MARKET INSIGHTS

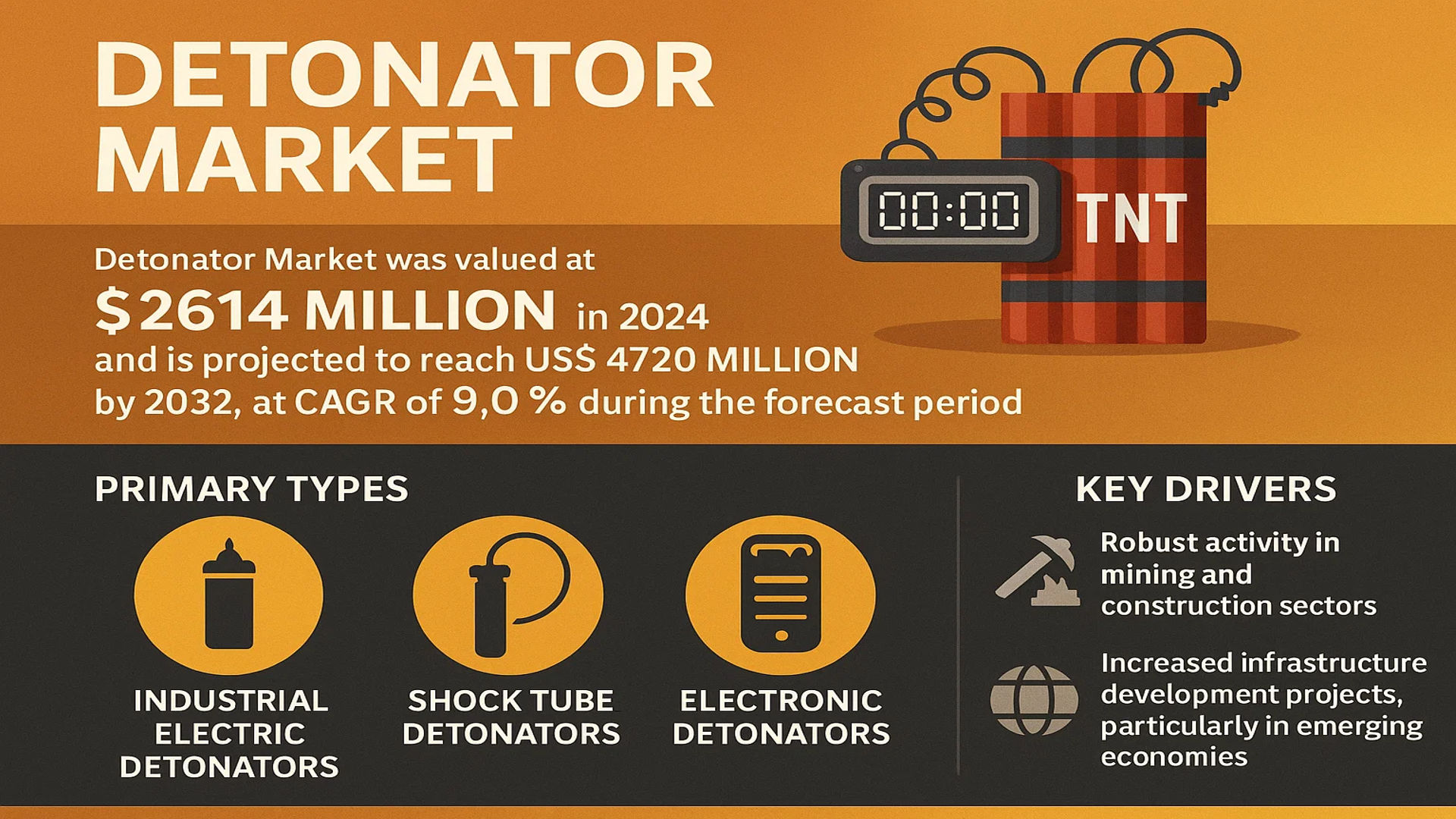

The global Detonator Market was valued at 2614 million in 2024 and is projected to reach US$ 4720 million by 2032, at a CAGR of 9.0% during the forecast period.

A detonator, frequently called a blasting cap, is a small sensitive device used to initiate a larger, more powerful but relatively insensitive secondary explosive. These components are critical for controlled demolition, mining operations, and large-scale excavation projects. The primary types include Industrial Electric Detonators, Shock Tube Detonators, and the increasingly adopted Electronic Detonators, each offering varying levels of precision and safety.

Market expansion is primarily driven by robust activity in the global mining and construction sectors, coupled with increased infrastructure development projects, particularly in emerging economies. However, the market also faces challenges due to stringent regulatory frameworks governing the storage, transportation, and use of explosives. Shock Tube Detonators currently dominate the product landscape, holding over 50% market share, owing to their enhanced safety features and reliability compared to traditional electric detonators. Geographically, EMEA (Europe, Middle East, and Africa) is the largest market, accounting for over 40% of global revenue, followed closely by the combined markets of the USA and China.

MARKET DYNAMICS

MARKET DRIVERS

Global Infrastructure Development and Mining Activities to Drive Market Expansion

The global detonator market is experiencing robust growth driven by increasing infrastructure development projects and expanding mining activities worldwide. Large-scale construction projects, including highways, railways, hydropower plants, and urban development initiatives, require controlled blasting operations for excavation and demolition purposes. The mining sector, particularly coal and metal mining, remains a primary consumer of detonators, with growing demand for minerals and metals fueling production increases. Emerging economies are investing significantly in infrastructure, with construction spending projected to reach unprecedented levels, thereby creating sustained demand for blasting equipment and explosives. The shift toward more efficient and safer blasting technologies further accelerates market adoption, as industries seek to improve operational efficiency while maintaining safety standards.

Technological Advancements in Electronic Detonators to Boost Market Growth

Technological innovation represents a significant driver for the detonator market, particularly with the development and adoption of electronic detonators. These advanced systems offer precise timing control, enhanced safety features, and reduced environmental impact compared to traditional detonators. The mining and construction industries are increasingly adopting electronic detonators to achieve better fragmentation, reduce vibration, and improve overall blasting efficiency. Major manufacturers are investing in research and development to create more sophisticated electronic detonation systems with improved connectivity and data logging capabilities. The superior performance characteristics of electronic detonators, including millisecond-level precision and reduced oversize rock formation, make them particularly valuable in large-scale mining operations where efficiency directly impacts profitability.

Stringent Safety Regulations and Environmental Concerns to Accelerate Market Adoption

Increasing regulatory focus on workplace safety and environmental protection is driving the adoption of advanced detonator technologies. Governments worldwide are implementing stricter safety standards for blasting operations, particularly in mining and construction sectors where accidents can have severe consequences. Modern detonator systems, especially electronic variants, offer enhanced safety features including better resistance to stray currents, improved reliability, and reduced risk of accidental detonation. Environmental considerations are also pushing industries toward more precise blasting technologies that minimize vibration, noise, and dust emissions. The growing emphasis on sustainable mining practices and reduced environmental footprint is encouraging operators to invest in advanced detonation systems that offer better control and reduced ecological impact.

MARKET RESTRAINTS

High Initial Investment Costs to Limit Market Penetration

The detonator market faces significant restraint due to the high initial investment required for advanced electronic detonation systems. While electronic detonators offer superior performance and safety benefits, their cost can be substantially higher than traditional shock tube or electric detonators. This cost differential creates adoption barriers, particularly in price-sensitive markets and among smaller mining operations with limited capital budgets. The comprehensive system requirements, including specialized blasting machines, programming equipment, and trained personnel, add to the overall investment burden. In developing regions where cost considerations often outweigh performance benefits, the premium pricing of advanced detonators can significantly slow market penetration and adoption rates.

Stringent Regulatory Compliance and Licensing Requirements to Hinder Market Growth

The detonator market operates under extensive regulatory frameworks that govern the manufacturing, transportation, storage, and usage of explosive materials. Compliance with these regulations requires significant administrative effort, specialized infrastructure, and continuous monitoring, creating substantial operational burdens for market participants. The licensing process for explosive materials is often complex and time-consuming, involving multiple government agencies and thorough background checks. These regulatory requirements vary across jurisdictions, creating challenges for multinational companies operating in multiple markets. The increasing complexity of regulatory frameworks, particularly regarding environmental protection and workplace safety, adds compliance costs and administrative overhead that can deter market entry and expansion.

Volatility in Raw Material Prices and Supply Chain Disruptions to Impact Market Stability

Market stability is affected by fluctuations in raw material prices and potential supply chain disruptions. The manufacturing of detonators requires specialized chemicals and materials whose prices can be volatile due to geopolitical factors, trade restrictions, and supply-demand imbalances. Recent global events have demonstrated how supply chain disruptions can affect the availability of critical components, leading to production delays and increased costs. The specialized nature of explosive materials means that alternative sourcing options are often limited, making the market vulnerable to supply chain interruptions. This volatility in input costs and supply availability creates uncertainty in pricing and delivery schedules, potentially affecting project timelines and operational planning for end-users.

MARKET CHALLENGES

Safety Concerns and Accident Risks to Challenge Market Development

The detonator market faces ongoing challenges related to safety concerns and the potential for accidents during handling, storage, and deployment. Despite technological advancements, the inherent nature of explosive materials means that improper handling can lead to serious incidents. The industry must continuously address safety protocols, employee training, and equipment maintenance to minimize risks. Recent incidents in various mining and construction operations highlight the persistent safety challenges, even with improved technologies. These safety concerns affect insurance costs, regulatory scrutiny, and public perception, creating additional operational challenges for market participants. The need for comprehensive safety systems and continuous training represents both a technical and financial challenge for companies operating in this sector.

Other Challenges

Technological Integration Complexities

Integrating advanced detonation systems with existing mining and construction operations presents significant technical challenges. The transition from traditional to electronic detonators requires substantial changes in operational procedures, staff training, and equipment compatibility. Many operations face difficulties in adapting their existing processes to accommodate new technologies, particularly in remote locations with limited technical support availability.

Skilled Workforce Shortage

The industry faces a growing shortage of qualified blasting professionals and technicians capable of operating advanced detonation systems. The specialized knowledge required for modern blasting operations is becoming increasingly scarce, particularly as experienced professionals retire and fewer new entrants join the field. This skills gap creates operational challenges and increases the risk of improper system usage.

MARKET OPPORTUNITIES

Growing Adoption of Automation and Digitalization to Create New Market Opportunities

The integration of automation and digital technologies presents significant growth opportunities for the detonator market. The development of smart blasting systems that incorporate IoT connectivity, real-time monitoring, and data analytics is transforming traditional blasting operations. These advanced systems enable remote operation, precise timing control, and comprehensive data collection for performance optimization. The mining industry’s increasing focus on digital transformation and operational efficiency is driving demand for connected detonation systems that can integrate with broader mine management platforms. The ability to collect and analyze blasting data provides valuable insights for improving fragmentation, reducing costs, and enhancing safety, creating new value propositions for advanced detonator systems.

Expansion in Emerging Markets to Provide Substantial Growth Potential

Emerging economies present substantial growth opportunities for the detonator market, driven by rapid infrastructure development and increasing mining activities. Countries across Asia, Africa, and South America are investing heavily in transportation infrastructure, energy projects, and urban development, all requiring extensive blasting operations. The mining sector in these regions is also expanding to meet global demand for minerals and metals, creating additional demand for blasting equipment. The relatively lower penetration of advanced detonation technologies in these markets provides significant upside potential for manufacturers offering modern, efficient systems. As these economies develop their regulatory frameworks and safety standards, the adoption of advanced detonation technologies is expected to accelerate.

Development of Environmentally Friendly Blasting Solutions to Open New Market Segments

Increasing environmental awareness and regulatory pressure are creating opportunities for developing more environmentally friendly blasting solutions. The market is seeing growing demand for detonation systems that reduce vibration, noise, dust, and other environmental impacts. Manufacturers are investing in technologies that minimize the ecological footprint of blasting operations while maintaining or improving performance characteristics. The development of low-vibration detonators, reduced-emission explosives, and precision blasting systems addresses growing environmental concerns while meeting operational requirements. This focus on environmental performance is opening new market segments and creating competitive advantages for companies that can deliver sustainable blasting solutions without compromising on efficiency or safety.

DETONATOR MARKET TRENDS

Advancements in Electronic Detonator Technology to Emerge as a Dominant Trend

The global detonator market is experiencing a significant technological shift from traditional pyrotechnic and shock tube systems toward advanced electronic detonators. These sophisticated devices offer unparalleled precision in timing and sequencing, which is critical for optimizing fragmentation, reducing vibration, and improving overall safety in mining and construction operations. The adoption rate for electronic detonators is growing at an estimated annual rate of over 12%, driven by their ability to provide millisecond-level accuracy, which can lead to a reduction in oversize material by up to 25% and a decrease in overall explosive consumption by approximately 15%. This transition is not merely about replacing old equipment; it represents a fundamental change in blasting philosophy, enabling complex blast designs that were previously impossible. Furthermore, the integration of wireless communication and remote initiation capabilities is enhancing operational safety by allowing personnel to be at a greater distance from the blast site, a crucial factor in reducing mining accidents.

Other Trends

Stringent Safety and Environmental Regulations

Globally, the enforcement of stricter safety protocols and environmental regulations is profoundly shaping the detonator market. Regulatory bodies are increasingly mandating the use of safer, more reliable initiation systems to mitigate the risks associated with misfires and accidental detonations. In regions like the EMEA and North America, regulations often require higher standards for product traceability and performance, which inherently favors the adoption of advanced electronic detonators over their less traceable non-electric counterparts. This regulatory pressure is a powerful market driver, compelling mining companies and contractors to invest in newer technologies to ensure compliance, avoid hefty fines, and protect their workforce. The focus on reducing environmental impact, such as controlling ground vibration and air overpressure, further accelerates this trend, as electronic systems provide the necessary control to meet these stringent limits effectively.

Infrastructure Development and Mining Sector Expansion

Sustained global investment in infrastructure development and the expansion of mining activities are primary drivers of demand for detonators. Major infrastructure projects, including the construction of highways, tunnels, and hydroelectric power plants, require extensive excavation and rock blasting. For instance, the global construction industry is projected to grow at a rate of 3.5% annually, directly correlating to increased consumption of explosives and initiation systems. Simultaneously, the mining sector, particularly for metals like copper and lithium essential for the energy transition, is experiencing robust growth. Metal mining operations accounted for over 30% of the detonator market volume in the recent past. This dual demand from construction and resource extraction creates a stable, long-term growth trajectory for the market, with emerging economies in Asia and South America representing particularly high-growth regions due to their ongoing industrialization and urban development initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global detonator market exhibits a semi-consolidated competitive structure, characterized by the presence of several multinational corporations, regional powerhouses, and specialized niche players. This landscape is driven by stringent safety regulations, technological innovation, and the critical need for reliable blasting solutions in mining and infrastructure development. The market’s top five manufacturers collectively command a significant share, exceeding 30% of global revenues, indicating a concentration of power among established leaders.

Orica Limited stands as a preeminent force in the market, leveraging its extensive global footprint and comprehensive portfolio of blasting solutions, including advanced electronic detonators. The company’s dominance is further solidified by its strong presence in the Asia-Pacific and EMEA regions, which together constitute the largest market share. Similarly, Dyno Nobel (a division of Incitec Pivot Limited) maintains a formidable position, particularly in North America, due to its continuous investment in R&D and strategic supply contracts with major mining conglomerates.

Chinese manufacturers have emerged as pivotal players, capitalizing on the vast domestic mining sector. Yunnan Civil Explosive and China National Instruments Import & Export Corporation (CNIGC) hold substantial market shares, supported by government initiatives in infrastructure and domestic resource extraction. Their growth is largely attributed to cost-competitive offerings and deep entrenchment in local supply chains. Meanwhile, MAXAM continues to strengthen its market presence, especially in Europe and South America, through technological advancements in its Shock Tube and Electronic Detonator lines, which align with the industry’s shift towards safer and more precise blasting methods.

Additionally, these leading companies are actively pursuing growth through strategic initiatives. Geographic expansion into emerging markets, particularly in Africa and Southeast Asia, is a common tactic. Furthermore, new product launches focusing on enhanced safety features, digital connectivity, and environmental sustainability are expected to be key differentiators. For instance, the development of wireless electronic initiation systems represents a significant innovation frontier. Companies like ENAEX and Sasol are also strengthening their positions through significant investments in automation and strategic partnerships with mining operators, ensuring their products are integrated into larger, more efficient operational ecosystems.

List of Key Detonator Companies Profiled

- Orica Limited (Australia)

- Dyno Nobel/IPL (USA)

- Yunnan Civil Explosive (China)

- China National Instruments Import & Export Corporation (CNIGC) (China)

- MAXAM (Spain)

- Huhua (China)

- Nanling Civil Explosive (China)

- Poly Permanent Union Holding (China)

- Sichuan Yahua Industrial Group (China)

- Sasol (South Africa)

- AEL Mining Services (South Africa)

- ENAEX (Chile)

- EPC Groupe (France)

- BME Mining (South Africa)

- NOF Corporation (Japan)

Segment Analysis:

By Type

Shock Tube Detonators Segment Dominates the Market Due to Superior Safety and Reliability in Harsh Environments

The market is segmented based on type into:

- Industrial Electric Detonators

- Subtypes: Instantaneous, short delay, and long delay

- Shock Tube Detonators

- Subtypes: Non-electric initiation systems and surface connectors

- Electronic Detonators

- Subtypes: Programmable and wireless initiation systems

By Application

Coal Mines Segment Leads Due to Extensive Global Mining Operations and High Explosive Consumption

The market is segmented based on application into:

- Coal Mines

- Metal Mines

- Non-metal Mines

- Railway or Road Construction

- Hydraulic & Hydropower Projects

- Quarrying and Construction

- Others

By End User

Mining Industry Represents the Largest End-user Segment Driven by Continuous Resource Extraction Needs

The market is segmented based on end user into:

- Mining Companies

- Subtypes: Surface mining and underground mining operations

- Construction Firms

- Demolition Contractors

- Government Infrastructure Projects

- Others

By Initiation System

Non-electric Initiation Systems Gain Traction Owing to Enhanced Safety Features and Reduced Stray Current Risks

The market is segmented based on initiation system into:

- Electric Initiation Systems

- Non-electric Initiation Systems

- Subtypes: Shock tube, detonating cord, and gas tube systems

- Electronic Initiation Systems

- Others

Regional Analysis: Detonator Market

EMEA (Europe, Middle East & Africa)

The EMEA region is the largest market for detonators globally, holding a share exceeding 40%. This dominance is driven by a combination of established mining industries, major infrastructure projects, and significant military expenditure. In Europe, stringent safety regulations and a strong focus on technological innovation, particularly in electronic detonators for precision blasting, are key market drivers. The EU’s commitment to raw material sovereignty, as outlined in its Critical Raw Materials Act, is expected to bolster mining activities, further supporting demand. The Middle East, particularly nations like Saudi Arabia and the UAE, is experiencing robust growth fueled by massive giga-projects like NEOM and ongoing urban development, which require extensive excavation and quarrying. Africa presents a mixed landscape; while South Africa has a mature mining sector, other regions show potential for growth, though this is often tempered by political instability and infrastructural challenges.

Asia-Pacific

The Asia-Pacific region is a powerhouse of volume consumption, largely propelled by China and India. China alone accounts for a significant portion of the global market share. The region’s growth is inextricably linked to its massive-scale infrastructure development, extensive coal mining operations, and rapid urbanization. While cost sensitivity keeps demand for conventional shock tube detonators high, there is a palpable and growing shift toward more advanced electronic systems. This transition is being driven by increasing government emphasis on mining safety standards and operational efficiency. The sheer scale of ongoing and planned construction and mining projects across Southeast Asia and India ensures that this region remains a critical and high-growth market for detonator manufacturers.

North America

Characterized by highly regulated and technologically advanced mining and construction sectors, North America is a significant market with a strong preference for high-performance, safe blasting solutions. The United States represents the bulk of regional demand. The market is driven by strict safety protocols enforced by agencies like MSHA (Mine Safety and Health Administration) and a steady flow of infrastructure renewal projects, including road construction and quarrying. There is a pronounced trend towards the adoption of electronic detonators, which offer superior precision and control, reducing environmental vibration and enhancing overall safety. Furthermore, the region’s shale oil and gas industry contributes to consistent demand for explosives and associated initiation systems.

South America

South America’s market is heavily influenced by its rich mineral wealth, particularly in countries like Chile, Peru, and Brazil, which are global leaders in copper, lithium, and iron ore production. The mining industry is the primary consumer of detonators here, demanding reliable products for large-scale open-pit and underground operations. However, the market’s growth trajectory can be volatile, often mirroring fluctuations in global commodity prices. Economic and political instability in certain countries can also impact investment in new mining projects, thereby affecting detonator sales. While there is interest in modern electronic systems, the widespread adoption is sometimes hindered by higher costs and a more traditional operational approach in some segments of the industry.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Detonator markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Detonator Market?

-> The global Detonator Market was valued at 2614 million in 2024 and is projected to reach US$ 4720 million by 2032, at a CAGR of 9.0% during the forecast period.

Which key companies operate in Global Detonator Market?

-> Key players include Yunnan Civil Explosive, Orica, CNIGC, Dyno Nobel/IPL, and MAXAM, among others.

What are the key growth drivers?

-> Key growth drivers include increased mining activities, infrastructure development projects, and demand for advanced electronic detonators.

Which region dominates the market?

-> EMEA is the largest market with over 40% share, followed by USA and China.

What are the emerging trends?

-> Emerging trends include adoption of electronic detonators, enhanced safety features, and sustainable blasting solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...