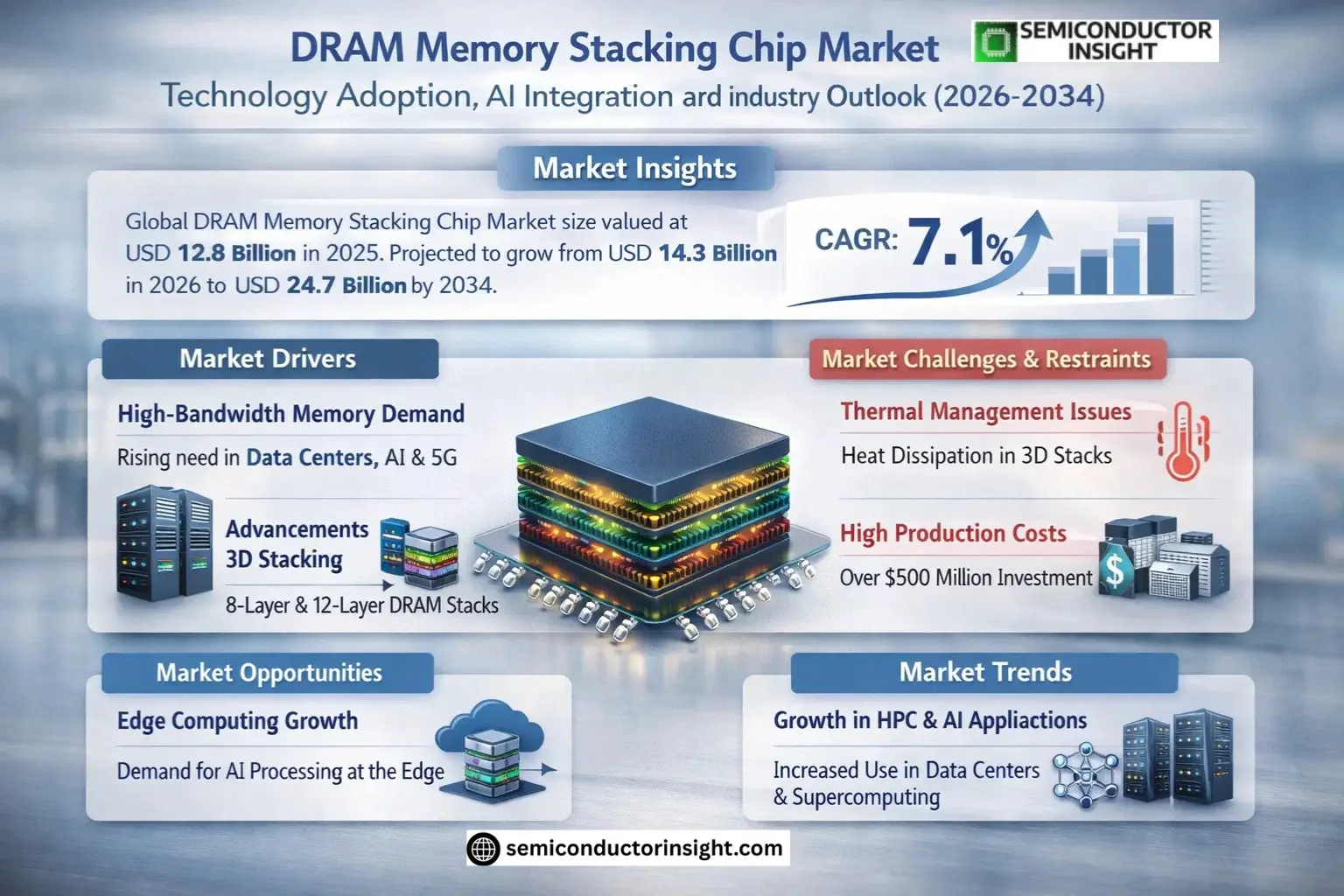

Market Insights

Global DRAM Memory Stacking Chip Market size was valued at USD 12.8 billion in 2025. The market is projected to grow from USD 14.3 billion in 2026 to USD 24.7 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

DRAM Memory Stacking Chips are advanced semiconductor components that vertically integrate multiple memory layers using through-silicon vias (TSVs) to enhance performance and reduce power consumption. These chips are critical for high-bandwidth applications such as data centers, AI accelerators, and next-generation mobile devices, offering improved speed and efficiency compared to traditional planar DRAM architectures.

The market growth is driven by increasing demand for high-performance computing, the proliferation of 5G networks, and advancements in artificial intelligence workloads. Key players like SK Hynix, Samsung, and Micron are investing heavily in 3D-stacking technologies to meet the rising need for faster and more energy-efficient memory solutions. For instance, in early 2024, SK Hynix announced mass production of its latest stacked DRAM modules optimized for AI servers, reinforcing the industry’s shift toward vertical integration.

MARKET DRIVERS

Growing Demand for High-Bandwidth Memory Solutions

DRAM Memory Stacking Chip Market is experiencing significant growth due to increasing demand for high-bandwidth memory in data centers, AI applications, and 5G infrastructure. Stacked DRAM solutions offer superior performance compared to traditional memory configurations, with bandwidth improvements exceeding 50% in some implementations. Global shift toward cloud computing has further accelerated adoption rates.

Advancements in 3D Stacking Technology

Recent breakthroughs in through-silicon via (TSV) technology have enabled more efficient DRAM memory stacking architectures. Major semiconductor manufacturers have successfully implemented 8-layer and 12-layer 3D DRAM stacks, achieving density improvements of 300% over planar alternatives. This technological progress directly supports the expansion of the DRAM Memory Stacking Chip Market.

Automotive applications, particularly in autonomous vehicle systems, are emerging as a key growth sector for DRAM Memory Stacking Chips, requiring reliable high-speed memory solutions for real-time data processing.

MARKET CHALLENGES

Thermal Management Complexities

DRAM Memory Stacking Chip implementations face significant thermal challenges due to increased power density in 3D configurations. Heat dissipation becomes critical for stacked DRAM modules, with testing showing temperature variations up to 15°C between layers in high-performance applications.

Other Challenges

Yield Optimization

Achieving acceptable production yields remains difficult for high-layer-count DRAM stacks, with current manufacturing processes typically showing 10-15% lower yields compared to conventional DRAM production.

MARKET RESTRAINTS

High Development and Production Costs

The capital-intensive nature of DRAM Memory Stacking Chip development creates significant barriers to market entry. TSV implementation and testing infrastructure requires investments exceeding USD 500 million for new fabrication facilities, limiting participation to established semiconductor companies with sufficient R&D budgets.

MARKET OPPORTUNITIES

Emerging Applications in Edge Computing

The rapid expansion of edge computing infrastructure presents new opportunities for DRAM Memory Stacking Chip manufacturers. Compact, high-performance memory solutions are becoming essential for edge devices processing AI workloads locally, with the market for edge-optimized DRAM stacks expected to triple by 2027.

DRAM Memory Stacking Chip Market Trends

Increased Adoption in High-Performance Computing

DRAM Memory Stacking Chip Market is witnessing significant growth due to rising demand in high-performance computing applications. Advanced packaging technologies like 3D stacking enable higher bandwidth and lower power consumption, making these chips ideal for data centers and AI workloads. Major manufacturers are investing heavily in process improvements to meet the demanding requirements of next-generation servers.

Other Trends

Shift Toward Higher Density Stacks

Market leaders are transitioning from 8-layer to 12-layer DRAM stacking configurations to address the increasing memory requirements of modern mobile devices and high-end graphics applications. This evolution allows for greater memory capacity within the same footprint, enabling thinner device designs and improved thermal performance.

Geographic Demand Shifts in DRAM Stacking Technology

Asia-Pacific continues to dominate DRAM Memory Stacking Chip consumption, driven by strong smartphone manufacturing in China and expanding data center infrastructure across the region. North America remains a key market for high-end applications, while European demand focuses primarily on automotive and industrial implementations of stacked memory solutions.

Material Innovations in Chip Stacking

Manufacturers are developing new bonding materials and through-silicon via (TSV) technologies to improve yield rates and reliability in stacked DRAM configurations. These advancements are critical as vertical integration becomes more complex with additional layers and finer pitch interconnects.

Competitive Landscape Evolution

The market remains concentrated among three major players – Samsung, SK Hynix, and Micron – who collectively control the majority of production capacity. These companies are accelerating technology roadmaps and forming strategic partnerships with foundries to maintain leadership in the DRAM Memory Stacking Chip sector.

COMPETITIVE LANDSCAPE

Key Industry Players

DRAM Memory Stacking Chip Market Dominated by Memory Manufacturing Giants

DRAM Memory Stacking Chip Market is highly concentrated with three major players SK Hynix, Samsung Electronics, and Micron Technology collectively commanding over 80% of global revenue share. These companies lead through advanced TSV (Through-Silicon Via) stacking technologies and economies of scale. Samsung maintains technological leadership with its 3D-stacked GDDR6 and HBM memory solutions, while SK Hynix specializes in high-bandwidth memory for AI/ML applications. Micron competes through cost-efficient production and partnerships with hyperscalers.

Emerging competitors like Nanya Technology and Winbond Electronics are gaining traction in niche segments such as low-power DRAM for IoT devices. Chinese players (CXMT, YMTC) are accelerating R&D with government support but face technological lag in advanced nodes below 20nm. Fabless companies like Rambus and Synopsys provide critical IP for chip designs, while OSAT firms (ASE Group, Amkor Technology) enable cost-effective packaging solutions for stacked DRAM architectures.

List of Key DRAM Memory Stacking Chip Companies Profiled

- SK Hynix

- Samsung Electronics

- Micron Technology

- Nanya Technology

- Winbond Electronics

- Rambus Inc.

- Powerchip Technology

- ChangXin Memory Technologies (CXMT)

- Yangtze Memory Technologies (YMTC)

- ASE Group

- Amkor Technology

- Synopsys

- Texas Instruments

- Intel Corporation

- Toshiba Memory

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Stacking 8 DRAM Chip dominates the market due to its widespread adoption in mainstream applications.

|

| By Application |

|

Servers represent the fastest-growing application segment:

|

| By End User |

|

Enterprise sector shows strongest adoption patterns:

|

| By Stacking Technology |

|

Through-Silicon Via (TSV) technology leads in adoption:

|

| By Vendor Type |

|

IDM (Integrated Device Manufacturers) dominate the supply chain:

|

Regional Analysis: Asia-Pacific DRAM Memory Stacking Chip Market

South Korea’s specialized DRAM production facilities achieve industry-leading defect density rates through proprietary stacking techniques. The country benefits from concentrated technological expertise in through-silicon vias (TSVs) and hybrid bonding processes that enable higher layer counts.

Local manufacturers are developing customized DRAM stacking solutions for AI accelerators, achieving superior thermal performance through innovative interposer designs. This addresses critical challenges in high-performance computing environments requiring dense memory configurations.

Collaborative research programs between major corporations and national institutes accelerate developments in advanced packaging technologies. Public-private initiatives focus on next-generation stacking materials and wafer-level integration techniques.

A vertically integrated supply ecosystem reduces dependence on foreign components, with domestic suppliers providing specialized equipment, chemicals, and substrates tailored for memory stacking production requirements.

Japan

Japan maintains strong capabilities in specialty DRAM stacking technologies for automotive and industrial applications. The region excels in reliability-focused designs for extreme environments, leveraging decades of expertise in materials science. Domestic manufacturers are advancing chiplet-based memory architectures through collaborations with equipment makers, while government initiatives promote the adoption of advanced packaging technologies across the semiconductor industry.

China

China is rapidly scaling up DRAM stacking chip production through aggressive investments in domestic semiconductor capabilities. The focus remains on import substitution, with multiple foundries developing competitive stacking technologies. Emerging Chinese players are gaining traction in consumer electronics applications, supported by state-funded research programs targeting next-generation memory architectures.

Taiwan

Taiwanese foundries play a crucial role in the DRAM stacking ecosystem through advanced packaging services for global memory vendors. The region’s OSAT (outsourced semiconductor assembly and test) providers are developing specialized solutions for heterogeneous integration, complementing leading-edge logic processes with memory stacking capabilities.

Southeast Asia

The ASEAN region is emerging as a strategic manufacturing hub for memory packaging and testing operations. Countries like Malaysia and Singapore are attracting investments in assembly facilities focused on cost-effective production of stacked DRAM solutions for mid-range applications, benefiting from established electronics manufacturing infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the DRAM Memory Stacking Chip Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of DRAM Memory Stacking Chip Market?

-> DRAM Memory Stacking Chip Market size was valued at USD 12.8 billion in 2025. The market is projected to grow from USD 14.3 billion in 2026 to USD 24.7 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Which key companies operate in DRAM Memory Stacking Chip Market?

-> Key players include SK Hynix, Samsung, Micron, among others. In 2025, the global top five players held approximately % market share.

What is the growth rate of Stacking 8 DRAM Chip segment?

-> Stacking 8 DRAM Chip segment will reach USD million by 2034, growing at a CAGR of % during the forecast period.

What are the key regional markets?

-> U.S. market is estimated at USD million in 2025, while China is projected to reach USD million by 2034.

What are the major application segments?

-> Major applications include Servers, Mobile Devices, and Others, with Servers accounting for significant market share in 2025.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...