Edge AI Embedded Systems Market Insights

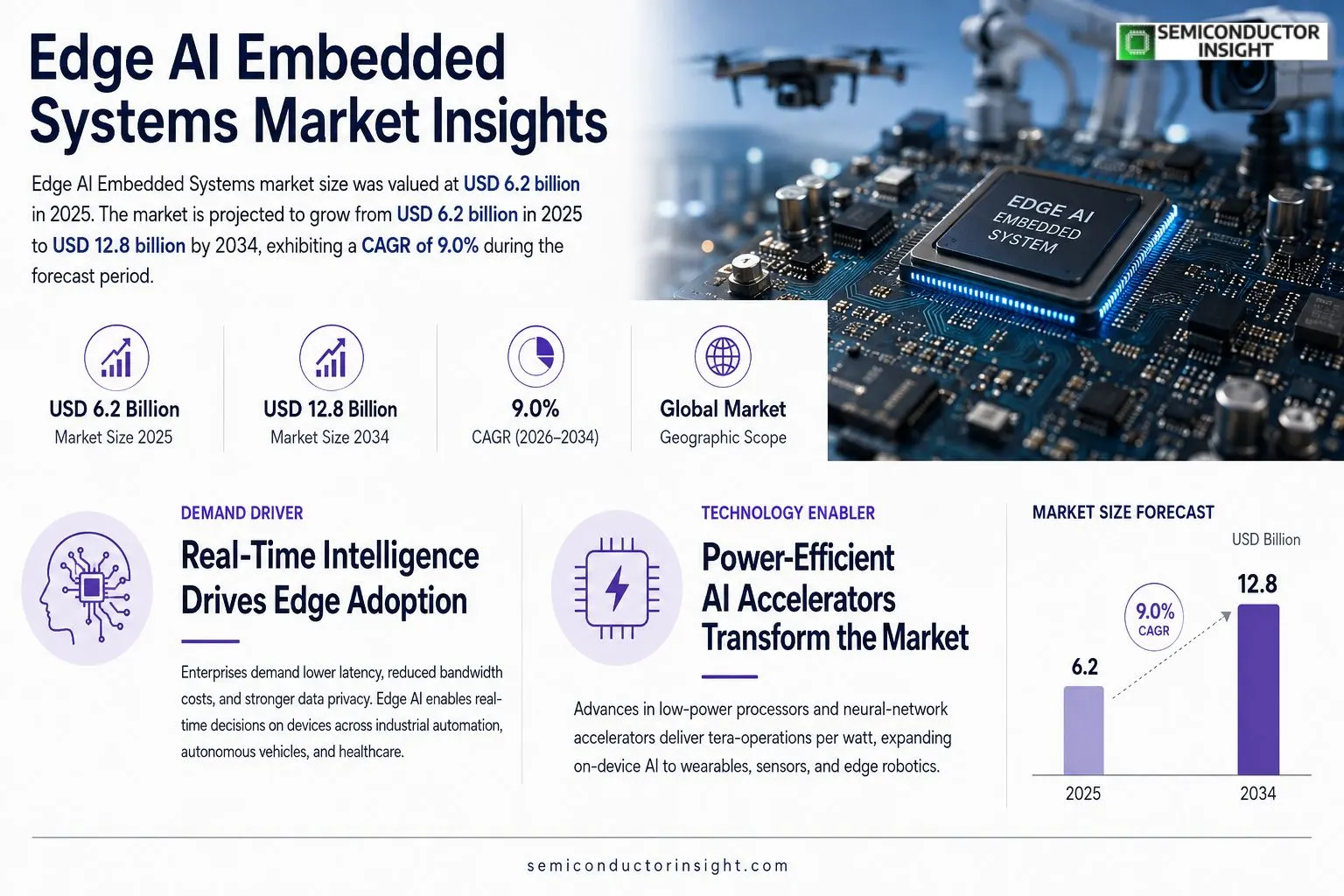

Edge AI Embedded Systems market size was valued at USD 6.2 billion in 2025. The market is projected to grow from USD 6.2 billion in 2025 to USD 12.8 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period.

Edge AI Embedded Systems combine artificial intelligence algorithms with embedded hardware to enable real‑time inference directly on devices such as sensors, cameras, drones, and industrial controllers. These systems integrate low‑power processors, neural‑network accelerators, and optimized software stacks so that data can be analyzed locally without reliance on cloud connectivity.The market is experiencing rapid growth because enterprises are seeking lower latency, reduced bandwidth costs, and enhanced data privacy across IoT deployments. Furthermore, rising adoption of autonomous vehicles, smart manufacturing, and wearable health monitors fuels demand for on‑device intelligence. Key playersincluding NVIDIA®, Intel®, Qualcomm®, Arm®, and Googleare expanding their edge‑AI portfolios through strategic partnerships; for example, in March 2024 NVIDIA® partnered with Microsoft Azure to deliver accelerated inference services at the network edge.

MARKET DRIVERS

Rising Adoption of Edge AI in Industrial Automation

Edge AI Embedded Systems Market is propelled by manufacturers seeking real‑time analytics on the shop floor. By processing data locally, factories reduce latency, lower bandwidth costs, and improve predictive maintenance accuracy, which in turn drives higher equipment uptime.

Expansion of 5G Connectivity

Widespread rollout of 5G networks enables reliable, high‑speed communication between edge devices and cloud resources. This connectivity accelerates deployment of AI models at the edge, especially in smart‑city and autonomous‑vehicle applications, enriching market momentum.

➤ “Edge AI offers the unique advantage of performing inference at the source, eliminating the need for perpetual data transfer to centralized servers.”

Additionally, the growing emphasis on data privacy and regulatory compliance encourages organizations to keep sensitive information on‑device, further amplifying demand for robust Edge AI embedded solutions.

MARKET CHALLENGES

High Development Costs and Skill Gaps

Designing optimized AI models for resource‑constrained embedded platforms requires specialized expertise. Companies often face steep R&D expenditures and a shortage of engineers proficient in both hardware acceleration and AI algorithm optimization.

Other Challenges

Integration Complexity

Integrating heterogeneous hardware componentssuch as ASICs, FPGAs, and microcontrollerswith existing software ecosystems can lead to prolonged time‑to‑market and increased validation effort.

Furthermore, ensuring consistent performance across diverse operating environments (temperature, vibration, power variability) adds another layer of technical difficulty for manufacturers.

MARKET RESTRAINTS

Stringent Power and Thermal Limits

Edge devices often operate on limited power budgets, especially in remote or battery‑powered deployments. Achieving high inference throughput while staying within thermal envelopes remains a critical constraint for many OEMs.Regulatory approvals for mission‑critical sectors, such as automotive safety and medical diagnostics, impose rigorous testing cycles that can delay product launches and increase compliance costs.Supply‑chain volatility for silicon components also restricts the ability of manufacturers to scale production quickly, further dampening market expansion.

MARKET OPPORTUNITIES

Emergence of TinyML and Low‑Power AI Frameworks

The advent of TinyML toolchains and ultra‑low‑power AI inference libraries unlocks new use cases for wearables, environmental sensors, and edge robotics. These software advancements reduce memory footprints, enabling sophisticated models to run on microcontrollers with sub‑milliwatt power consumption.Edge AI integration with renewable‑energy management systems presents a sizable growth avenue. Real‑time load forecasting and adaptive control at the edge can optimize micro‑grid stability while minimizing reliance on centralized data centers.Finally, strategic partnerships between semiconductor vendors and AI software providers are fostering turnkey solutions, lowering entry barriers for mid‑size enterprises looking to embed intelligence directly into their products.

Edge AI Embedded Systems Market Trends

Real‑time Inference Reducing Latency and Bandwidth Costs

Edge AI Embedded Systems Market is being reshaped by the need for instant data processing at the device level. Enterprises are moving away from cloud‑centric models because on‑device inference eliminates round‑trip latency, often cutting response times by 10‑20 ms, reduces bandwidth expenses, and strengthens data privacy. Industries such as autonomous transportation, smart factories, and wearable health monitoring are deploying sensors, cameras and controllers that run neural‑network models locally. This capability enables deterministic response times that are essential for safety‑critical functions, while also supporting massive IoT rollouts where continuous cloud connectivity is costly or impossible. The shift also aligns with regulatory trends that favor on‑premise data handling, especially in sectors handling personal health or financial information.

Other Trends

Power‑Efficient Hardware Accelerators

Low‑power processors and dedicated neural‑network accelerators are a cornerstone of the market’s growth. Chip designers such as Arm, Qualcomm, and Intel have introduced microarchitectures that deliver multiple tera‑operations per watt, allowing edge devices to run sophisticated AI workloads within tight energy envelopes. These designs incorporate heterogeneous compute blocks, on‑chip SRAM, and power‑gating techniques that keep average draw below 500 mW for common vision models. Integrated memory hierarchies and custom instruction sets further reduce energy consumption, making edge AI viable for remote sensors, battery‑operated drones, and wearable devices that must operate for weeks without recharge. As a result, manufacturers can embed AI capabilities in products that previously lacked the compute headroom, expanding the addressable market for on‑device intelligence across agriculture, logistics, and public safety.

Strategic Partnerships Expanding the Edge AI Ecosystem

Collaboration between hardware vendors and cloud providers is accelerating adoption across Edge AI Embedded Systems Market. In March 2024 NVIDIA partnered with Microsoft Azure to deliver accelerated inference services at the network edge, while Intel announced joint solutions with Google that simplify model deployment on edge processors through a unified software stack. Qualcomm recently launched a development kit that integrates its AI‑engine with Amazon Web Services, enabling developers to move models from the cloud to device with a single API. These alliances provide standardized toolchains, robust security features, and managed update mechanisms, lowering barriers for enterprises that lack deep AI expertise. The combined effect of power‑efficient silicon and a mature ecosystem positions the market for sustained double‑digit growth through 2034. Analysts expect that by 2030 the majority of new industrial IoT deployments will include edge AI capabilities as standard. This trend reinforces the strategic importance of integrated AI hardware for future competitive advantage.

COMPETITIVE LANDSCAPEKey Industry Players

Edge AI Embedded Systems Market – Competitive Overview

Edge AI Embedded Systems Market is anchored by a handful of technology giants that dominate processor design, neural‑network acceleration, and software ecosystems. NVIDIA leads the space with its Jetson portfolio, offering high‑performance GPUs and dedicated TensorRT inference engines that power autonomous robots, drones, and industrial vision systems. Intel complements this leadership through its Xeon and Atom lines, coupled with OpenVINO tooling that standardizes deployment across heterogeneous edge devices. Qualcomm’s Snapdragon platforms bring low‑power AI to mobile‑class edge nodes, while Arm’s CPU/IP architectures enable a broad ecosystem of licensees to embed AI accelerators directly into silicon. Google’s Edge TPU delivers specialized ASIC performance for on‑device inference, often bundled with TensorFlow Lite for rapid model deployment. Collectively these firms shape a tiered market structure where scalable hardware platforms are paired with mature development stacks, creating high entry barriers for newcomers.Beyond the dominant tier, several niche and challenger companies are gaining traction by addressing vertical‑specific requirements or offering alternative accelerator architectures. Mythic provides analog‑compute AI chips that promise ultra‑low power consumption for wearables and IoT sensors. Horizon Robotics focuses on automotive edge AI with its Journey series, delivering sensor‑fusion capabilities for driver‑assist systems. Gyrfalcon introduces ultra‑compact FPGA‑based AI modules suited for space‑constrained robotics. Additionally, companies such as Ambarella, Alibaba Cloud (Aliyun), Qualcomm‑based start‑ups, and Israeli firm Syntiant contribute specialized DSP and neural‑net solutions that enrich the competitive landscape and foster innovation across edge deployments.

List of Key Edge AI Embedded Systems Companies Profiled

- NVIDIA

- Intel

- Qualcomm

- Arm

- Mythic

- Horizon Robotics

- Gyrfalcon

- Ambarella

- Alibaba Cloud

- Syntiant

- EdgeIQ

- Renesas Electronics

- Analog Devices

- XCELLSIS

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neural Accelerator Chips are emerging as the leading segment because they enable high‑throughput inference while keeping energy consumption modest. They support complex models on the edge, allowing devices such as drones and cameras to make split‑second decisions. • Integration with system‑on‑chip designs simplifies hardware stacks. • Growing software ecosystems accelerate developer adoption and reduce time‑to‑market for AI‑enabled products. |

| By Application |

|

Smart Manufacturing dominates this dimension due to its demand for real‑time quality inspection, predictive maintenance, and adaptive control. Edge AI lets factories process sensor streams locally, preserving confidentiality and minimizing latency. • On‑device analytics enable immediate corrective actions, reducing scrap. • Seamless integration with legacy PLCs accelerates digital transformation without extensive cloud reliance. |

| By End User |

|

Industrial Automation is the leading end‑user segment, driven by the need for ultra‑low latency decision loops on the shop floor. Edge AI embedded systems embed intelligence directly in controllers and sensors, improving safety and efficiency. • Real‑time anomaly detection prevents equipment failures. • Local processing respects data‑privacy regulations in regulated environments. |

| By Connectivity |

|

Wi‑Fi / 5G Integrated Nodes are gaining traction as they combine high bandwidth with edge compute, allowing rich sensor data to be analysed locally while still supporting occasional cloud sync. • Reduced reliance on continuous connectivity lowers operational costs. • Enables smooth hand‑off between edge and cloud for advanced analytics. |

| By Ecosystem |

|

Open‑Source AI Frameworks drive democratization of edge AI, allowing developers to port models across heterogeneous hardware. This fosters rapid prototyping and cross‑industry innovation. • Community contributions accelerate optimization for low‑power silicon. • Seamless integration with vendor SDKs simplifies deployment pipelines. |

Regional Analysis: North America

North America

The integration of Edge AI Embedded Systems in industrial automation is gaining momentum, enabling predictive maintenance, quality control, and process optimization. This trend is driven by the need for increased efficiency, reduced downtime, and enhanced safety in manufacturing operations.

Retailers are leveraging Edge AI Embedded Systems to enhance customer experience, optimize inventory management, and improve operational efficiency. Applications include computer vision for customer analytics, smart checkout systems, and personalized recommendations.

The healthcare sector is adopting Edge AI Embedded Systems for applications such as remote patient monitoring, medical imaging analysis, and wearable health devices. This facilitates timely interventions, improves patient outcomes, and reduces healthcare costs.

Edge AI Embedded Systems are crucial for the development of autonomous vehicles, enabling real-time perception, decision-making, and control. This technology is essential for ensuring the safety and reliability of self-driving cars.

North America

The North American Edge AI Embedded Systems Market is projected to experience substantial growth in the coming years, driven by increasing investments in research and development, supportive government policies, and a growing awareness of the potential benefits of edge computing. The market is characterized by a competitive landscape with both established players and emerging startups vying for market share. Key trends include the development of energy-efficient edge devices, the adoption of AIoT platforms, and the growing emphasis on cybersecurity. The demand for customized solutions tailored to specific industry needs is also a significant factor shaping the market dynamics.

Europe

Europe’s Edge AI Embedded Systems Market is steadily expanding, fueled by a strong focus on innovation and a well-established industrial base. The region’s emphasis on data privacy and security is driving demand for secure edge solutions. Key applications include smart manufacturing, logistics, and public safety. Government initiatives promoting digital transformation are also contributing to market growth.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for Edge AI Embedded Systems. This growth is propelled by rapid industrialization, increasing urbanization, and significant investments in smart city initiatives. China, Japan, and South Korea are leading markets in the region, with a strong focus on AI-powered manufacturing and infrastructure development.

South America

South America’s Edge AI Embedded Systems Market is emerging, driven by growing adoption of IoT and automation technologies. Key applications are emerging in agriculture, mining, and logistics. The region presents significant growth opportunities for companies offering cost-effective and scalable edge solutions.

Middle East & Africa

The Edge AI Embedded Systems Market in the Middle East & Africa is experiencing moderate growth, driven by increasing investments in smart infrastructure and digital transformation. The region presents opportunities in areas such as smart grids, transportation, and healthcare.

Report Scope

This market research report provides a comprehensive analysis of the Edge AI Embedded Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Edge AI Embedded Systems Market?

-> Edge AI Embedded Systems Market was valued at USD 6.2 billion in 2025 and is expected to reach USD 12.8 billion by 2034.

Which key companies operate in Edge AI Embedded Systems Market?

-> Key players include NVIDIA®, Intel®, Qualcomm®, Arm®, and Google, among others.

What are the key growth drivers?

-> Key growth drivers include the need for lower latency, reduced bandwidth costs, enhanced data privacy, and the rising adoption of autonomous vehicles, smart manufacturing, and wearable health monitors.

Which region dominates the market?

-> The reference does not provide specific regional dominance details.

What are the emerging trends?

-> Emerging trends include integration of AI with IoT at the edge, development of low‑power processors and neural‑network accelerators, and strategic partnerships that expand edge‑AI service offerings.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...