MARKET INSIGHTS

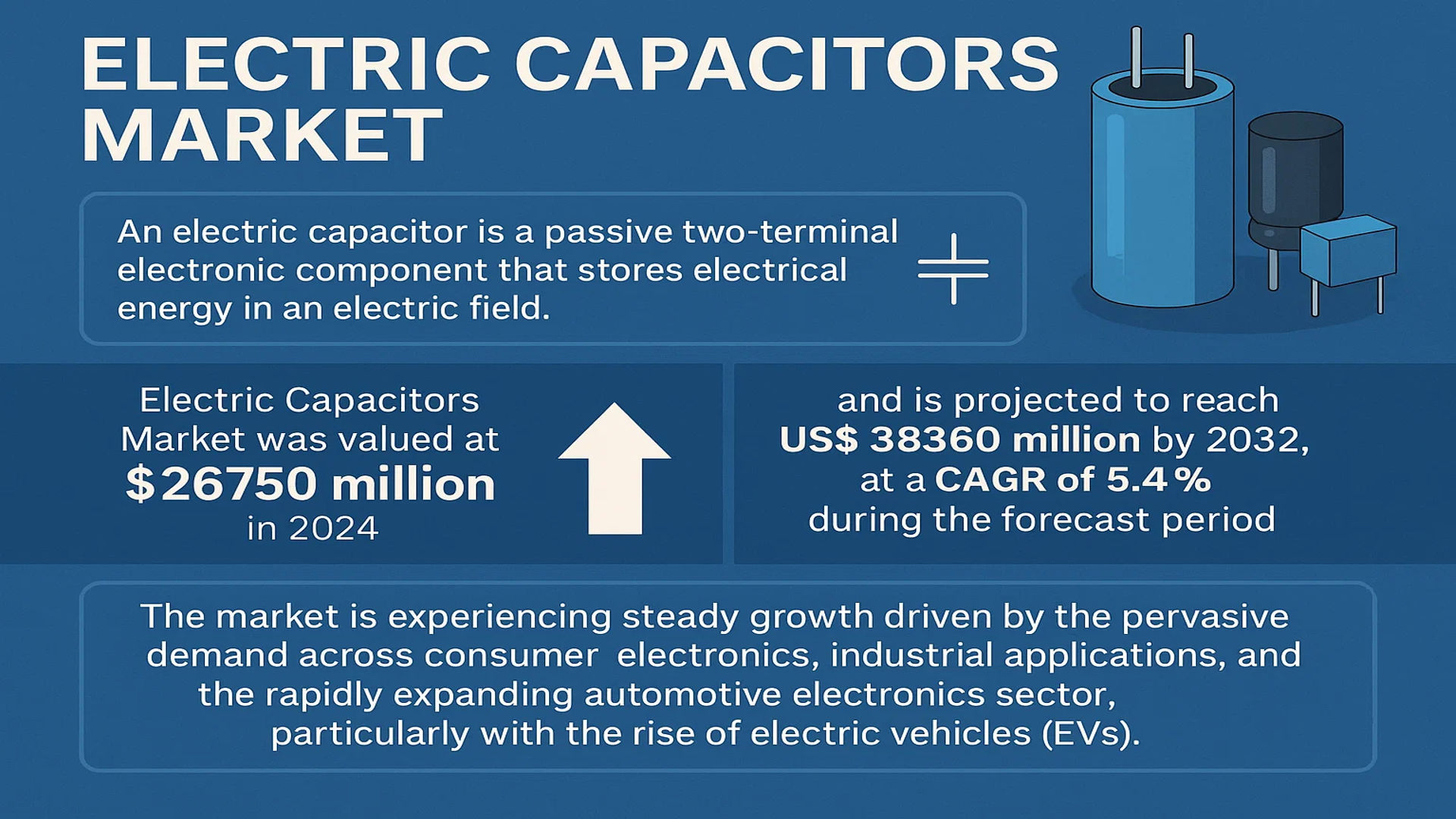

The global Electric Capacitors Market was valued at 26750 million in 2024 and is projected to reach US$ 38360 million by 2032, at a CAGR of 5.4% during the forecast period.

An electric capacitor is a passive two-terminal electronic component that stores electrical energy in an electric field. It consists of two conductive plates separated by an insulating material called a dielectric. When connected to a power source, one plate accumulates a positive charge while the other accumulates a negative charge, enabling the capacitor to store and release energy as needed in a circuit.

The market is experiencing steady growth driven by the pervasive demand across consumer electronics, industrial applications, and the rapidly expanding automotive electronics sector, particularly with the rise of electric vehicles (EVs). Furthermore, the ongoing global push for renewable energy integration and grid modernization is fueling demand for capacitors in power systems and energy storage applications. China dominates as the largest consumption market, holding approximately 40% of the global share, due to its massive electronics manufacturing base. Key players such as Murata, KYOCERA, and TDK lead the market with extensive product portfolios and continuous innovation in miniaturization and performance.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Consumer Electronics and IoT Devices to Drive Market Expansion

The global electric capacitors market is experiencing robust growth driven by the widespread adoption of consumer electronics and Internet of Things (IoT) devices. The consumer electronics segment, which accounts for over 40% of market share, continues to expand with increasing demand for smartphones, laptops, wearables, and smart home devices. The IoT ecosystem, projected to connect over 29 billion devices by 2030, requires substantial capacitor integration for power management, signal conditioning, and energy storage applications. This surge is particularly evident in Asia-Pacific, where manufacturing hubs in China, Japan, and South Korea produce approximately 65% of global electronic components. The continuous miniaturization of electronic devices while maintaining performance standards further accelerates the need for advanced capacitor technologies with higher capacitance values and smaller form factors.

Renewable Energy and Electric Vehicle Adoption to Accelerate Market Growth

The global transition toward renewable energy and electric mobility represents a significant growth driver for the electric capacitors market. The renewable energy sector, particularly solar and wind power installations, requires extensive capacitor deployment for power conditioning, energy storage, and grid stability applications. With global renewable energy capacity expected to reach 4,500 GW by 2030, the demand for high-performance capacitors in inverters, converters, and energy storage systems continues to escalate. Simultaneously, the electric vehicle market, projected to reach 45 million annual sales by 2030, utilizes capacitors extensively in power electronics, battery management systems, and charging infrastructure. The automotive segment’s capacitor requirements are particularly demanding, needing components that can withstand high temperatures, vibrations, and rigorous performance standards while maintaining reliability over extended operational lifetimes.

5G Infrastructure Deployment and Industrial Automation to Fuel Demand

The global rollout of 5G networks and increasing industrial automation investments are creating substantial opportunities for capacitor manufacturers. 5G infrastructure requires advanced capacitors for base stations, network equipment, and communication devices, with the market for 5G infrastructure components projected to exceed $50 billion annually by 2025. These applications demand capacitors with high frequency characteristics, low equivalent series resistance, and excellent temperature stability. Concurrently, Industry 4.0 initiatives are driving capacitor demand in industrial automation, robotics, and smart manufacturing systems. The industrial segment, representing approximately 25% of the capacitor market, requires components that can operate reliably in harsh environments while providing precise performance characteristics for motor drives, power supplies, and control systems.

MARKET RESTRAINTS

Raw Material Price Volatility and Supply Chain Disruptions to Constrain Market Growth

The electric capacitors market faces significant challenges from raw material price fluctuations and supply chain vulnerabilities. Capacitor manufacturing relies on critical materials including rare earth elements, aluminum, tantalum, and specialty ceramics, all subject to price volatility and supply constraints. The tantalum market, essential for high-performance capacitors, experiences periodic supply disruptions due to geopolitical factors and mining challenges, with prices fluctuating by up to 35% annually. Similarly, nickel and copper prices have shown volatility of 20-30% in recent years, directly impacting production costs. The COVID-19 pandemic further exposed supply chain weaknesses, with capacitor lead times extending from typical 8-12 weeks to 20-30 weeks during peak disruptions. These factors create pricing pressure and availability challenges, particularly for small and medium-sized manufacturers lacking long-term supply agreements.

Technical Limitations in Miniaturization and Performance to Hinder Market Advancement

While consumer electronics demand continues to drive miniaturization, capacitor technology faces fundamental physical limitations that restrain further size reduction while maintaining performance characteristics. The relationship between capacitance value, voltage rating, and physical size presents engineering challenges, particularly for applications requiring high capacitance in compact form factors. Ceramic capacitors, representing over 45% of the market, encounter limitations in dielectric constant stability and piezoelectric effects at smaller dimensions. Similarly, electrolytic capacitors face challenges in achieving higher temperature ratings and longer operational lifetimes in reduced packages. These technical constraints become increasingly critical as electronic devices push toward thinner profiles and higher power densities, requiring capacitor manufacturers to invest significantly in research and development to overcome these physical barriers while maintaining cost competitiveness.

Environmental Regulations and Recycling Challenges to Impact Market Dynamics

Stringent environmental regulations and recycling challenges present substantial restraints for the electric capacitors market. The Restriction of Hazardous Substances (RoHS) directive and similar regulations worldwide limit the use of certain materials in electronic components, requiring manufacturers to reformulate products and invest in alternative technologies. Capacitors containing hazardous materials face disposal and recycling challenges, with recovery rates for valuable materials remaining below 30% in most regions. The European Union’s Circular Economy Action Plan and similar initiatives globally are pushing manufacturers toward extended producer responsibility, increasing compliance costs and operational complexity. Additionally, the industry faces pressure to reduce carbon footprint throughout the manufacturing process, particularly energy-intensive production methods for certain capacitor types, adding further cost pressures and operational constraints.

MARKET CHALLENGES

Intense Price Competition and Margin Pressure to Challenge Market Sustainability

The electric capacitors market experiences intense price competition, particularly in standardized product categories, creating significant margin pressure for manufacturers. The industry’s competitive landscape includes numerous global players and regional manufacturers, leading to price-based competition that erodes profitability. Average selling prices for multilayer ceramic capacitors have declined by approximately 5-7% annually despite increasing technical requirements, while electrolytic capacitor prices have shown similar downward trends. This price erosion occurs while raw material and manufacturing costs continue to rise, squeezing profit margins across the industry. The challenge is particularly acute for medium-sized manufacturers lacking the scale advantages of market leaders, forcing consolidation through mergers and acquisitions as companies seek operational efficiencies and broader product portfolios to maintain competitiveness.

Other Challenges

Technology Transition Risks

Rapid technological evolution presents challenges in product lifecycle management and inventory risk. The transition to new capacitor technologies and materials requires significant capital investment while existing product lines face obsolescence risk. Manufacturers must balance investment in emerging technologies with maintaining profitability from established products, creating strategic challenges in resource allocation and technology roadmap development.

Quality Consistency and Reliability Demands

Increasing reliability requirements across automotive, industrial, and medical applications demand exceptional quality consistency that challenges manufacturing processes. Automotive-grade capacitors require failure rates below 1 part per million and operational lifetimes exceeding 15 years, creating stringent production and testing requirements that increase manufacturing complexity and cost while maintaining competitive pricing.

MARKET OPPORTUNITIES

Emerging Applications in Medical Electronics and Aerospace to Create New Growth Avenues

The medical electronics and aerospace sectors present significant growth opportunities for advanced capacitor technologies. The medical device market, projected to reach $600 billion by 2025, requires capacitors with exceptional reliability, miniaturization, and biocompatibility for applications including implantable devices, diagnostic equipment, and monitoring systems. These applications demand capacitors with ultra-high reliability, often requiring operational lifetimes exceeding 10 years with failure rates below 0.1 parts per million. Similarly, the aerospace and defense sector requires components that can withstand extreme environmental conditions, radiation hardness, and extended operational lifetimes. The commercial aerospace market’s recovery and increased defense spending worldwide create opportunities for capacitors meeting MIL-SPEC and space-grade requirements, representing premium market segments with higher margins and specialized technical requirements.

Advanced Research in Supercapacitors and Hybrid Solutions to Enable New Applications

Ongoing research and development in supercapacitors and hybrid energy storage solutions creates substantial opportunities for market expansion. Supercapacitors, offering power densities orders of magnitude higher than traditional batteries and capacitors, find increasing applications in energy harvesting, peak power support, and rapid cycling applications. The global supercapacitor market is projected to grow at over 15% annually, driven by applications in renewable energy systems, electric vehicles, and industrial power management. Hybrid solutions combining battery and capacitor technologies offer optimized performance characteristics for specific applications, particularly in automotive start-stop systems, renewable energy smoothing, and uninterruptible power supplies. These advanced technologies command premium pricing and require specialized manufacturing capabilities, creating opportunities for companies with strong research and development resources and intellectual property portfolios.

Strategic Partnerships and Vertical Integration to Enhance Market Position

The evolving market landscape creates opportunities through strategic partnerships and vertical integration initiatives. Leading capacitor manufacturers are forming alliances with semiconductor companies, electronic design firms, and end-product manufacturers to develop integrated solutions that optimize system performance. These collaborations enable capacitor companies to move beyond component supply toward providing complete sub-system solutions, increasing value capture and customer stickiness. Simultaneously, vertical integration opportunities exist in raw material processing, advanced manufacturing equipment development, and recycling technologies. Companies investing backward integration into material processing can secure supply stability and cost advantages, while forward integration into module assembly and system integration creates additional revenue streams. The trend toward regionalization of supply chains further encourages local manufacturing and partnership development, particularly in North America and Europe where governments are incentivizing domestic electronic component production.

ELECTRIC CAPACITORS MARKET TRENDS

Miniaturization and High-Frequency Performance Driving Ceramic Capacitor Dominance

The relentless push towards smaller, more powerful electronic devices is profoundly shaping capacitor technology and market dynamics. Ceramic capacitors, which command over 45% of the global market share, are at the forefront of this trend due to their excellent high-frequency characteristics and suitability for surface-mount technology (SMT). This dominance is fueled by the consumer electronics sector, which accounts for the largest application segment. The proliferation of 5G infrastructure, which requires capacitors capable of operating at extremely high frequencies with minimal signal loss, has further accelerated demand for advanced multilayer ceramic chip capacitors (MLCCs). While this growth is robust, it is tempered by the complex manufacturing processes and supply chain vulnerabilities for certain rare-earth materials used in these components.

Other Trends

Electrification of Automotive Systems

The rapid transition towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is creating a substantial new demand vector for high-performance capacitors. These systems require robust components capable of handling high voltages, extreme temperatures, and significant power fluctuations. Film and aluminum electrolytic capacitors are seeing increased adoption in onboard chargers, inverters, and DC-DC converters. The global automotive electronics segment is projected to be one of the fastest-growing application areas, with estimates suggesting it could surpass a value of $8 billion by 2030. This growth is intrinsically linked to global EV sales, which surpassed 10 million units in 2022 and continue to climb, necessitating a parallel expansion in capacitor production and innovation.

Expansion in Renewable Energy and Industrial Automation

The global focus on energy transition and industrial modernization is significantly boosting demand for capacitors in the energy and industrial sectors. In renewable energy applications, such as solar inverters and wind turbine converters, capacitors are critical for power conditioning, filtering, and energy storage. Double-layer/super capacitors are gaining traction for their ability to provide high bursts of power and their long lifecycle, making them ideal for smoothing intermittent energy supply from renewable sources. Concurrently, the rise of Industry 4.0 and industrial IoT is driving the need for reliable capacitors in motor drives, power supplies, and control systems. This dual demand from energy and industrial automation is creating a stable, long-term growth driver that is less susceptible to the cyclicality of the consumer electronics market.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Leverage Innovation and Strategic Expansion to Dominate Market Share

The global electric capacitors market exhibits a semi-consolidated structure, characterized by intense competition among established multinational corporations, specialized manufacturers, and emerging regional players. Murata Manufacturing Co., Ltd. (Japan) stands as the undisputed market leader, commanding a significant revenue share. This dominance is primarily attributed to its extensive portfolio of ceramic capacitors, which hold over 45% of the total market, and its deeply entrenched supply relationships within the consumer electronics and automotive sectors globally.

TDK Corporation (Japan) and KYOCERA Corporation (Japan) also maintain formidable market positions, collectively holding a substantial portion of the global revenue. Their growth is fueled by continuous investment in R&D for miniaturization and high-capacitance solutions, which are critical for next-generation electronics like smartphones and electric vehicle power systems. Furthermore, their strong production foothold in Asia, the largest consumption region with a 40% market share, provides a distinct competitive advantage in terms of cost and supply chain efficiency.

Additionally, these industry titans are aggressively pursuing growth through geographical expansions, particularly into North America and Europe, and through a consistent pipeline of new product launches tailored for high-growth applications like renewable energy storage and automotive electronics. This strategic focus is expected to further solidify their market standing throughout the forecast period.

Meanwhile, other key players like Samsung Electro-Mechanics (South Korea) and Taiyo Yuden Co., Ltd. (Japan) are strengthening their global presence through significant capital expenditures in advanced manufacturing facilities and strategic partnerships with major OEMs. Companies such as Vishay Intertechnology, Inc. (U.S.) and KEMET (a part of Yageo Corporation, Taiwan) are focusing on portfolio diversification into tantalum and aluminum electrolytic capacitors to capture value in industrial and energy applications, ensuring robust and sustained competition across different capacitor segments.

List of Key Electric Capacitors Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- KYOCERA Corporation (Japan)

- Samsung Electro-Mechanics (South Korea)

- Taiyo Yuden Co., Ltd. (Japan)

- Nippon Chemi-Con Corporation (Japan)

- Panasonic Corporation (Japan)

- Nichicon Corporation (Japan)

- Rubycon Corporation (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Yageo Corporation (Taiwan)

Segment Analysis:

By Type

Ceramic Capacitor Segment Commands the Market Owing to its Pervasive Use in Consumer Electronics and Telecommunications

The market is segmented based on type into:

- Ceramic Capacitor

- Film/Paper Capacitors

- Aluminium Capacitors

- Tantalum/Niobium Capacitors

- Double-Layer/Super capacitors

By Application

Consumer Electronics Segment Leads Due to High Integration in Smartphones, Laptops, and Wearable Devices

The market is segmented based on application into:

- Industrial

- Automotive Electronics

- Consumer Electronics

- Energy

- Other

Regional Analysis: Electric Capacitors Market

Asia-Pacific

As the dominant force in the global electric capacitors market, the Asia-Pacific region accounts for approximately 40% of global consumption, with China being the single largest market. This supremacy is driven by a massive and deeply entrenched electronics manufacturing ecosystem, producing everything from consumer gadgets to industrial machinery. The region is a hub for key global players like Murata, TDK, and Samsung Electro-Mechanics, whose manufacturing bases fuel both domestic consumption and massive exports. While cost-competitive, high-volume ceramic capacitors lead production, there is a significant and growing push toward innovation. This is particularly evident in the development of advanced capacitors for new energy vehicles, 5G infrastructure, and renewable energy systems, aligning with national initiatives like China’s Made in China 2025. The sheer scale of industrial output and rapid technological adoption ensures this region will remain the engine of global market growth for the foreseeable future.

North America

The North American market is characterized by a strong demand for high-reliability and advanced technology capacitors, particularly for the aerospace, defense, medical, and telecommunications sectors. Stringent quality standards and a focus on cutting-edge research and development drive the adoption of specialized components, including tantalum, niobium, and high-performance ceramic capacitors. The region’s market is further bolstered by significant investments in electric vehicle production, smart grid modernization, and data center infrastructure. While the volume consumption is lower than in Asia-Pacific, the value per unit is often higher due to the technical specifications required. The presence of major OEMs and a robust innovation landscape, supported by companies like KEMET (now part of Yageo) and Vishay, ensures a steady demand for premium, performance-driven capacitor solutions.

Europe

The European market is shaped by rigorous environmental regulations, such as the RoHS and REACH directives, which heavily influence material selection and manufacturing processes for capacitors. This regulatory environment fosters innovation in eco-friendly designs and the development of capacitors with longer lifecycles and higher efficiency. The region exhibits strong demand from the automotive industry, especially with the accelerated transition to electric vehicles, which require sophisticated capacitor systems for power management and onboard electronics. Furthermore, a well-established industrial automation sector and investments in renewable energy projects contribute to stable market growth. European manufacturers often compete on the basis of quality, precision engineering, and adherence to sustainability benchmarks, rather than competing solely on cost.

South America

The South American electric capacitors market is in a developing phase, with growth primarily tied to the expansion of industrial automation, consumer electronics penetration, and infrastructure projects. Brazil and Argentina represent the most significant markets within the region. However, economic volatility and currency fluctuations can pose challenges for long-term investment and stable growth, sometimes limiting the widespread adoption of the latest technological advancements. The market is largely served by imports from global leaders and regional distributors, with demand focused on more cost-effective solutions like aluminium electrolytic and ceramic capacitors for applications in consumer durables and basic industrial equipment.

Middle East & Africa

This region represents an emerging market with potential driven by gradual infrastructure development, urbanization, and the slow expansion of manufacturing capabilities. Key growth areas include the development of telecommunications networks, energy infrastructure, and the consumer electronics sector. However, the market currently faces constraints due to limited local production, resulting in a heavy reliance on imports. While the demand for durable components is present, progress can be slowed by economic factors and a focus on more affordable, standard-grade capacitors rather than cutting-edge technologies. Nonetheless, long-term growth prospects are tied to increased economic diversification and urban development initiatives in key nations.

Report Scope

This market research report provides a comprehensive analysis of the global Electric Capacitors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electric Capacitors Market?

-> Electric Capacitors Market was valued at 26750 million in 2024 and is projected to reach US$ 38360 million by 2032, at a CAGR of 5.4% during the forecast period.

Which key companies operate in Global Electric Capacitors Market?

-> Key players include Murata, KYOCERA, TDK, Samsung Electro, and Taiyo Yuden, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, automotive electrification, and renewable energy infrastructure development.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China accounting for approximately 40% of global consumption.

What are the emerging trends?

-> Emerging trends include miniaturization of components, development of high-capacitance supercapacitors, and integration of capacitors in IoT and AI applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...