MARKET INSIGHTS

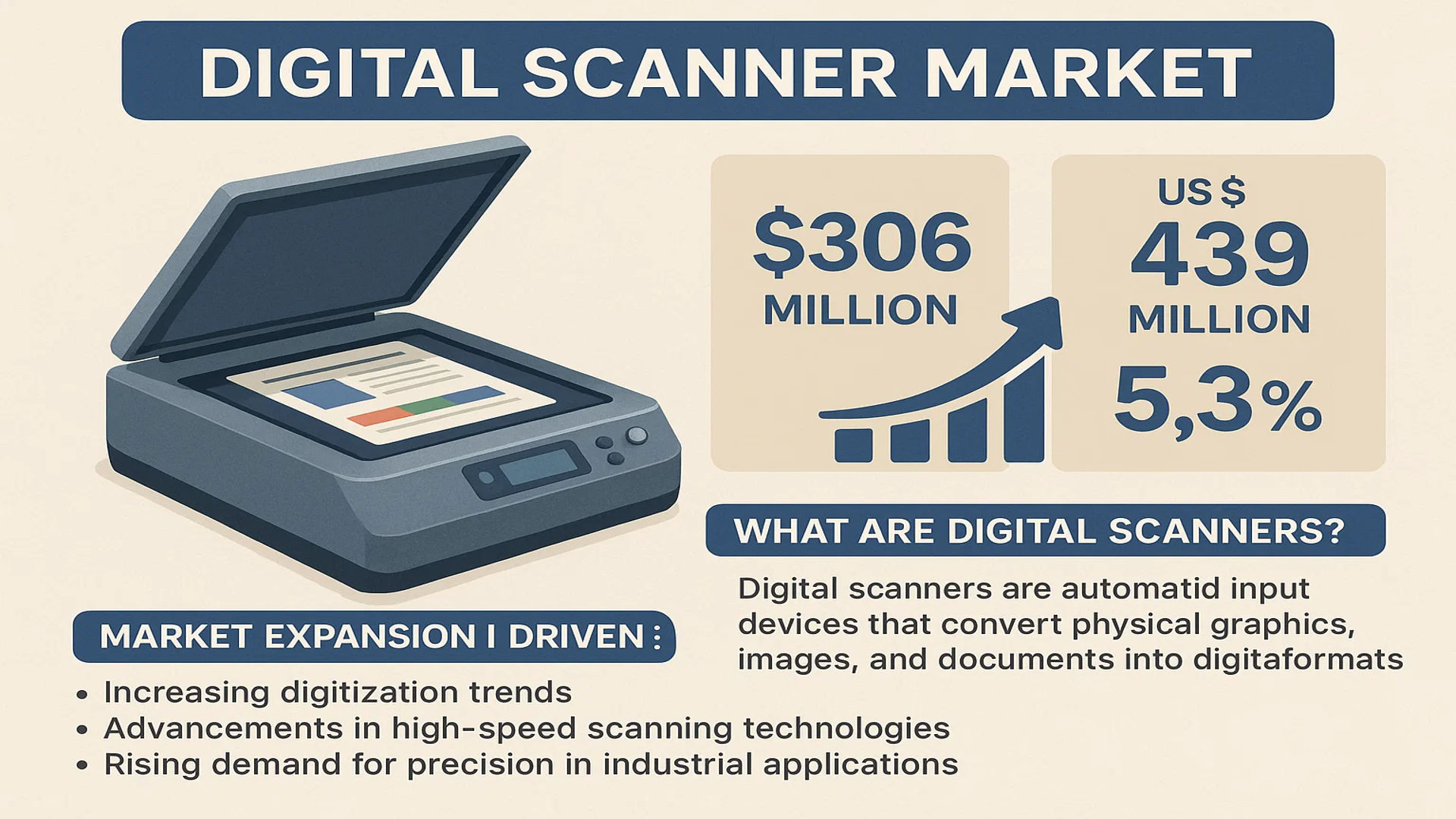

The global Digital Scanner Market was valued at 306 million in 2024 and is projected to reach US$ 439 million by 2032, at a CAGR of 5.3% during the forecast period.

Digital scanners are automated input devices that convert physical graphics, images, and documents into digital formats. Utilizing photoelectric technology, these devices detect light signals, transform them into electrical signals, and further convert them into digital data via analog-to-digital (A/D) converters. The processed data is then transmitted to computers for editing, storage, or output. These scanners are widely adopted across industries such as manufacturing, healthcare, and cultural preservation for applications like quality control, 3D modeling, and archival digitization.

Market expansion is driven by increasing digitization trends, advancements in high-speed scanning technologies, and rising demand for precision in industrial applications. The U.S. holds a dominant market position, while China exhibits rapid growth potential. Key players like FARO Technologies, Hexagon, and 3D Systems are focusing on innovation and strategic partnerships to strengthen their market presence. For instance, handheld and high-speed scanners are gaining traction due to their portability and efficiency, contributing to segment growth.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Speed 3D Scanning in Industrial Applications Accelerates Market Growth

The digital scanner market is experiencing robust growth due to increasing adoption in industrial manufacturing and quality control applications. Advanced 3D scanning technologies enable rapid measurement and inspection of complex components with micron-level precision, reducing production errors by up to 40% compared to traditional methods. Industries such as aerospace, automotive, and heavy machinery are investing heavily in portable 3D scanners to streamline reverse engineering and metrology processes, with high-speed models accounting for nearly 32% of total market revenue in 2024.

Healthcare Digitization Boom Expands Scanning Adoption

Medical facilities worldwide are transitioning to digital workflows, driving demand for specialized document and imaging scanners. The hospital digitization rate has increased from 58% in 2020 to over 72% in 2024, creating sustained demand for high-volume document scanners. Meanwhile, handheld 3D scanners are revolutionizing patient-specific medical device manufacturing and surgical planning, with dental applications alone representing 18% of the medical scanning segment. This dual demand from administrative and clinical applications creates robust growth opportunities across scanner categories.

➤ The integration of AI-powered auto-categorization in document scanners has reduced medical records processing time by 65%, accelerating ROI for healthcare providers.

Furthermore, government mandates for electronic health records and the expansion of telemedicine services globally continue to fuel scanner adoption in the healthcare vertical. This sector is projected to maintain a 7.2% CAGR through 2032, exceeding overall market growth rates.

MARKET RESTRAINTS

High Initial Investment Costs Restrict SME Adoption

While premium 3D scanning systems deliver exceptional accuracy, their substantial upfront costs create barriers for small and mid-sized enterprises. Industrial-grade scanners with sub-millimeter precision carry price tags exceeding $50,000, requiring 18-24 months for ROI realization. This pricing structure has limited penetration in price-sensitive emerging markets where manual measurement alternatives remain prevalent. Even document scanning solutions with advanced features often carry 30-40% cost premiums over basic models, slowing replacement cycles.

Technical Complexities in High-Precision Applications

Achieving consistent accuracy in challenging environments presents ongoing technical hurdles. Factors like surface reflectivity, ambient lighting conditions, and material properties can degrade scan quality, requiring expensive add-ons or repeated scans. The learning curve for advanced scanning software remains steep, with certification programs typically requiring 80+ hours of training for full operator competency. These technical barriers discourage rapid scaling in industrial environments where reliability is paramount.

MARKET OPPORTUNITIES

Emerging Hybrid Scanning Technologies Open New Application Avenues

The convergence of photogrammetry and structured light scanning presents transformative opportunities across multiple sectors. Next-gen hybrid systems combine the portability of handheld scanners with the accuracy of fixed systems, achieving tolerances under 0.01mm while reducing setup time by 60%. These advancements are unlocking new use cases in areas like heritage preservation, where high-detail scanning of delicate artifacts was previously impractical. Similarly, manufacturing applications benefit from hybrid systems’ ability to capture both macro geometries and micro surface details simultaneously.

Cloud-Based Scanning Ecosystems Create Recurring Revenue Streams

Scanner manufacturers are transitioning towards service-based models through cloud platform integrations. These solutions enable real-time data processing, remote collaboration, and AI-powered analysis – features that command 20-30% premium subscription fees. Early adopters report 40% higher customer retention rates with cloud-connected devices compared to standalone units. The shift also facilitates predictive maintenance capabilities through IoT connectivity, reducing field service costs while improving equipment uptime.

MARKET CHALLENGES

Intense Market Competition Squeezes Profit Margins

The digital scanner landscape has become increasingly crowded, with over 50 active manufacturers competing across price segments. Industry-wide average selling prices have declined 12% since 2020 due to Chinese manufacturers entering mid-range markets. While premium brands maintain technological advantages, the proliferation of “good enough” alternatives at 40-50% lower price points pressures R&D budgets. This competitive dynamic forces continuous innovation while maintaining cost discipline – a balance that challenges even established players.

Regulatory Compliance Adds Development Complexity

Evolving data security standards and product certifications create development bottlenecks. Medical scanners must comply with HIPAA, GDPR, and various regional healthcare data protocols, adding 6-9 months to product cycles. Industrial models require UL, CE, and other safety certifications that vary by territory. These compliance requirements increase time-to-market while raising development costs by an estimated 15-20%, particularly for global product launches.

DIGITAL SCANNER MARKET TRENDS

Demand for High-Speed Scanning Solutions to Drive Market Growth

The digital scanner market is witnessing significant growth, driven by the rising need for high-speed scanning solutions across industries such as manufacturing, healthcare, and cultural heritage preservation. With increasing digitization, companies are adopting automated scanning devices to streamline data capture, enhance accuracy, and reduce operational costs. High-speed scanners, which now account for over 40% of global market revenue, enable rapid processing of large-scale documents, 3D models, and engineering blueprints. These scanners are particularly crucial in manufacturing, where precision and efficiency in reverse engineering and quality control are paramount.

Other Trends

Adoption of Handheld 3D Scanners in Healthcare

The healthcare sector is increasingly leveraging digital scanners, especially handheld 3D variants, for medical imaging, prosthetics design, and surgical planning. A growing aging population and advancements in minimally invasive surgical techniques are boosting the adoption of precise scanning devices. In dentistry, for example, digital intraoral scanners have reduced traditional mold-taking processes from hours to minutes, improving patient comfort and workflow efficiency. The healthcare segment is projected to grow at a CAGR of 6.8% by 2032, driven by expanding applications in telemedicine and remote diagnostics.

Integration of AI and Cloud-Based Scanning Solutions

Artificial Intelligence (AI) and cloud-based processing are transforming digital scanners into smart, connected devices. Advanced algorithms now enhance image recognition, noise reduction, and automated measurement extraction—reducing human intervention by up to 30%. Cloud integration allows real-time data sharing and collaborative workflows, particularly beneficial for global engineering teams and archival projects. Museums, for instance, utilize AI-powered scanners for artifact preservation, creating high-resolution digital twins that can be studied without risking damage to original pieces.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competitive Edge in Digital Scanning

The global digital scanner market features a diverse mix of established multinational players and emerging challengers. With industrial applications expanding across manufacturing, healthcare, and cultural preservation sectors, competitors are aggressively investing in higher precision, faster processing speeds, and AI-powered scanning solutions. This technological arms race is reshaping market dynamics as companies position themselves for the projected $439 million valuation by 2032.

FARO Technologies and Hexagon currently dominate the high-end segment, leveraging their expertise in industrial measurement systems. Both companies reported year-over-year revenue growth in their digital scanning divisions through 2024, capitalizing on demand from automotive and aerospace manufacturers requiring sub-millimeter accuracy for quality control processes.

The handheld scanner segment sees intense competition between Artec 3D and Shining 3D, with both companies recently launching lighter, more ergonomic designs featuring real-time mesh processing. This innovation push comes as museums and archaeological teams increasingly adopt portable scanners for artifact preservation, creating a high-growth niche within the broader market.

Healthcare applications represent another battleground, where ZEISS and Nikon Metrology are making strategic inroads. Their medical-grade scanners demonstrate how the industry is moving beyond traditional manufacturing uses. Recent FDA clearances for diagnostic scanning systems indicate this segment could drive disproportionate growth in coming years, with companies actively forming partnerships with hospital networks and research institutions.

List of Key Digital Scanner Manufacturers Profiled

- FARO Technologies (U.S.)

- Creaform (Canada)

- Artec 3D (Luxembourg)

- 3D Systems (U.S.)

- Hexagon AB (Sweden)

- Shining 3D (China)

- Trimble Inc. (U.S.)

- Nikon Metrology (Japan)

- ZEISS Group (Germany)

- Hewlett-Packard Development Company (U.S.)

- Epson (Japan)

- NextEngine (U.S.)

- Leica Geosystems (Switzerland)

- Zebra Technologies (U.S.)

Segment Analysis:

By Type

High-Speed Scanners Lead the Market Owing to Rising Demand in Industrial and Medical Applications

The market is segmented based on type into:

- High-Speed Scanners

- Handheld Scanners

- Subtypes: Laser, Structured Light, and Others

- Desktop Scanners

- Other Specialized Scanners

By Application

Manufacturing and Engineering Design Segment Drives Market Growth Due to Increasing Automation and Digitalization

The market is segmented based on application into:

- Manufacturing and Engineering Design

- Cultural Heritage and Museums

- Medicine and Healthcare

- Subtypes: Dental Imaging, Prosthetics, and Others

- Architecture and Construction

- Other Applications

Regional Analysis: Digital Scanner Market

Asia-Pacific

The Asia-Pacific region dominates the global digital scanner market, accounting for the largest share in 2024, driven primarily by rapid industrialization and technological advancements in countries like China, Japan, and India. China, as the manufacturing hub of the world, witnesses significant adoption of high-speed digital scanners for industrial automation and quality control. Japan leads in precision engineering applications, particularly in electronics manufacturing. Meanwhile, India’s growing healthcare and infrastructure sectors are fueling demand for portable and handheld scanning solutions. The region benefits from strong government support for digital transformation initiatives and the presence of local manufacturers offering cost-competitive alternatives to international brands.

North America

North America represents the second-largest market for digital scanners, characterized by early adoption of advanced technologies and high investments in R&D. The U.S. leads the region with extensive applications in healthcare (for medical imaging and diagnostics), aerospace (for component inspection), and cultural heritage preservation. Strict quality standards in manufacturing and the presence of major players like FARO Technologies and 3D Systems drive innovation in high-precision scanning solutions. Canada’s growing engineering and construction sectors contribute to steady demand for 3D scanning technologies, particularly in infrastructure development projects.

Europe

Europe maintains a strong position in the digital scanner market, with Germany, France, and the U.K. as key contributors. The region excels in high-end industrial applications, especially in automotive manufacturing and aerospace, where precision scanning is critical for quality assurance. Strict EU regulations regarding product quality and safety standards encourage adoption of advanced scanning technologies. The cultural heritage sector also presents significant opportunities, with museums and conservation projects increasingly digitizing artifacts. European manufacturers focus on developing eco-friendly and energy-efficient scanners to align with the region’s sustainability goals.

South America

The South American digital scanner market is emerging, with Brazil and Argentina showing promising growth. While adoption rates trail behind more developed regions, increasing industrialization and infrastructure projects are driving demand, particularly in the construction and mining sectors. Economic volatility and limited technology budgets pose challenges, but the market benefits from growing awareness of digital scanning benefits in quality control and reverse engineering. Local manufacturers are entering the market with cost-effective solutions tailored to regional needs.

Middle East & Africa

This region demonstrates the fastest growth potential, albeit from a smaller base. The UAE and Saudi Arabia lead in adoption, fueled by smart city initiatives and infrastructure megaprojects requiring advanced scanning technologies. The oil & gas industry represents a key application area for inspection and maintenance. While limited local manufacturing capabilities result in reliance on imports, government initiatives to diversify economies are creating new opportunities. South Africa shows particular promise in healthcare and mining applications, though market expansion is constrained by infrastructure challenges in some areas.

Report Scope

This market research report provides a comprehensive analysis of the Global Digital Scanner market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Digital Scanner market was valued at USD 306 million in 2024 and is projected to reach USD 439 million by 2032, at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (High Speed, Handheld, Others), application (Manufacturing & Engineering Design, Cultural Heritage, Healthcare), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including FARO Technologies, Creaform, Artec 3D, 3D Systems, Hexagon, their product portfolios, R&D focus, and recent M&A activities.

- Technology Trends & Innovation: Assessment of photoelectric scanning technologies, A/D conversion advancements, and integration with digital workflows.

- Market Drivers & Restraints: Evaluation of digital transformation initiatives, Industry 4.0 adoption versus high equipment costs and technical complexity.

- Stakeholder Analysis: Strategic insights for OEMs, system integrators, and investors in the digital scanning ecosystem.

Research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital Scanner Market?

-> Digital Scanner Market was valued at 306 million in 2024 and is projected to reach US$ 439 million by 2032, at a CAGR of 5.3% during the forecast period.

Which key companies operate in Global Digital Scanner Market?

-> Key players include FARO Technologies, Creaform, Artec 3D, 3D Systems, Hexagon, Shining 3D, and Trimble, among others.

What are the key growth drivers?

-> Key growth drivers include digital transformation across industries, demand for high-precision scanning, and adoption in healthcare diagnostics.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific shows the highest growth potential.

What are the emerging trends?

-> Emerging trends include AI-powered scanning automation, portable handheld scanners, and integration with 3D printing technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...