Digital Health Sensor IC Market Insights

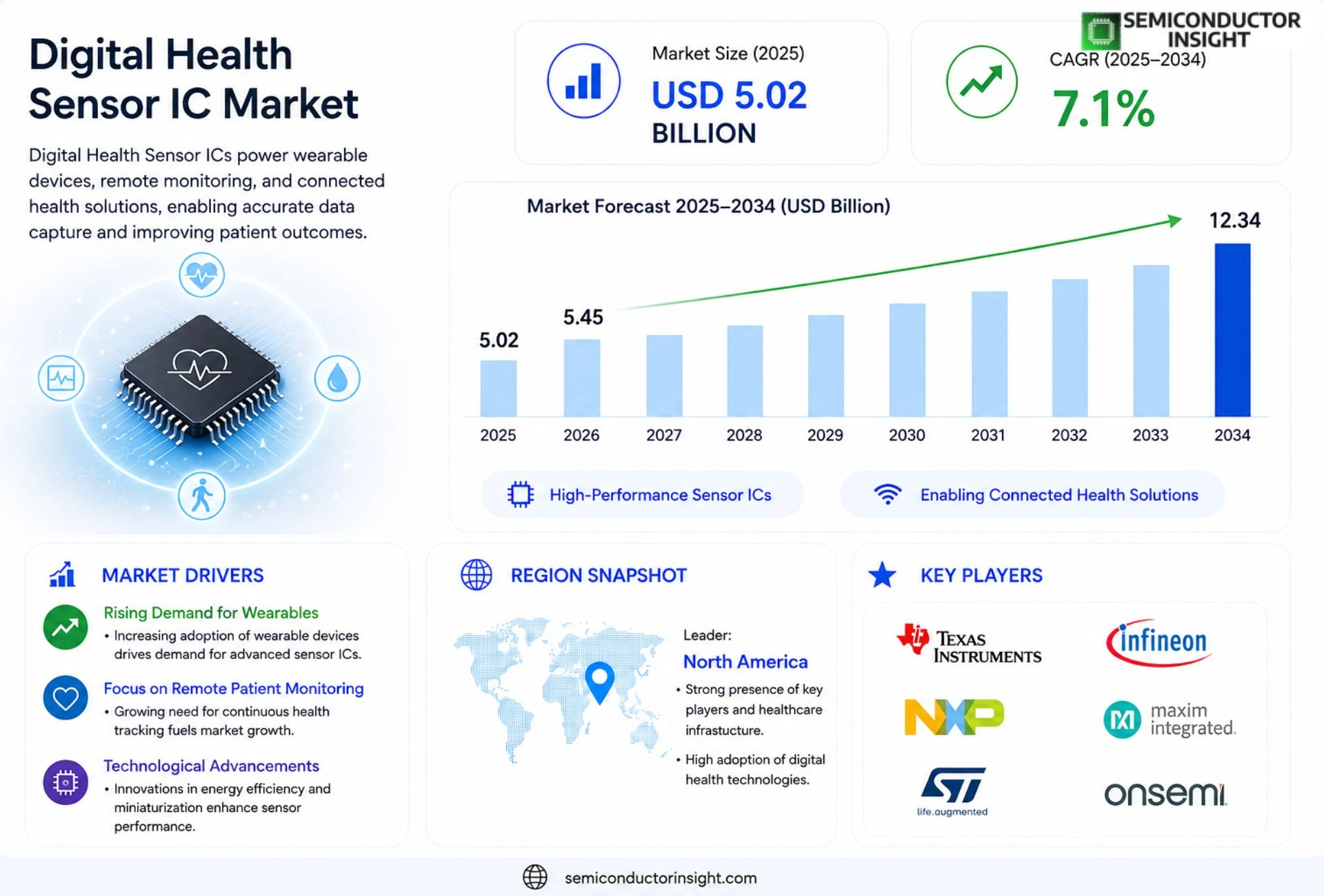

Global Digital Health Sensor IC market size was valued at USD 5.02 billion in 2025. The market is projected to grow from USD 5.45 billion in 2026 to USD 12.34 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Digital Health Sensor integrated circuits are miniature semiconductor components that convert physiological signals,such as heart rate, blood oxygen saturation, glucose levels, or motion,into precise electrical outputs for real‑time analysis in wearables, implantable devices, and tele‑health platforms. These ICs integrate analog front‑ends, analog‑to‑digital converters, power‑management blocks and wireless communication modules within a single chip footprint.

The market is experiencing rapid growth because of expanding remote patient monitoring programs, rising consumer demand for continuous wellness tracking, and supportive regulatory frameworks that accelerate device approvals. Furthermore, advances in low‑power design and AI‑enabled edge processing are driving cost reductions and battery life improvements. Key players such as Texas Instruments, Analog Devices, STMicroelectronics, and Qualcomm are launching next‑generation sensor families; for instance, in March 2024 STMicroelectronics announced a partnership with Philips to co‑develop ultra‑low‑power pulse‑oximeter sensors for hospital‑grade wearables.

MARKET DRIVERS

Rising Demand for Remote Patient Monitoring

Digital Health Sensor IC market is being propelled by a surge in remote patient monitoring solutions, especially after the pandemic accelerated telehealth adoption. Hospitals and clinics are integrating sensor ICs into wearable devices to capture real‑time vitals, reducing readmission rates by up to 15%.

Expansion of Wearable Health Ecosystems

Consumer wearables equipped with high‑precision sensor ICs now account for more than 40% of new device shipments, driving economies of scale that lower component costs by roughly 12% annually.

➤ “Integrated sensor ICs are the cornerstone of next‑generation digital health platforms, enabling continuous, low‑power monitoring.”

Regulatory frameworks such as the FDA’s guidance on interoperable medical devices are further encouraging manufacturers to adopt standards‑compliant Digital Health Sensor IC solutions, creating a predictable pathway to market.

MARKET CHALLENGES

Security and Data Privacy Concerns

Despite growth, the sector faces heightened scrutiny over data encryption and patient consent. Breaches involving sensor data can erode trust and trigger costly compliance penalties, slowing deployment in sensitive care settings.

Other Challenges

High Development Costs

Designing ultra‑low‑power sensor ICs that meet medical grade reliability often requires multi‑year R&D cycles and specialized fabrication, limiting entry for smaller players.

MARKET RESTRAINTS

Stringent Certification Timelines

Achieving CE or FDA approval for sensor ICs can extend product launch timelines by 12‑18 months, discouraging rapid iteration and imposing a financial burden on developers.

Limited availability of advanced semiconductor manufacturing capacity in regions with strong health‑tech ecosystems also constrains supply, leading to intermittent shortages during peak demand periods.

Finally, the need for cross‑compatibility with legacy medical equipment forces designers to adopt older process nodes, which hampers performance improvements.

MARKET OPPORTUNITIES

Integration with AI‑Driven Analytics

Embedding AI accelerators alongside sensor ICs creates a lucrative niche for predictive health monitoring, where early detection algorithms can reduce chronic disease costs by an estimated 20%.

Emerging Markets Adoption

Rapid urbanization and growing middle‑class populations in Asia‑Pacific and Latin America are spurring government‑backed digital health initiatives, presenting a growth runway of over $1 billion for Digital Health Sensor IC market by 2030.

Digital Health Sensor IC Market Trends

Integration of AI‑Enabled Edge Processing

Manufacturers are embedding artificial‑intelligence algorithms directly into sensor ICs to perform on‑chip data filtration and anomaly detection. This shift reduces the reliance on cloud resources, shortens latency, and prolongs battery life in wearable and implantable devices. By processing physiological signals at the edge, developers can deliver real‑time alerts for conditions such as arrhythmia or hypoxia, enhancing the clinical value of remote monitoring solutions. Security modules incorporated at the silicon level are also becoming standard, providing encrypted transmission of biometric data and protecting patient privacy. The convergence of AI with sensor fusion allows simultaneous monitoring of heart rate, SpO₂, and motion, delivering richer datasets for clinicians. Moreover, standardized firmware interfaces simplify integration across heterogeneous health platforms, reducing time‑to‑market for new wearable solutions. Interoperability standards are adopted for consistent data exchange across devices. Edge‑optimized ML models can predict deteriorations minutes before clinical onset. Robust encryption and compliance with GDPR and HIPAA guidelines are now integral to sensor firmware, ensuring secure patient data handling.

Other Trends

Low‑Power Architecture Expansion

Advances in sub‑nanowatt design and multi‑stage power‑management modules are driving the next generation of ultra‑low‑power sensor ICs. Companies such as Texas Instruments and Analog Devices have released parts that operate below the power envelope of traditional analog front‑ends, enabling continuous monitoring without frequent battery replacement. This architectural focus aligns with the growing demand for multi‑day wearables in consumer health and long‑term implant programs. The move toward heterogeneous integration enables analog front‑ends to share a common substrate with digital signal processors, further shrinking board space. Advanced packaging such as wafer‑level chip‑scale packages improves thermal dissipation and supports flexible form factors for patch‑type sensors. Energy‑harvesting techniques, including thermoelectric and kinetic converters, are being explored to supplement battery power, pushing the feasibility of years‑long autonomous operation. Designers leverage advanced 28 nm CMOS nodes to add functionality while keeping leakage minimal. Flexible substrates enable conformal skin‑attached sensors for continuous measurement of additional parameters. Dynamic power‑gating and deep‑sleep modes allow the IC to shut down non‑essential blocks, further extending operational life between charges.

Strategic Partnerships Driving Clinical Adoption

Collaboration between semiconductor firms and healthcare equipment manufacturers is accelerating regulatory clearance pathways. For example, a recent partnership between STMicroelectronics and a leading medical device maker resulted in an ultra‑low‑power pulse‑oximeter sensor specifically calibrated for hospital‑grade wearables. Such alliances streamline integration, reduce development cycles, and provide clinicians with validated sensor performance, reinforcing the overall momentum of the sector. Over‑the‑air update standards enable secure firmware refreshes, extending device lifecycles and improving diagnostics. Evolving reimbursement for remote diagnostics boosts manufacturers’ incentive to invest in next‑gen sensor ICs. AI‑driven diagnostics built on on‑chip analytics are projected to become standard care components, reinforcing long‑term growth prospects for the sector. Continued collaboration between chipset designers and healthcare providers will drive innovation cycles faster than ever.

COMPETITIVE LANDSCAPE

Key Industry Players

Digital Health Sensor IC Market: Competitive Dynamics, Strategic Alliances, and Leading Semiconductor Innovators Shaping the Future of Connected Healthcare

The global Digital Health Sensor IC market is characterized by intense competition among established semiconductor giants and specialized fabless chip designers, all vying to capture share in a landscape valued at USD 5.02 billion in 2025 and projected to reach USD 12.34 billion by 2034 at a CAGR of 7.1%. Texas Instruments, Analog Devices, and STMicroelectronics collectively anchor the market with comprehensive analog front-end portfolios and deep integration capabilities spanning heart rate monitoring, blood oxygen saturation measurement, and motion-sensing applications. STMicroelectronics, for instance, announced a strategic partnership with Philips in March 2024 to co-develop ultra-low-power pulse-oximeter sensor ICs specifically engineered for hospital-grade wearables, underscoring how leading players are pursuing collaborative innovation to accelerate time-to-market. Qualcomm continues to differentiate through its AI-enabled edge processing platforms, combining wireless communication modules with sensor fusion capabilities within highly compact system-on-chip architectures designed for next-generation remote patient monitoring and continuous wellness tracking devices. These dominant players leverage vertically integrated R&D ecosystems, substantial IP portfolios, and established supply chain relationships with global OEM wearable and medical device manufacturers to sustain their competitive positions.

Beyond the dominant tier, a robust ecosystem of specialized and niche players is actively reshaping the Digital Health Sensor IC competitive landscape by targeting specific physiological measurement verticals and low-power design niches. Maxim Integrated, now part of Analog Devices, has long been recognized for its biopotential and optical sensor IC families widely deployed in consumer fitness wearables and clinical-grade devices. Silicon Laboratories and Nordic Semiconductor have carved out significant positions by offering ultra-low-power wireless sensor SoCs optimized for Bluetooth Low Energy-enabled health monitoring applications. NXP Semiconductors competes through its secure, multi-protocol connectivity ICs tailored for implantable and remote monitoring platforms, while Renesas Electronics addresses the industrial medical segment with precision mixed-signal sensor ICs. Emerging players including Rockley Photonics and ams OSRAM are advancing photonic-based sensor IC technologies capable of non-invasive continuous glucose and biomarker monitoring, representing the next frontier of differentiation in this rapidly evolving market. The competitive intensity is further amplified by strategic mergers, cross-industry partnerships, and sustained R&D investments directed at achieving lower power consumption, higher measurement accuracy, and seamless AI-driven edge analytics integration within ever-smaller chip footprints.

List of Key Digital Health Sensor IC Companies Profiled

- Texas Instruments Incorporated

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Qualcomm Technologies, Inc.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- ams OSRAM AG

- Rockley Photonics Holdings Limited

- Infineon Technologies AG

- Microchip Technology Incorporated

- ROHM Semiconductor

- Murata Manufacturing Co., Ltd.

- Robert Bosch Sensortec GmbH

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Analog Front‑End Sensors

|

| By Application |

|

Wearable Fitness Trackers

|

| By End User |

|

Patients

|

| By Power Consumption |

|

Ultra Low‑Power

|

| By Integration Level |

|

Fully Integrated SoCs

|

Regional Analysis: North America

United States

The increasing popularity of wearable devices, such as smartwatches and fitness trackers, is a significant driver for Digital Health Sensor ICs. These devices leverage sensors to track various physiological parameters, including heart rate, blood oxygen levels, and sleep patterns, providing valuable insights into individual health.

Remote patient monitoring (RPM) is gaining traction as healthcare providers seek to improve patient outcomes and reduce hospital readmissions. Digital Health Sensor ICs play a crucial role in enabling RPM by collecting and transmitting patient data wirelessly, allowing for continuous monitoring and timely interventions.

Implantable sensors are revolutionizing the treatment of various medical conditions. These devices can continuously monitor vital signs, deliver medication, or provide therapeutic interventions directly within the body. The demand for smaller, more biocompatible, and longer-lasting implantable sensors is driving innovation in Digital Health Sensor ICs.

Digital Health Sensor ICs are integral components of advanced diagnostic devices used in hospitals and clinics. These devices enable faster, more accurate, and less invasive diagnostic procedures, leading to improved patient care and outcomes.

Europe

Europe presents a significant market for Digital Health Sensor IC market, characterized by a strong emphasis on healthcare innovation and a growing adoption of digital health technologies. Several countries, including Germany, the UK, and France, are leading the way in investing in digital health initiatives, creating favorable market conditions for sensor ICs. The regulatory environment in Europe, particularly the GDPR, presents both challenges and opportunities for companies operating in the region. Focus is on patient data privacy and security, pushing for robust security features within sensor IC designs. The strong presence of established medical device manufacturers and research institutions, alongside government support for digital health, contributes to the sustained growth of the market.

Asia-Pacific

Asia-Pacific is poised for rapid growth Digital Health Sensor IC market, driven by a large and aging population, increasing healthcare expenditure, and growing awareness of digital health solutions. Countries like China and Japan are emerging as key markets, with significant investments in healthcare infrastructure and digital health initiatives. The region’s affordability and large patient base provide a substantial opportunity for manufacturers of low-cost Digital Health Sensor ICs. However, navigating complex regulatory landscapes and ensuring data privacy are critical challenges for companies entering the Asian-Pacific market. The increasing adoption of mobile health (mHealth) applications further supports the demand for compact and power-efficient sensor ICs.

South America

South America represents a developing market for Digital Health Sensor ICs, with growing interest in improving healthcare access and efficiency. Increasing government initiatives to modernize healthcare systems and a rising middle class with greater disposable income are driving demand for digital health solutions. The market is currently characterized by a focus on basic monitoring devices and remote patient monitoring in underserved areas. Challenges include limited healthcare infrastructure and regulatory complexities across different countries in the region. However, the potential for growth in key markets like Brazil and Argentina remains significant.

Middle East & Africa

The Middle East & Africa region is an emerging market for Digital Health Sensor IC market, with growing investments in healthcare infrastructure and a rising demand for digital health solutions. Increasing prevalence of chronic diseases, such as diabetes and cardiovascular disease, is driving the need for remote patient monitoring and diagnostic tools. Countries like Saudi Arabia and the UAE are leading the way in adopting digital health technologies, creating opportunities for sensor IC manufacturers. Challenges include infrastructure limitations and regulatory inconsistencies across different countries. The region presents a long-term growth opportunity, particularly with increasing government focus on improving healthcare outcomes.

Report Scope

This market research report provides a comprehensive analysis of the Digital Health Sensor IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Digital Health Sensor IC Market?

-> Digital Health Sensor IC market size was valued at USD 5.02 billion in 2025. The market is projected to grow from USD 5.45 billion in 2026 to USD 12.34 billion by 2034, exhibiting a CAGR of 7.1%.

Which key companies operate Digital Health Sensor IC market?

-> Key players include Texas Instruments, Analog Devices, STMicroelectronics, Qualcomm, among others.

What are the key growth drivers?

-> Key growth drivers include expanding remote patient monitoring programs, rising consumer demand for continuous wellness tracking, supportive regulatory frameworks, advances in low‑power design, and AI‑enabled edge processing.

Which region dominates the market?

-> The reference does not specify a dominant region; market growth is observed across multiple regions globally.

What are the emerging trends?

-> Emerging trends include ultra‑low‑power sensor designs, AI/IoT integration at the edge, and enhanced wireless communication modules for wearable and implantable health devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...