MARKET INSIGHTS

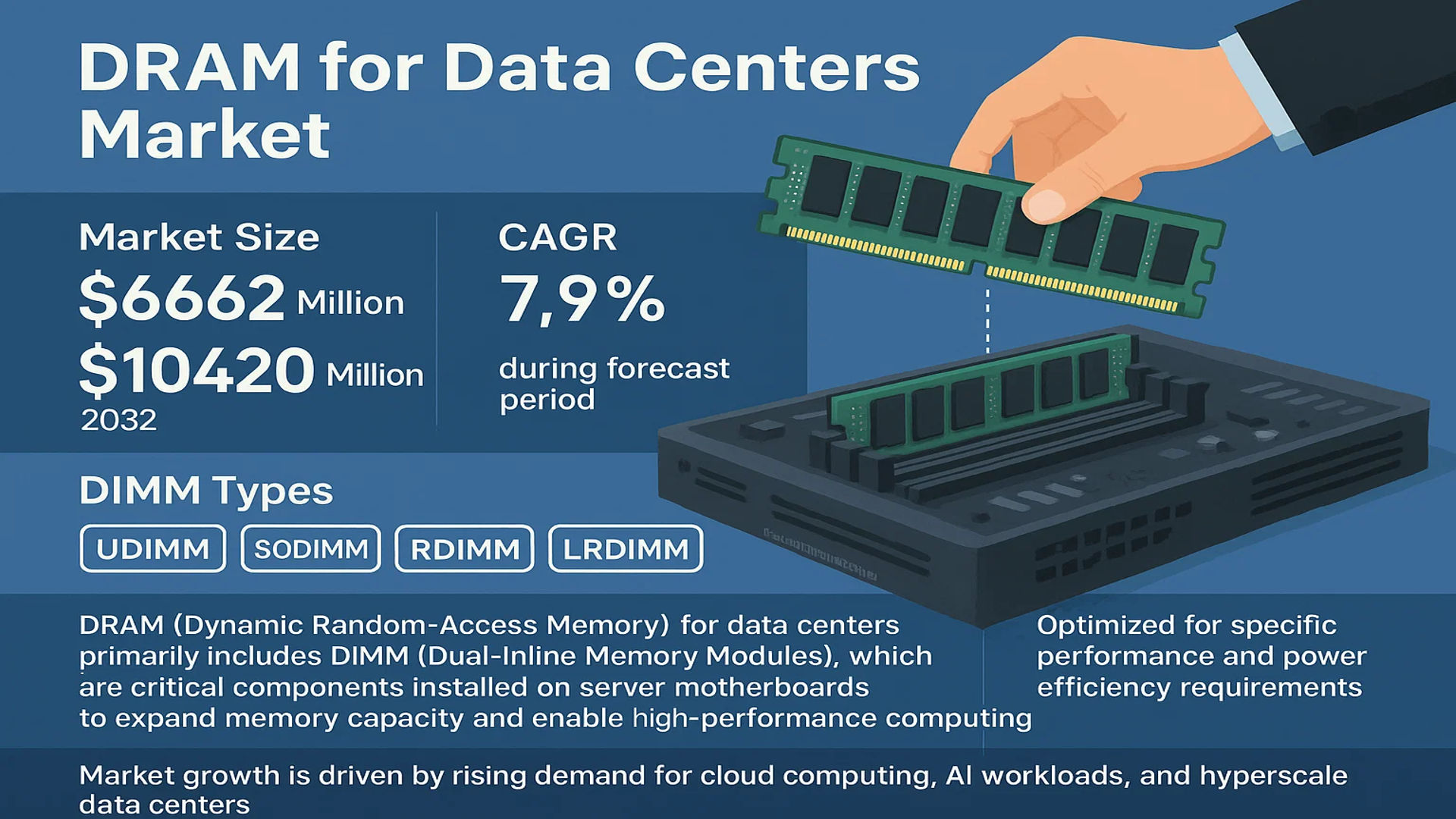

The global DRAM for Data Centers Market was valued at 5662 million in 2024 and is projected to reach US$ 10420 million by 2032, at a CAGR of 7.9% during the forecast period.

DRAM (Dynamic Random-Access Memory) for data centers primarily includes DIMM (Dual-Inline Memory Modules), which are critical components installed on server motherboards to expand memory capacity and enable high-performance computing. These modules support large-scale data processing and multitasking operations in modern data-intensive environments. The main types of server DIMMs include UDIMM, SODIMM, RDIMM, MRDIMM, and LRDIMM, each optimized for specific performance and power efficiency requirements.

The market growth is driven by rising demand for cloud computing, AI workloads, and hyperscale data centers, which require high-bandwidth, low-latency memory solutions. Additionally, advancements in memory technologies, such as DDR5 adoption and heterogeneous memory architectures, are accelerating innovation. Leading players like Samsung, SK Hynix, and Micron Technology dominate the market, with strategic investments in capacity expansion and next-gen DRAM development to meet escalating demand from enterprises and hyperscalers globally.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Data-Centric Applications to Accelerate DRAM Demand

The global data center DRAM market is experiencing robust growth due to the exponential rise in data-intensive applications across industries. Cloud computing adoption has surged, with hyperscale data centers requiring high-performance memory solutions to handle workloads efficiently. Artificial intelligence and machine learning applications, which rely heavily on fast memory access, are projected to account for over 30% of data center DRAM consumption by 2025. The shift towards 5G networks and edge computing further amplifies this demand, as these technologies require distributed data processing with low-latency memory solutions. Advanced DIMM architectures like LRDIMM and MRDIMM are gaining traction as they offer superior bandwidth and capacity for these compute-heavy applications.

Technological Advancements in Memory Architecture Fuel Market Expansion

Innovation in DRAM technology continues to push the boundaries of performance and efficiency. The transition to DDR5 architecture represents a significant leap forward, offering potentially double the bandwidth of DDR4 while improving power efficiency by approximately 20%. This is particularly crucial for data centers, where energy consumption accounts for a substantial portion of operational costs. Memory manufacturers are also developing advanced packaging technologies like 3D-stacked DRAM and hybrid memory cube solutions that deliver higher density and improved thermal characteristics. These innovations enable data centers to process larger datasets more efficiently, supporting the growing demands of big data analytics and real-time processing applications.

MARKET RESTRAINTS

Volatility in DRAM Pricing and Supply Chain Disruptions Impede Market Stability

The data center DRAM market faces significant challenges from price volatility and supply chain constraints. The memory industry is known for its cyclical nature, with pricing fluctuations of up to 30% between quarters affecting procurement strategies. Geopolitical tensions and trade restrictions have further complicated the supply chain, particularly affecting the availability of critical raw materials and manufacturing equipment. These disruptions have led to extended lead times for high-density DRAM modules, forcing data center operators to maintain higher inventory levels and impacting total cost of ownership calculations.

Power Consumption Concerns Limit Adoption in Energy-Sensitive Markets

While DRAM performance continues to improve, power consumption remains a significant barrier to adoption in certain markets. Memory subsystems can account for over 20% of a server’s total power budget, making energy efficiency a critical consideration for large-scale deployments. In regions with strict environmental regulations or high energy costs, data center operators are increasingly looking towards alternative memory technologies or architectural approaches to reduce power consumption. This has created pressure on DRAM manufacturers to develop more efficient solutions without compromising performance, adding complexity to the R&D process.

MARKET CHALLENGES

Integration Complexities with Emerging Compute Architectures

The rapid evolution of data center compute architectures presents significant integration challenges for DRAM technologies. Heterogeneous computing environments combining CPUs, GPUs, and specialized accelerators require memory solutions that can efficiently serve multiple processing units simultaneously. The industry is grappling with memory bandwidth limitations that create bottlenecks in these complex systems. While solutions like CXL (Compute Express Link) offer promise for memory pooling and expansion, implementation at scale remains technically challenging and requires significant ecosystem development.

Other Challenges

Thermal Management Issues

As DRAM densities increase, thermal management becomes increasingly critical. High-performance modules operating in tightly packed server racks face cooling challenges that can impact reliability and longevity. This is particularly problematic in high-ambient-temperature environments where traditional cooling approaches may be insufficient.

Security Vulnerabilities

Memory-related security threats such as Rowhammer attacks and side-channel vulnerabilities continue to pose risks for data center operators. Mitigating these threats requires additional hardware and software safeguards that can impact performance or increase costs.

MARKET OPPORTUNITIES

Emerging Memory Technologies Create New Growth Avenues

The convergence of DRAM with emerging memory technologies presents significant opportunities for market expansion. Solutions that combine DRAM with persistent memory technologies are gaining traction for applications requiring both high performance and data persistence. The development of specialized DRAM variants optimized for specific workloads, such as AI training or in-memory databases, enables manufacturers to address niche market segments with premium-priced products. Additionally, the growing demand for security-enhanced memory modules in financial and government sectors creates opportunities for value-add solutions.

Regional Data Center Expansion Drives Localized Demand

The global proliferation of data centers creates opportunities for regional market growth. Emerging markets in Southeast Asia, Latin America, and Africa are experiencing rapid data center construction, with projected capacity increases exceeding 30% annually in some regions. This expansion is driving demand for localized memory solutions tailored to specific environmental conditions and application requirements. Memory manufacturers can capitalize on this trend by developing region-specific product variants and establishing local support infrastructure.

DRAM FOR DATA CENTERS MARKET TRENDS

Rising Demand for High-Performance Computing Fuels DRAM Adoption in Data Centers

The global DRAM for data centers market is experiencing robust growth, driven by the increasing demand for high-performance computing (HPC) and cloud-based services. With data centers requiring higher memory bandwidth to support artificial intelligence (AI), machine learning (ML), and big data analytics workloads, the adoption of advanced DRAM modules such as RDIMM and LRDIMM has surged. These modules provide lower latency and higher capacity, critical for real-time data processing. The market is projected to grow at a 7.9% CAGR, reaching $10.42 billion by 2032, up from $5.66 billion in 2024. Furthermore, innovations like DDR5 DRAM, offering higher speeds and energy efficiency, are accelerating this trend.

Other Trends

Expansion of Hyperscale Data Centers

The proliferation of hyperscale data centers, particularly in North America and Asia-Pacific, is significantly boosting DRAM demand. Hyperscalers such as Amazon Web Services, Google Cloud, and Microsoft Azure require high-density memory modules to handle massive data workloads efficiently. In response, leading manufacturers are developing high-capacity LRDIMMs (Load-Reduced DIMMs), which minimize electrical load while supporting capacities exceeding 256GB per module. The shift towards 5G networks and edge computing is further amplifying the need for faster, low-latency memory solutions, reinforcing the DRAM market’s growth trajectory.

Energy Efficiency and AI-Driven Memory Optimization

As sustainability becomes a key priority for data center operators, energy-efficient DRAM solutions are gaining prominence. Manufacturers are increasingly focusing on developing low-power DDR5 modules that reduce power consumption by up to 20% compared to previous generations. Another emerging trend is the integration of AI-driven dynamic memory allocation, enabling intelligent resource management across server workloads. This reduces idle power waste while improving overall system efficiency. Additionally, heterogeneous memory architectures combining DRAM with persistent memory technologies like Intel Optane are being explored to optimize cost-performance ratios in large-scale data centers.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading DRAM Manufacturers Focus on Innovation to Capture Data Center Market Share

The global DRAM for Data Centers market is highly competitive, dominated by a mix of established memory giants and emerging players striving to meet the escalating demands of cloud computing and AI-driven workloads. Samsung, the market leader, maintains its stronghold through continuous advancements in high-bandwidth memory (HBM) and DDR5 technologies, capturing the largest revenue share in 2024. The company’s ability to scale production and deliver energy-efficient solutions has cemented its position across North America, Asia, and Europe.

SK Hynix and Micron Technology follow closely, leveraging their expertise in high-performance server DRAM modules like RDIMM and LRDIMM. Both companies are aggressively investing in next-generation memory architectures to support data-intensive applications in hyperscale data centers. Their recent breakthroughs in 3D-stacked DRAM and hybrid memory cube designs have given them a technological edge, particularly for AI/ML workloads.

Meanwhile, Changxin Memory Technologies (CXMT) is rapidly emerging as a formidable challenger, especially in the Asian market. Backed by significant government investments, CXMT is expanding its DDR4 and DDR5 product lines to reduce regional dependency on imported memory solutions. Their cost-competitive offerings are gaining traction among Chinese cloud service providers and enterprise data center operators.

The competitive intensity is further fueled by strategic maneuvers from Kingston Technology and SMART Modular Technologies, who are differentiating through value-added services like customized memory configurations and extended lifecycle support. These companies are capitalizing on the growing demand for legacy system upgrades in enterprise environments.

List of Key DRAM Manufacturers for Data Centers

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- Micron Technology (U.S.)

- Changxin Memory Technologies (CXMT) (China)

- Kingston Technology Company, Inc. (U.S.)

- SMART Modular Technologies (U.S.)

- ADATA Technology (Taiwan)

- Rambus (U.S.)

- Kimtigo (China)

- Transcend Information (Taiwan)

- Innodisk (Taiwan)

- TeamGroup (Taiwan)

Segment Analysis:

By Type

RDIMM Segment Leads the Market Due to High Performance and Error-Correcting Capabilities

The market is segmented based on type into:

- UDIMM (Unbuffered DIMM)

- SODIMM (Small Outline DIMM)

- RDIMM (Registered DIMM)

- MRDIMM (MultiRank DIMM)

- LRDIMM (Load-Reduced DIMM)

- Others

By Application

IDC (Internet Data Center) Segment Dominates Due to Rising Cloud Computing Demand

The market is segmented based on application into:

- IDC (Internet Data Center)

- EDC (Enterprise Data Center)

- Others

By Technology

DDR5 Gains Traction for Enhanced Bandwidth and Power Efficiency

The market is segmented based on technology into:

- DDR3

- DDR4

- DDR5

- Others

By Capacity

High-Capacity DRAM Modules in Demand for Data-Intensive Workloads

The market is segmented based on capacity into:

- 8GB

- 16GB

- 32GB

- 64GB

- 128GB and Above

Regional Analysis: DRAM for Data Centers Market

Asia-Pacific

The Asia-Pacific region dominates the global DRAM for Data Centers market, driven primarily by rapid digital transformation across China, Japan, and South Korea. China, home to tech giants like Alibaba and Tencent, leads in hyperscale data center deployments, fueling demand for high-capacity RDIMM and LRDIMM modules. In 2024, China accounted for over 40% of the region’s DRAM consumption, with Japan and India following closely. The proliferation of 5G networks and AI workloads has intensified the need for low-latency memory solutions, pushing manufacturers like Samsung and SK Hynix to expand production capacities. However, geopolitical tensions and export restrictions pose potential supply chain challenges.

North America

North America remains a critical hub for advanced DRAM solutions, particularly in high-performance computing (HPC) and cloud services. The U.S. hosts major hyperscalers such as AWS, Google, and Microsoft, which collectively drove 35% of regional DRAM demand in 2024. Investments in AI infrastructure and federal initiatives like the CHIPS Act have accelerated adoption of energy-efficient DDR5 modules. Canada and Mexico are witnessing steady growth due to increasing enterprise cloud migration, though their markets remain smaller compared to the U.S. The region prioritizes RDIMM and MRDIMM technologies for bandwidth-intensive applications.

Europe

Europe’s DRAM market is shaped by stringent data sovereignty laws (e.g., GDPR) and sustainability mandates, compelling data center operators to adopt energy-optimized memory solutions. Germany, the UK, and France collectively represent 60% of regional DRAM consumption, with a focus on modular and heterogeneous memory architectures. The European Chips Act has spurred local R&D in low-power DDR variants, but reliance on Asian suppliers persists. Hyperscale growth is tempered by energy crisis aftershocks, leading to selective investments in liquid-cooled server farms with efficient DRAM configurations.

South America

South America’s DRAM market is emerging, with Brazil and Argentina accounting for 75% of regional demand. Limited local data center infrastructure results in higher dependence on imported UDIMM and SODIMM modules for cost-sensitive deployments. While cloud adoption is rising steadily, economic instability and currency fluctuations hinder large-scale DRAM procurement. The region shows potential for growth as colocation providers expand, but progress lags behind global trends due to underdeveloped HPC ecosystems and modest 5G rollout speeds.

Middle East & Africa

This region exhibits niche demand concentrated in UAE, Saudi Arabia, and South Africa, where smart city initiatives and oil economy digitalization drive selective DRAM adoption. Hybrid cooling solutions deployed in desert data centers favor thermally resilient memory modules. Market maturity remains low, with most operators opting for standard RDIMMs over cutting-edge alternatives. Though investments like Saudi Arabia’s NEOM project signal long-term potential, current DRAM uptake is constrained by limited local manufacturing and fragmented supply chains.

Report Scope

This market research report provides a comprehensive analysis of the global DRAM for Data Centers market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global DRAM for Data Centers market was valued at USD 5,662 million in 2024 and is projected to reach USD 10,420 million by 2032, growing at a CAGR of 7.9% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (UDIMM, SODIMM, RDIMM, MRDIMM, LRDIMM, Others), application (IDC, EDC, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Samsung, SK Hynix, Micron Technology, and Changxin Memory Technologies (CXMT).

- Technology Trends & Innovation: Assessment of emerging technologies, including higher bandwidth and lower latency solutions, increased capacity with enhanced energy efficiency, and intelligent memory management systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing cloud computing demands and big data analytics, along with challenges like supply chain constraints and high manufacturing costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the DRAM for Data Centers market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DRAM for Data Centers Market?

-> DRAM for Data Centers Market was valued at 5662 million in 2024 and is projected to reach US$ 10420 million by 2032, at a CAGR of 7.9% during the forecast period.

Which key companies operate in Global DRAM for Data Centers Market?

-> Key players include Samsung, SK Hynix, Micron Technology, Changxin Memory Technologies (CXMT), Kingston Technology Company, Inc., and SMART Modular Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for cloud computing services, increasing data center investments, and the proliferation of AI and big data analytics applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by significant data center expansion in China and other emerging markets, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include development of high-capacity LRDIMM modules, energy-efficient memory solutions, and integration of advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...