MARKET INSIGHTS

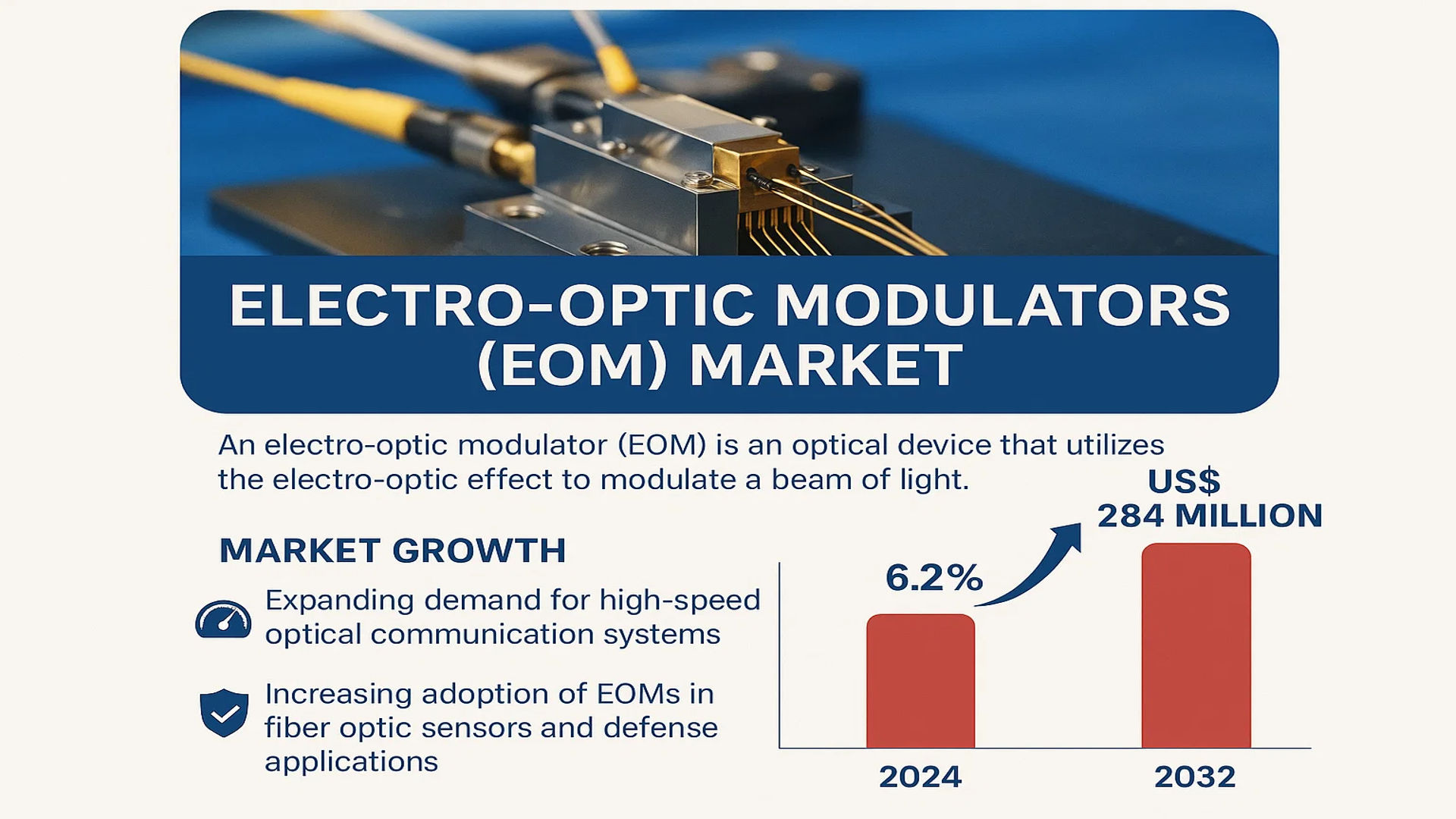

The global Electro-Optic Modulators (EOM) Market was valued at 189 million in 2024 and is projected to reach US$ 284 million by 2032, at a CAGR of 6.2% during the forecast period.

An electro-optic modulator (EOM) is a critical optical device that utilizes a signal-controlled element exhibiting the electro-optic effect to modulate a beam of light. This modulation can be imposed on the beam’s phase, frequency, amplitude, or polarization, making EOMs fundamental components for precise control of light in advanced photonic systems.

The market’s steady growth is primarily driven by the expanding demand for high-speed optical communication systems and the increasing adoption of EOMs in fiber optic sensors and defense applications. Furthermore, technological advancements in materials like lithium niobate (LiNbO₃) are enhancing modulator performance. The market is also characterized by a high degree of consolidation; the top three players—Thorlabs, Jenoptik, and iXblue—collectively hold approximately 66% of the global market share, underscoring the competitive landscape dominated by established technological leaders.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Optical Communication Networks to Drive Electro-Optic Modulators Demand

The global surge in data consumption, driven by 5G deployment, cloud computing, and IoT proliferation, is fundamentally increasing the need for high-speed, high-bandwidth optical communication systems. Electro-optic modulators serve as critical components in these systems by enabling efficient encoding of electrical signals onto optical carriers. With data traffic projected to grow exponentially—reaching over 180 zettabytes annually by 2025—telecommunication providers and data centers are aggressively upgrading infrastructure, which directly fuels demand for advanced EOMs capable of supporting higher modulation rates and improved signal integrity. This infrastructure modernization is particularly evident in North America and Asia-Pacific, where investments in fiber-optic networks exceed $80 billion annually.

Advancements in Defense and Aerospace Technologies to Accelerate Market Growth

Electro-optic modulators are increasingly deployed in defense applications such as LiDAR, free-space optical communication, and electronic warfare systems due to their ability to provide precise control over laser beams with minimal latency. Global defense spending, which surpassed $2.2 trillion in 2023, continues to prioritize investments in electro-optical and infrared systems, creating sustained demand for high-performance EOMs. These devices enable critical capabilities including secure communications, target designation, and surveillance, with modern systems requiring modulation bandwidths exceeding 40 GHz. Furthermore, the growing adoption of satellite constellations for global connectivity is driving additional demand for space-qualified EOMs that can withstand extreme environmental conditions while maintaining precise performance specifications.

Growth in Quantum Computing and Sensing Applications to Fuel Market Expansion

The emerging field of quantum technology represents a significant growth frontier for electro-optic modulators. Quantum computing systems require precise control of optical qubits, where EOMs manipulate phase and amplitude with unprecedented accuracy. Meanwhile, quantum sensing applications—including gravitational wave detection and magnetic field mapping—depend on modulators to maintain interferometric stability at femtosecond precision. National investments in quantum technology research have exceeded $30 billion globally, with both public and private sectors accelerating development timelines. This technological convergence is pushing manufacturers to develop modulators with lower half-wave voltages, reduced optical losses, and enhanced thermal stability, creating new revenue streams beyond traditional telecommunications markets.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Fabrication Processes to Limit Market Penetration

The production of high-performance electro-optic modulators involves sophisticated materials like lithium niobate, gallium arsenide, and organic polymers, which require precise crystal growth and nanofabrication techniques. These processes demand specialized equipment, cleanroom facilities, and highly trained personnel, resulting in manufacturing costs that can exceed $5,000 per unit for advanced devices. While volume production reduces per-unit costs, the market remains constrained by the capital-intensive nature of fabrication facilities, which require investments ranging from $50 million to $200 million for modern production lines. This economic barrier particularly affects smaller manufacturers and limits price competition, ultimately restraining market growth in cost-sensitive applications.

Technical Challenges in Integration and Performance Consistency to Hinder Adoption

Integrating electro-optic modulators into existing optical systems presents significant technical hurdles, particularly regarding polarization stability, thermal management, and impedance matching. Many applications require modulators to maintain performance across temperature variations exceeding 100°C, necessitating sophisticated compensation mechanisms that add complexity and cost. Additionally, achieving consistent performance across production batches remains challenging due to material variations and fabrication tolerances, with yield rates for high-end modulators sometimes falling below 60%. These technical constraints become particularly problematic in emerging applications like quantum technology and biomedical imaging, where performance specifications often push the boundaries of current manufacturing capabilities.

Supply Chain Vulnerabilities and Material Availability to Constrain Market Development

The electro-optic modulator market faces constraints from limited availability of critical materials, particularly lithium niobate crystals, which account for approximately 70% of commercial modulators. Global production capacity for optical-grade lithium niobate remains concentrated among few suppliers, creating vulnerability to supply disruptions and price volatility. Furthermore, geopolitical factors affecting rare earth elements and specialized substrates introduce additional uncertainty into the supply chain. These material constraints become increasingly problematic as demand grows, with lead times for certain modulator types extending beyond 12 months during periods of market expansion. This supply-demand imbalance particularly affects research institutions and smaller commercial users who lack the purchasing power of large telecommunications equipment manufacturers.

MARKET CHALLENGES

Intense Competitive Pressure and Rapid Technological Obsolescence to Challenge Market Players

The electro-optic modulator market is characterized by rapid technological evolution, where product lifecycles frequently measure less than three years before becoming obsolete. Manufacturers must continuously invest in research and development—typically exceeding 15% of revenue—to maintain competitiveness, creating financial pressure particularly for smaller companies. This innovation race is further intensified by the entry of new players leveraging alternative technologies such as silicon photonics and plasmonics, which threaten to disrupt traditional modulator designs. Meanwhile, pricing pressure from large-volume buyers in the telecommunications sector continues to compress profit margins, with annual price declines of 8-12% becoming commonplace for standard modulator designs.

Other Challenges

Standardization and Interoperability Issues

The absence of universal standards for modulator interfaces and performance metrics creates integration challenges for end-users. Different manufacturers employ varying electrical interfaces, optical connector types, and control protocols, forcing system integrators to develop custom solutions that increase development costs and time-to-market. This lack of standardization becomes particularly problematic in emerging applications where multiple modulator types must work together seamlessly, such as in quantum computing systems or advanced photonic integrated circuits.

Technical Specialization and Knowledge Gap

The highly specialized nature of electro-optic technology has created a significant skills shortage, with an estimated global deficit of 15,000 trained photonics engineers. This knowledge gap affects both manufacturers and end-users, slowing adoption rates and increasing implementation costs. Educational institutions struggle to keep pace with industry requirements, as photonics curricula often lag behind commercial developments by several years. This human resource challenge compounds the technical difficulties of implementing advanced modulator systems, particularly in regions with less developed photonics ecosystems.

MARKET OPPORTUNITIES

Emerging Applications in Biomedical Imaging and Healthcare to Create New Growth Frontiers

Electro-optic modulators are finding expanding applications in medical technology, particularly in advanced imaging systems such as multiphoton microscopy, optical coherence tomography, and laser surgery systems. These medical applications require modulators capable of precise pulse shaping, high repetition rates, and exceptional reliability—specifications that align with ongoing technological advancements. The global medical laser market, projected to exceed $8 billion by 2026, represents a significant opportunity for modulator manufacturers who can develop devices meeting stringent regulatory requirements while providing the performance needed for next-generation diagnostic and therapeutic systems. Recent developments in endoscopic imaging and minimally invasive surgery techniques particularly drive demand for miniaturized modulators with enhanced functionality.

Development of Integrated Photonics and Silicon-Based Modulators to Enable Mass Market Applications

The convergence of photonics and semiconductor manufacturing techniques is creating opportunities for electro-optic modulators based on silicon photonics and other integrated platforms. These technologies promise reduced cost, improved reliability, and smaller form factors—critical factors for volume applications in consumer electronics, automotive LiDAR, and data communications. Investments in photonic integrated circuit development have exceeded $2 billion annually, with major semiconductor companies entering the field through acquisitions and partnerships. This technological shift enables modulator performance previously available only in discrete devices to be integrated alongside electronic components, opening applications in 5G infrastructure, autonomous vehicles, and artificial intelligence acceleration where size, power consumption, and cost constraints previously limited adoption.

Advancements in Material Science and Fabrication Techniques to Unlock New Performance Capabilities

Breakthroughs in material science—particularly involving thin-film lithium niobate, organic electro-optic materials, and heterogeneous integration—are creating opportunities for modulators with significantly improved performance characteristics. These advancements enable devices with bandwidths exceeding 100 GHz, reduced drive voltages below 1V, and improved linearity for advanced modulation formats. Meanwhile, novel fabrication techniques including wafer bonding, direct writing, and self-assembly processes promise to reduce manufacturing costs while improving yield rates. The commercialization of these technologies could expand the addressable market for electro-optic modulators into applications currently served by alternative technologies, while simultaneously enabling new capabilities in existing applications such as coherent communications and optical signal processing.

ELECTRO-OPTIC MODULATORS (EOM) MARKET TRENDS

Demand Surge in Optical Telecommunications Drives Market Expansion

The global electro-optic modulators market is experiencing robust growth, primarily fueled by escalating demand within the optical telecommunications sector. As data traffic continues to explode, projected to exceed 4.8 zettabytes annually by 2028, network infrastructure requires increasingly sophisticated components for high-speed data transmission. EOMs are critical for encoding electrical signals onto optical carriers, enabling the high-bandwidth capabilities essential for 5G backhaul, data centers, and fiber-to-the-home (FTTH) deployments. The shift towards higher modulation formats like 16-QAM and 64-QAM to maximize spectral efficiency further intensifies the need for precise, high-performance modulators. This trend is particularly pronounced in North America, which commands approximately 33% of the global market share, driven by substantial investments in telecommunications infrastructure and early adoption of next-generation technologies.

Other Trends

Technological Advancements in High-Frequency and Broadband Modulators

Continuous innovation is a hallmark of the EOM landscape, with significant R&D focused on developing devices capable of operating at higher frequencies and broader bandwidths. Manufacturers are pushing the boundaries to achieve modulation speeds exceeding 40 GHz and bandwidths covering multiple octaves to meet the demands of advanced scientific research, military applications, and quantum computing systems. The integration of novel materials like thin-film lithium niobate (TFLN) is a key development, offering superior performance characteristics compared to traditional bulk crystals. This material advancement enables the production of modulators with lower half-wave voltages, reduced device footprints, and enhanced thermal stability, making them ideal for integrated photonic circuits. These technological leaps are crucial for applications requiring extreme precision, such as gravitational wave detection and optical atomic clocks.

Expansion in Defense and Space Applications Creates New Opportunities

The defense and aerospace sectors represent a rapidly growing application segment for electro-optic modulators, anticipated to be one of the fastest-growing areas during the forecast period. These industries utilize EOMs in critical systems including LiDAR (Light Detection and Ranging), free-space optical communication (FSOC), electronic warfare, and remote sensing. The unique ability of EOMs to provide high-speed, jitter-free control of laser beams makes them indispensable for target designation, rangefinding, and secure communications. Global defense spending, which surpassed 2.2 trillion U.S. dollars recently, directly fuels procurement of advanced electro-optical systems. Furthermore, the burgeoning space economy, with increased satellite deployments for Earth observation and deep-space communication, relies heavily on robust and radiation-hardened optical modulators to ensure signal integrity in harsh environments, presenting a sustained growth avenue for market players.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Positioning Drive Market Leadership

The global Electro-Optic Modulators (EOM) market exhibits a semi-consolidated structure, characterized by the presence of a few dominant players alongside several specialized medium and small-sized companies. This landscape is shaped by high technical barriers to entry, which necessitate significant expertise in materials science and photonics engineering. Market leadership is primarily determined by a company’s ability to deliver high-performance, reliable modulators across a diverse range of wavelengths and applications, from telecommunications to defense.

Thorlabs Inc. stands as a preeminent force in the market, commanding a significant portion of the global revenue share. Its dominance is largely attributable to its extensive and vertically integrated product portfolio, which spans basic amplitude modulators to sophisticated broadband and fiber-coupled devices. The company’s robust direct-to-customer sales model and strong distribution network across North America and Europe further cement its leading position, enabling it to serve both research institutions and industrial clients effectively.

Similarly, Jenoptik AG and iXblue (now part of Exail) are other major contenders, collectively accounting for a substantial market share. Jenoptik’s strength lies in its industrial-grade solutions and long-standing relationships with clients in the automotive and manufacturing sectors, particularly in Europe. iXblue, renowned for its advanced lithium niobate modulators, has carved a niche in high-demand applications like quantum technologies and undersea fiber-optic communications, leveraging its deep material science capabilities.

Beyond the top tier, companies are aggressively pursuing growth through innovation and strategic expansion. For instance, Conoptics Inc. and QUBIG GmbH are strengthening their market presence by focusing on specialized, high-frequency modulators crucial for scientific research applications. Their strategy involves significant investment in R&D to push the boundaries of modulation bandwidth and low-drift performance, which are critical parameters for next-generation experiments in physics and metrology.

Meanwhile, players like EOSPACE Inc. and AdvR Inc. are capitalizing on the burgeoning demand in the aerospace and defense sectors. Their growth is fueled by strategic partnerships with defense contractors and investments in developing radiation-hardened and ruggedized modulators capable of operating in extreme environments. This focus on high-reliability applications ensures their continued relevance and growth within a highly competitive landscape.

List of Key Electro-Optic Modulator (EOM) Companies Profiled

- Thorlabs Inc. (U.S.)

- Jenoptik AG (Germany)

- iXblue (Exail) (France)

- EOSPACE Inc. (U.S.)

- AdvR Inc. (U.S.)

- Conoptics Inc. (U.S.)

- QUBIG GmbH (Germany)

- Agiltron Inc. (Photonwares) (U.S.)

- A.P.E Angewandte Physik & Elektronik GmbH (Germany)

- Keyang Photonics Co., Ltd. (China)

Segment Analysis:

By Type

Phase Modulators Segment Leads Due to Critical Role in High-Speed Optical Communication Systems

The market is segmented based on type into:

- Phase Modulators

- Amplitude Modulators

- Polarization Modulators

- Others

By Application

Optical Telecommunications Segment Dominates Owing to Massive Demand for High-Bandwidth Data Transmission

The market is segmented based on application into:

- Optical Telecommunications

- Space and Defense Applications

- Fiber Optics Sensors

- Instrument and Industrial Systems

- Others

By End User

Telecom Service Providers Hold Largest Share Fueled by 5G and Fiber Optic Network Expansion

The market is segmented based on end user into:

- Telecom Service Providers

- Defense and Aerospace Organizations

- Research and Academic Institutions

- Industrial Manufacturing

- Others

Regional Analysis: Electro-Optic Modulators (EOM) Market

North America

North America is the dominant force in the global Electro-Optic Modulators market, holding the largest market share at approximately 33% and serving as the largest production hub with a 46% share. This leadership is anchored by the United States, which hosts major industry players like Thorlabs and Conoptics. The region’s advanced technological infrastructure and substantial investment in research and development, particularly from the defense and telecommunications sectors, are primary growth drivers. The U.S. Department of Defense’s continued prioritization of photonics and laser technologies for applications in sensing, communications, and directed energy systems creates a steady, high-value demand for sophisticated EOMs. Furthermore, the robust optical telecommunications network, essential for data centers and high-speed internet infrastructure, relies heavily on these components for signal modulation. While the market is mature, innovation focuses on developing higher bandwidth modulators and more compact, integrated designs to meet the evolving needs of quantum computing research and next-generation optical networks.

Europe

Europe represents a significant and technologically advanced market, accounting for roughly 27% of global consumption. The region is characterized by a strong manufacturing base, with key contributors like Germany’s Jenoptik and France’s iXblue leading innovation. Market growth is heavily influenced by stringent EU regulations and funding initiatives that promote technological sovereignty and advanced manufacturing, particularly in photonics. Applications in industrial laser systems for precision manufacturing, automotive LiDAR, and scientific research instruments are major demand drivers. European entities are also at the forefront of developing EOMs for space and defense applications, requiring components that meet extreme reliability and performance standards. Collaboration between academia, research institutes like the Max Planck Society, and industry fosters a continuous pipeline of innovation, ensuring Europe remains a critical center for high-performance, specialized electro-optic modulators.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for Electro-Optic Modulators, propelled by its massive electronics manufacturing and telecommunications expansion. China is the undeniable epicenter of this growth, representing about 17% of the global market and housing producers like Keyang Photonics. The country’s national strategies, such as “Made in China 2025,” which emphasizes advanced photonics, are accelerating domestic production and adoption. While the region has a significant volume share, the market is notably bifurcated. There is strong demand for cost-competitive modulators from the vast consumer electronics and industrial sectors. Simultaneously, there is rapidly growing investment from Japan, South Korea, and China in high-end applications, including quantum technology research and next-generation optical communication networks, creating a parallel demand for premium, high-performance devices.

South America

The South American market for Electro-Optic Modulators is nascent but presents identifiable long-term opportunities. Current demand is primarily concentrated in academic and research institutions in countries like Brazil and Argentina, which utilize EOMs for scientific experiments and developing local technological capabilities. The limited industrial manufacturing base for high-tech optics means the market is almost entirely import-dependent, with key suppliers from North America and Europe dominating. Growth is constrained by economic volatility, which impacts funding for research and capital expenditure on advanced equipment. However, gradual infrastructure modernization, particularly in telecommunications, and a growing awareness of photonics’ potential in agriculture and natural resource management are slowly introducing new application areas, suggesting a path for future, albeit measured, market development.

Middle East & Africa

The market in the Middle East & Africa is in its very early stages of development. Activity is primarily isolated to a few key nations, notably Israel, a recognized global tech hub with expertise in defense and aerospace applications that utilize EOM technology. Saudi Arabia and the UAE are also making strategic investments in diversifying their economies through technology and innovation cities, which could eventually stimulate demand for photonic components. However, across most of the region, the lack of a local manufacturing base, limited industrial R&D expenditure, and a small number of end-use industries that require such specialized components result in minimal current market penetration. Growth is expected to be slow and tied to specific government-led technology initiatives rather than organic industrial demand.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Electro-Optic Modulators (EOM) market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electro-Optic Modulators (EOM) Market?

-> Electro-Optic Modulators (EOM) Market was valued at 189 million in 2024 and is projected to reach US$ 284 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in Global Electro-Optic Modulators (EOM) Market?

-> Key players include Thorlabs, Jenoptik, iXblue, EOSPACE, AdvR, Conoptics, QUBIG GmbH, Agiltron (Photonwares), A.P.E, and Keyang Photonics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand in optical telecommunications, expansion of fiber optics sensors, and growing applications in space and defense sectors.

Which region dominates the market?

-> North America is the largest market, holding a share of approximately 33%, followed by Europe and China with shares of 27% and 17%, respectively.

What are the emerging trends?

-> Emerging trends include miniaturization of devices, integration with quantum computing systems, and advancements in high-speed modulation technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...