MARKET INSIGHTS

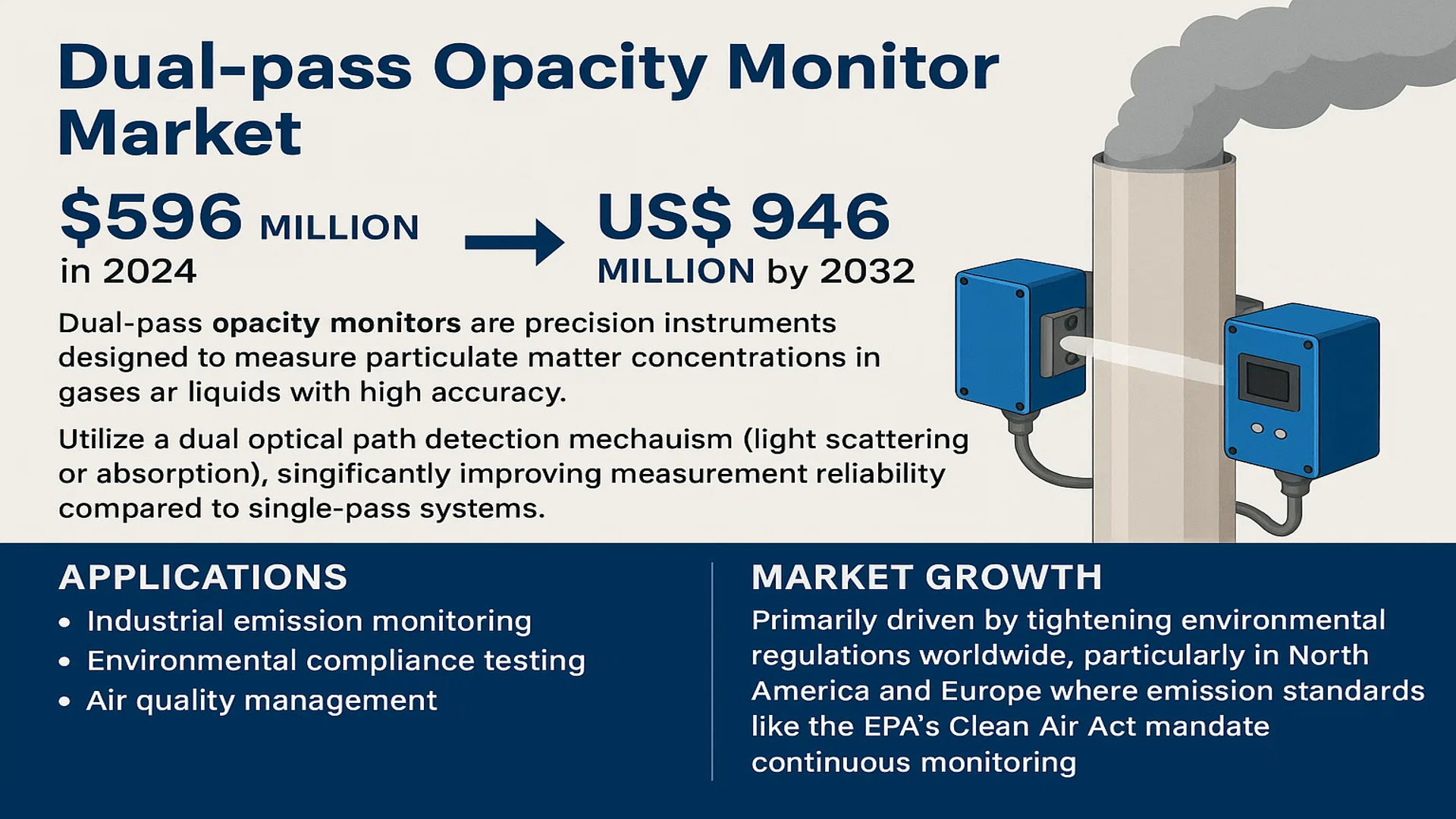

The global Dual-pass Opacity Monitor Market was valued at 596 million in 2024 and is projected to reach US$ 946 million by 2032, at a CAGR of 6.9% during the forecast period.

Dual-pass opacity monitors are precision instruments designed to measure particulate matter concentrations in gases or liquids with high accuracy. These devices utilize a dual optical path detection mechanism (light scattering or absorption), significantly improving measurement reliability compared to single-pass systems. They play a critical role in industrial emission monitoring, environmental compliance testing, and air quality management across sectors like power generation, manufacturing, and waste incineration.

Market growth is primarily driven by tightening environmental regulations worldwide, particularly in North America and Europe where emission standards like the EPA’s Clean Air Act mandate continuous monitoring. The light scattering method segment currently dominates the technology landscape due to its superior sensitivity for fine particulate detection. Meanwhile, Asia-Pacific emerges as the fastest-growing regional market, with China’s industrial expansion and air pollution control initiatives contributing significantly to demand. Key industry players including AMETEK Land, SICK, and Durag are expanding their product portfolios with advanced IoT-enabled monitors to capitalize on this growth.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations Fuel Adoption of Dual-Pass Opacity Monitors

The global push towards cleaner air quality has led to the implementation of stringent emission standards across industries, significantly driving demand for precise monitoring solutions. Governments worldwide are enforcing lower particulate matter (PM) thresholds, with many regions now requiring continuous opacity monitoring for compliance. For example, recent updates to industrial emission standards now mandate real-time particulate monitoring in power plants, cement factories, and chemical processing units. This regulatory pressure compels industries to adopt advanced dual-pass opacity monitors that provide the required measurement accuracy and reliability.

Growing Industrialization in Emerging Markets Creates Sustained Demand

Rapid industrialization across developing economies presents a significant growth opportunity for the dual-pass opacity monitor market. Regions like Asia-Pacific are witnessing unprecedented industrial expansion, particularly in sectors that generate substantial particulate emissions. Manufacturing output in these markets has grown significantly, necessitating advanced monitoring equipment to comply with both local and international environmental standards. The superior accuracy of dual-pass technology compared to single-pass systems makes it the preferred choice for industries facing increasing regulatory scrutiny.

Technological Advancements Enhance Performance and Reliability

Continuous innovations in optical measurement technologies are elevating the capabilities of dual-pass opacity monitors. Modern systems now incorporate advanced signal processing algorithms, improved optical components, and enhanced self-diagnostic features. These technological improvements result in higher measurement precision, reduced maintenance requirements, and better performance in challenging industrial environments. The development of smart monitoring systems with predictive maintenance capabilities further increases their value proposition for industrial operators.

MARKET RESTRAINTS

High Initial Costs Limit Adoption Among Small-Scale Industries

While dual-pass opacity monitors offer superior performance, their higher price point compared to conventional monitoring solutions presents a significant adoption barrier. The sophisticated optical systems and advanced electronics required for dual-pass measurement significantly increase manufacturing costs. For small and medium enterprises operating with limited capital budgets, this cost differential often makes basic monitoring systems more attractive despite their lower accuracy.

Additional Challenges

Complex Installation and Maintenance Requirements

The precise alignment required for dual-pass measurement systems increases installation complexity and ongoing maintenance needs. Unlike simpler single-pass systems, dual-pass monitors require careful optical path alignment and regular calibration to maintain measurement accuracy. This creates operational challenges in harsh industrial environments where equipment may be subject to vibration, temperature variations, and particulate buildup.

Competition from Alternative Monitoring Technologies

Emerging particulate monitoring technologies using different measurement principles pose competitive challenges. Some newer systems offer comparable accuracy at potentially lower costs, creating price pressure on traditional opacity monitoring solutions. This dynamic may slow market growth for dual-pass systems in cost-sensitive applications.

MARKET OPPORTUNITIES

Expansion of Continuous Emission Monitoring Systems (CEMS) Creates New Applications

The growing adoption of comprehensive CEMS in industrial facilities presents significant opportunities for dual-pass opacity monitor manufacturers. These integrated monitoring solutions increasingly require high-accuracy particulate measurement components. The ability of dual-pass systems to provide reliable, low-maintenance monitoring makes them ideal for integration into these complex systems. Recent regulatory trends favoring continuous monitoring over periodic testing further strengthen this opportunity.

Emerging Applications in Ambient Air Quality Monitoring Expand Market Potential

While traditionally focused on industrial emissions, dual-pass opacity technology is finding new applications in ambient air quality monitoring networks. The need for more precise particulate measurement in urban environments and near industrial zones creates demand for advanced monitoring solutions. These applications benefit from the technology’s ability to maintain accuracy across varying environmental conditions.

Strategic Partnerships with Regulatory Bodies Create Market Access Opportunities

Collaborations between monitor manufacturers and environmental agencies present pathways for market expansion. Many regulatory bodies are actively seeking input from technology providers as they develop new monitoring standards and protocols. Companies that establish these strategic relationships can influence future regulatory requirements while positioning their products as preferred solutions.

MARKET CHALLENGES

Technical Limitations in Extreme Operating Conditions

Dual-pass opacity monitors face significant performance challenges in certain industrial environments. High-temperature exhaust streams, heavily laden with particulates, can degrade optical components over time. Similarly, applications involving corrosive gases or high humidity levels may compromise measurement accuracy and equipment longevity. These limitations constrain adoption in some of the most challenging industrial applications.

Other Challenges

Data Integration and Compatibility Issues

The increasing digitization of environmental monitoring creates integration challenges for legacy opacity monitoring systems. Ensuring seamless data transfer between monitors and modern plant information systems requires continuous software updates and hardware modifications. This evolving integration landscape adds complexity to product development and deployment.

Intense Global Competition Pressures Profit Margins

The opacity monitoring market has become increasingly competitive, with manufacturers facing price pressure from both established players and new market entrants. This competitive intensity makes it challenging to maintain profitability while continuing to invest in research and development. Companies must balance cost optimization with the need to innovate and differentiate their offerings.

DUAL-PASS OPACITY MONITOR MARKET TRENDS

Advancements in Measurement Technologies to Drive Market Growth

The global dual-pass opacity monitor market is experiencing significant growth, driven by technological advancements in particulate matter measurement. Manufacturers are increasingly adopting light scattering and absorption-based technologies to improve measurement accuracy and reliability. The development of integrated IoT-enabled monitoring systems has further enhanced real-time data collection and analysis, making these devices indispensable for environmental compliance and industrial process control. Recent improvements in optical sensor durability and calibration stability have extended product lifespans by approximately 30%, reducing total cost of ownership for end-users.

Other Trends

Stringent Environmental Regulations

Governments worldwide are implementing stricter emission norms, creating sustained demand for high-precision opacity monitoring solutions. The EPA’s Clean Air Act amendments and equivalent EU directives have mandated continuous emission monitoring systems (CEMS) across power plants and manufacturing facilities. This regulatory push has increased adoption rates by 15-20% annually in regulated industries, with particularly strong growth in Asia-Pacific regions where industrialization continues rapidly alongside environmental policy development.

Industrial Digitization and Smart Factory Integration

The Industry 4.0 revolution is transforming how opacity monitors are deployed and utilized. Modern dual-pass systems now feature cloud connectivity and predictive maintenance capabilities, allowing for more efficient plant operations. Major manufacturers report that smart monitoring solutions can reduce unplanned downtime by up to 25% in continuous process industries. The integration of AI-powered analytics is further enhancing the ability to detect particulate matter patterns and predict emission events before they occur, creating new value propositions for industrial users.

Expansion of Application Areas

While traditional applications in power generation and cement manufacturing continue to dominate, new use cases are emerging in waste incineration, chemical processing, and semiconductor manufacturing. The transportation sector is also adopting portable opacity monitors for vehicle emissions testing. This diversification is expected to contribute significantly to market growth, with niche applications projected to account for nearly 20% of total revenue by 2032. The development of compact, lower-cost models has further enabled this expansion into new verticals.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Competition

The global dual-pass opacity monitor market is characterized by a moderately fragmented competitive landscape, with established multinational corporations competing alongside regional specialists. Acoem and SICK AG currently lead the market, collectively accounting for approximately 28% of global revenue in 2024. Their dominance stems from comprehensive product portfolios covering both light scattering and absorption technologies, coupled with extensive service networks across North America and Europe.

While European manufacturers like Durag and AMETEK Land maintain strong positions in industrial emission monitoring applications, Asian players such as Shanghai Shouli Industry and Juguang Technology are rapidly gaining traction through competitive pricing and localized support. This regional specialization creates distinct competitive dynamics across different geographical markets.

The market has witnessed increased consolidation activity in recent years, with larger firms acquiring specialized technology providers to enhance their measurement capabilities. A notable example includes AMETEK Land’s 2023 acquisition of a UK-based optical measurement specialist, strengthening its position in the energy sector. Such strategic moves are reshaping competitive balances while accelerating technological advancements.

Emerging competition comes from digitally-native monitoring solution providers integrating IoT capabilities with traditional opacity measurement. Companies like Redkoh and HNL Systems are differentiating themselves through cloud-based data analytics platforms, creating new value propositions beyond hardware accuracy alone. This evolution suggests future competition will increasingly center on data integration capabilities rather than purely on measurement precision.

List of Key Dual-pass Opacity Monitor Manufacturers

- Acoem (France)

- SICK AG (Germany)

- Durag Group (Germany)

- AMETEK Land (UK)

- LISUN Electronics (China)

- CODEL International (UK)

- HNL Systems (India)

- Redkoh Industries (U.S.)

- Environmental Monitor Service (Italy)

- MRU Instruments (Germany)

- Shanghai Shouli Industry (China)

- Shanghai Precision Instruments (China)

- Juguang Technology (China)

Segment Analysis:

By Type

Light Scattering Method Dominates the Market Due to Superior Accuracy in Particulate Measurement

The market is segmented based on type into:

- Light Scattering Method

- Subtypes: Forward Scattering, Backward Scattering, and others

- Light Absorption Method

By Application

Industrial Emission Monitoring Segment Leads Due to Strict Government Regulations Worldwide

The market is segmented based on application into:

- Industrial Emission Monitoring

- Ambient Air Quality Monitoring

- Transportation and Energy

- Others

By End User

Environmental Agencies Hold Significant Share as Key Regulators of Air Quality Standards

The market is segmented based on end user into:

- Government and Environmental Agencies

- Industrial Facilities

- Research Institutions

- Others

Regional Analysis: Dual-pass Opacity Monitor Market

Asia-Pacific

The Asia-Pacific region dominates the global dual-pass opacity monitor market, driven by rapid industrialization and strict enforcement of air quality regulations in countries like China and India. China holds the largest market share, with government initiatives such as the Air Pollution Prevention and Control Action Plan mandating emission monitoring across key industries. The growing adoption of light scattering method opacity monitors in power plants and manufacturing facilities, coupled with increasing investment in smart city projects, fuels market expansion. India’s expanding cement and chemical industries further contribute to demand. However, price sensitivity remains a challenge, pushing manufacturers to develop cost-effective solutions without compromising accuracy.

North America

Stringent environmental regulations, particularly the U.S. EPA’s Clean Air Act, drive the adoption of high-precision dual-pass opacity monitors in industrial emission monitoring applications. The U.S. market benefits from technological advancements by key players like AMETEK Land and SICK, which focus on integrating AI-driven analytics for real-time data interpretation. Canada’s oil & gas sector also contributes significantly to market growth, with opacity monitors being widely used in refineries. While the region prioritizes compliance and accuracy, the shift toward remote monitoring solutions presents new opportunities for innovation and efficiency.

Europe

Europe’s market growth is propelled by stringent EU emission standards (e.g., Industrial Emissions Directive) and the increasing focus on sustainable industrial practices. Germany and the U.K. lead regional demand, with industries such as automotive and pharmaceuticals adopting dual-pass monitors to adhere to environmental norms. Water-based and low-maintenance opacity monitors are gaining traction, particularly in countries enforcing circular economy principles. Additionally, partnerships between manufacturers and regulatory bodies ensure continuous product upgrades, making Europe a hub for advanced monitoring solutions.

South America

The market in South America is emerging, with Brazil and Argentina showing moderate growth due to expanding mining and energy sectors. While regulatory frameworks are evolving, inconsistent enforcement limits widespread adoption. The region’s preference for economical monitoring solutions, however, has led to the popularity of refurbished and locally manufactured devices. Investments in infrastructure and rising environmental awareness provide long-term opportunities, though economic volatility remains a hurdle for large-scale deployment of high-end opacity monitors.

Middle East & Africa

Demand for dual-pass opacity monitors in the Middle East is primarily driven by the oil & gas and petrochemical industries, with Saudi Arabia and the UAE leading the market. Strict emission norms in free zones and industrial cities are accelerating adoption. Africa’s market, though nascent, shows potential with increasing mining activities in South Africa and Nigeria. Funding constraints and lack of technical expertise hinder faster growth, but foreign investments in industrial projects are expected to boost demand for advanced monitoring systems in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Dual-pass Opacity Monitor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 596 million in 2024 and is projected to reach USD 946 million by 2032, growing at a CAGR of 6.9%.

- Segmentation Analysis: Detailed breakdown by product type (Light Scattering Method, Light Absorption Method), application (Industrial Emission Monitoring, Ambient Air Quality Monitoring, Transportation and Energy, Others), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Acoem, SICK, Durag, AMETEK Land, and LISUN Electronics, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging measurement technologies, integration with IoT platforms, and advancements in optical sensing techniques.

- Market Drivers & Restraints: Evaluation of factors such as stringent environmental regulations, industrial emission standards, and technological limitations affecting market growth.

- Stakeholder Analysis: Strategic insights for equipment manufacturers, environmental monitoring agencies, industrial facilities, and regulatory bodies.

The report employs primary and secondary research methodologies, including expert interviews and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Dual-pass Opacity Monitor Market?

-> Dual-pass Opacity Monitor Market was valued at 596 million in 2024 and is projected to reach US$ 946 million by 2032, at a CAGR of 6.9% during the forecast period.

Which key companies operate in Global Dual-pass Opacity Monitor Market?

-> Key players include Acoem, SICK, Durag, AMETEK Land, LISUN Electronics, CODEL, and MRU Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include stringent environmental regulations, increasing industrial emissions monitoring requirements, and technological advancements in optical measurement systems.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive maintenance, development of portable monitoring solutions, and increasing adoption in emerging economies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...