Market Insights

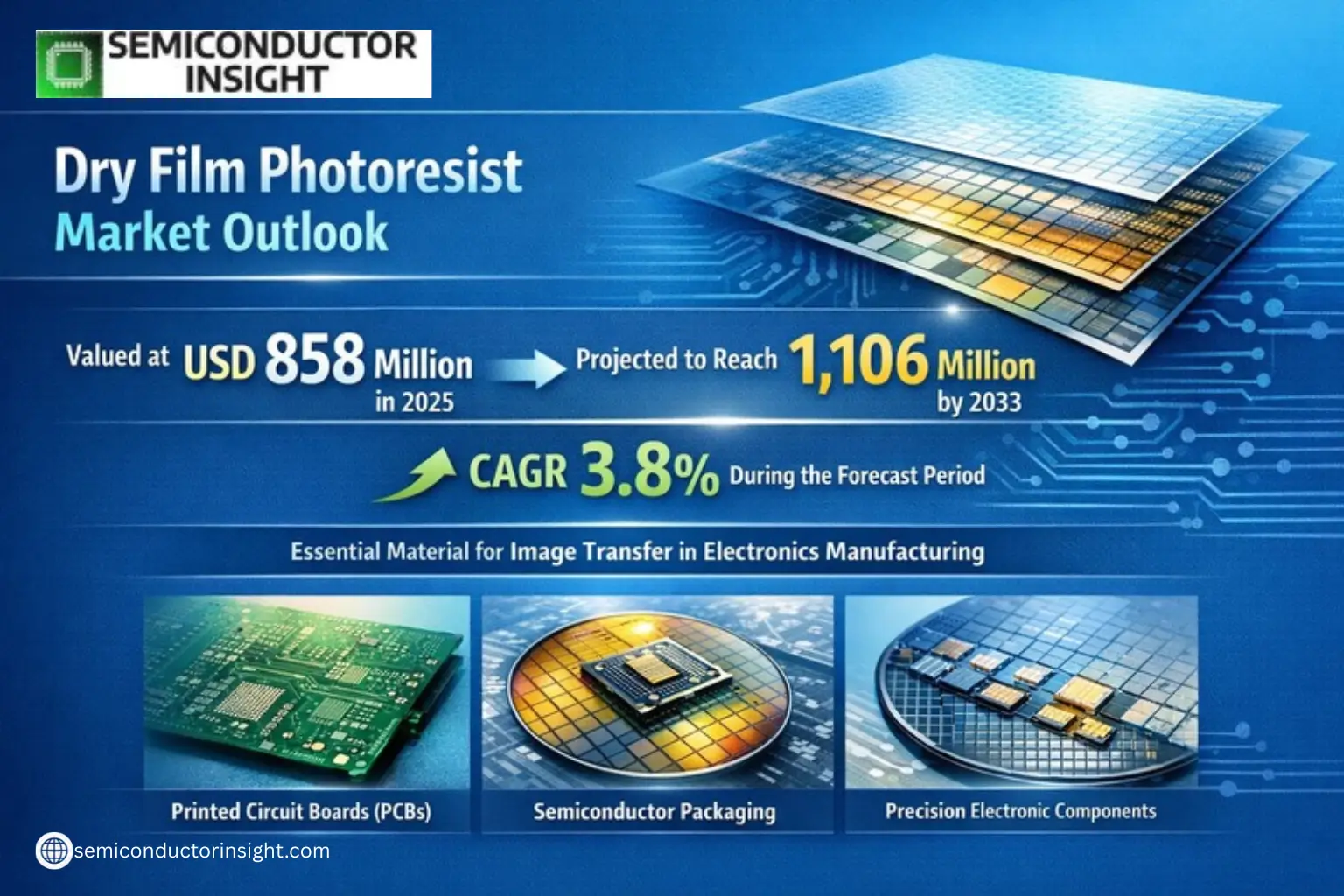

Global Dry Film Photoresist Market was valued at USD 858 million in 2025 and is projected to reach USD 1,106 million by 2033, exhibiting a CAGR of 3.8% during the forecast period.

Dry Film Photoresist (DFPR) is a critical material used in the image transfer process for manufacturing printed circuit boards (PCBs), semiconductor packaging, and other precision electronic components. It consists of a light-sensitive polymer film laminated onto substrates, enabling high-resolution patterning essential for modern electronics.

The market growth is driven by increasing demand for miniaturized electronic devices, advancements in PCB technology, and the expansion of 5G infrastructure. However, environmental concerns regarding chemical waste from photoresist processing pose challenges. The Asia-Pacific region dominates production and consumption, accounting for approximately 73% of global demand, followed by North America (17%) and Europe (8%). Japan leads manufacturing with over 55% market share among producing nations.

Key industry players including Asahi Kasei, Eternal Chemical, and Showa Denko Materials collectively hold about 80% of the global market. Recent developments focus on eco-friendly formulations with lower VOC emissions and improved resolution capabilities below 10μm line widths to meet next-generation semiconductor requirements.

MARKET DRIVERS

Growing Demand in PCB Manufacturing

The exponential growth in printed circuit board (PCB) production is a key driver for the dry film photoresist market. With PCB demand rising across consumer electronics, automotive, and industrial applications, manufacturers are increasingly adopting dry film photoresist for precise circuit patterning. The technology enables higher resolution and better adhesion than liquid alternatives.

Advancements in Semiconductor Packaging

Dry film photoresist finds extensive application in advanced semiconductor packaging technologies like fan-out wafer-level packaging (FOWLP) and 2.5D/3D IC integration. These packaging methods require ultra-thin, high-performance photoresists to achieve fine line/space geometries below 5µm.

Additionally, the transition to miniaturized electronic components and the proliferation of IoT devices further accelerates adoption in microelectronics manufacturing.

MARKET CHALLENGES

High Material and Processing Costs

Dry film photoresist systems require significant capital investment in application equipment and controlled environments. The material costs for high-performance resist formulations remain substantially higher than liquid alternatives, particularly for advanced lithography applications below 10µm features.

Other Challenges

Technical Limitations for Sub-2µm Applications

While dry film photoresist excels in many PCB applications, it faces competition from advanced liquid photoresists and direct imaging technologies in ultra-fine semiconductor applications requiring sub-2µm resolutions.

MARKET RESTRAINTS

Environmental Regulations on Chemicals

Stringent environmental regulations governing photoresist chemicals, particularly in North America and Europe, limit formulation options. The REACH and RoHS directives impose restrictions on certain photoactive compounds and solvents used in dry film photoresist manufacturing, increasing compliance costs.

MARKET OPPORTUNITIES

Emerging Applications in Flexible Electronics

The rapid expansion of flexible electronics presents significant growth potential for dry film photoresist manufacturers. The technology’s compatibility with flexible substrates and ability to maintain performance under mechanical stress makes it ideal for foldable displays, wearable devices, and flexible PCBs. Market analysts anticipate over 15% annual growth in flexible electronics applications through 2030.

Dry Film Photoresist Market Trends

Steady Growth Projected for Dry Film Photoresist Market

Global Dry Film Photoresist Market, valued at USD 858 million in 2025, is expected to grow at a CAGR of 3.8% to reach USD 1106 million by 2033. This growth is driven by increasing demand from PCB manufacturing, semiconductor packaging, and other electronics applications. Asia-Pacific dominates with 73% market share, followed by Americas (17%) and Europe (8%).

Other Trends

Consolidated Market Landscape

Three manufacturers – Asahi Kasei, Eternal, and Showa Denko Materials – control approximately 80% of the global Dry Film Photoresist Market. Japan leads production with 55% share, while China Taiwan and United States follow. This concentration impacts pricing strategies and innovation trends in the industry.

Application-Specific Growth Patterns

The PCB segment remains the largest application area for Dry Film Photoresists, particularly for rigid boards, flexible circuits, and HDI products. Semiconductor packaging is emerging as a key growth sector, driven by miniaturization trends in IC substrates and advanced packaging technologies.

Technical Developments in Photoresist Formulations

Manufacturers are focusing on developing higher-resolution Dry Film Photoresists to meet the demands of finer circuitry in PCBs and semiconductor applications. Both positive and negative photoresist types are seeing improvements in sensitivity, adhesion properties, and environmental stability to enhance production yields.

Regional Market Dynamics

While Asia-Pacific continues its dominance, North America and Europe are showing increased adoption of Dry Film Photoresists in high-end applications. Emerging markets in Southeast Asia are becoming important manufacturing hubs, benefiting from the regional electronics supply chain integration.

COMPETITIVE LANDSCAPE

Key Industry Players

Japan Dominates Dry Film Photoresist Market with 55% Global Production Share

Dry Film Photoresist Market is highly consolidated, with the top three manufacturers Asahi Kasei, Eternal, and Showa Denko Materials controlling approximately 80% of global production capacity. Asahi Kasei leads the market with superior R&D capabilities and extensive patent holdings in photoresist formulations. Japanese firms dominate production, leveraging advanced chemical engineering expertise to serve high-growth PCB and semiconductor packaging sectors. Regional players maintain niche positions through specialized formulations for flexible circuits and advanced packaging applications.

Emerging manufacturers in China Taiwan and South Korea are gaining traction by offering cost-competitive alternatives, though they face quality perception challenges compared to Japanese suppliers. Companies like Chang Chun Group and Kolon Industries are expanding capacity to capitalize on growing demand from Asian PCB fabricators. The market exhibits high entry barriers due to stringent technical requirements, long product validation cycles, and established customer relationships of incumbent players.

List of Key Dry Film Photoresist Companies Profiled

- Asahi Kasei Corporation

- Eternal Materials Co.

- Showa Denko Materials Co., Ltd.

- DuPont de Nemours, Inc.

- Chang Chun Group

- Kolon Industries, Inc.

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Fujifilm Electronics Materials

- JSR Corporation

- Hitachi Chemical Co., Ltd.

- Duksan Hi-Metal Co., Ltd.

- LG Chem Ltd.

- Daxin Materials Corporation

- Guangzhou Guanghua Microelectronics Materials

- Shin-Etsu Chemical Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Positive Dry Film Photoresist

|

| By Application |

|

PCB Applications

|

| By End User |

|

Electronics Manufacturing

|

| By Technology |

|

Subtractive Process

|

| By Material Composition |

|

Acrylic-based

|

Regional Analysis: Dry Film Photoresist Market

Asia-Pacific’s concentration of semiconductor fabs creates sustained demand for high-performance dry film photoresists. The region hosts over 60% of global semiconductor production capacity, with major players continually expanding manufacturing footprints.

As the world’s primary printed circuit board manufacturing base, the region drives innovation in photoresist formulations for high-density interconnect and flexible PCB applications, with Taiwan and China leading production volumes.

National semiconductor independence programs across APAC countries foster local dry film photoresist development, with China’s “Made in China 2025” and South Korea’s semiconductor industry roadmaps providing strategic impetus.

Early adoption of advanced packaging technologies like fan-out wafer-level packaging drives demand for specialized photoresists, with Asian foundries at the forefront of implementing next-generation lithography processes.

North America

North America maintains significant dry film photoresist demand through its high-tech electronics manufacturing and R&D activities. The region’s focus on cutting-edge semiconductor technologies, particularly in the United States, creates specialized requirements for advanced photoresist formulations. Defense and aerospace applications drive niche demand for high-reliability materials, while reshoring initiatives in semiconductor manufacturing gradually increase regional consumption. Leading research institutions collaborate with photoresist manufacturers to develop novel materials for emerging applications in flexible electronics and advanced packaging.

Europe

Europe’s dry film photoresist market benefits from strong automotive electronics and industrial equipment manufacturing sectors. German and French PCB manufacturers demand high-performance photoresists for automotive applications, while Nordic countries drive innovation in flexible electronics. The region’s stringent environmental regulations push development of eco-friendly photoresist formulations. Collaborative R&D projects between academia and industry foster development of specialized materials for MEMS and sensor applications.

South America

South America shows emerging demand for dry film photoresists, primarily serving domestic electronics manufacturing needs. Brazil represents the largest regional market with growing PCB production for automotive and consumer electronics applications. Limited local manufacturing capabilities create reliance on imports, though regional trade agreements facilitate material sourcing. The market shows potential for growth as regional electronics production expands, particularly in industrial automation and renewable energy applications.

Middle East & Africa

MEA exhibits niche demand concentrated in electronics assembly and maintenance operations. Israel’s high-tech sector drives some specialized photoresist requirements, while GCC countries show increasing PCB fabrication activity. The region serves primarily as an import market with limited local production. Emerging industrial diversification programs in Gulf states may create future growth opportunities as they develop local electronics manufacturing capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Dry Film Photoresist Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Dry Film Photoresist Market?

-> Dry Film Photoresist Market was valued at USD 858 million in 2025 and is projected to reach USD 1,106 million by 2033, exhibiting a CAGR of 3.8% during the forecast period.

What is the CAGR of Dry Film Photoresist Market during forecast period (2025-2033)?

-> The market is expected to grow at a CAGR of 3.8% during the forecast period (2025-2033).

Which key companies operate in Dry Film Photoresist Market?

-> Key players include Asahi Kasei, Eternal, Showa Denko Materials, Dupont, Chang Chun Group, and Kolon Industries, with top 3 manufacturers holding about 80% market share.

What are the major application areas?

-> Dry Film Photoresist is widely used in Printed Circuit Boards (Rigid board, Flexible, HDI), Lead Frame, Chemical milling, IC Substrate, and IC packaging.

Which region dominates the market?

-> Asia-Pacific is the largest market with about 73% share, followed by Americas (17%) and Europe (8%).

Which country is the largest producer?

-> Japan is the largest producer with over 55% share, followed by China Taiwan and United States.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...