Market Insights

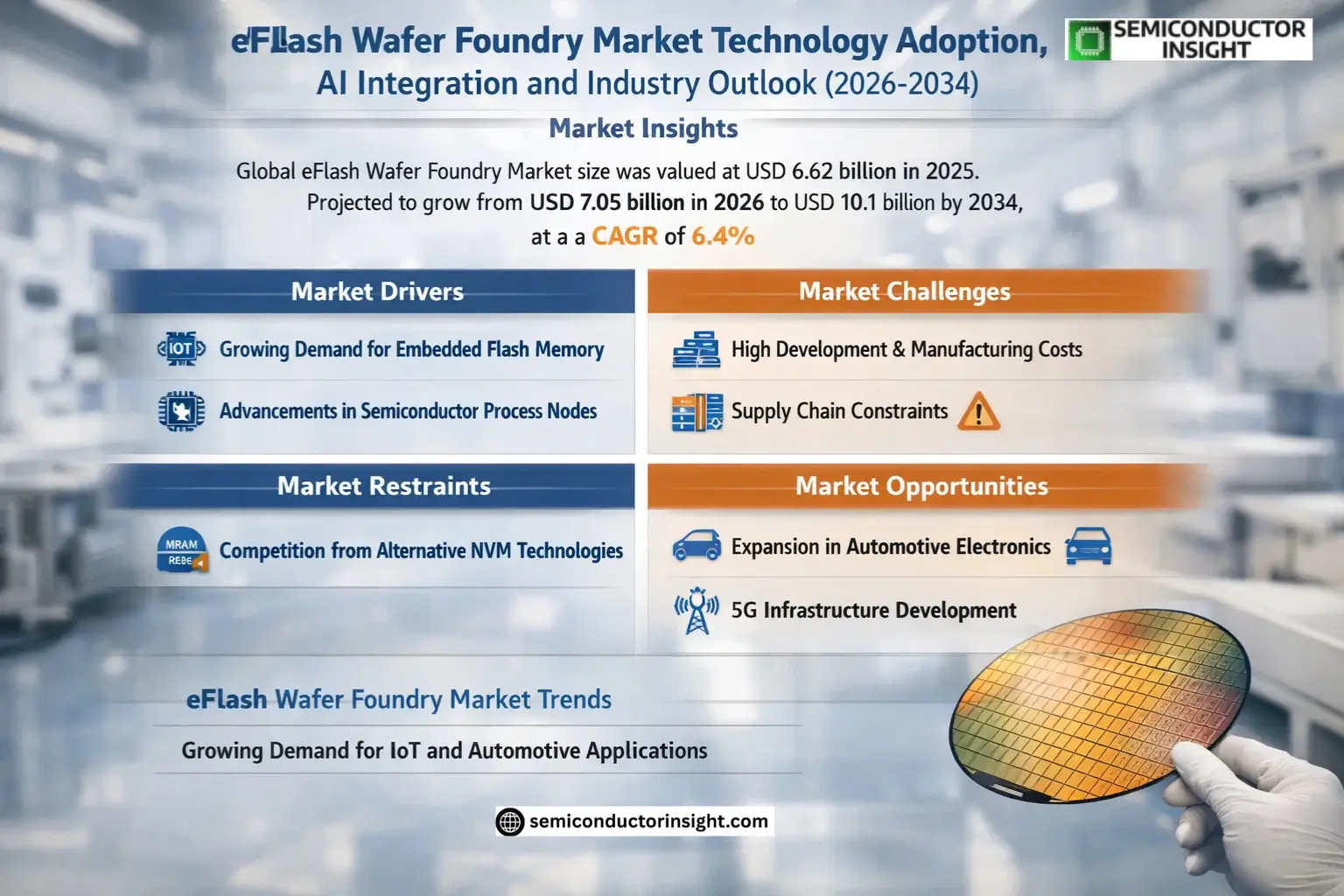

Global eFlash Wafer Foundry Market size was valued at USD 6.62 billion in 2025. The market is projected to grow from USD 7.05 billion in 2026 to USD 10.1 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period.

Embedded Flash (eFlash) memory is a critical technology for programmable semiconductor devices requiring compact designs and energy-efficient processing. It enables microcontrollers to store both executable code and operational data, supporting essential functions like over-the-air (OTA) updates for IoT devices and automotive systems. Key process nodes in this market include 28nm, 40nm, and legacy technologies down to 0.25µm.

Market expansion is driven by rising demand for smart cards, automotive electronics, and industrial IoT applications where secure, updatable firmware is essential. Leading foundries like TSMC and GlobalFoundries dominate production, with advanced nodes gaining traction for power-sensitive applications while mature nodes remain vital for cost-optimized solutions.

MARKET DRIVERS

Growing Demand for Embedded Flash Memory

eFlash Wafer Foundry Market is experiencing significant growth driven by the rising demand for embedded flash memory in IoT devices, automotive electronics, and smart appliances. With over 65% of microcontrollers now incorporating eFlash technology, foundries are scaling production to meet industry needs.

Advancements in Semiconductor Process Nodes

Leading eFlash wafer foundries are transitioning to 40nm and below process nodes, offering improved performance and power efficiency. This technological evolution enables higher-density memory solutions that are critical for next-generation applications.

Foundries specializing in eFlash technology are seeing increased investments as demand for reliable, non-volatile memory solutions continues to expand across multiple industries.

MARKET CHALLENGES

High Development and Manufacturing Costs

eFlash Wafer Foundry Market faces significant challenges in maintaining cost-effectiveness while developing advanced process technologies. The specialized equipment required for eFlash production represents a substantial capital investment for foundries.

Other Challenges

Technology Migration Difficulties

Transitioning to smaller process nodes presents technical hurdles in maintaining flash memory reliability while reducing cell sizes, requiring extensive R&D investments.

Supply Chain Constraints

The specialized materials and equipment needed for eFlash production remain vulnerable to global supply chain disruptions, impacting production timelines.

MARKET RESTRAINTS

Competition from Alternative NVM Technologies

eFlash Wafer Foundry Market faces competition from emerging memory technologies such as MRAM and ReRAM, which offer potential advantages in certain applications. However, eFlash maintains dominance in cost-sensitive, high-volume applications where proven reliability is critical.

MARKET OPPORTUNITIES

Expansion in Automotive Electronics

The automotive sector presents significant growth opportunities for eFlash wafer foundries, with increasing demand for memory solutions in ADAS, infotainment systems, and vehicle electrification. The automotive eFlash market segment is projected to grow at 12% annually through 2028.

5G Infrastructure Development

Global 5G network expansion is driving demand for eFlash solutions in base stations and networking equipment, creating new opportunities for specialized wafer foundries to supply high-reliability memory components.

eFlash Wafer Foundry Market TrendsGrowing Demand for IoT and Automotive Applications

eFlash Wafer Foundry Market is experiencing significant growth driven by increasing adoption in IoT devices and automotive electronics. Embedded Flash technology enables secure, low-power storage solutions essential for smart connected devices. Major foundries are expanding production capacity for 28nm and 40nm nodes to meet demand from automotive MCU manufacturers requiring reliable non-volatile memory.

Other Trends

Process Node Specialization

Leading foundries are focusing on optimizing 28nm-55nm eFlash processes, as these nodes offer the best balance of performance, power efficiency and cost for most applications. While advanced nodes below 28nm are being developed, the majority of current production remains in established mature nodes due to their proven reliability and economic viability.

Regional Market Expansion

Asia-Pacific dominates eFlash Wafer Foundry production with TSMC, UMC and SMIC leading the market. However, North American and European automotive manufacturers are driving increased demand, prompting foundries to establish strategic partnerships with regional suppliers. The market is seeing increased investment in China’s domestic foundries to reduce reliance on foreign suppliers.

Foundry Competition Intensifies

TSMC maintains leadership in advanced eFlash processes, while GlobalFoundries and UMC compete strongly in mainstream nodes. Second-tier foundries are specializing in niche applications like industrial MCUs and secure elements. The market is seeing consolidation as smaller players form alliances to compete with industry leaders in this capital-intensive sector.

Technology Innovation Focus

Key manufacturers are investing in improved endurance and data retention characteristics for automotive-grade eFlash. Development efforts focus on achieving higher temperature tolerance and radiation hardening for mission-critical applications. Innovations in 3D eFlash architectures aim to address scaling challenges beyond 28nm nodes while maintaining cost-effectiveness.

COMPETITIVE LANDSCAPE

Key Industry Players

Dominance of Leading Foundries in Specialized eFlash Technology

Taiwan Semiconductor Manufacturing Company (TSMC) leads Global eFlash Wafer Foundry Market with approximately 35% revenue share in 2025, owing to its advanced 28nm and 40nm eFlash process nodes. The market exhibits an oligopolistic structure where top five players collectively control nearly 75% of production capacity, with GlobalFoundries and United Microelectronics Corporation (UMC) following TSMC in market positioning due to their specialized automotive-grade and industrial IoT compatible eFlash solutions.

Emerging Chinese foundries like SMIC and Hua Hong Semiconductor are gaining traction through government-supported capacity expansions, particularly for 55nm-90nm eFlash nodes used in consumer electronics. Meanwhile, specialty foundries such as Tower Semiconductor and X-FAB maintain strong positions in niche applications including medical devices and industrial MCUs, leveraging their legacy 0.11μm to 0.25μm eFlash processes.

List of Key eFlash Wafer Foundry Companies Profiled

- Taiwan Semiconductor Manufacturing Company (TSMC)

- GlobalFoundries

- United Microelectronics Corporation (UMC)

- Semiconductor Manufacturing International Corporation (SMIC)

- Tower Semiconductor

- Powerchip Semiconductor Manufacturing Corporation (PSMC)

- Vanguard International Semiconductor (VIS)

- Hua Hong Semiconductor

- Shanghai Huali Microelectronics Corporation (HLMC)

- X-FAB

- DB HiTek

- Nexchip

- MagnaChip Semiconductor

- ON Semiconductor

- Rohm Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

28nm and 40nm eFlash Process dominates as the leading segment due to:

|

| By Application |

|

IoT Applications represent the fastest-growing segment because:

|

| By End User |

|

Automotive Tier 1 Suppliers are driving significant demand growth due to:

|

| By Technology Node |

|

Advanced Nodes are gaining prominence with attributes including:

|

| By Supply Chain Position |

|

Pure-play Foundries maintain leadership due to:

|

Regional Analysis: Asia-Pacific eFlash Wafer Foundry Market

Taiwan accounts for over 60% of global eFlash wafer production through TSMC’s technology leadership. The island’s foundries excel in high-reliability eFlash for automotive and industrial applications, with strong IP protection attracting international design houses.

Chinese foundries like SMIC are rapidly upgrading eFlash capabilities through technology transfers and equipment investments. Domestic demand for consumer electronics and EV components drives specialization in cost-optimized eFlash variants with localized IP.

Samsung combines eFlash foundry services with its DRAM expertise, creating optimized embedded memory solutions for AI chipsets. This vertical integration provides unique performance advantages in high-bandwidth memory applications.

Japanese foundries specialize in AEC-Q100 qualified eFlash solutions with exceptional endurance characteristics. Partnerships with automotive OEMs enable customized process optimizations for next-generation vehicle electronics and ADAS systems.

North America

The North American eFlash Wafer Foundry Market centers on specialized analog/mixed-signal applications and defense contracts. GlobalFoundries and SkyWater maintain capacity in legacy eFlash nodes (180nm-90nm) for aerospace, medical devices, and industrial automation sectors. The region shows growing demand for radiation-hardened eFlash variants in space applications, with foundries developing proprietary isolation techniques. While trailing Asia in volume production, North America maintains technological advantages in security-focused eFlash implementations through partnerships with FPGA and microcontroller vendors.

Europe

European foundries like STMicroelectronics focus on automotive-grade eFlash solutions with stringent quality requirements. The region’s strength lies in 90nm-55nm embedded flash processes for automotive MCUs and smart energy applications. European Commission initiatives promote sovereign eFlash capabilities through joint R&D projects targeting IoT security applications. The market shows increasing interest in low-power eFlash variants for wearable medical devices and industrial sensors, with foundries developing specialized SONOS-based processes for these applications.

Middle East & Africa

The emerging Middle Eastern semiconductor strategy includes planned eFlash foundry investments targeting IoT and smart city applications. Israel’s Tower Semiconductor provides specialized eFlash processes for defense and communication systems, while new UAE initiatives aim to develop foundry capabilities for automotive components. Africa’s market remains nascent but shows potential for localized eFlash production serving mobile payment and renewable energy monitoring applications as the regional electronics manufacturing base expands.

South America

South America’s eFlash wafer foundry presence centers on assembly and test operations serving regional automotive and consumer electronics demand. Brazil’s Ceitec maintains limited eFlash capabilities for RFID and identification chips, while most advanced foundry services are imported from Asia. The region shows growing demand for eFlash-based industrial controllers and smart grid components, with potential for technology transfers from established foundry partners in North America and Europe.

Report Scope

This market research report provides a comprehensive analysis of the eFlash Wafer Foundry Market , covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of eFlash Wafer Foundry Market?

-> eFlash Wafer Foundry Market size was valued at USD 6.62 billion in 2025. The market is projected to grow from USD 7.05 billion in 2026 to USD 10.1 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period.

What is the growth rate of eFlash Wafer Foundry Market?

-> The market is expected to grow at a CAGR of 6.4% during the forecast period (2025-2034).

Which key companies operate in eFlash Wafer Foundry Market?

-> Key players include TSMC, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, X-FAB, among others.

What are the key applications of eFlash Wafer Foundry?

-> Key applications include Smart Card, MCU, IoT Applications, Automotive, and others.

Which process nodes are covered in the report?

-> The report covers key process nodes including 28nm, 40nm, 45nm, 55nm, 90nm, 0.11um, 0.13um and 0.25µm eFlash process.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...