MARKET INSIGHTS

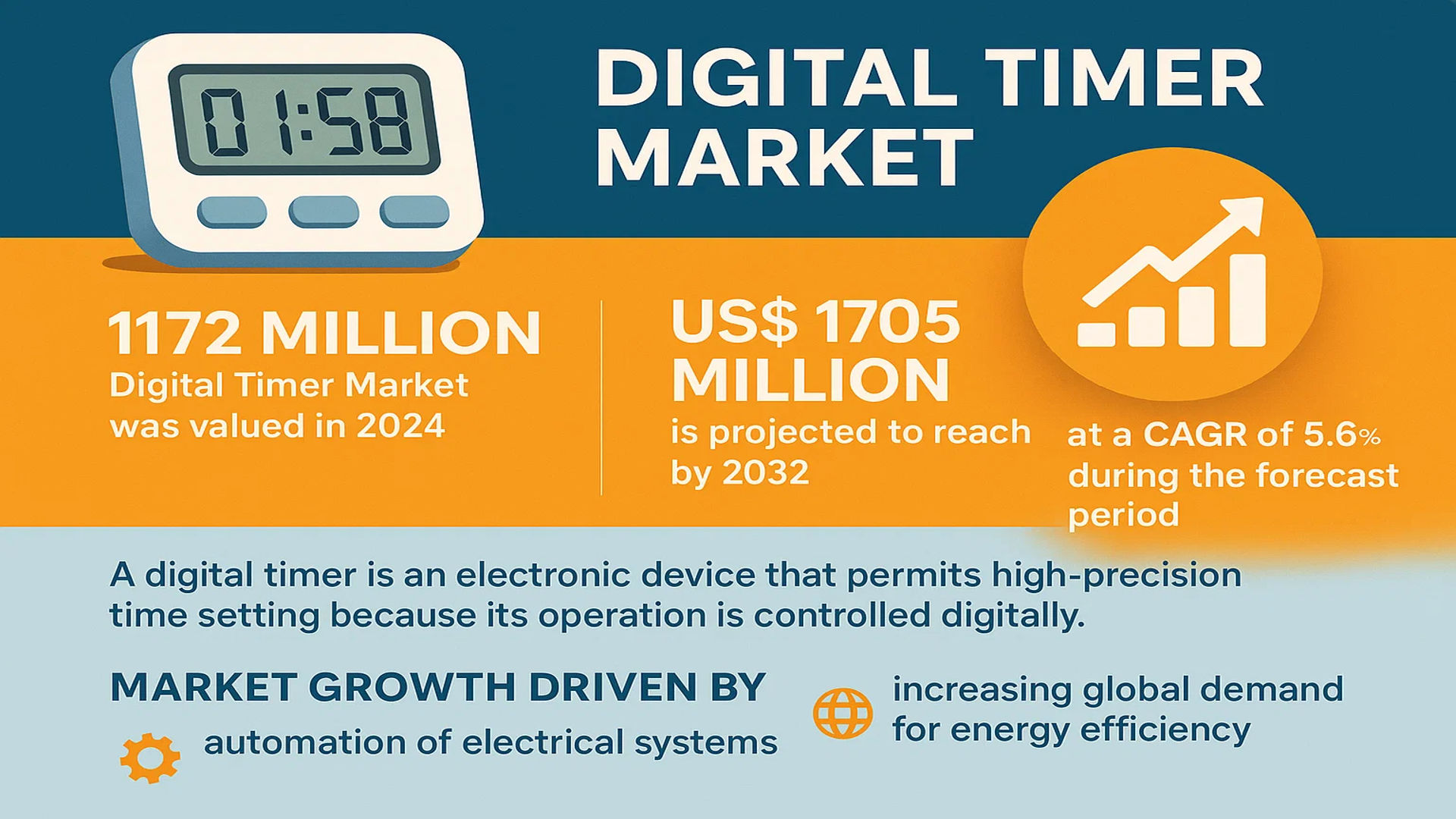

The global Digital Timer Market was valued at 1172 million in 2024 and is projected to reach US$ 1705 million by 2032, at a CAGR of 5.6% during the forecast period.

A digital timer is an electronic device that permits high-precision time setting because its operation is controlled digitally. These devices utilize digital switches for easy configuration and can digitally display the elapsed time, offering superior accuracy and user interface clarity compared to their analog counterparts. They are fundamental components in automating processes across residential, commercial, and industrial settings.

The market growth is primarily driven by the increasing global demand for energy efficiency and the automation of electrical systems. Furthermore, the expansion of smart home infrastructure and the rising adoption of Industrial Internet of Things (IIoT) solutions are significant contributors. North America holds the largest market share, accounting for over 30% of global revenue, followed closely by China and Europe. Key players such as Honeywell, Schneider Electric, and Legrand dominate the competitive landscape, with the top five manufacturers collectively holding over 20% of the market share.

MARKET DYNAMICS

MARKET DRIVERS

Global Smart Home and Building Automation Expansion Driving Digital Timer Adoption

The proliferation of smart home technologies and building automation systems represents a primary growth driver for the digital timer market. The global smart home market is experiencing exponential growth, with projections indicating adoption rates increasing by over 15% annually across developed markets. Digital timers serve as fundamental components in these systems, enabling precise scheduling of lighting, HVAC, and appliance operations. The transition from traditional electromechanical timers to digital counterparts is accelerating due to their superior accuracy, programmability, and integration capabilities with IoT ecosystems. Modern digital timers offer precision within milliseconds, compared to mechanical timers that typically maintain accuracy within 30 seconds, representing a significant improvement in operational efficiency. This enhanced precision is particularly crucial in industrial applications where timing discrepancies can result in substantial production losses or safety hazards.

Energy Efficiency Regulations and Sustainability Initiatives Boosting Market Demand

Stringent energy efficiency regulations worldwide are compelling commercial and residential property owners to adopt energy management solutions, including digital timers. Many countries have implemented building codes requiring automatic lighting controls in commercial buildings, with digital timers being among the most cost-effective compliance solutions. The European Union’s Energy Performance of Buildings Directive mandates that all new buildings must be nearly zero-energy by 2025, driving increased adoption of energy-saving devices. Digital timers contribute significantly to energy conservation by eliminating unnecessary energy consumption during unoccupied hours. Studies indicate that properly programmed digital timers can reduce lighting energy consumption by 25-30% in commercial applications and 10-15% in residential settings. This energy reduction capability aligns with global sustainability goals and corporate social responsibility initiatives, further accelerating market adoption across multiple sectors.

Industrial Automation and Industry 4.0 Integration Fueling Market Growth

The ongoing industrial automation revolution and Industry 4.0 implementation are creating substantial demand for precision timing devices across manufacturing sectors. Digital timers are integral to automated production lines, process control systems, and equipment sequencing operations. The manufacturing sector’s digital transformation requires timing accuracy that mechanical devices cannot provide, particularly in high-speed production environments where timing discrepancies measured in milliseconds can cause significant quality issues. The automotive manufacturing industry alone utilizes thousands of digital timers in assembly lines for controlling robotic operations, conveyor systems, and quality testing procedures. The precision offered by digital timers enables manufacturers to optimize production cycles, reduce waste, and maintain consistent product quality, making them indispensable components in modern industrial operations.

MARKET RESTRAINTS

Price Sensitivity in Emerging Markets Limiting Adoption Rates

Despite technological advantages, digital timers face significant price sensitivity challenges in emerging economies and cost-conscious market segments. The price differential between basic mechanical timers and entry-level digital timers remains substantial, with digital variants typically costing 200-300% more than their mechanical counterparts. This price gap creates adoption barriers in price-sensitive markets where initial cost often outweighs long-term benefits. In developing regions, where electrical infrastructure modernization occurs gradually, consumers and businesses frequently prioritize basic functionality over advanced features. The agricultural sector in emerging economies, which represents a substantial potential market for irrigation timing applications, particularly demonstrates resistance to digital timer adoption due to budget constraints and perceived complexity. This price sensitivity is further exacerbated by local manufacturing of low-cost mechanical timers that satisfy basic timing requirements without the premium associated with digital technology.

Technical Complexity and User Interface Challenges Hindering Widespread Adoption

Digital timer interfaces, while offering advanced functionality, present usability challenges that restrain market growth among non-technical users. Many residential and small business users find digital programming interfaces confusing compared to the straightforward dial-setting mechanism of mechanical timers. The learning curve associated with programming multiple on/off cycles, holiday settings, and randomizer functions often discourages potential adopters. Industry assessments indicate that approximately 35% of digital timer returns occur due to user difficulty in programming rather than product malfunction. This usability challenge is particularly pronounced among older demographic segments and in applications where infrequent reprogramming is necessary. Manufacturers face the ongoing challenge of balancing advanced features with intuitive user interfaces, as overly simplified interfaces may not support the complex scheduling requirements that justify digital timer adoption in the first place.

Competition from Integrated Smart Home Systems Constraining Standalone Timer Market

The digital timer market faces increasing competition from integrated smart home systems and building automation platforms that incorporate timing functionality within broader control systems. As smart home adoption accelerates, consumers increasingly prefer comprehensive solutions that combine timing, sensing, and control capabilities rather than standalone timing devices. Major smart home platform providers are incorporating sophisticated scheduling capabilities directly into their hubs and controllers, reducing the need for separate digital timers. This trend is particularly evident in the residential sector, where whole-home automation systems can manage lighting, climate, and appliance scheduling through centralized control interfaces. The convenience of managing all automated functions through a single interface diminishes the appeal of individual digital timers, despite their specialized capabilities. This integration trend requires digital timer manufacturers to either develop compatible smart home integrations or risk becoming redundant in increasingly connected environments.

MARKET CHALLENGES

Technological Obsolescence and Rapid Innovation Cycle Creating Market Pressures

The digital timer market faces significant challenges related to technological obsolescence and compressed product life cycles. Rapid advancements in wireless communication protocols, IoT integration capabilities, and user interface technologies render existing products obsolete within increasingly shorter timeframes. Manufacturers must continuously invest in research and development to maintain competitiveness, with development cycles for new digital timer models now averaging 18-24 months compared to 5-7 years for mechanical timers. This accelerated innovation cycle creates substantial financial pressure, particularly for small and medium-sized manufacturers with limited R&D budgets. The constant need for technological upgrades also affects inventory management, as older models become difficult to sell once newer versions with enhanced features enter the market. This challenge is compounded by the extended product lifespan of digital timers, which typically operate reliably for 7-10 years, creating a replacement market that evolves slower than technological innovation.

Other Challenges

Supply Chain Vulnerabilities

Global supply chain disruptions continue to challenge digital timer manufacturers, particularly regarding electronic components and display technologies. The industry experienced significant component shortages and price fluctuations following recent global events, with lead times for microcontrollers and LCD displays extending to 52 weeks in some cases. These supply chain challenges force manufacturers to either maintain larger inventory buffers, increasing carrying costs, or risk production delays that affect market responsiveness.

Cybersecurity Concerns

As digital timers become increasingly connected to networks and IoT systems, cybersecurity vulnerabilities present growing challenges. Network-connected digital timers can potentially serve as entry points for cyber attacks on building management systems or industrial control networks. Addressing these security concerns requires additional investment in encryption, authentication protocols, and ongoing firmware updates, increasing development costs and complexity.

MARKET OPPORTUNITIES

IoT Integration and Smart City Development Creating New Growth Avenues

The integration of digital timers with Internet of Things platforms and smart city infrastructure presents substantial growth opportunities across multiple application segments. Municipalities worldwide are investing in smart street lighting systems that require sophisticated timing controls integrated with light sensors and network connectivity. These systems enable cities to optimize energy consumption while maintaining public safety through precisely controlled lighting schedules. The global smart street lighting market is projected to grow significantly, creating corresponding demand for advanced digital timing solutions. Digital timer manufacturers are developing products with built-in wireless connectivity, remote programming capabilities, and integration with central management systems. These connected timers enable facility managers to monitor and adjust timing schedules across multiple locations from centralized dashboards, providing operational flexibility that mechanical timers cannot offer. The ability to implement complex scheduling patterns, including seasonal adjustments and special event programming, makes digital timers essential components in modern urban infrastructure projects.

Renewable Energy Integration and Microgrid Applications Driving Specialty Timer Demand

The expanding renewable energy sector and development of microgrid systems create specialized opportunities for advanced digital timers with enhanced reliability and precision capabilities. Solar and wind energy installations require precise timing controls for synchronization with conventional power grids, load management, and storage system optimization. Digital timers in these applications must maintain exceptional accuracy and operate reliably in harsh environmental conditions. The global transition toward renewable energy sources is driving investment in supporting infrastructure, including advanced control systems where digital timers play critical roles. Microgrid applications particularly benefit from digital timers capable of managing complex power switching sequences, generator start/stop controls, and demand response operations. These specialized applications often command premium pricing due to their critical nature and technical requirements, providing higher-margin opportunities for manufacturers with the technical capability to meet stringent performance specifications.

Retrofit Market and Infrastructure Modernization Offering Sustained Growth Potential

The extensive installed base of outdated timing systems in commercial, industrial, and municipal infrastructure represents a substantial long-term opportunity for digital timer replacement and upgrades. Many facilities continue using electromechanical timers installed decades ago, creating a replacement market driven by reliability concerns, energy efficiency improvements, and functionality enhancements. Building owners and facility managers increasingly recognize that modern digital timers can provide rapid return on investment through energy savings alone, with payback periods typically ranging from 12-24 months in commercial lighting applications. Government incentives and energy efficiency programs further accelerate replacement cycles by subsidizing upgrades to digital control systems. The retrofit market is particularly robust in regions with aging infrastructure and strong energy conservation policies, creating predictable demand patterns that manufacturers can target with specific product offerings designed for replacement applications rather than new construction.

DIGITAL TIMER MARKET TRENDS

Integration with Smart Home Ecosystems Emerges as Dominant Trend

The proliferation of smart home technology is fundamentally reshaping the digital timer landscape, driving demand for connected, intelligent devices. Digital timers are increasingly being integrated into broader Internet of Things (IoT) ecosystems, allowing for remote control via smartphones and synchronization with other smart appliances. This connectivity enables advanced features such as energy consumption monitoring, automated scheduling based on user behavior, and voice control through platforms like Amazon Alexa and Google Assistant. The global smart home market’s expansion, which is projected to exceed a value of $500 billion by 2030, provides a powerful tailwind for this segment. Manufacturers are responding by embedding Wi-Fi and Bluetooth modules into their timers, moving beyond simple electromechanical switching to offer comprehensive home automation solutions that prioritize both convenience and energy efficiency.

Other Trends

Energy Efficiency and Sustainability Mandates

Global emphasis on reducing carbon footprints and improving energy efficiency is a significant catalyst for the digital timer market. Governments and regulatory bodies worldwide are implementing stricter energy codes for both residential and commercial buildings, mandating the use of automated control systems to minimize wasteful energy consumption. Digital timers are crucial components in these systems, precisely managing the operation of HVAC units, lighting, and industrial equipment to align with occupancy patterns and peak/off-peak energy tariffs. This trend is particularly pronounced in regions with high energy costs and ambitious sustainability targets, where the return on investment for an energy-saving timer can be realized in a relatively short period, further accelerating adoption rates across various sectors.

Industrial Automation and Industry 4.0 Adoption

The ongoing transition towards Industry 4.0 and fully automated manufacturing processes is creating robust demand for high-precision, reliable digital timers in industrial applications. These devices are integral to programmable logic controllers (PLCs) and automated assembly lines, where they manage timing sequences for machinery operation, process control, and safety interlocks with millisecond accuracy. The need for reduced downtime, enhanced production efficiency, and improved product quality is pushing manufacturers to upgrade from older analog timers to digital variants that offer greater programming flexibility, diagnostics, and network connectivity. This trend is supported by sustained investment in industrial automation, with the global market expected to maintain a strong growth trajectory, thereby ensuring a steady stream of demand for advanced digital timing solutions in manufacturing and process industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Innovation and Global Expansion Define Market Leadership

The global digital timer market exhibits a fragmented yet competitive structure, characterized by the presence of multinational conglomerates, specialized electronics firms, and regional manufacturers. This dynamic creates a landscape where innovation, distribution networks, and brand reputation are critical differentiators. The market’s semi-consolidated nature means that while a few major players hold significant influence, numerous smaller companies successfully compete by catering to niche applications or specific geographic markets.

Honeywell and Schneider Electric are recognized as dominant forces, collectively holding a substantial portion of the global market share. Their leadership is underpinned by extensive product portfolios that span both simple consumer-grade timers and sophisticated industrial programmable versions. Furthermore, their robust global distribution and supply chain networks ensure product availability across North America, Europe, and the rapidly growing Asia-Pacific region, solidifying their market positions.

Established players like Legrand and Panasonic also command considerable market share, leveraging their strong brand equity and deep integration into the building automation and consumer electronics sectors, respectively. Their growth is largely driven by continuous investment in research and development, leading to the introduction of energy-efficient and smart-connected timers that align with global trends in IoT and building management systems.

Meanwhile, companies such as Omron and Eaton are strengthening their standing through strategic mergers and acquisitions, technological enhancements, and a focused approach on high-value industrial automation segments. Their efforts to develop timers with higher precision, durability, and connectivity features are key to capturing growth in the industrial device application, which is a major end-use sector.

List of Key Digital Timer Companies Profiled

- Honeywell International Inc. (U.S.)

- Schneider Electric SE (France)

- Legrand S.A. (France)

- Panasonic Corporation (Japan)

- Leviton Manufacturing Co., Inc. (U.S.)

- Intermatic Incorporated (U.S.)

- Omron Corporation (Japan)

- Eaton Corporation plc (Ireland)

- Larsen & Toubro Limited (India)

- Havells India Ltd. (India)

Segment Analysis:

By Type

LCD Display Digital Timer Segment Dominates the Market Due to Superior Readability and Versatility

The market is segmented based on type into:

- LED Display Digital Timer

- LCD Display Digital Timer

By Application

Lighting System Segment Leads Due to Widespread Adoption in Energy Management and Automation

The market is segmented based on application into:

- Industrial Device

- Lighting System

- Others

By End User

Commercial Segment Leads Due to High Demand for Automation and Energy Efficiency

The market is segmented based on end user into:

- Residential

- Commercial

- Industrial

By Technology

Programmable Segment Leads Due to Advanced Features and Customization Capabilities

The market is segmented based on technology into:

- Basic Digital Timer

- Programmable Digital Timer

- Smart Digital Timer

Regional Analysis: Digital Timer Market

North America

North America is the largest market for digital timers globally, holding over 30% market share. This dominance is driven by widespread adoption in residential, commercial, and industrial applications, supported by stringent energy efficiency standards and a robust smart home infrastructure. The United States, in particular, is a major contributor due to high consumer awareness and the presence of key market players like Honeywell, Leviton, and Intermatic. The region’s focus on energy conservation and the integration of IoT in building automation systems are significant growth drivers. However, market maturity means growth rates are steady rather than explosive, with innovation focused on connectivity and user-friendly interfaces.

Europe

Europe represents a highly developed market for digital timers, characterized by strong environmental regulations and a push towards sustainable energy usage. The EU’s energy efficiency directives and the growth of smart city projects across countries like Germany, France, and the U.K. fuel demand. The market is sophisticated, with a high preference for advanced, programmable timers integrated into home and industrial automation systems. Leading companies such as Schneider Electric and Legrand have a strong foothold here. While the market is well-established, replacement demand and technological upgrades, particularly in wireless and app-controlled timers, continue to provide opportunities for growth.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for digital timers, propelled by rapid industrialization, urbanization, and increasing investments in infrastructure development. China and India are the primary engines of this growth, accounting for a significant volume share. The market here is highly price-sensitive, with a strong presence of local manufacturers offering cost-effective solutions. However, there is a noticeable and growing shift towards more reliable and feature-rich timers, especially in the industrial and commercial sectors. The burgeoning middle class and government initiatives promoting energy efficiency are gradually increasing the adoption of digital timers in residential applications as well.

South America

The digital timer market in South America is in a developing phase, experiencing gradual growth. Economic volatility in key countries like Brazil and Argentina often impacts investment in new technologies, slowing down market expansion. The primary demand stems from the industrial sector and specific commercial applications. While awareness of energy-saving benefits is increasing, price sensitivity remains a significant barrier to the widespread adoption of advanced digital timer solutions. The market potential is recognized, but realization is dependent on improved economic stability and greater regulatory support for energy management.

Middle East & Africa

This region presents an emerging market for digital timers, with growth primarily concentrated in more developed economies and urban centers. The United Arab Emirates, Saudi Arabia, and South Africa are seeing increased demand driven by commercial construction, hospitality, and industrial projects. However, the market’s development is uneven across the region. Limited awareness, lower prioritization of energy efficiency in some areas, and a preference for lower-cost alternatives currently restrict more robust growth. Nonetheless, long-term potential exists as infrastructure development continues and the focus on modernizing building management systems intensifies.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Digital Timer markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital Timer Market?

-> Digital Timer Market was valued at 1172 million in 2024 and is projected to reach US$ 1705 million by 2032, at a CAGR of 5.6% during the forecast period.

Which key companies operate in Global Digital Timer Market?

-> Key players include Honeywell, Leviton, Legrand, Intermatic, Schneider Electric, Panasonic, Omron, and Eaton, among others.

What are the key growth drivers?

-> Key growth drivers include smart home adoption, industrial automation, energy efficiency regulations, and infrastructure modernization.

Which region dominates the market?

-> North America holds the largest market share (over 30%), followed by China and Europe.

What are the emerging trends?

-> Emerging trends include IoT integration, wireless connectivity, touchscreen interfaces, and cloud-based timer management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...