MARKET INSIGHTS

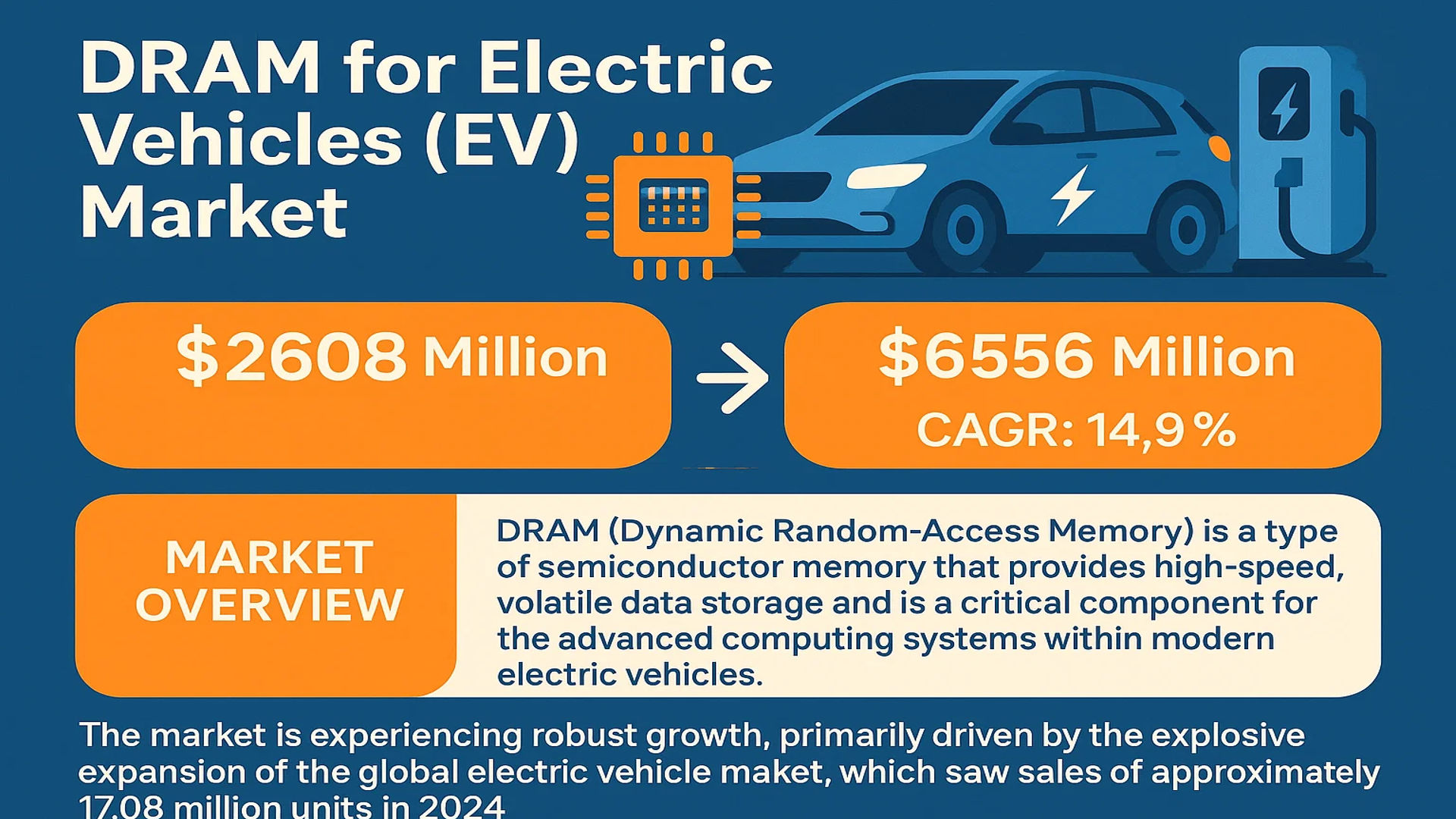

The global DRAM for Electric Vehicles (EV) Market was valued at 2608 million in 2024 and is projected to reach US$ 6556 million by 2032, at a CAGR of 14.9% during the forecast period.

DRAM (Dynamic Random-Access Memory) is a type of semiconductor memory that provides high-speed, volatile data storage and is a critical component for the advanced computing systems within modern electric vehicles. It is widely deployed in key vehicle modules such as infotainment systems, Advanced Driver-Assistance Systems (ADAS), digital video recorders (DVRs), and central vehicle control units to enable rapid data processing and real-time functionality.

The market is experiencing robust growth, primarily driven by the explosive expansion of the global electric vehicle market, which saw sales of approximately 17.08 million units in 2024. The increasing intelligence and connectivity of EVs necessitate higher memory capacities; for instance, L3+ autonomous driving systems now require 8-16GB of DRAM, a significant leap from the 1-4GB used in earlier models for basic functions. Furthermore, technological advancements from key players, such as the development of AEC-Q100 qualified, high-temperature resistant DRAM solutions by companies like Micron and Samsung, are crucial for meeting the stringent automotive environment demands and are propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Electric Vehicle Adoption to Accelerate DRAM Demand

The global electric vehicle market is experiencing unprecedented expansion, creating robust demand for automotive-grade DRAM. With electric vehicle sales reaching approximately 17.08 million units in 2024 and maintaining double-digit growth rates, the need for advanced memory solutions has become critical. China, as the world’s largest electric vehicle market, achieved remarkable penetration rates exceeding 41% with sales surpassing 10 million units, demonstrating the massive scale of this transformation. This rapid adoption directly correlates with increased DRAM requirements as modern electric vehicles evolve from basic transportation to sophisticated computing platforms. The transition from internal combustion engines to electric powertrains has fundamentally changed vehicle architecture, creating new memory-intensive applications that drive DRAM consumption across multiple systems simultaneously.

Advanced Driver Assistance Systems and Autonomous Driving Requirements to Fuel Market Expansion

The progression toward higher levels of vehicle autonomy represents a significant catalyst for DRAM market growth. While early electric vehicles typically utilized 1-4GB DRAM configurations for basic infotainment functions, the requirements for Level 3 and beyond autonomous driving systems have escalated dramatically. Modern autonomous driving platforms now demand 8-16GB DRAM capacities to process complex sensor fusion algorithms, real-time decision-making, and machine learning operations. The bandwidth requirements have similarly increased, with advanced platforms demonstrating threefold improvements to support trillions of artificial intelligence decisions per second. This technological evolution necessitates specialized automotive-grade DRAM that meets stringent reliability standards while delivering exceptional performance under demanding automotive conditions.

Increasing Vehicle Digitalization and Connectivity Features to Drive Memory Requirements

Modern electric vehicles are transforming into connected digital platforms, creating substantial demand for high-performance DRAM solutions. The integration of sophisticated infotainment systems, digital instrument clusters, and vehicle-to-everything communication capabilities requires significant memory resources. Contemporary electric vehicles typically feature multiple high-resolution displays, advanced audio systems, and seamless connectivity options that collectively consume substantial DRAM capacity. Furthermore, the implementation of over-the-air update capabilities necessitates additional memory allocation for update packages and system redundancy. The trend toward software-defined vehicles further amplifies these requirements, as automakers increasingly rely on software features and updates to differentiate their products and enhance customer experiences post-purchase.

MARKET CHALLENGES

Stringent Automotive Certification Requirements and Quality Standards to Pose Implementation Challenges

The automotive industry’s rigorous quality and reliability standards present significant challenges for DRAM manufacturers seeking to enter the electric vehicle market. Automotive-grade DRAM must comply with AEC-Q100 qualification standards and demonstrate exceptional performance across extreme temperature ranges from -40°C to 125°C. These requirements necessitate specialized manufacturing processes and extensive testing protocols that substantially increase production costs and development timelines. The certification process typically involves thousands of hours of accelerated life testing and validation under simulated automotive conditions, creating barriers for new market entrants and extending time-to-market for new DRAM solutions.

Other Challenges

Supply Chain Constraints and Manufacturing Capacity Limitations

The specialized nature of automotive-grade DRAM production creates supply chain challenges that can impact market growth. Automotive manufacturers require guaranteed long-term supply agreements and extensive quality documentation, which strains existing manufacturing capacity. The transition to more advanced DRAM nodes further complicates production, as automotive qualifications require stable processes that often lag behind consumer electronics advancements. These factors collectively create supply-demand imbalances during periods of rapid electric vehicle market expansion.

Technical Complexity in Automotive Integration

Integrating high-performance DRAM into automotive systems presents numerous technical challenges related to signal integrity, power management, and thermal considerations. The electromagnetic compatibility requirements in electric vehicles are particularly stringent due to high-power electrical systems and multiple electronic control units operating simultaneously. Ensuring reliable DRAM operation amidst these challenging conditions requires sophisticated system design and validation approaches that increase development complexity and cost.

MARKET RESTRAINTS

Economic Volatility and Automotive Industry Cyclicality to Restrain Market Growth

The capital-intensive nature of electric vehicle production and the automotive industry’s cyclical characteristics create market restraints for DRAM suppliers. Economic uncertainties and fluctuations in consumer demand can significantly impact electric vehicle production volumes, thereby affecting DRAM consumption patterns. The automotive industry’s traditional model of multi-year development cycles also creates challenges for DRAM manufacturers who must align their product roadmaps with vehicle development timelines. This mismatch between semiconductor innovation cycles and automotive development schedules can restrain the adoption of cutting-edge DRAM technologies in electric vehicles.

Cost Sensitivity in Electric Vehicle Manufacturing to Limit Premium DRAM Adoption

Despite the premium nature of electric vehicles, manufacturers face intense cost pressure that restricts widespread adoption of high-performance DRAM solutions. The automotive industry’s focus on cost reduction per vehicle creates challenges for incorporating advanced memory technologies, particularly in mass-market electric vehicle segments. This cost sensitivity is exacerbated by the complex supply chain and multiple tiers of suppliers involved in automotive component manufacturing, each adding margin requirements that ultimately increase the final cost of DRAM solutions.

Technological Evolution Pace Mismatch Between Semiconductor and Automotive Industries

The differing innovation cycles between the semiconductor and automotive industries create significant restraints for DRAM adoption in electric vehicles. While semiconductor technology typically advances every 12-18 months, automotive development cycles often span 3-5 years. This disconnect makes it challenging to incorporate the latest DRAM technologies into vehicle designs, as automakers require stable, long-term component availability. The qualification processes for automotive-grade components further extend this timeline, creating a natural lag in technology adoption that restrains market growth for cutting-edge DRAM solutions.

MARKET OPPORTUNITIES

Emergence of Software-Defined Vehicles and Centralized Computing Architectures to Create New Growth Frontiers

The automotive industry’s transition toward software-defined vehicles and centralized computing architectures presents substantial opportunities for DRAM market expansion. This architectural shift consolidates multiple electronic control units into high-performance domain controllers and centralized computers, dramatically increasing memory requirements per vehicle. These advanced computing platforms require high-bandwidth, high-capacity DRAM solutions to support complex software stacks, artificial intelligence workloads, and continuous functional updates. The trend toward vehicle operating systems and cloud-connected services further amplifies these opportunities, creating new revenue streams for DRAM manufacturers capable of delivering automotive-qualified solutions.

Development of Specialized Automotive DRAM Solutions for Next-Generation Applications

The evolution of electric vehicle technologies creates opportunities for specialized DRAM products tailored to specific automotive applications. The increasing adoption of lidar, radar, and camera systems for autonomous driving requires optimized memory solutions that balance performance, power efficiency, and reliability. Similarly, the growth of vehicle-to-everything communication and advanced telematics systems creates demand for DRAM solutions with enhanced security features and extended temperature range capabilities. These application-specific requirements enable DRAM manufacturers to develop differentiated products and capture premium market segments.

Expansion of Electric Vehicle Models and Market Segments to Broaden Addressable Market

The diversification of electric vehicle offerings across multiple price points and vehicle segments creates expanding opportunities for DRAM suppliers. As electric vehicle technology matures and production scales, manufacturers are introducing models across various market segments from economy to luxury vehicles. This expansion increases the overall addressable market for automotive DRAM while creating opportunities for product differentiation based on performance tiers and feature sets. The global nature of electric vehicle adoption further enhances these opportunities, as different regions may have varying requirements for DRAM specifications based on local infrastructure, regulations, and consumer preferences.

DRAM FOR ELECTRIC VEHICLES (EV) MARKET TRENDS

Advancements in Autonomous Driving and In-Vehicle Experience to Emerge as a Trend in the Market

The evolution towards higher levels of vehicle autonomy represents the most significant driver for automotive DRAM demand. While early electric vehicles utilized modest memory capacities of 1-4GB primarily for infotainment, the requirements for Level 3 and above autonomous driving systems have created a paradigm shift. These advanced systems process enormous data streams from multiple sensors including LiDAR, radar, and high-resolution cameras, necessitating both higher bandwidth and greater capacity memory solutions. For instance, Tesla’s Hardware 4.0 platform utilizes Micron’s GDDR6 memory, which provides a bandwidth increase of approximately 300% over previous generations to support the trillions of AI computations required per second for real-time decision making. This technological arms race among automakers to deliver safer and more capable autonomous features directly fuels the adoption of cutting-edge DRAM solutions, with capacities now regularly reaching 8-16GB per vehicle and projected to grow further as L4/L5 systems approach commercialization.

Other Trends

Proliferation of Connected Vehicle Features and OTA Updates

The transformation of vehicles into connected platforms has dramatically increased the need for robust and reliable memory solutions. Modern electric vehicles function as rolling data centers, constantly communicating with cloud services, other vehicles, and infrastructure. This connectivity enables features like real-time traffic updates, remote diagnostics, and streaming entertainment services, all of which require substantial memory resources. Furthermore, the industry’s shift toward over-the-air (OTA) update capabilities represents a critical memory-intensive function. These updates, which can range from minor software patches to major system upgrades, require temporary storage space during installation while ensuring fail-safe operation. The average size of these update packages has grown from hundreds of megabytes to multiple gigabytes, necessitating high-capacity DRAM that can handle both the storage and processing demands without compromising vehicle safety or performance.

Increasing Electrification and Regional Market Expansion

The global acceleration of electric vehicle adoption continues to drive the automotive DRAM market forward, with particular strength in key regions. China maintains its position as the dominant market, with EV sales exceeding 10 million units in 2024 and achieving a remarkable 41% penetration rate of new vehicle sales. This massive scale creates substantial demand for memory components across all vehicle segments. Meanwhile, Europe and North America represent additional strong growth markets, together accounting for over 80% of global EV sales alongside China. This regional concentration influences DRAM specifications, as manufacturers must account for varying environmental conditions, regulatory requirements, and consumer preferences across markets. The stringent AEC-Q100 qualification standards, which ensure components can withstand temperatures up to 125°C and resist electromagnetic interference, have become table stakes for automotive-grade DRAM suppliers seeking to compete in these diverse but demanding regional markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Drive Innovation to Meet Escalating EV Memory Demands

The global DRAM for Electric Vehicles market exhibits an oligopolistic structure dominated by established memory semiconductor leaders, though several specialized players maintain significant niches. Micron Technology and Samsung Electronics collectively commanded approximately 65% of the automotive DRAM market share in 2024, leveraging their technological leadership in high-bandwidth memory solutions and extensive automotive-grade product portfolios. Their dominance stems from early investments in AEC-Q100 qualified components and strategic partnerships with major EV manufacturers, particularly in the advanced driver-assistance systems (ADAS) segment.

SK Hynix maintained a strong third position with approximately 15% market share, particularly excelling in LPDDR5 solutions for infotainment systems. The company’s growth is attributed to its aggressive pricing strategy and reliable supply chain relationships with Korean and Chinese EV manufacturers. Meanwhile, Winbond and ISSI (acquired by Sino Wealth Electronic Ltd.) have carved significant niches in the cost-sensitive segments, specializing in DDR3 and older generation memory for entry-level electric vehicles and basic control systems.

These industry leaders are accelerating R&D investments to develop next-generation automotive DRAM solutions. Micron’s recent GDDR6 implementation in Tesla’s HW4.0 platform demonstrates the industry shift toward higher bandwidth requirements, while Samsung’s 8GB LPDDR5 modules designed for L4 autonomous driving systems represent the cutting edge of automotive memory technology. The competitive intensity is further heightened by increasing entry barriers, as automotive certification processes require significant capital investment and 2-3 years of qualification testing.

Regional dynamics significantly influence competition, with Asian manufacturers dominating supply to China’s massive EV market (representing over 40% of global EV sales), while European and American suppliers focus on premium segments with stricter safety and performance requirements. The ongoing industry consolidation, evidenced by ISSI’s acquisition and Nanya’s strategic partnerships, suggests the market is moving toward greater integration across the semiconductor supply chain to ensure reliability and volume production capabilities.

List of Key DRAM for Electric Vehicles Companies Profiled

- Micron Technology, Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- SK Hynix Inc. (South Korea)

- STMicroelectronics N.V. (Switzerland)

- Integrated Silicon Solution, Inc. (ISSI) (U.S.)

- Nanya Technology Corporation (Taiwan)

- Winbond Electronics Corporation (Taiwan)

Segment Analysis:

By Type

DDR4 Segment Dominates the Market Due to its Optimal Balance of Performance, Cost, and Reliability

The market is segmented based on type into:

- DDR3

- Subtypes: Standard DDR3, Low Power DDR3 (LPDDR3)

- DDR4

- Subtypes: Standard DDR4, Low Power DDR4 (LPDDR4)

- DDR5

- Subtypes: Standard DDR5, Low Power DDR5 (LPDDR5)

- Others

- Subtypes: GDDR6, GDDR7

By Application

ADAS Segment Leads Due to High Memory Bandwidth Requirements for Sensor Fusion and AI Processing

The market is segmented based on application into:

- Infotainment System

- ADAS

- DVR

- Vehicle Control Unit

- Others

By End User

Passenger Vehicle Segment Leads Due to High Production Volumes and Consumer Demand for In-Vehicle Technology

The market is segmented based on end user into:

- Passenger Vehicle

- Commercial Vehicle

- Others

Regional Analysis: DRAM for Electric Vehicles (EV) Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global DRAM for EV market, driven by its position as the world’s largest electric vehicle manufacturing hub. China, the world’s largest EV market with sales exceeding 10 million units in 2024 and a penetration rate of 41%, is the primary engine of growth. This massive production scale creates immense demand for automotive-grade memory. The region is characterized by intense competition and rapid technological adoption. While cost sensitivity keeps DDR3 and DDR4 relevant for entry-level models, there is a strong and accelerating shift towards higher-performance DDR5 and GDDR6 solutions to support advanced infotainment and Level 3+ autonomous driving systems. Local and global memory giants like Samsung and SK Hynix have a significant manufacturing and R&D presence here, ensuring a robust supply chain. The focus is on innovation tailored to the high-volume, feature-diverse vehicles produced for the domestic and export markets.

North America

North America represents a high-value, technologically advanced market for automotive DRAM. Stringent safety and performance standards, coupled with the early and aggressive adoption of autonomous driving technology by companies like Tesla and General Motors, drive the demand for high-bandwidth, high-capacity memory modules. Tesla’s HW4.0 platform, which utilizes Micron’s GDDR6 memory to process trillions of AI decisions per second, exemplifies this trend. The market is dominated by the need for AEC-Q100 qualified components that can withstand extreme automotive environments. While the volume of EVs sold is less than in Asia-Pacific, the average DRAM content per vehicle is among the highest globally, as premium infotainment, advanced driver-assistance systems (ADAS), and over-the-air (OTA) update capabilities become standard. This makes the region a critical market for leading-edge product launches and innovation.

Europe

Europe is a major and mature market for DRAM in electric vehicles, underpinned by a strong automotive OEM base and rigorous regulatory frameworks that encourage vehicle connectivity and safety. The region’s focus on premium and luxury EVs from manufacturers like Volkswagen Group, BMW, and Mercedes-Benz fuels demand for sophisticated memory solutions that power digital cockpits, high-resolution displays, and complex ADAS functionalities. EU safety regulations and NCAP ratings often act as a catalyst for adopting newer technologies, pushing the market towards higher-density DDR4 and DDR5 modules. Furthermore, the presence of key automotive semiconductor suppliers and a robust infrastructure for testing and validation makes Europe a central hub for the development and integration of next-generation automotive memory, with a strong emphasis on quality, reliability, and compliance.

South America

The DRAM for EV market in South America is in a nascent but developing stage. The adoption rate is intrinsically linked to the gradual electrification of the region’s vehicle fleet, which is currently slower compared to other global markets. Economic volatility and inconsistent government incentives for EV adoption present significant challenges, often making cost the primary purchasing driver. This results in a market currently dominated by lower-to-mid-tier DRAM solutions (primarily DDR3 and older DDR4), as manufacturers prioritize affordability over advanced features. However, as major global OEMs increase their presence and local governments potentially introduce more supportive policies, the market is expected to gradually evolve, creating long-term opportunities for memory suppliers as the demand for more connected and feature-rich electric vehicles grows.

Middle East & Africa

The market for DRAM in electric vehicles across the Middle East and Africa is emerging. Growth is primarily concentrated in more developed nations within the Gulf Cooperation Council (GCC), such as Israel and the UAE, where government visions for economic diversification are fostering initial investments in EV infrastructure and adoption. The demand is currently limited to luxury and high-end EV imports, which utilize advanced memory modules. However, widespread market development is constrained by factors including limited EV charging infrastructure, a lack of strong local manufacturing, and minimal regulatory push for electrification. Consequently, the demand for automotive DRAM is presently a niche segment, but it holds potential for future growth as urban development and sustainability initiatives gain momentum across the region.

Report Scope

This market research report provides a comprehensive analysis of the global and regional DRAM for Electric Vehicles (EV) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DRAM for Electric Vehicles (EV) Market?

-> DRAM for Electric Vehicles (EV) Market was valued at 2608 million in 2024 and is projected to reach US$ 6556 million by 2032, at a CAGR of 14.9% during the forecast period..

Which key companies operate in Global DRAM for Electric Vehicles (EV) Market?

-> Key players include Micron Technology, Samsung Electronics, SK Hynix, STMicroelectronics, ISSI, Nanya, and Winbond, among others.

What are the key growth drivers?

-> Key growth drivers include explosive growth in global EV sales (17.08 million units in 2024), increasing demand for advanced infotainment and ADAS systems, and the transition towards higher autonomy (L3+), requiring 8-16GB DRAM capacities.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven primarily by China, which accounted for over 10 million EV sales in 2024 with a 41% penetration rate.

What are the emerging trends?

-> Emerging trends include the adoption of AEC-Q100 qualified high-temperature DRAM (125°C), integration of GDDR6 for AI processing (e.g., Tesla HW4.0), and the shift from DDR4 to DDR5/LPDDR5 technologies to support L4/L5 autonomous driving requirements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...