MARKET INSIGHTS

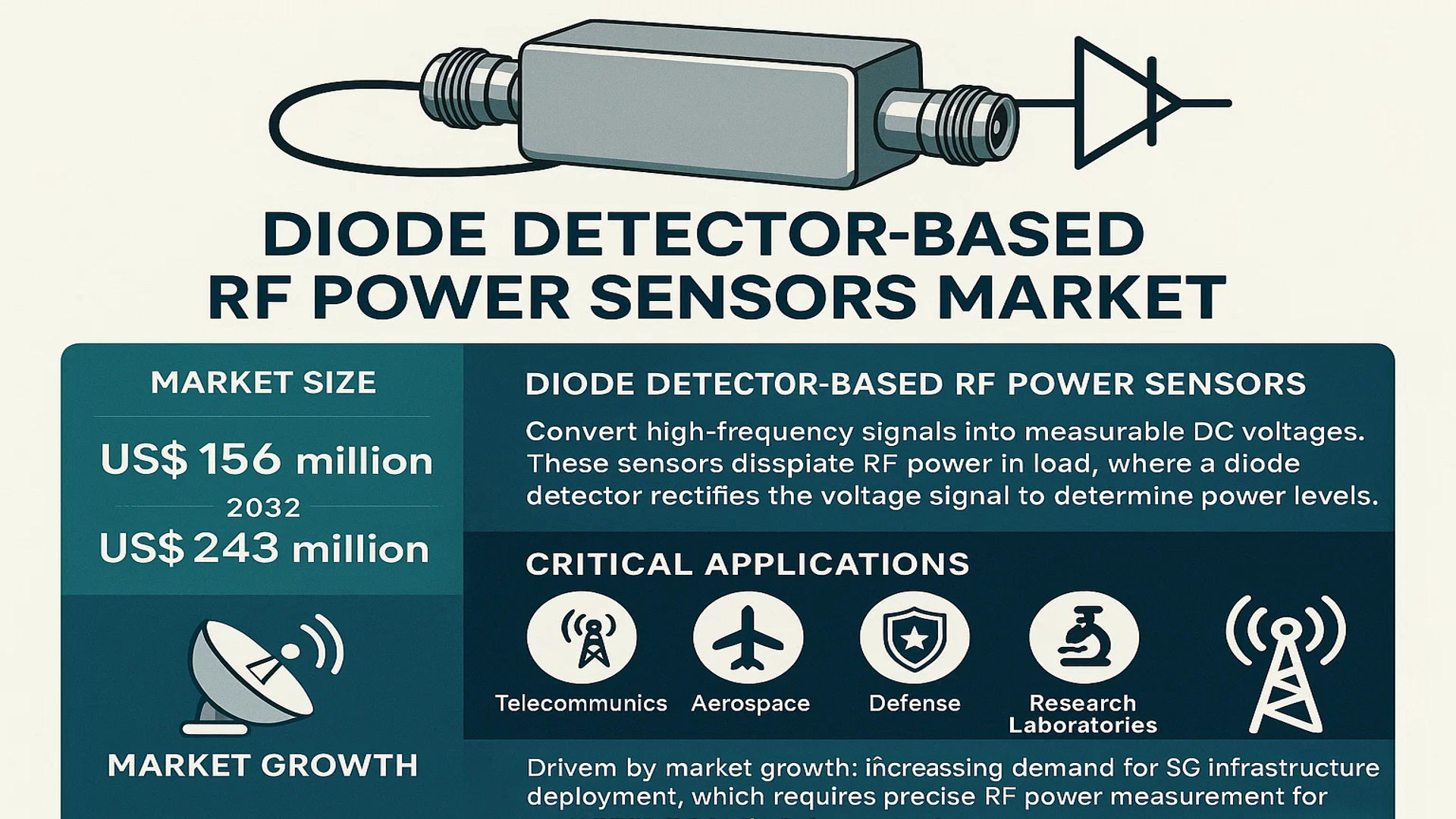

The global Diode Detector based RF Power Sensors Market size was valued at US$ 156 million in 2024 and is projected to reach US$ 243 million by 2032, at a CAGR of 6.6% during the forecast period 2025-2032.

Diode detector-based RF power sensors are precision measurement devices that convert high-frequency signals into measurable DC voltages. These sensors dissipate RF power in a load, where a diode detector rectifies the voltage signal to determine power levels. They are critical components in applications such as telecommunications, aerospace, defense, and research laboratories, offering high accuracy across wide frequency ranges.

The market growth is driven by increasing demand for 5G infrastructure deployment, which requires precise RF power measurement for network optimization. Furthermore, the expansion of satellite communication systems and advancements in radar technologies are contributing to market expansion. Key players like Keysight Technologies and Rohde & Schwarz are developing compact, high-performance sensors to meet evolving industry needs, particularly in portable and field applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for 5G Infrastructure Deployment Accelerates Market Growth

The global rollout of 5G networks is significantly driving demand for diode detector-based RF power sensors. These components are critical for base station testing and maintenance, ensuring accurate power measurements in mmWave frequencies. As telecom operators invest heavily in 5G infrastructure – with annual capital expenditures surpassing $200 billion globally – the need for precise RF measurement tools has intensified. Diode detectors offer advantages like wide dynamic range and fast response times, making them indispensable for 5G network optimization.

Increasing Defense and Aerospace Applications Fuel Market Expansion

Modern defense systems increasingly rely on diode detector sensors for radar, electronic warfare, and satellite communications. These applications require rugged, high-performance measurement solutions capable of operating in extreme environmental conditions. With defense budgets expanding globally – particularly in North America and Asia-Pacific regions – procurement of advanced RF measurement equipment is growing at approximately 8-10% annually. Military modernization programs specifically mandate the use of diode-based sensors for their reliability in mission-critical operations.

➤ Recent developments in gallium nitride (GaN) technology have enhanced diode detector capabilities, enabling new applications in phased array radar systems and 5G beamforming architectures.

Growth in IoT and Smart Device Manufacturing Creates New Demand

The explosion of IoT devices and smart technologies requires extensive RF testing during product development and manufacturing. Diode detector sensors play a vital role in radio frequency compliance testing, with the global IoT testing equipment market projected to grow at over 14% CAGR through 2030. Wireless connectivity standards like Wi-Fi 6 and Bluetooth 5.0 demand more sophisticated power measurement capabilities that diode-based solutions can provide economically.

MARKET RESTRAINTS

High Initial Investment Costs Limit Adoption in Price-Sensitive Markets

While diode detector sensors offer superior performance, their relatively higher costs compared to thermocouple-based alternatives create adoption barriers. Precision manufacturing requirements and specialized materials contribute to prices that can be 30-50% higher than competing technologies. This pricing disparity significantly impacts procurement decisions in cost-conscious markets like consumer electronics manufacturing and academic research institutions.

Other Restraints

Thermal Stability Challenges

Temperature sensitivity remains a key limitation for diode detectors, particularly in outdoor applications. Power measurement accuracy can drift by 0.1-0.3 dB/°C, requiring expensive temperature compensation circuits in critical applications. This technical constraint forces some users toward alternative sensing technologies in environments with extreme temperature variations.

Frequency Range Limitations

Traditional diode detectors face performance degradation above 40 GHz, constraining their usefulness in emerging mmWave applications. While recent technological advancements have extended this limit, the specialized components required for high-frequency operation add substantial cost, limiting market penetration in cutting-edge 5G and satellite communication systems.

MARKET CHALLENGES

Supply Chain Disruptions Impact Component Availability

The semiconductor shortages affecting global electronics markets have significantly impacted RF power sensor manufacturing. Specialty diodes and precision components face lead times extending beyond 6 months in some cases, disrupting production schedules. Industry reports indicate that 40-60% of sensor manufacturers experienced order delays in 2023, with the situation only gradually improving through 2024.

Skilled Workforce Shortage Limits Innovation Potential

The RF measurement industry faces a critical shortage of engineers proficient in both analog circuit design and high-frequency measurement techniques. With less than 15% of electrical engineering graduates specializing in RF technologies, companies struggle to maintain cutting-edge R&D teams. This talent gap slows the development of next-generation diode detector solutions needed to address emerging application requirements.

MARKET OPPORTUNITIES

Emerging Space and Satellite Applications Present Untapped Potential

The rapidly expanding commercial space sector creates new opportunities for RF power measurement technologies. With over 25,000 satellites expected to launch in the next decade, demand for space-qualified diode detectors is growing exponentially. These applications require radiation-hardened components capable of operating in extreme conditions – a niche where diode-based sensors excel. Companies developing specialized aerospace-grade solutions are well-positioned to capitalize on this $800+ million opportunity.

Integration with AI Creates Smart Measurement Solutions

The integration of machine learning algorithms with diode detector sensors enables predictive maintenance and automated calibration capabilities. This convergence of hardware and AI creates opportunities in industrial IoT applications, where smart RF sensors can monitor equipment health and optimize wireless system performance. Early adopters of AI-enhanced measurement solutions report 30-40% improvements in testing efficiency and equipment uptime.

DIODE DETECTOR BASED RF POWER SENSORS MARKET TRENDS

5G Network Expansion Driving Demand for Advanced RF Power Sensors

The global rollout of 5G infrastructure is significantly increasing the adoption of diode detector-based RF power sensors due to their accuracy in measuring high-frequency signals. These sensors play a crucial role in base station testing, ensuring proper power levels for stable network performance. The portable segment is projected to grow at a CAGR of approximately 9.2% from 2024 to 2032, as field technicians require compact solutions for on-site measurements. Furthermore, advancements in semiconductor technology have improved the linearity and dynamic range of diode sensors, making them indispensable for modern wireless communication systems.

Other Trends

Automation in Test & Measurement Equipment

The integration of diode-based RF sensors into automated test systems is transforming industrial applications. Manufacturers are incorporating these sensors with IoT-enabled platforms for real-time power monitoring in smart factories. This trend aligns with Industry 4.0 requirements, where precise RF measurements ensure optimal performance of wireless industrial devices. The laboratory usage segment currently holds over 35% market share but field applications are growing rapidly as wireless testing moves beyond controlled environments.

Defense & Aerospace Sector Fueling Technological Innovations

Military radar systems and avionics testing are creating specialized demand for ruggedized diode detector solutions. These applications require sensors with wider frequency ranges (up to 40 GHz) and better thermal stability compared to commercial versions. The U.S. maintains technological leadership in this segment, accounting for nearly 45% of defense-related RF sensor purchases globally. Recent product launches feature enhanced EMI shielding and extended calibration intervals specifically designed for harsh operational environments. Meanwhile, Asia Pacific is emerging as a growth hotspot with China’s defense modernization program allocating significant funds for RF test equipment upgrades.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations Drive Market Leadership in RF Power Sensing Technology

The global diode detector-based RF power sensors market exhibits a competitive landscape characterized by a mix of established multinational corporations and specialized manufacturers. Keysight Technologies and Rohde & Schwarz currently dominate the sector, collectively holding over 35% of the market share in 2024. Their leadership stems from comprehensive product portfolios spanning laboratory-grade precision instruments to rugged field-deployable solutions.

Yokogawa Electric Corporation and Anritsu Corporation maintain strong positions in the Asia-Pacific region, leveraging their expertise in industrial measurement systems. These companies have recently expanded their RF power sensor lines to address emerging 5G and IoT applications, with Yokogawa reporting a 12% year-on-year growth in this segment during Q1 2024.

Meanwhile, Teledyne Technologies has been aggressively pursuing market share through strategic acquisitions, including their 2023 purchase of a specialized RF components manufacturer. This move strengthened their position in aerospace and defense applications, which account for approximately 28% of global RF power sensor demand.

The market also features several innovative mid-size players such as Giga-tronics and Good Will Instruments, who compete through specialization in niche applications. Giga-tronics recently introduced a breakthrough in high-frequency diode detector technology, achieving 40% faster response times compared to industry standards.

List of Key Diode Detector Based RF Power Sensor Manufacturers

- Keysight Technologies (U.S.)

- Rohde & Schwarz (Germany)

- Yokogawa Electric Corporation (Japan)

- Anritsu Corporation (Japan)

- Teledyne Technologies (U.S.)

- Cobham Advanced Electronic Solutions (U.K.)

- Giga-tronics (U.S.)

- Chroma ATE Inc. (Taiwan)

- Good Will Instruments Co., Ltd. (Taiwan)

- B&K Precision Corporation (U.S.)

- Fortive Corporation (U.S.)

Product differentiation remains a critical competitive factor, with market leaders investing heavily in developing sensors with wider frequency ranges (up to 110 GHz in some premium models) and improved thermal stability. The industry has also seen growing emphasis on software integration, with leading vendors offering advanced signal processing algorithms as value-added features.

Recent market developments include a notable shift toward modular and programmable RF power sensors, particularly in telecommunications infrastructure deployments. Several manufacturers have formed strategic partnerships with network equipment providers to develop application-specific solutions, creating new growth opportunities in the competitive landscape.

Segment Analysis:

By Type

Portable Segment Leads Market Growth Owing to Increasing Demand for On-Site Measurements

The market is segmented based on type into:

- Portable

- Stationary

By Application

Directional Power Calculation Segment Dominates Due to Critical Role in RF System Analysis

The market is segmented based on application into:

- Directional Power Calculation

- Determining Total Power

- Indicating Peak Envelope Power

- Pulse Power Measurement

- Laboratory Usage

- Field Usage

By End-Use Industry

Telecommunications Sector Drives Adoption for Network Maintenance and Optimization

The market is segmented based on end-use industry into:

- Telecommunications

- Aerospace & Defense

- Electronics Manufacturing

- Research & Academia

- Others

By Frequency Range

GHz Range Segment Holds Significant Share for High-Frequency Applications

The market is segmented based on frequency range into:

- kHz Range

- MHz Range

- GHz Range

Regional Analysis: Diode Detector based RF Power Sensors Market

Asia-Pacific

The Asia-Pacific region dominates the global diode detector based RF power sensors market, driven by rapid technological advancements and expanding telecommunications infrastructure. China leads this growth, accounting for nearly 40% of regional demand, as 5G deployment accelerates across major cities. Japan and South Korea follow closely, with their established electronics manufacturing sectors driving innovation in sensor accuracy and miniaturization. India’s market is growing at above-average rates due to increasing RF testing requirements in defense and aerospace applications. While cost sensitivity remains a factor, manufacturers are shifting toward higher-value diode sensors with enhanced frequency ranges (up to 40 GHz) to meet evolving industry standards in wireless communication testing.

North America

North America maintains strong demand for high-precision diode detector RF power sensors, particularly in aerospace, defense, and semiconductor sectors. The U.S. holds approximately 65% of regional market share, with rigorous military RF testing protocols (including MIL-STD-461 compliance) sustaining demand. Major manufacturers like Keysight and Anritsu continue introducing compact, modular sensors for field applications. Canada shows increasing adoption in telecommunications infrastructure monitoring, while Mexico’s expanding electronics assembly plants generate steady demand for quality control sensors. The region prioritizes sensors with superior temperature stability (±0.5 dB) and fast response times (<1 µs) for critical RF power measurements in research and industrial applications.

Europe

Europe’s market emphasizes precision and regulatory compliance, with Germany and the U.K. as primary demand drivers. Stringent EMC directives and automotive RF testing standards (ECE R10) necessitate reliable diode-based sensors across vehicle-to-everything (V2X) communication systems. The Nordic countries demonstrate particular strength in R&D applications, with specialized sensors for millimeter-wave research. France and Italy show growing demand from aerospace sectors, where diode detectors provide crucial power measurements for satellite communication systems. European manufacturers focus on developing sensors with low measurement uncertainty (±1.5% typical) and wide dynamic ranges (up to 70 dB) to meet diverse application needs across industries.

Middle East & Africa

This emerging market shows gradual growth, primarily driven by defense sector investments and telecommunications infrastructure expansion. The UAE and Saudi Arabia account for over 50% of regional demand, deploying diode sensors in radar systems and 5G network testing. South Africa demonstrates potential in mineral exploration applications using specialized RF sensors. While market penetration remains limited by technical expertise gaps, partnerships with global manufacturers are improving access to advanced diode detector solutions. The region shows preference for ruggedized sensor models capable of operating in extreme environmental conditions (up to 55°C ambient temperature) with stable calibration performance.

South America

South America’s market progresses steadily, though economic volatility temporarily impacts capital expenditures in test and measurement equipment. Brazil leads regional adoption, particularly in academic research institutions and aerospace testing facilities. Argentina shows nascent demand growth in industrial RF applications, while Chile’s expanding astronomy sector utilizes specialized diode sensors for radio telescope systems. Local manufacturing remains limited, creating import dependency challenges. However, the region demonstrates increasing interest in cost-effective portable diode sensors (covering 100 MHz to 6 GHz range) suitable for field service applications in telecommunications maintenance.

Report Scope

This market research report provides a comprehensive analysis of the Global Diode Detector based RF Power Sensors Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Portable and Stationary), application (Directional Power Calculation, Determining Total Power, Indicating Peak Envelope Power, Pulse Power Measurement, Laboratory Usage, Field Usage), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Yokogawa, Teledyne, Cobham, Giga-tronics, Chroma, Good Will Instruments, B&K Precision, Anritsu, Fortive, Keysight, and Rohde & Schwarz, covering their product offerings, market share, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in RF power measurement, integration with IoT systems, and advancements in diode detector technology.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for wireless communication technologies, along with challenges like supply chain constraints and regulatory requirements.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving RF power sensor ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Diode Detector based RF Power Sensors Market?

-> Diode Detector based RF Power Sensors Market size was valued at US$ 156 million in 2024 and is projected to reach US$ 243 million by 2032, at a CAGR of 6.6% during the forecast period 2025-2032.

Which key companies operate in Global Diode Detector based RF Power Sensors Market?

-> Key players include Yokogawa, Teledyne, Cobham, Giga-tronics, Chroma, Good Will Instruments, B&K Precision, Anritsu, Fortive, Keysight, and Rohde & Schwarz.

What are the key growth drivers?

-> Key growth drivers include increasing demand for wireless communication technologies, expansion of 5G networks, and growing adoption in aerospace & defense applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to witness the highest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include development of miniaturized sensors, integration with IoT platforms, and increasing adoption of gallium arsenide (GaAs) diode technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...