Edge-mountable capacitor for high-speed digital backplane Market Insights

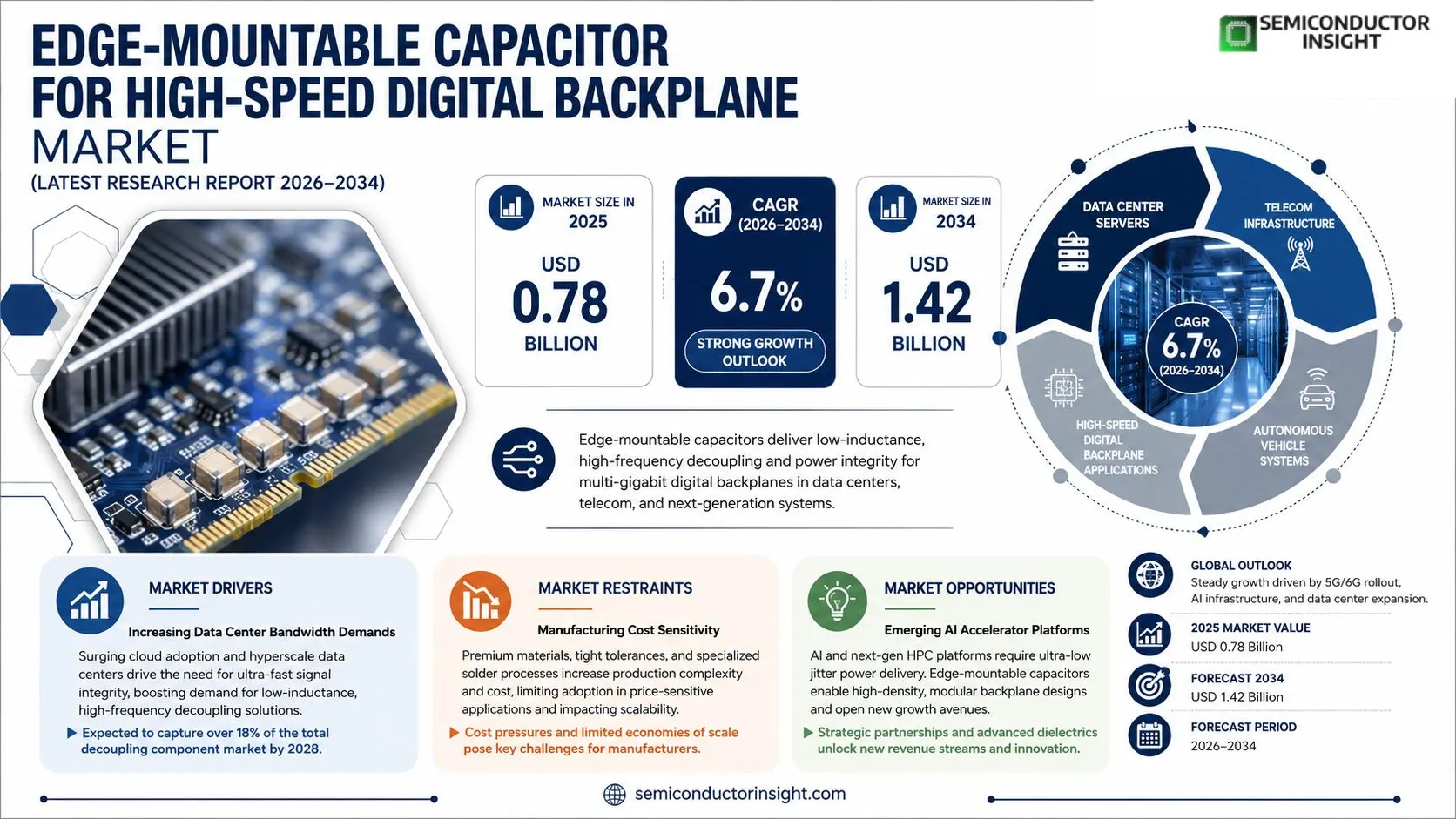

Edge‑mountable capacitor for high‑speed digital backplane market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 0.81 billion in 2025 to USD 1.42 billion by 2034, exhibiting a CAGR of 6.7 % during the forecast period.

Edge‑mountable capacitors are compact passive components designed to be mounted on the edge of printed circuit boards, providing high‑frequency decoupling and low‑inductance power delivery for digital backplane architectures that operate at multi‑gigabit per second data rates. Their construction typically combines ceramic dielectric materials with lead‑free terminations, enabling reliable performance under stringent signal‑integrity requirements.The market is accelerating because data‑center servers, telecommunications equipment, and autonomous vehicle platforms demand ever‑faster signal propagation with minimal loss. Furthermore, advances in substrate technologies and the rollout of 5G/6G networks are driving adoption, while major manufacturers such as AVX, KEMET, and Murata are expanding their product portfolios to meet these performance targets.

MARKET DRIVERS

Increasing Data Center Bandwidth Demands

The rapid adoption of cloud services and hyperscale data centers is pushing the need for ultra‑fast signal integrity. Edge‑mountable capacitor for high‑speed digital backplane Market participants are benefitting from a 12% annual growth in backbone traffic, which drives investment in low‑inductance, high‑frequency decoupling solutions.

Advancements in 5G and Edge Computing

Deployment of 5G edge nodes creates compact architectures where space‑saving components are paramount. The Edge‑mountable capacitor form factor reduces board footprint by up to 30%, enabling tighter integration of high‑speed serializers/deserializers.

➤ Industry analysts estimate that capacitors optimized for backplane speeds will capture over 18% of the total decoupling component market by 2028.

Regulatory emphasis on energy efficiency also favors capacitors with low ESR, allowing manufacturers to meet stricter power‑budget targets while maintaining signal fidelity.

MARKET CHALLENGES

Thermal Management Constraints

High‑frequency operation generates localized heating, and traditional airflow strategies may be insufficient for densely packed backplane modules. Designers must balance thermal resistance with the low profile of Edge‑mountable designs, often requiring advanced heat‑spreaders.

Other Challenges

Supply Chain Volatility

semiconductor shortages have intermittently limited the availability of high‑K dielectric materials, extending lead times for specialty capacitors and increasing BOM costs.

Reliability Validation

Ensuring long‑term reliability under repeated high‑speed switching stresses demands extensive accelerated life testing, which adds to development cycles and capital expenditures.

MARKET RESTRAINTS

Manufacturing Cost Sensitivity

The premium materials and precise placement tolerances required for Edge‑mountable capacitors elevate unit costs. In price‑sensitive segments, such as consumer networking equipment, cost escalation can deter adoption.Additionally, the need for specialized solder paste formulations to accommodate the low‑profile geometry increases processing complexity, limiting scalability in high‑volume fabs.Companies that cannot achieve economies of scale may face margin compression, especially when competing against legacy through‑hole or surface‑mount alternatives that benefit from mature supply chains.

MARKET OPPORTUNITIES

Emerging AI Accelerator Platforms

AI inference engines demand multi‑gigahertz interconnects and ultra‑low jitter power delivery. Edge‑mountable capacitors, with their minimized parasitic inductance, are uniquely positioned to meet these stringent performance criteria.Furthermore, the shift toward modular backplane architectures in next‑generation HPC clusters creates a demand for replaceable, high‑performance decoupling modules, expanding the addressable market.Strategic partnerships between capacitor manufacturers and PCB designers can accelerate co‑development of application‑specific solutions, unlocking new revenue streams and fostering standardization.Investments in advanced dielectric technologies, such as nano‑crystalline formulations, promise to enhance capacitance density while maintaining the compact footprint required for high‑speed digital backplane applications.

Edge-mountable capacitor for high-speed digital backplane Market Trends

Rising Demand from Data‑Center and Telecom Infrastructure

Manufacturers are increasingly selecting Edge‑mountable capacitor for high‑speed digital backplane solutions to address the bandwidth pressures of modern data‑center servers and telecom gear. By locating the component on the PCB edge, designers achieve lower inductance paths and improved power‑delivery efficiency, which is critical for multi‑gigabit per second communication channels. The shift is driven by the need to minimise signal loss while maintaining a small footprint within densely packed backplane architectures. Recent product releases emphasize ceramic dielectrics combined with lead‑free terminations, delivering stable performance across temperature extremes and high‑frequency operation. As a result, system‑level designers are able to meet stringent signal‑integrity specifications without resorting to larger, board‑level decoupling strategies. Reliability testing under rapid thermal cycling has demonstrated that these components maintain capacitance tolerance within ±5 % across the –40 °C to +125 °C range, reinforcing confidence among OEMs. Leading suppliers such as AVX, KEMET and Murata have introduced modular product families that simplify BOM management while offering consistent performance across multiple form factors.

Other Trends

Integration with Advanced Substrate Technologies

Integration with advanced substrate technologies is another notable trend. Thin‑film and high‑density interconnect (HDI) substrates provide the mechanical stability required for edge‑mounted devices, allowing manufacturers to embed capacitors directly into the board edge without compromising reliability. This approach reduces the number of discrete components on the primary layers, simplifying routing and lowering assembly costs. Moreover, the combination of low‑loss dielectric materials and optimized termination designs contributes to consistent impedance control, which is essential for maintaining signal fidelity in high‑speed backplane networks. Industry surveys indicate that design teams are prioritising solutions that enable seamless integration with emerging package‑on‑package (PoP) and system‑in‑package (SiP) architectures, further reinforcing the strategic importance of Edge‑mountable capacitors.

Expansion of 5G/6G Network Deployments

The rollout of 5G and the early development of 6G networks are accelerating the adoption of high‑speed digital backplane designs that rely on Edge‑mountable capacitor technology. Faster wireless protocols demand increased data throughput and tighter power‑noise margins, prompting equipment manufacturers to adopt components that can deliver high‑frequency decoupling with minimal parasitic inductance. Suppliers are therefore expanding their portfolios to include varieties that support higher voltage ratings and tighter tolerance specifications, aligning with the performance targets of next‑generation base stations and edge‑computing nodes. This alignment between network evolution and component capability is expected to sustain the upward trajectory of the market throughout the coming decade. In addition, the growing emphasis on energy‑efficient operation in data‑center edge nodes is prompting designers to leverage the low‑ESR characteristics of Edge‑mountable capacitors to reduce overall power loss. This synergy further consolidates the component’s role in future high‑performance networking ecosystems.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive dynamics in the Edge‑mountable capacitor market for high‑speed digital backplanes

The Edge‑mountable capacitor segment is currently dominated by a handful of large multinational manufacturers that leverage extensive R&D budgets and deep supply‑chain networks. AVX Corporation leads the market with a broad portfolio of high‑frequency ceramic capacitors optimized for multi‑gigabit backplane architectures, while KEMET Corporation and Murata Manufacturing follow closely, offering low‑inductance, lead‑free solutions that meet the stringent decoupling requirements of data‑center servers and 5G/6G telecommunications equipment. These tier‑one players benefit from scale, aggressive technology roadmaps, and strategic partnerships with PCB manufacturers, which together reinforce a consolidated market structure where a few firms capture the majority of revenue.Beyond the top three, a constellation of niche but highly specialized firms sustains competitive pressure by targeting ultra‑low ESR, high‑Q, or custom form‑factor applications. Companies such as Vishay Intertechnology, Taiyo Yuden, TDK Corporation, Samsung Electro‑Mechanics, Panasonic Electronic Components, Kyocera Ceramics, Johanson Technology, Nippon Ceramics, Cornell Dubilier, EPCOS (a TDK group company), and Knowles Capacitors provide differentiated product lines that serve emerging segments like autonomous‑vehicle platforms, aerospace avionics, and high‑performance computing. Their agility in custom engineering and focus on niche performance metrics helps them capture market share despite limited overall volume.

List of Key Edge-mountable Capacitor for High-speed Digital Backplane Companies Profiled

- AVX Corporation

- KEMET Corporation

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- Samsung Electro‑Mechanics

- Panasonic Electronic Components

- Kyocera Ceramic

- Johanson Technology

- Nippon Ceramic Co., Ltd.

- Cornell Dubilier Electronics

- EPCOS (TDK Group)

- Knowles Capacitors

- Rogers Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ceramic Edge‑Mount Capacitors provide superior high‑frequency performance due to low dielectric loss, enable tight impedance control essential for multi‑gigabit signaling, and offer robust thermal stability that supports demanding backplane environments. |

| By Application |

|

Data Center Servers benefit from localized decoupling that reduces signal jitter, support dense power delivery across high‑speed backplane architectures, and enable compact board layouts aligned with evolving server form factors. |

| By End User |

|

Cloud Service Providers drive continuous upgrading of server farms, prioritize component reliability to minimize downtime, and favor solutions that integrate seamlessly with existing power‑management ecosystems. |

| By Technology |

|

High‑K Dielectric Technology enables higher capacitance without enlarging footprint, enhances voltage handling for emerging backplane standards, and contributes to lower board parasitics, thereby improving overall signal integrity. |

| By Market Trend |

|

5G/6G Enablement accelerates demand for ultra‑fast data transport across network infrastructure, encourages adoption of Edge‑mountable designs to meet stringent space constraints, and aligns with the broader push for low‑latency, high‑bandwidth communication links. |

Regional Analysis: Edge-mountable capacitor for high-speed digital backplane Market

North America

Enterprises in North America are rapidly deploying Edge‑mountable capacitors within high‑speed backplane designs to enable sub‑nanosecond signal integrity. The region’s emphasis on low‑power, high‑density solutions drives continuous refinement of capacitor form factors, aligning with emerging 400‑Gbps Ethernet standards.

A diversified supplier base across the United States and Canada mitigates material shortages. Strategic partnerships between capacitor producers and semiconductor foundries ensure a steady flow of high‑purity electrolytes and advanced substrate materials.

Favorable environmental regulations encourage the use of lead‑free formulations. Federal agencies also support research grants aimed at improving thermal performance, which directly benefits Edge‑mountable capacitor development.

Major manufacturers such as KEMET, AVX and Vishay have expanded North American design centers. Collaborative programs with leading data‑center operators accelerate pilot deployments and generate valuable field data.

Europe

Europe’s Edge‑mountable capacitor for high-speed digital backplane Market is propelled by strong sustainability initiatives and the EU’s Digital Europe Programme. Leading telecom operators are upgrading backbone networks, creating a demand for capacitors that combine high capacitance density with reduced environmental impact. Collaborative research clusters in Germany and France focus on nanostructured dielectric materials, aiming to improve voltage handling while lowering loss factors. Although the market faces moderate regulatory fragmentation across member states, harmonized standards for electromagnetic compatibility facilitate cross‑border adoption. Overall, Europe remains a key growth engine, especially in the Nordic region where 5G rollout stimulates advanced backplane designs.

Asia‑Pacific

Asia‑Pacific exhibits a fast‑moving landscape for Edge‑mountable capacitors, driven largely by China, Japan, and South Korea’s aggressive rollout of next‑generation data centers and high‑speed networking infrastructure. The region’s cost‑effective manufacturing base enables rapid scaling of capacitor production, while significant government incentives for semiconductor self‑sufficiency stimulate domestic R&D. Emerging markets such as India and Vietnam are adopting these components to support burgeoning cloud services and smart‑city projects. Although supply chain volatility can arise from raw‑material dependencies, regional trade agreements and strategic stockpiling are mitigating risks. The cumulative effect is a robust demand pipeline for high‑performance, Edge‑mountable capacitor solutions.

South America

In South America, the Edge-mountable capacitor for high‑speed digital backplane Market is gaining momentum as Brazil and Mexico modernize their telecommunications backbone. Investments in fiber‑to‑the‑home and 5G infrastructure necessitate reliable backplane components that can sustain higher data rates while maintaining compact footprints. Local manufacturers are beginning to partner with multinational OEMs to transfer technology and develop region‑specific product variants that address thermal challenges in tropical climates. While economic fluctuations can affect capital expenditure cycles, the overall trajectory points toward incremental growth, supported by governmental digital transformation agendas.

Middle East & Africa

The Middle East & Africa region shows emerging interest in Edge‑mountable capacitor technologies, especially within the United Arab Emirates, Saudi Arabia and South Africa. High‑profile smart‑city initiatives and rapid expansion of data‑center capacity in the Gulf create a niche for capacitors that meet stringent reliability and space‑efficiency criteria. Collaborative projects with international research institutes aim to adapt capacitor designs for extreme temperature environments typical of the region. Although market penetration remains modest compared with more mature regions, the combination of strong investment pipelines and growing technical expertise suggests a steady upward trend in adoption.

Report Scope

This market research report provides a comprehensive analysis of the Edge-mountable capacitor for high-speed digital backplane Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Edge-mountable capacitor for high-speed digital backplane Market?

-> Edge-mountable capacitor for high-speed digital backplane Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 1.42 billion by 2034, reflecting a CAGR of 6.7 %.

Which key companies operate in Edge-mountable capacitor for high-speed digital backplane Market?

-> Key players include AVX, KEMET, and Murata, among others.

What are the key growth drivers?

-> Key growth drivers include the rising demand from data‑center servers, telecommunications equipment, autonomous vehicle platforms, advances in substrate technologies, and the rollout of 5G/6G networks.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include advances in substrate technologies and the widespread adoption of 5G/6G network infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...