MARKET INSIGHTS

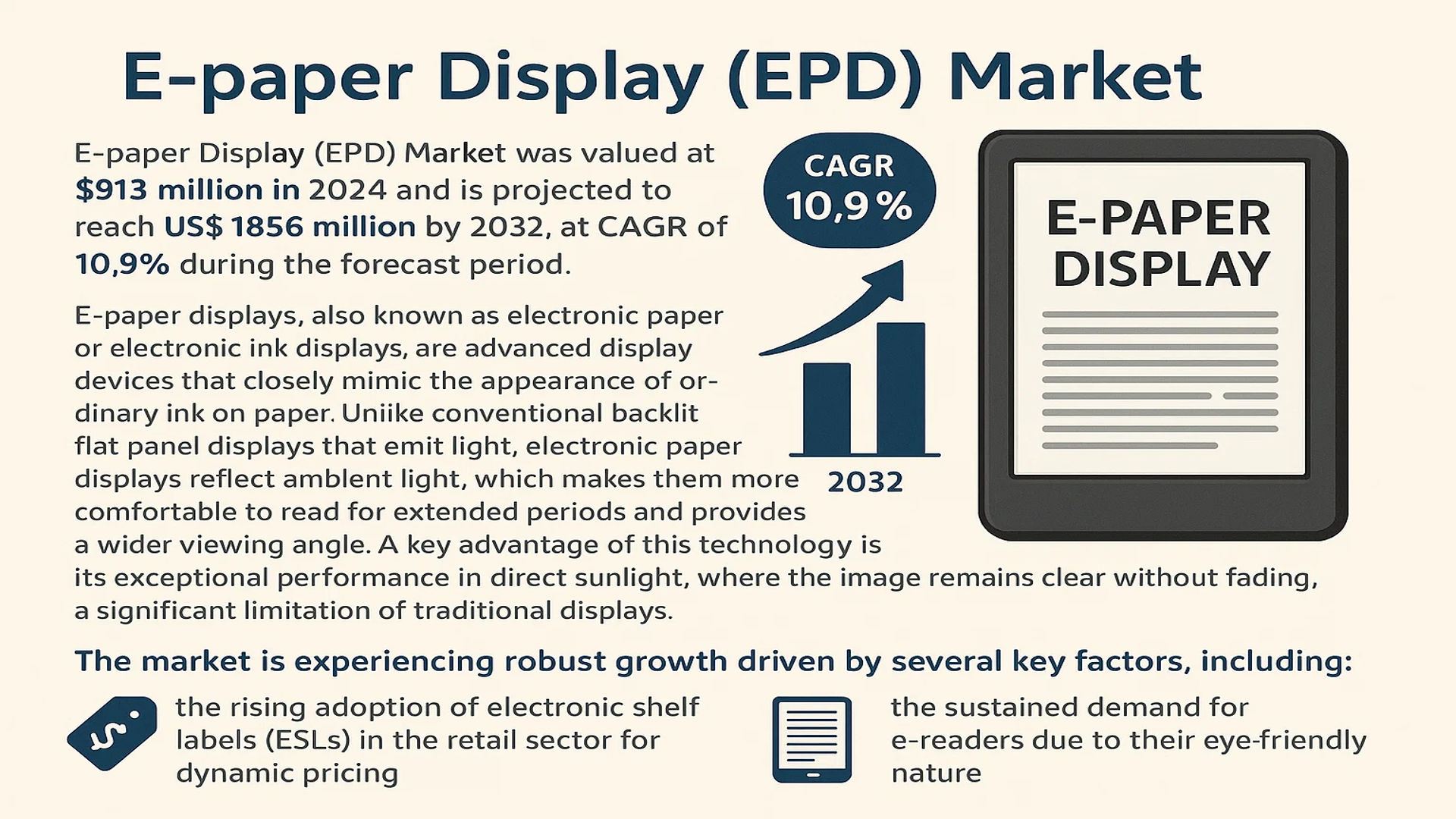

The global E-paper Display (EPD) Market was valued at 913 million in 2024 and is projected to reach US$ 1856 million by 2032, at a CAGR of 10.9% during the forecast period.

E-paper displays, also known as electronic paper or electronic ink displays, are advanced display devices that closely mimic the appearance of ordinary ink on paper. Unlike conventional backlit flat panel displays that emit light, electronic paper displays reflect ambient light, which makes them more comfortable to read for extended periods and provides a wider viewing angle. A key advantage of this technology is its exceptional performance in direct sunlight, where the image remains clear without fading, a significant limitation of traditional displays.

The market is experiencing robust growth driven by several key factors, including the rising adoption of electronic shelf labels (ESLs) in the retail sector for dynamic pricing and the sustained demand for e-readers due to their eye-friendly nature. Furthermore, advancements in flexible and color EPD technologies are opening new applications in wearables, public transportation signage, and smart logistics. The market is also highly concentrated, with the top five manufacturers holding a collective market share exceeding 80%. E Ink Holdings Inc. is the dominant player, with other significant contributors including LG Display, Pervasive Displays, and OED Technologies.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Display Solutions to Propel Market Growth

The global push toward sustainability and energy conservation is significantly driving the adoption of E-paper Display (EPD) technology. Unlike conventional LCD or OLED displays that require constant power to maintain images, EPDs consume power only during image changes, making them exceptionally energy-efficient. This characteristic is particularly valuable in applications requiring always-on displays, such as electronic shelf labels (ESLs) and digital signage. The retail sector’s growing emphasis on reducing energy consumption—where traditional displays can account for up to 40% of a store’s energy usage—is accelerating EPD integration. With global energy costs rising and sustainability regulations tightening, businesses are increasingly adopting EPD solutions to lower operational expenses and meet environmental targets.

Expansion of IoT and Smart Infrastructure to Boost EPD Adoption

The rapid growth of the Internet of Things (IoT) ecosystem and smart city initiatives worldwide is creating substantial opportunities for E-paper displays. EPDs are ideal for IoT applications due to their low power consumption, sunlight readability, and ability to operate for extended periods without maintenance. Smart transportation systems, for instance, are deploying EPDs in electronic bus stop signs and railway information displays, where visibility in direct sunlight and minimal power requirements are critical. The global IoT market’s expansion, projected to connect over 29 billion devices by 2030, is driving demand for energy-efficient display technologies that can operate reliably in diverse environmental conditions without frequent battery replacements or external power sources.

Furthermore, innovations in flexible and large-format EPDs are enabling new applications in smart packaging, wearable technology, and architectural integration, expanding the technology’s reach beyond traditional e-readers and retail labels.

➤ For instance, several European cities have implemented solar-powered EPD information kiosks that operate continuously without grid connection, demonstrating the technology’s suitability for sustainable urban infrastructure.

The convergence of EPD technology with energy harvesting systems and low-power wireless communication protocols is further enhancing its value proposition for distributed IoT applications, positioning it as a key enabling technology for the next generation of smart devices and infrastructure.

MARKET CHALLENGES

Limited Color Reproduction and Refresh Rates to Constrain Application Scope

Despite significant advancements, E-paper displays face inherent technological limitations that challenge their adoption in certain applications. The most prominent constraint is the limited color reproduction capability compared to emissive display technologies. While recent developments have introduced color EPDs, they typically offer a limited color gamut and lower saturation levels than LCD or OLED alternatives. This restriction makes them less suitable for applications requiring vibrant multimedia content or detailed color graphics. Additionally, the relatively slow refresh rates of EPD technology—typically ranging from 500 milliseconds to several seconds—create challenges for dynamic content applications where real-time updates are essential.

Other Challenges

Manufacturing Scale and Cost Efficiency

The specialized manufacturing processes required for EPD production present scalability challenges. While the market has grown substantially, production volumes remain significantly lower than those of mainstream display technologies, resulting in higher per-unit costs. The complex layer structure involving microcapsules or electrophoretic fluids requires precise manufacturing conditions and specialized equipment, limiting the number of facilities capable of mass production. This manufacturing complexity contributes to cost structures that are approximately 30-40% higher than comparable-sized LCD panels, creating adoption barriers in price-sensitive market segments.

Environmental Sensitivity and Durability Concerns

EPD performance can be affected by extreme environmental conditions, particularly temperature variations. The electrophoretic fluids or electronic inks used in these displays have operational temperature ranges typically between 0°C and 50°C, limiting deployment in harsh environments. Additionally, while EPDs excel in sunlight readability, prolonged exposure to UV radiation can gradually degrade display performance over time. These environmental sensitivities require careful consideration in outdoor applications and necessitate protective measures that can increase total system costs.

MARKET RESTRAINTS

Competition from Advanced Display Technologies to Limit Market Penetration

The E-paper display market faces intense competition from continually improving alternative display technologies. LCD manufacturers have developed ultra-low-power variants that approach EPD’s energy efficiency while offering superior color performance and refresh rates. Similarly, OLED technology advancements have produced reflective and low-power variants that challenge EPD’s value proposition in certain applications. These competing technologies benefit from massive manufacturing scale and ongoing R&D investments driven by consumer electronics markets, enabling rapid cost reductions and performance improvements that EPD manufacturers struggle to match.

Furthermore, the development of hybrid display solutions that combine EPD with other technologies creates competitive pressure. Some manufacturers are integrating partial EPD elements with conventional displays to achieve energy savings while maintaining performance characteristics, potentially reducing the market for pure EPD solutions in applications where compromise is acceptable.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare and Education to Create New Growth Pathways

The healthcare and education sectors present significant growth opportunities for E-paper display technology. In healthcare, EPDs are increasingly used for patient wristbands, medical signage, and portable diagnostic equipment displays where readability, low power consumption, and sterilization compatibility are critical requirements. The global healthcare digitization trend, accelerated by the need for contactless solutions and efficient patient management systems, is driving adoption of EPD-based solutions that can operate for years without battery replacement while maintaining clear information display.

In educational applications, EPD technology enables the development of digital textbooks and note-taking devices that mimic paper’s readability while providing digital convenience. The growing adoption of digital learning platforms and the push toward reducing paper consumption in educational institutions create favorable conditions for EPD integration. Several educational technology providers have launched E-paper based devices specifically designed for academic use, combining the eye comfort of paper with the functionality of digital devices.

Additionally, the development of advanced EPD technologies with improved color capabilities, faster refresh rates, and flexible form factors is opening new application areas in consumer electronics, automotive displays, and smart packaging. These technological advancements, combined with growing environmental awareness and regulatory support for energy-efficient technologies, position EPD for expanded market penetration across multiple sectors.

E-PAPER DISPLAY (EPD) MARKET TRENDS

Advancements in Color and Flexible EPD Technology to Emerge as a Trend in the Market

Advancements in color and flexible electronic paper display technology are fundamentally reshaping the market landscape and expanding its application potential. While traditional monochrome EPDs have dominated e-readers for years, the recent commercial rollout of advanced color e-paper, such as E Ink’s Gallery™ Palette and Print Color ePaper, is unlocking new verticals. These technologies utilize advanced color filter arrays and improved pigments to achieve a color gamut that is increasingly viable for retail signage and educational tools. Furthermore, the development of truly flexible and even rollable e-paper substrates is progressing beyond the prototype stage. This evolution is crucial because it enables integration into non-traditional form factors, such as curved smart surfaces on consumer electronics and wearable devices, creating a new addressable market beyond rigid displays. While the initial cost premium remains a barrier, manufacturing efficiencies are expected to bring these advanced displays into more competitive price points, further accelerating adoption.

Other Trends

Sustainability and Energy Efficiency Driving Retail Adoption

The global push for sustainability and energy efficiency is a powerful driver for EPD adoption, particularly within the retail sector for Electronic Shelf Labels (ESLs). Unlike conventional LCD or LED price tags, EPDs consume power only when the image is changed, leading to exceptionally low energy consumption. A single ESL can operate for up to five years on a small coin-cell battery, eliminating the need for wiring and reducing maintenance costs. This energy-saving characteristic is a significant operational advantage for large retail chains managing thousands of labels. Consequently, the ESL segment is experiencing robust growth, with deployments accelerating in Europe and North America as retailers seek to modernize stores, enable dynamic pricing, and bolster their green credentials. The scalability of these systems makes them an attractive investment for achieving long-term operational efficiency.

Expansion into New Application Verticals Beyond E-Readers

The expansion of E-paper displays into new application verticals beyond the mature e-reader market is a defining trend for future growth. While e-readers still account for a substantial portion of the market, innovation is fueling penetration into diverse fields. In transportation and logistics, EPDs are being widely adopted for smart baggage tags at airports and parcel tracking labels, valued for their durability and long battery life. The healthcare sector is utilizing them for patient bed charts and medical wristbands because they reduce screen fatigue and can be updated wirelessly. Furthermore, the architecture, engineering, and construction (AEC) industry is exploring their use in dynamic blueprints and site signage. This diversification is critical for the market’s health because it reduces reliance on a single application and taps into the growing Internet of Things (IoT) ecosystem, where always-on, low-power displays are essential.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global E-paper Display (EPD) market exhibits a semi-consolidated competitive structure, characterized by a mix of dominant technology innovators and specialized manufacturers vying for market share. E Ink Holdings Inc. stands as the undisputed market leader, commanding a significant portion of global revenues due to its pioneering electrophoretic display technology and extensive patent portfolio. The company’s strategic partnerships with major e-reader brands and expansion into retail electronic shelf labels (ESLs) have solidified its position, particularly across Asia and North America.

LG Display and Pervasive Displays also hold considerable market influence, driven by their advanced manufacturing capabilities and diverse application focus. LG Display’s investment in large-format EPDs for advertising and public transport signage, combined with Pervasive Displays’ strength in the e-reader and IoT device segments, has enabled both companies to capture substantial value in this growing market. Their growth is further propelled by continuous innovation in display resolution, color technology, and energy efficiency.

Additionally, these industry leaders are actively pursuing growth through geographical expansion and new product launches. For instance, recent developments include the introduction of flexible E-paper displays and advanced color e-paper technologies, which are expected to open new application avenues in wearable technology and smart packaging. Such initiatives are anticipated to significantly enhance their market presence over the coming years.

Meanwhile, players like Qualcomm (through its Mirasol display technology) and Plastic Logic are strengthening their positions through substantial R&D investments and strategic collaborations. Qualcomm’s focus on low-power, high-refresh-rate displays for smartwatches and IoT devices, and Plastic Logic’s development of ultra-thin, flexible EPDs for niche applications, demonstrate the diverse strategies employed to compete and innovate in this dynamic landscape.

List of Key E-paper Display (EPD) Companies Profiled

- E Ink Holdings Inc. (Taiwan)

- LG Display Co., Ltd. (South Korea)

- Pervasive Displays Inc. (Taiwan)

- Qualcomm Technologies, Inc. (U.S.)

- Liquavista B.V. (Netherlands)

- Plastic Logic GmbH (Germany)

- OED Technologies Co., Ltd. (China)

- Gamma Dynamics (U.S.)

- Industrial Technology Research Institute (ITRI) (Taiwan)

Segment Analysis:

By Technology

Electrophoretic Display (EPD) Segment Dominates the Market Due to its Mature Technology and Widespread Adoption in E-Readers

The market is segmented based on technology into:

- Electrophoretic Display (EPD)

- Subtypes: Microcapsule, Microcup, and others

- Electrowetting Display (EWD)

- Electrochromic Display (ECD)

- Cholesteric Liquid Crystal Display (Ch-LCD)

- Others

By Application

E-Reader Segment Leads Due to High Consumer Demand for Low-Power, Eye-Friendly Reading Devices

The market is segmented based on application into:

- E-Reader

- Electronic Shelf Label (ESL)

- Wearables

- Subtypes: Smartwatches, Fitness trackers, and others

- Public and Retail Signage

- Others

By Size

Medium-Sized Displays Hold Significant Share Owing to their Versatility Across Key Applications

The market is segmented based on size into:

- Small (Less than 6 inches)

- Medium (6 inches to 10 inches)

- Large (More than 10 inches)

By Substrate

Glass Substrate Segment is Prevalent Due to its Rigidity and Established Manufacturing Processes

The market is segmented based on substrate into:

- Glass

- Plastic/Flexible

- Metal

- Others

Regional Analysis: E-paper Display (EPD) Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the E-paper Display market, accounting for over 60% of global consumption by volume. This dominance is primarily driven by China, which alone represents the largest single market, followed by significant manufacturing and consumption hubs in Taiwan and South Korea. The region’s leadership is underpinned by its massive electronics manufacturing ecosystem, which produces the vast majority of the world’s e-readers. Furthermore, the rapid adoption of Electronic Shelf Labels (ESLs) in the retail sectors of countries like China, Japan, and South Korea, fueled by urbanization and the push for smart retail infrastructure, is a major growth driver. While cost sensitivity remains a factor, the region is also a hotbed for innovation, with local players and major global manufacturers like E Ink (headquartered in Taiwan) driving advancements in display technology.

North America

North America represents a mature and high-value market for EPD technology, characterized by strong demand for premium e-reading devices and early adoption of innovative applications. The United States is the core of this region, with a consumer base that has a high affinity for technology and a retail sector increasingly investing in digitalization through Electronic Shelf Labels for dynamic pricing and inventory management. Significant potential exists in niche applications such as smart home displays, wearable technology, and digital signage in corporate and public spaces. The market is driven by a focus on energy efficiency, the superior readability of E-paper, and sustainability initiatives, as these displays consume power only when the image changes. Leading technology companies and retailers in the region are key partners for EPD manufacturers.

Europe

Europe is a steadily growing market for E-paper displays, with demand largely fueled by stringent environmental regulations and a strong focus on sustainability. The region’s well-established retail sector, particularly in Western European nations like Germany, France, and the UK, is a primary adopter of Electronic Shelf Label systems to enhance operational efficiency and reduce paper waste. Furthermore, European consumers show a high propensity for e-readers, supporting a stable market for EPDs in that segment. The market is also seeing increased integration in public transportation systems for passenger information displays and in smart city infrastructure. Innovation is key, with research institutions and companies exploring advanced color E-paper and flexible display applications, aligning with the region’s broader goals of energy conservation and technological advancement.

South America

The E-paper Display market in South America is nascent but shows promising long-term growth potential. Economic volatility and infrastructure challenges have historically slowed the widespread adoption of newer technologies. However, the region’s large and growing retail sector, especially in major economies like Brazil and Argentina, presents a significant opportunity for Electronic Shelf Labels as a tool for modernization and efficiency. The adoption rate is gradual, often hindered by higher initial costs compared to traditional paper labels and a need for greater awareness of the long-term ROI. As economic conditions stabilize and digital infrastructure improves, the market is expected to gain momentum, driven by the need for retail automation and the growing popularity of e-books.

Middle East & Africa

The Middle East and Africa region represents an emerging market for E-paper displays, with growth currently concentrated in more developed economies and specific sectors. In the Middle East, particularly in Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia, investments in smart city projects and modern retail infrastructure are creating demand for ESLs and informational displays. The African market is at a much earlier stage of development, with adoption limited by infrastructure gaps and economic constraints. However, the region’s overall potential is significant, driven by a young, tech-savvy population and ongoing urbanization. The long-term outlook is positive, with growth expected to accelerate as digital penetration increases and the benefits of low-power, sunlight-readable displays become more widely recognized.

Report Scope

This market research report provides a comprehensive analysis of the global and regional E-paper Display (EPD) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global E-paper Display (EPD) Market?

-> E-paper Display (EPD) Market was valued at 913 million in 2024 and is projected to reach US$ 1856 million by 2032, at a CAGR of 10.9% during the forecast period.

Which key companies operate in Global E-paper Display (EPD) Market?

-> Key players include E Ink, LG Display, Liquavistar, Pervisive Displays, and OED, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient displays, expansion of the e-reader market, and adoption in retail for electronic shelf labels.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China holding over 60% share, followed by China Taiwan.

What are the emerging trends?

-> Emerging trends include development of color EPD technology, flexible substrates, and integration into IoT devices and smart packaging.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...