, with China alone producing over half of all electronic components worldwide. The region’s dominance stems from complete supply chain integration, from raw material processing to final product assembly, supported by massive government investments in semiconductor fabrication plants and decades of accumulated manufacturing expertise. The ecosystem benefits from continuous technology transfer between leading countries in the region.

Asia-Pacific’s electronic components supply chain demonstrates unprecedented integration, with neighboring countries specializing in complementary production stages. China focuses on mass production of standard components, Taiwan excels in semiconductor manufacturing and advanced chip design, South Korea leads in memory chips and display technologies, while Japan maintains leadership in high-precision components and specialized materials. This integration creates a production network unmatched in other regions, allowing Asia-Pacific to maintain competitive advantage in both cost and technological advancement simultaneously.

While Asia-Pacific leads in manufacturing, the region has increasingly become the global center for electronics research and development. South Korea and Japan maintain the highest R&D investment-to-GDP ratios globally, with China now producing more electronics patents than any other country. Taiwan’s semiconductor R&D capabilities rival global leaders, particularly in chip design and process optimization. The region hosts numerous corporate and government research institutes specifically focused on next-generation electronic components.

Asia-Pacific itself represents the largest and fastest-growing market for electronic components, fueled by rising incomes, digitalization initiatives, and massive technology adoption. China’s domestic demand alone exceeds North America and Europe combined for many component categories. The region’s demand drives innovation toward consumer electronics applications and supports scale that enables cost-competitive production. This internal demand creates a self-sustaining cycle where manufacturing scale drives down costs, enabling wider adoption, which in turn drives further production scale-up and innovation.

North America

North America maintains strength in semiconductor design, aerospace and defense components, and specialized high-performance computing applications. The region benefits from strong university research, venture capital funding for hardware startups, and close collaboration between defense agencies and component manufacturers. While losing volume production to Asia, North America maintains leadership in design, architecture, and high-value-added specialized components through continuous innovation in areas like AI chips, quantum computing components, and next-generation semiconductor materials.

Europe

Europe maintains competitiveness in industrial and automotive electronics, with Germany’s automotive sector driving demand for high-reliability components. The region excels in precision manufacturing equipment for electronics production, semiconductor manufacturing equipment, and specialty materials. Europe maintains strong positions in photonics, sensor technologies, and industrial IoT components while leveraging integration with North America on defense and aerospace applications. The region’s focus on quality and reliability over pure cost-competitiveness creates differentiated positioning.

Latin America

Latin America’s electronic components market primarily serves domestic demand with limited export orientation. Brazil and Mexico developed significant manufacturing capabilities, particularly in automotive electronics and consumer goods, though they remain net importers of advanced components. The region benefits from proximity to North American markets while facing challenges in supply chain integration and technology transfer. Recent growth focuses on serving domestic demand from growing middle classes while developing specialized capabilities in medical electronics and renewable energy components.

Middle East & Africa

Middle East & Africa represent developing markets with growth potential but current limited scale. The region focuses primarily on final assembly rather than component manufacturing, though Israel developed significant capabilities in security and military electronics. African nations increasingly serve as markets for inexpensive components while developing local assembly capacity. The region shows potential in renewable energy components and mobile technology applications, though infrastructure challenges remain for advanced manufacturing.

Report Scope

This market research report provides a comprehensive analysis of the Electronic Components Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Electronic Components Market?

-> Electronic Components Market was valued at USD 461790 million in 2024 and is expected to reach USD 634480 million by 2032.

What is the CAGR for Electronic Components Market?

-> The CAGR for Electronic Components Market is 4.7% during the forecast period 2024-2032.

What are the key market segments?

-> The market is segmented by type into active components, passive components, and electromechanical components. By application, it covers automotive, communications and computing, lighting, industrial, medical, security applications, and others.

Which regions dominate the market?

-> Asia-Pacific is the largest and fastest-growing market, followed by North America and Europe. The growth is driven by increasing electronics production, technological advancements, and high demand from end-use industries.

Who are the key market players?

-> Key players include Texas Instruments, Murata, STMicroelectronics, NXP Semiconductors, Infineon Technologies, TE Connectivity, and Samsung Electro-Mechanics, among others.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...