MARKET INSIGHTS

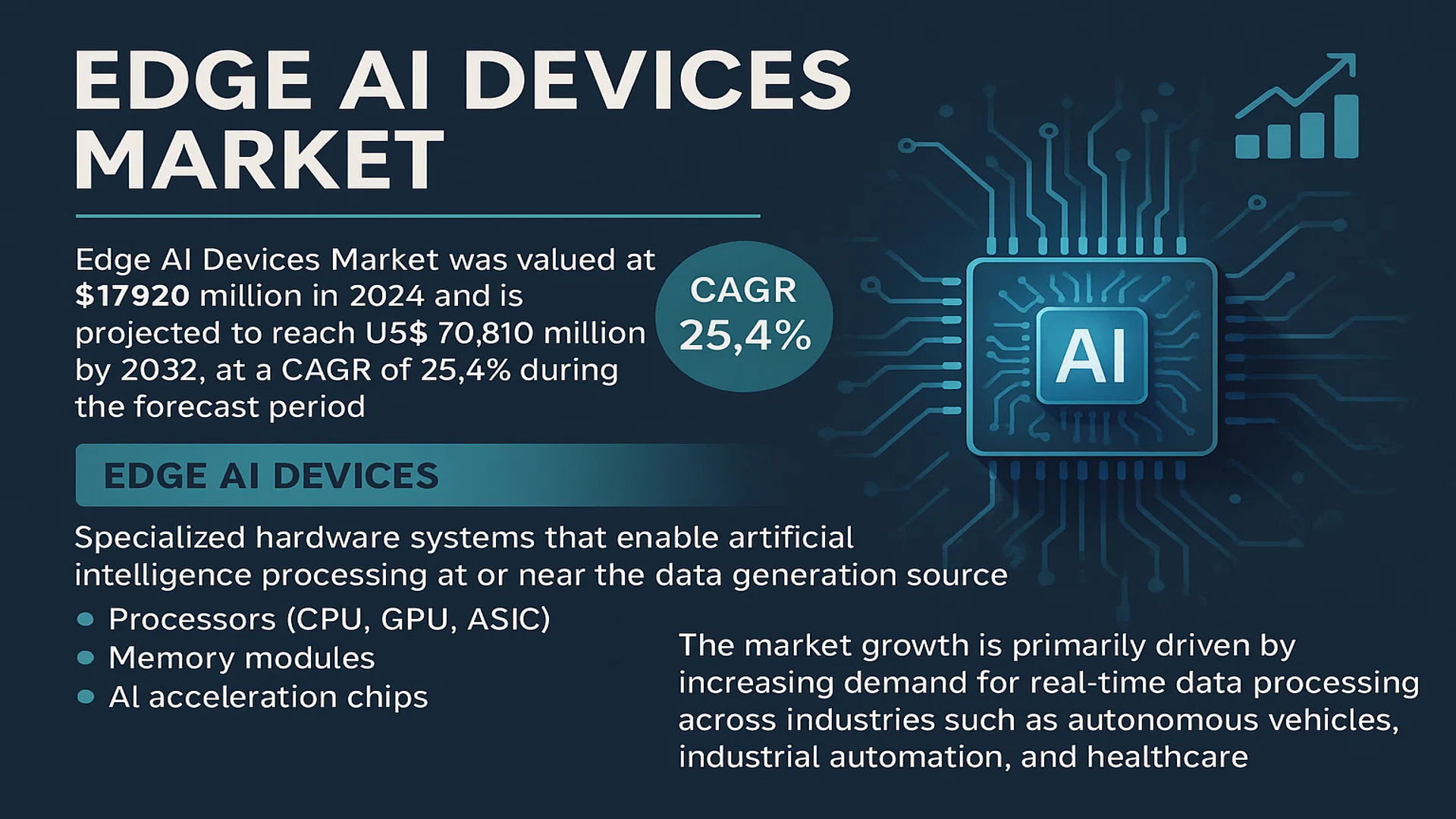

The global Edge AI Devices Market was valued at 17920 million in 2024 and is projected to reach US$ 70810 million by 2032, at a CAGR of 25.4% during the forecast period.

Edge AI Devices are specialized hardware systems that enable artificial intelligence processing at or near the data generation source. These devices eliminate the need to transmit all data to centralized cloud servers by performing computations locally on edge nodes or embedded systems. Key components include processors (CPU, GPU, ASIC), memory modules, and AI acceleration chips designed for tasks like computer vision, natural language processing, and predictive analytics.

The market growth is primarily driven by increasing demand for real-time data processing across industries such as autonomous vehicles, industrial automation, and healthcare. The shift towards decentralized computing architectures to reduce latency and improve data privacy is accelerating adoption. Technological advancements in AI chipsets by key players like NVIDIA (with their Jetson platform) and Intel (through Habana Labs acquisitions) are further propelling market expansion. North America currently leads in market share due to strong enterprise AI adoption, while Asia-Pacific is expected to witness the fastest growth owing to rapid industrial digitization.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Real-Time AI Processing to Accelerate Edge AI Adoption

The global Edge AI Devices market is experiencing robust growth, projected to grow from $17.92 billion in 2024 to $70.81 billion by 2032 at a 25.4% CAGR. This surge is primarily driven by industries requiring real-time data processing with minimal latency. Autonomous vehicles, for instance, rely on Edge AI for instant decision-making, where even milliseconds of delay could lead to accidents. Similarly, industrial automation systems use Edge AI for predictive maintenance, analyzing equipment sensor data locally to prevent costly downtime. The healthcare sector benefits through AI-powered diagnostic tools that process patient data securely at the point-of-care without relying on cloud connectivity.

Stringent Data Privacy Regulations Fueling Edge Computing Investments

Global data protection laws like GDPR and HIPAA are compelling organizations to adopt Edge AI solutions that minimize sensitive data transmission. With over 150 data privacy regulations enacted worldwide since 2020, enterprises increasingly prefer processing data locally rather than risking exposure through cloud transmission. Financial institutions are deploying Edge AI for fraud detection, while hospitals use it for analyzing medical images directly on devices. This regulatory push aligns with consumer expectations – recent studies show 78% of users prioritize data privacy when choosing digital services.

Additionally, the rapid development of 5G networks creates synergy with Edge AI by enabling efficient distribution of computing tasks between devices and nearby edge servers. This combination allows complex AI models to run partially on devices while offloading intensive computations to nearby infrastructure, optimizing both performance and energy efficiency.

MARKET RESTRAINTS

High Development Costs and Hardware Limitations Pose Adoption Barriers

Despite strong demand, Edge AI adoption faces significant cost challenges. Developing specialized AI chips for edge devices requires investments exceeding $100 million for cutting-edge designs, limiting participation to major semiconductor players. Even established players face yield issues, with new AI accelerator architectures often achieving less than 60% production efficiency in initial manufacturing runs. These costs ultimately impact end-product pricing, making edge AI solutions prohibitively expensive for many small and medium enterprises.

The technology also grapples with inherent hardware constraints. Edge devices must balance three competing priorities: computational power, energy efficiency, and physical size. Current AI models often require trade-offs – a device might excel at image recognition but lack sufficient memory for natural language processing. Memory bandwidth limitations create bottlenecks, as many edge processors can only support a fraction of the data throughput needed for complex neural networks.

MARKET CHALLENGES

Fragmented Ecosystem and Standardization Issues Challenge Market Growth

The Edge AI landscape suffers from ecosystem fragmentation, with incompatible frameworks and toolchains across different hardware platforms. Developers must frequently modify AI models for each processor architecture, significantly increasing time-to-market. The lack of universal standards means a model optimized for one vendor’s AI accelerator may perform poorly on another, despite similar specifications. This fragmentation discourages investment, as enterprises fear vendor lock-in or premature technology obsolescence.

Simultaneously, the industry faces a severe talent shortage. Training staff to develop edge-optimized AI models requires expertise in both machine learning and embedded systems – a rare combination. Educational institutions struggle to keep pace with the rapidly evolving technology, creating a workforce gap estimated at over 1 million qualified professionals globally.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare and Smart Cities Offer Significant Growth Potential

Edge AI presents transformative opportunities in healthcare through portable diagnostic devices. AI-enabled ultrasound systems, for example, can provide immediate analyses in remote areas without internet connectivity. Similarly, wearable health monitors with embedded AI can detect irregular heart rhythms and alert users in real-time. The global market for AI-powered medical devices is projected to exceed $20 billion by 2027, with edge-based solutions capturing an increasing share.

Smart city infrastructure represents another promising opportunity. Cities worldwide are deploying edge AI for traffic management, analyzing video feeds from intersections to optimize light timing and reduce congestion. Environmental monitoring systems use edge processing to track air quality across urban areas while minimizing data transmission costs. These applications benefit from government smart city initiatives, with investments in such technologies growing at over 15% annually.

The industrial sector continues to innovate with Edge AI, particularly in quality control applications. Manufacturing plants are implementing vision systems that inspect products on production lines, detecting defects with greater accuracy than human workers. These systems can process thousands of images per minute locally, eliminating the latency of cloud-based alternatives while protecting proprietary manufacturing data.

EDGE AI DEVICES MARKET TRENDS

Smart Manufacturing and Automation to Drive Demand for Edge AI Devices

The rapid adoption of Industry 4.0 and smart manufacturing technologies is accelerating the deployment of Edge AI devices in industrial automation. By processing data locally, these devices enable real-time decision-making for predictive maintenance, quality control, and robotics. The growing emphasis on reducing operational downtime in manufacturing has led to significant investments in Edge AI, with the industrial automation segment expected to contribute over 30% of the total market revenue by 2030. Furthermore, advancements in sensor technologies and AI algorithms are enhancing the capabilities of Edge devices in complex industrial environments.

Other Trends

Healthcare Sector Leveraging Edge AI for Real-Time Diagnostics

In the healthcare sector, Edge AI is revolutionizing medical imaging, wearables, and remote patient monitoring. The ability to process sensitive patient data locally while maintaining compliance with privacy regulations makes Edge AI a preferred solution. For instance, AI-powered portable diagnostic tools can analyze medical images at the point of care with accuracy levels exceeding 92%, significantly reducing diagnosis times. The growing geriatric population and increasing chronic disease prevalence are further fueling market expansion in this segment.

Autonomous Vehicles Pushing the Boundaries of Edge Computing

The autonomous vehicle sector represents one of the most demanding applications for Edge AI, requiring ultra-low latency processing of vast sensor data streams. Leading automotive manufacturers are integrating powerful Edge AI processors capable of delivering over 100 TOPS (Tera Operations Per Second) to enable real-time object detection and path planning. The rising demand for advanced driver-assistance systems (ADAS) and Level 4 autonomous vehicles is projected to drive the automotive Edge AI market to grow at a CAGR of 28.7% through 2032. This growth is further supported by government initiatives promoting smart transportation infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Tech Giants and Semiconductor Innovators Dominate the Edge AI Market

The global Edge AI Devices market exhibits a dynamic and highly competitive landscape, dominated by established semiconductor giants and rapidly growing tech innovators. NVIDIA leads the market with its powerful GPU-based solutions, capturing nearly 23% of the revenue share in 2024, primarily due to its unmatched parallel processing capabilities that are critical for AI workloads at the edge. Their Jetson series has become a benchmark in industrial and automotive edge computing applications.

Following closely, Intel and Qualcomm command significant market presence with their specialized AI chipsets. Intel’s OpenVINO toolkit and Qualcomm’s AI Engine have become industry standards for optimizing AI models on edge devices. Meanwhile, Huawei has shown remarkable growth in the Asian markets with its Ascend chips, challenging traditional players through aggressive pricing and regional partnerships.

The competitive scenario is further intensified by tech behemoths like Google and Apple, who are vertically integrating edge AI capabilities into their ecosystems. Google’s Tensor Processing Units (TPUs) and Apple’s Neural Engine demonstrate how software-hardware co-design can deliver superior performance-per-watt ratios, a crucial factor for battery-powered edge devices.

Strategic Developments Shaping the Market

Recent years have witnessed strategic realignments as companies position themselves for the edge computing revolution. NVIDIA’s acquisition of ARM (though ultimately unsuccessful) highlighted the industry’s recognition of energy-efficient processor architectures for edge applications. Similarly, AMD has made significant inroads through its acquisition of Xilinx, combining CPU/GPU strengths with FPGA flexibility ideal for adaptable edge solutions.

Emerging players are carving niches in specific segments – Samsung with its Exynos processors excel in mobile edge applications, while Texas Instruments dominates industrial edge nodes with its ultra-low-power processors. The market also sees increasing specialization, with companies like ARM focusing on licensing energy-efficient designs and IBM bringing enterprise-grade AI acceleration to the edge.

List of Key Edge AI Device Companies Profiled

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Google LLC (U.S.)

- Apple Inc. (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Samsung Electronics (South Korea)

- Texas Instruments Incorporated (U.S.)

- ARM Limited (U.K.)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

Segment Analysis:

By Type

GPU-Based Edge AI Devices Lead the Market Due to High Processing Efficiency

The market is segmented based on type into:

- CPU based

- GPU based

- ASIC based

- Others

By Application

Autonomous Driving Segment Dominates Due to Rising Adoption of AI in Vehicles

The market is segmented based on application into:

- Autonomous Driving

- Industrial Automation

- Healthcare

- Other

By End-User Industry

Manufacturing Sector Leads Due to Growing AI Integration in Smart Factories

The market is segmented based on end-user industry into:

- Manufacturing

- Automotive

- Healthcare

- Consumer Electronics

- Others

By Component

Hardware Segment Dominates Market Share Due to Rising Demand for Edge AI Processors

The market is segmented based on component into:

- Hardware

- Subtypes: Processors, Sensors, Memory Units, and others

- Software

- Services

Regional Analysis: Edge AI Devices Market

North America

North America dominates the Edge AI Devices market, primarily driven by rapid technological adoption in the U.S. and Canada. The region benefits from strong investments in AI infrastructure, with companies like NVIDIA, Intel, and Qualcomm leading innovation. The growing deployment of Edge AI in autonomous vehicles, smart manufacturing, and healthcare applications is accelerating market expansion. The U.S. government’s increasing focus on AI research initiatives, including funding through the CHIPS and Science Act, further strengthens the ecosystem. However, data privacy regulations, such as CCPA, create compliance challenges for Edge AI developers.

Asia-Pacific

The Asia-Pacific region is experiencing the fastest growth in Edge AI adoption, propelled by China’s aggressive AI investments and India’s expanding IoT landscape. Chinese tech giants like Huawei and Alibaba are heavily investing in Edge AI chipsets for smart cities and industrial automation. Japan and South Korea contribute significantly to the market through advancements in robotics and 5G-integrated Edge devices. While cost sensitivity remains a barrier in some markets, governments are actively promoting digital transformation, making APAC a high-potential region for future Edge AI expansion.

Europe

Europe’s Edge AI market is driven by stringent data protection laws (GDPR) that incentivize localized AI processing to ensure compliance. The region shows strong demand for Edge AI in industrial automation and healthcare, supported by Germany’s Industry 4.0 initiatives and the UK’s AI strategy framework. Though technological adoption is slower compared to North America, the EU’s focus on ethical AI and increasing 5G network coverage is creating opportunities. However, regulatory complexities and fragmented standards across member states pose challenges for uniform market growth.

Middle East & Africa

The MEA region is gradually adopting Edge AI solutions, with the UAE and Saudi Arabia leading in smart city projects and digital infrastructure development. Edge AI applications in oil & gas predictive maintenance and surveillance systems are gaining traction. While investments are rising, limited technical expertise and infrastructure gaps in certain countries restrain broader adoption. Government-backed initiatives like Saudi Vision 2030 and UAE’s AI Strategy 2031 indicate long-term commitment to building an AI-driven economy in the region.

South America

South America presents emerging opportunities in the Edge AI market, though adoption remains behind other regions due to economic instability and limited R&D investments. Brazil shows potential in agricultural AI applications and smart manufacturing, while Argentina focuses on fintech innovations. The lack of widespread 5G availability and skilled workforce shortages are key barriers. However, increasing foreign investments in technology hubs, particularly in Chile and Colombia, signal gradual market maturation.

Report Scope

This market research report provides a comprehensive analysis of the Global Edge AI Devices Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 17,920 million in 2024 and is projected to reach USD 70,810 million by 2032 at a CAGR of 25.4%.

- Segmentation Analysis: Detailed breakdown by product type (CPU-based, GPU-based, ASIC-based, Others), application (Autonomous Driving, Industrial Automation, Healthcare, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants including NVIDIA, Intel, Qualcomm, Google, Apple, AMD, Huawei, Samsung, Texas Instruments, ARM, IBM, Microsoft, and AWS, covering their product portfolios and strategic initiatives.

- Technology Trends & Innovation: Assessment of AI acceleration at the edge, low-power processing architectures, and the integration of machine learning capabilities in endpoint devices.

- Market Drivers & Restraints: Evaluation of factors such as demand for real-time processing, privacy concerns, 5G deployment, and challenges in power efficiency and thermal management.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, device OEMs, software developers, and enterprise adopters regarding market opportunities and technology roadmaps.

The research methodology combines primary interviews with industry experts and analysis of verified market data from reputable sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Edge AI Devices Market?

-> Edge AI Devices Market was valued at 17920 million in 2024 and is projected to reach US$ 70810 million by 2032, at a CAGR of 25.4% during the forecast period.

Which key companies operate in Global Edge AI Devices Market?

-> Key players include NVIDIA, Intel, Qualcomm, Google, Apple, AMD, Huawei, Samsung, Texas Instruments, ARM, IBM, Microsoft, and Amazon Web Services (AWS).

What are the key growth drivers?

-> Growth is driven by demand for real-time AI processing, increasing IoT adoption, privacy regulations requiring local data processing, and 5G network expansion enabling edge computing.

Which region dominates the market?

-> North America currently leads in adoption, while Asia-Pacific is expected to grow at the fastest rate due to manufacturing capabilities and government AI initiatives.

What are the emerging trends?

-> Emerging trends include AI-optimized ASICs, federated learning at the edge, energy-efficient neural processors, and the integration of edge AI in autonomous vehicles and smart cities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...