Electrical Cable Conduits (Only Metal Made) Market MARKET INSIGHTS

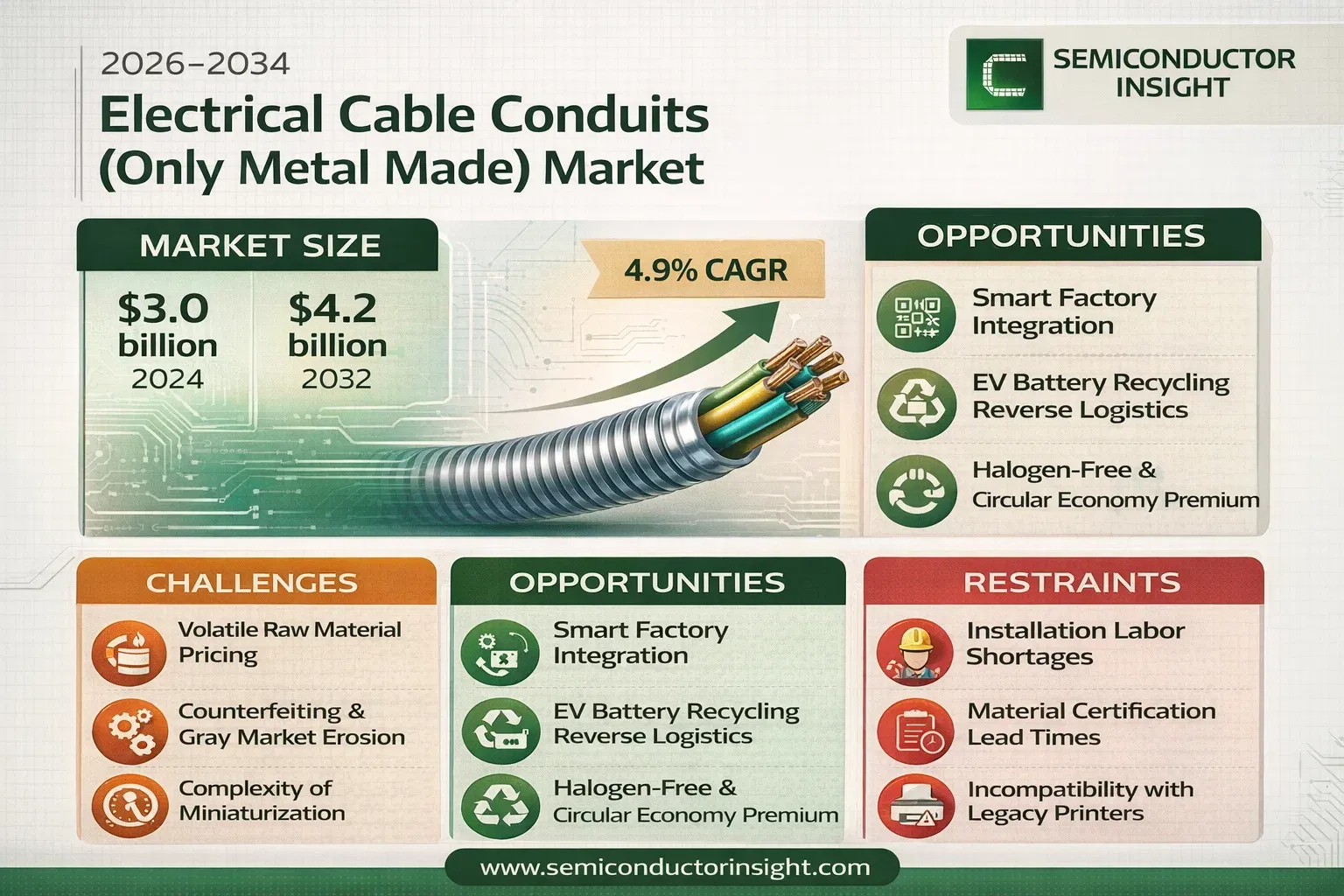

Global Electrical Cable Conduits (Only Metal Made) Market was valued at 3046 million in 2024 and is projected to reach USD 4217 million by 2032, at a CAGR of 4.9% during the forecast period.

An electrical conduit is a tube used to protect and route electrical wiring in a building or nonbuilding structure. While conduits can be made from various materials, metal conduits are specialized rigid or flexible tubes, typically manufactured from steel or aluminum, that provide superior mechanical protection, electromagnetic shielding, and fire resistance for electrical cables. These systems are crucial for ensuring safety and compliance with stringent electrical codes in industrial and commercial applications.

The market is experiencing steady growth driven by several factors, including global infrastructure development, increased investment in industrial automation, and stringent safety regulations mandating the use of robust cable management systems. Furthermore, the rising demand for energy and utility projects, coupled with the expansion of data centers and telecommunications infrastructure, is contributing to market expansion. The market is highly concentrated, with the top three players Atkore, ABB, and Legrand collectively holding approximately 75% of Global market share, indicating a mature and competitive landscape.

Electrical Cable Conduits (Only Metal Made) Market MARKET DYNAMICS

Electrical Cable Conduits (Only Metal Made) Market MARKET DRIVERS

Rising Investments in Infrastructure Development to Accelerate Market Expansion

Global Electrical Cable Conduits (Only Metal Made) Market is experiencing robust growth driven by substantial investments in infrastructure development across both developed and emerging economies. Government initiatives and private sector funding are fueling construction activities in residential, commercial, and industrial sectors, creating sustained demand for reliable electrical protection systems. The construction industry’s expansion, particularly in smart city projects and industrial corridors, requires advanced electrical infrastructure where metal conduits provide superior mechanical protection, electromagnetic shielding, and fire resistance compared to alternative materials. Major infrastructure projects worldwide are incorporating metal conduits as standard components in electrical installations, ensuring long-term durability and safety compliance in demanding environments.

Increasing Emphasis on Electrical Safety Standards to Boost Market Growth

Stringent electrical safety regulations and building codes are significantly driving the adoption of metal electrical conduits globally. Regulatory bodies and industry standards organizations are mandating enhanced protection measures for electrical wiring systems, particularly in hazardous environments and high-risk applications. Metal conduits offer superior protection against physical damage, moisture, corrosion, and electromagnetic interference, making them essential for compliance with safety requirements. The growing awareness of electrical fire hazards and the need for robust wiring protection systems in industrial facilities, commercial buildings, and critical infrastructure projects are compelling specifiers and contractors to prefer metal conduits over plastic alternatives. This heightened focus on safety compliance is creating sustained demand across various end-use sectors.

Furthermore, the implementation of international electrical standards and certification requirements is reinforcing market growth. These standards mandate specific performance characteristics that metal conduits consistently meet, ensuring reliable operation in diverse environmental conditions.

The convergence of regulatory requirements with technological advancements in conduit manufacturing is creating additional growth opportunities, as manufacturers develop products that exceed minimum compliance standards while offering improved installation efficiency and longevity.

MARKET CHALLENGES

Volatility in Raw Material Prices to Challenge Market Stability

Electrical Cable Conduits (Only Metal Made) Market faces significant challenges from fluctuating raw material prices, particularly steel and aluminum, which constitute the primary manufacturing inputs. Price volatility in these commodities directly impacts production costs and profit margins for conduit manufacturers. Market dynamics such as trade policies, supply chain disruptions, and global economic conditions create uncertainty in material pricing, making long-term planning and cost management increasingly difficult. These fluctuations can lead to inconsistent product pricing, affecting project budgeting and procurement decisions across the construction and electrical industries.

Other Challenges

Intense Competition from Alternative Materials

The market faces growing competition from non-metallic conduit materials, particularly advanced plastics and composite solutions. These alternatives offer advantages in corrosion resistance, installation flexibility, and cost-effectiveness in certain applications. While metal conduits maintain superiority in mechanical protection and fire resistance, the continuous improvement in plastic conduit performance characteristics is eroding metal conduit market share in price-sensitive segments and less demanding applications.

Installation Complexity and Labor Costs

The installation of metal conduits requires specialized skills and tools compared to alternative materials, contributing to higher labor costs and longer installation times. The need for bending, threading, and proper grounding techniques demands trained electricians, while the physical weight of metal conduits adds to handling challenges. These factors can deter contractors from specifying metal conduits in projects where installation efficiency and cost containment are primary considerations.

Electrical Cable Conduits (Only Metal Made) Market MARKET RESTRAINTS

Environmental Regulations and Sustainability Concerns to Limit Market Growth

Environmental considerations and sustainability mandates are increasingly restraining the metal electrical conduits market. Manufacturing processes for metal conduits involve significant energy consumption and carbon emissions, drawing attention from regulatory bodies and environmentally conscious specifiers. The industry faces pressure to adopt greener manufacturing practices and reduce the environmental footprint of metal conduit production. Additionally, end-of-life disposal considerations and recycling requirements add complexity to the product lifecycle management.

Stricter environmental regulations governing industrial emissions and waste management are compelling manufacturers to invest in cleaner production technologies and sustainable material sourcing. These compliance requirements increase operational costs and may affect product pricing competitiveness. The growing preference for sustainable building materials in green construction projects also disadvantages metal conduits compared to recyclable plastic alternatives in certain applications where environmental credentials outweigh performance advantages.

Furthermore, corrosion protection treatments and coatings used in metal conduits face increasing regulatory scrutiny regarding chemical content and environmental impact. Compliance with evolving chemical regulations requires continuous product reformulation and testing, adding to development costs and time-to-market for new products.

Electrical Cable Conduits (Only Metal Made) Market MARKET OPPORTUNITIES

Expansion in Renewable Energy Infrastructure to Create New Growth Avenues

The rapid global expansion of renewable energy infrastructure presents significant opportunities for metal electrical conduits market growth. Solar farms, wind energy facilities, and energy storage installations require robust electrical protection systems that can withstand harsh environmental conditions and provide long-term reliability. Metal conduits offer essential protection for critical electrical connections in renewable energy applications, where exposure to weather elements, UV radiation, and mechanical stresses demands superior durability.

The transition toward clean energy is driving substantial investments in grid modernization and distributed energy resources, creating sustained demand for high-performance electrical infrastructure components. Metal conduits are increasingly specified in these applications due to their ability to protect sensitive control and power cables from environmental factors and electromagnetic interference. The growing emphasis on grid resilience and reliability in renewable energy integration further supports metal conduit adoption in utility-scale projects and distributed generation installations.

Additionally, government incentives and policy support for renewable energy development are accelerating project timelines and expanding market scope. The alignment of metal conduit performance characteristics with the demanding requirements of renewable energy infrastructure positions the market for continued growth as global energy transition initiatives gain momentum.

ELECTRICAL CABLE CONDUITS (ONLY METAL MADE) MARKET TRENDS

Rising Infrastructure Investments and Industrial Automation Drive Global Demand

Global Electrical Cable Conduits (Only Metal Made) Market is experiencing robust growth, primarily fueled by massive infrastructure development projects and the accelerating adoption of industrial automation worldwide. Global construction spending is projected to reach approximately D 15.2 trillion annually by 2025, creating substantial demand for robust electrical protection systems. Concurrently, the industrial automation market is expanding at a CAGR of nearly 9%, necessitating advanced wiring solutions in manufacturing facilities. Metal conduits, particularly rigid variants which command over 70% market share, are preferred for their superior mechanical protection, electromagnetic shielding, and fire resistance properties compared to non-metallic alternatives. This trend is most pronounced in the industrial manufacturing sector, which represents the largest application segment, as factories modernize their electrical systems to support smart manufacturing and Industry 4.0 initiatives.

Other Trends

Stringent Safety Regulations and Building Codes

Governments and international standards bodies are increasingly mandating stricter electrical safety protocols, which is a significant market driver. Regulations such as the National Electrical Code (NEC) in the United States and the International Electrotechnical Commission (IEC) standards globally often specify or strongly recommend the use of metal conduits in commercial, industrial, and multi-residential buildings for enhanced fire safety and mechanical protection. This regulatory push is compelling architects, engineers, and contractors to specify metal conduit systems, especially in high-risk environments like energy plants, data centers, and transportation hubs. The emphasis on improving resilience against natural disasters and mitigating electrical fire risks continues to solidify the position of metal conduits as a critical component in modern electrical installations.

Material Innovation and Product Development

While the core material remains metal, manufacturers are heavily investing in product innovation to enhance performance, ease of installation, and corrosion resistance. The development of lighter, more durable aluminum alloys and advanced coated steel conduits addresses challenges related to weight and installation in corrosive environments, such as chemical plants or coastal areas. Furthermore, there is a growing trend towards pre-fabricated conduit systems that reduce on-site labor time and costs, a crucial factor given Global shortage of skilled electricians. These innovations are not only improving the functional attributes of the products but are also expanding their application scope into new areas like offshore wind farms and solar power installations, where environmental durability is paramount.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Leverage Innovation and Global Reach to Maintain Market Dominance

Global Electrical Cable Conduits (Only Metal Made) Market is characterized by a semi-consolidated structure, featuring a mix of multinational giants, specialized mid-tier firms, and regional suppliers. This dynamic creates a competitive environment where scale, product innovation, and geographic penetration are critical for success. The market’s top three players collectively command a significant portion of global sales, estimated at approximately 75% of the total market share, underscoring the influence of these key entities.

Atkore International stands as a dominant force in this sector. Its leadership is largely attributed to an extensive and diversified product portfolio that includes a wide range of rigid and flexible metal conduits, coupled with a formidable manufacturing and distribution network primarily concentrated in North America. The company’s strategic focus on serving the robust industrial manufacturing and energy utility sectors has solidified its top position.

Similarly, ABB Ltd. and Legrand hold considerable market shares, leveraging their strong brand recognition and global operational footprints. ABB’s strength is deeply rooted in its comprehensive electrification solutions, where metal conduits are a critical component, especially for large-scale infrastructure and industrial projects. Legrand, on the other hand, capitalizes on its strong presence in building infrastructure across Europe and North America, offering specialized conduit systems tailored for commercial and residential applications.

Beyond the top three, companies like Schneider Electric and Calpipe Industries are actively strengthening their positions. They are pursuing aggressive growth strategies centered on research and development to introduce more durable and corrosion-resistant products, alongside strategic acquisitions to expand their geographical reach and customer base. These initiatives are crucial for capturing market share in emerging economies and high-growth application segments.

Meanwhile, other players such as ANAMET ELECTRICAL, Inc. and Wheatland Tube Company compete effectively by specializing in niche applications or by offering highly cost-competitive products. Their growth is often driven by deep relationships with regional distributors and a focus on meeting specific technical standards required in different geographic markets, such as those for extreme environments or hazardous locations.

List of Key Companies Profiled in the Metal Electrical Cable Conduits Market

- Atkore International Group Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Legrand S.A. (France)

- Schneider Electric SE (France)

- Calpipe Industries, Inc. (U.S.)

- Barton Engineering (U.K.)

- ZJK (China)

- ANAMET ELECTRICAL, Inc. (U.S.)

- Wheatland Tube Company (U.S.)

- Kingland & Pipeline (China)

Segment Analysis:

By Type

Rigid Conduits Segment Dominates the Market Due to Superior Mechanical Protection and Durability

The market is segmented based on type into:

- Rigid Metal Conduit (RMC)

- Intermediate Metal Conduit (IMC)

- Electrical Metallic Tubing (EMT)

- Flexible Metal Conduit (FMC)

- Liquidtight Flexible Metal Conduit (LFMC)

By Application

Industrial Manufacturing Segment Leads Due to High Demand for Robust Electrical Infrastructure

The market is segmented based on application into:

- Industrial Manufacturing

- Energy and Utility

- IT and Telecommunications

- Transportation

- Commercial Construction

By End User

Commercial and Industrial Sectors Drive Demand Owing to Stringent Safety Regulations and Infrastructure Development

The market is segmented based on end user into:

- Industrial

- Commercial

- Residential

- Utility and Infrastructure

By Material

Galvanized Steel Conduits Hold Major Share Due to Excellent Corrosion Resistance and Longevity

The market is segmented based on material into:

- Galvanized Steel

- Stainless Steel

- Aluminum

- Copper

Regional Analysis: Electrical Cable Conduits (Only Metal Made) Market

North America

The North American market is characterized by robust demand driven by stringent building codes, such as the National Electrical Code (NEC), which mandate the use of high-quality, durable metal conduits for safety and fire protection. Significant investments in infrastructure modernization, including the D 1.2 trillion Infrastructure Investment and Jobs Act, are fueling demand across commercial construction, data centers, and industrial projects. The region’s mature manufacturing sector and the push for grid modernization in the energy sector further support steady consumption. Major players like Atkore and Calpipe have a strong presence, leveraging advanced manufacturing to supply galvanized steel and aluminum conduits that meet rigorous standards for corrosion resistance and mechanical protection.

Europe

Europe represents a key market where strict regulatory standards and a focus on quality and sustainability drive adoption. EU directives and national regulations emphasize the use of metal conduits for their superior mechanical strength, electromagnetic shielding capabilities, and recyclability. The ongoing renovation of aging infrastructure, particularly in Germany, France, and the UK, alongside investments in renewable energy projects and smart building technologies, creates consistent demand. The market is highly competitive, with leading companies like Legrand, ABB, and Schneider Electric offering innovative, compliant solutions. However, high material costs and a competitive landscape with numerous local fabricators present challenges for market expansion.

Asia-Pacific

The Asia-Pacific region is the largest and fastest-growing market globally, accounting for a dominant share of volume consumption. This growth is propelled by massive urbanization, extensive infrastructure development, and rapid industrialization, particularly in China and India. Government initiatives, such as China’s Belt and Road Initiative and India’s Smart Cities Mission, require vast quantities of reliable electrical infrastructure, including metal conduits. While cost sensitivity leads to significant use of alternative materials like PVC, the need for superior protection in industrial, energy, and transportation applications ensures strong demand for metal variants. Local manufacturing is strong, but international players compete by establishing production facilities and partnerships within the region.

South America

The South American market is in a developmental phase, with growth opportunities tied to gradual infrastructure expansion and industrial projects in countries like Brazil and Argentina. Economic volatility and fluctuating investment in construction have historically led to an inconsistent demand pattern. The market is price-sensitive, often favoring lower-cost alternatives, but metal conduits maintain a crucial position in mining, oil & gas, and heavy industrial applications where durability is non-negotiable. The lack of stringent, uniformly enforced electrical codes across the region can hinder the widespread adoption of premium metal conduit systems, making market penetration a challenge for international suppliers.

Middle East & Africa

This region presents an emerging market with potential driven by large-scale construction, urban development, and energy projects, particularly in the Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE. The extreme environmental conditions and requirements for durable, long-lasting infrastructure in oil & gas and construction favor the use of robust metal conduits. However, market growth is often constrained by budget limitations, economic diversification efforts, and a reliance on imported products, which can affect supply chain stability and final costs. While demand is rising, the pace of adoption is slower compared to more developed regions, presenting a long-term growth opportunity.

Report Scope

This market research report provides a comprehensive analysis of Global and regional Electrical Cable Conduits (Only Metal Made) Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging manufacturing techniques, corrosion-resistant coatings, and evolving industry standards for metal conduits.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for raw material suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electrical Cable Conduits (Only Metal Made) Market?

-> Electrical Cable Conduits (Only Metal Made) Market was valued at 3046 million in 2024 and is projected to reach USD 4217 million by 2032, at a CAGR of 4.9% during the forecast period..

Which key companies operate in Global Electrical Cable Conduits (Only Metal Made) Market?

-> Key players include Atkore, ABB, Legrand, Schneider Electric, Calpipe, Barton Engineering, ZJK, ANAMET ELECTRICAL, Wheatland, and Kingland & Pipeline, among others.

What are the key growth drivers?

-> Key growth drivers include increasing infrastructure development, rising demand from industrial manufacturing, and stringent safety regulations requiring robust cable protection systems.

Which region dominates the market?

-> North America and Europe collectively hold approximately 50% of Global market share, with both regions offering strong growth prospects.

What are the emerging trends?

-> Emerging trends include development of lightweight yet durable metal alloys, increased adoption of corrosion-resistant coatings, and integration of smart monitoring systems in conduit installations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...