MARKET INSIGHTS

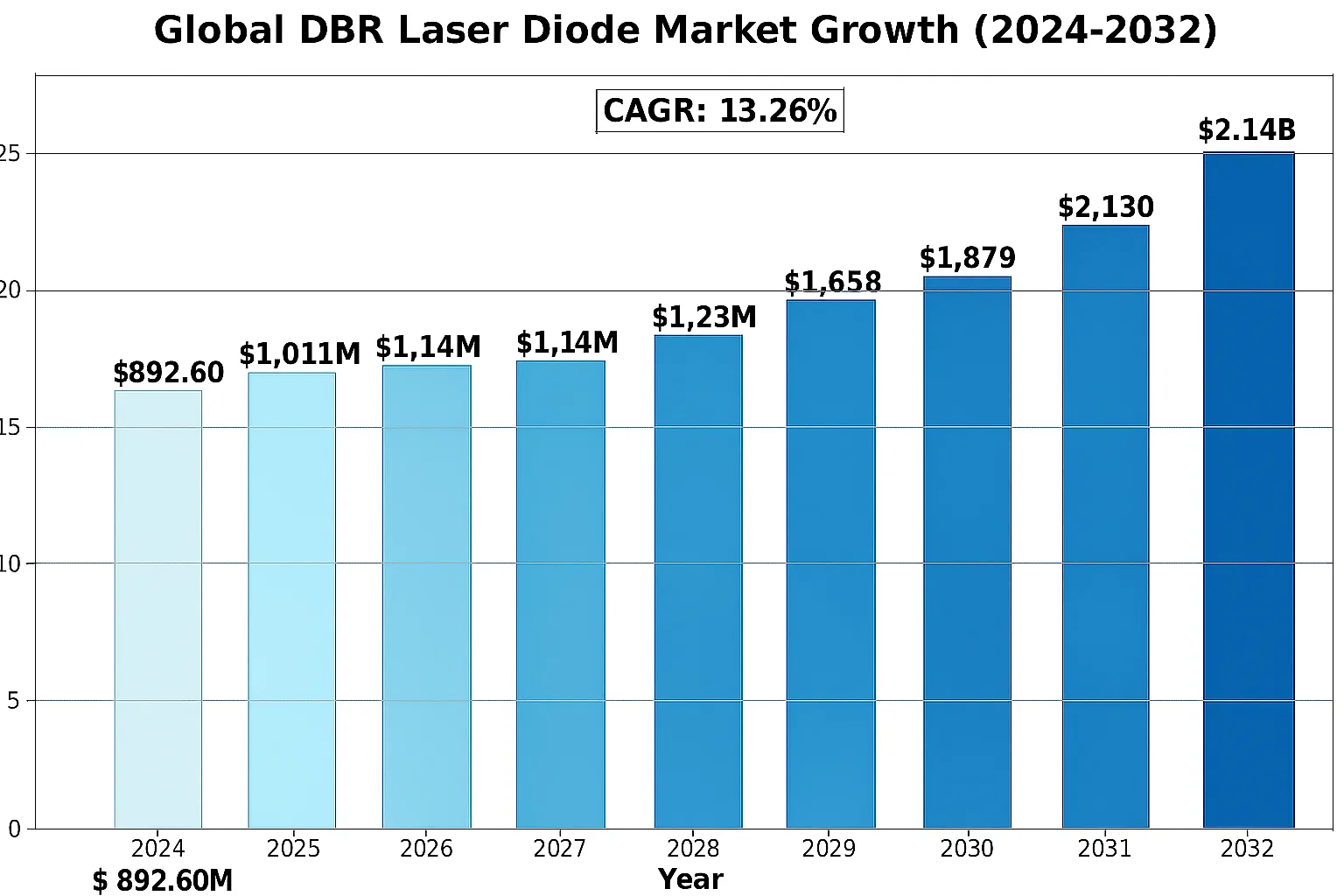

The global DBR Laser Diode Market size was valued at US$ 892.60 million in 2024 and is projected to reach US$ 2.14 billion by 2032, at a CAGR of 13.26% during the forecast period 2025–2032. The U.S. accounts for 35% of the market share, while China is emerging as the fastest-growing region with an estimated 9.2% CAGR through 2032.

DBR (Distributed Bragg Reflector) laser diodes are advanced semiconductor devices that integrate optical gratings for wavelength stabilization. These components combine single-epitaxial growth structures with precision-fabricated gain ridges to deliver superior performance in narrow-linewidth applications. The technology enables precise wavelength control, making it critical for telecommunications, spectroscopy, and optical sensing applications.

The market growth is driven by increasing 5G infrastructure deployments, which require high-performance optical components for base stations. Data center expansion and demand for fiber optic repeaters further contribute to adoption. Recent technological advancements have improved tuning ranges, with the below 10GHz segment projected to grow at 7.4% CAGR. Key players like Photodigm and Thorlabs continue to innovate, with Photodigm’s latest DBR lasers achieving <1 MHz linewidth for quantum technology applications.

MARKET DRIVERS

Accelerated 5G Deployment Fueling Demand for High-Performance Laser Diodes

The global rollout of 5G networks is creating unprecedented demand for DBR laser diodes, which serve as critical components in optical communication systems. With 5G base stations requiring significantly higher bandwidth and lower latency compared to 4G infrastructure, the need for precise wavelength-stabilized lasers has surged. Recent industry benchmarks indicate that the market for optical components in 5G infrastructure will grow at over 25% CAGR through 2030, with DBR lasers capturing a substantial share due to their superior performance in dense wavelength division multiplexing (DWDM) applications. Furthermore, the exponential growth in mobile data traffic, projected to exceed 700 exabytes monthly by 2025, is necessitating network upgrades that depend heavily on these advanced laser solutions.

Data Center Expansion Driving Adoption of High-Speed Optical Interconnects

Modern hyperscale data centers are increasingly adopting DBR laser diodes to address bandwidth demands in server-to-server communication. As cloud computing and AI workloads intensify, data center operators are migrating from traditional electrical interconnects to optical solutions that offer higher throughput and lower power consumption. Industry analysis reveals that the optical transceiver market for data centers surpassed $10 billion in 2024, with tunable DBR lasers becoming the preferred choice for 400G and emerging 800G Ethernet standards. Leading technology firms have begun integrating these lasers into their next-generation switching architectures, citing their superior thermal stability and narrow linewidth characteristics that enable longer transmission distances.

Medical Laser Applications Creating New Growth Verticals

The healthcare sector is embracing DBR laser technology for advanced diagnostic and therapeutic applications, particularly in minimally invasive surgical procedures and biomedical sensing. With the global medical lasers market projected to reach $8 billion by 2027, manufacturers are developing specialized DBR variants optimized for precise tissue ablation and optical coherence tomography. Recent regulatory approvals for laser-based surgical devices incorporating wavelength-stabilized diodes have opened new revenue streams, particularly in ophthalmology and dermatology. The ability to maintain consistent output at specific wavelengths makes DBR lasers indispensable for procedures requiring exact dosimetry and minimal thermal damage to surrounding tissues.

MARKET RESTRAINTS

High Production Costs Limit Market Penetration in Price-Sensitive Segments

The sophisticated fabrication processes required for DBR laser diodes result in significantly higher production costs compared to conventional laser solutions. Epitaxial growth techniques and grating formation processes demand specialized equipment and cleanroom facilities that contribute to manufacturing expenses nearly 40-50% higher than DFB lasers. These cost barriers make DBR technology economically viable only for high-performance applications, restricting adoption in consumer electronics and automotive sectors where price sensitivity is paramount. While recent advances in manufacturing efficiency have reduced some costs, the price premium remains a persistent challenge for broader market expansion.

Complex Packaging Requirements Challenge Mass Production

DBR lasers require hermetic packaging with precise thermal management to maintain wavelength stability, adding substantial complexity to the manufacturing workflow. Industry benchmarks indicate that packaging accounts for approximately 30-35% of total device cost, with yield rates in final assembly stages often below 60% for high-performance variants. The need for specialized materials like thermoelectric coolers and custom optical isolators further compounds these challenges, creating bottlenecks in production scaling. Manufacturers are investing heavily in automated assembly solutions, but the tight tolerances required for DBR operation continue to limit production throughput compared to simpler laser architectures.

Regulatory Hurdles in Medical and Defense Applications

Stringent certification requirements in healthcare and military sectors create lengthy approval cycles for DBR laser products, delaying time-to-market. Medical device approvals typically require 12-18 months of clinical validation, while defense applications often entail rigorous environmental testing and compliance with military specifications. These regulatory barriers disproportionately affect smaller manufacturers lacking the resources to navigate complex certification processes. Furthermore, export controls on high-power laser components in certain jurisdictions create additional trade compliance challenges that can restrict market access for global suppliers.

MARKET OPPORTUNITIES

Emerging LiDAR Applications in Autonomous Vehicles Present Growth Potential

The rapid advancement of autonomous vehicle technology is creating significant opportunities for DBR laser diode manufacturers. As automotive LiDAR systems evolve toward higher resolution and longer detection ranges, the demand for wavelength-stable, single-mode lasers is increasing dramatically. Industry forecasts predict the automotive LiDAR market will exceed $5 billion annually by 2030, with frequency-modulated continuous wave (FMCW) systems adopting DBR lasers for their coherence length advantages. Several leading automakers have already incorporated these lasers into prototype perception systems, demonstrating superior performance in challenging weather conditions compared to conventional pulsed LiDAR solutions.

Quantum Technology Development Opens New Research Applications

Government and academic investments in quantum computing infrastructure are driving demand for ultra-stable laser sources with precise wavelength control. DBR lasers have emerged as critical components in quantum optics experiments, particularly for trapping and cooling atoms in quantum simulators. National research initiatives across major economies have allocated over $3 billion collectively to quantum technology development, with a substantial portion earmarked for enabling photonic components. As these technologies transition from laboratory research to commercial applications, the requirement for robust, field-deployable DBR laser systems is expected to grow significantly in the coming decade.

Integration with Silicon Photonics Enables Next-Generation Optical Networks

The convergence of DBR technology with silicon photonics platforms presents compelling opportunities for high-volume optical transceiver production. Recent breakthroughs in hybrid integration techniques have demonstrated the viability of combining III-V DBR lasers with silicon waveguides, potentially reducing packaging costs by up to 60% compared to discrete solutions. Major cloud providers are actively evaluating these co-packaged optical solutions for next-generation data center interconnects, seeking to overcome bandwidth limitations in traditional electrical interconnects. This technological synergy could dramatically expand the addressable market for DBR lasers by enabling cost-effective deployment in high-density computing environments.

MARKET CHALLENGES

Supply Chain Disruptions Impact Critical Material Availability

The DBR laser industry faces ongoing supply chain vulnerabilities for specialized semiconductor materials and substrates. Gallium arsenide (GaAs) wafers, essential for high-performance DBR fabrication, have experienced severe price fluctuations due to geopolitical factors and production capacity constraints. Industry reports indicate spot prices for 6-inch GaAs substrates have increased by over 35% in recent years, squeezing manufacturer margins. Furthermore, the highly concentrated nature of the supply base creates single-point-of-failure risks, with over 70% of global indium phosphide (InP) production controlled by a handful of suppliers. These material constraints pose significant challenges for production scale-up efforts during periods of surging demand.

Intense Competition from Alternative Laser Technologies

Established DFB laser manufacturers and emerging MEMS-tunable laser providers are aggressively competing with DBR solutions across multiple application segments. While DBR lasers offer superior wavelength stability, their higher costs make them vulnerable to displacement in price-sensitive markets. Industry analysis suggests that DFB lasers currently maintain over 65% market share in optical communications, benefiting from more mature manufacturing ecosystems. Additionally, novel external cavity laser designs utilizing silicon photonics integration are beginning to challenge traditional DBR implementations in certain high-performance applications. Manufacturers must continue innovating to maintain competitive differentiation as alternative technologies evolve.

Technology Obsolescence Risks in Fast-Evolving Optical Standards

The rapid evolution of optical communication protocols creates constant pressure on DBR laser developers to keep pace with changing technical requirements. Emerging coherent detection schemes and advanced modulation formats demand increasingly stringent laser specifications, potentially rendering existing product designs obsolete. For instance, the transition from 400G to 800G Ethernet standards requires lasers with narrower linewidths and improved thermal stability, necessitating costly redesigns of existing DBR platforms. This technological churn forces manufacturers to maintain substantial R&D investments just to retain market position, while also confronting the risk of inventory write-offs when product cycles accelerate faster than anticipated.

DBR LASER DIODE MARKET TRENDS

Growing Demand for High-Speed Fiber Optic Communication to Drive Market Growth

The increasing adoption of 5G technology and data center expansion is significantly boosting the demand for DBR (Distributed Bragg Reflector) laser diodes. These components are critical for high-bandwidth optical communication systems, offering superior wavelength stability and narrow linewidth compared to conventional laser diodes. The global push toward ultra-fast internet infrastructure has resulted in DBR lasers becoming indispensable in applications such as optical transceivers, coherent communication, and fiber optic sensing. With telecom operators aggressively deploying next-gen networks, the market is projected to witness steady growth, particularly in regions investing heavily in digital infrastructure.

Other Trends

Advancements in Tunable Laser Technology

The development of wavelength-tunable DBR lasers has opened new avenues in optical networking and sensing applications. Recent innovations allow tuning ranges exceeding 40GHz, which is crucial for dense wavelength division multiplexing (DWDM) systems. This capability ensures higher data transmission capacities while reducing the need for multiple fixed-wavelength lasers. Manufacturers are also integrating these devices with advanced modulation techniques, further improving spectral efficiency. The shift toward software-defined networking (SDN) in data centers is creating additional demand for tunable laser solutions, as they offer flexibility in configuring optical links dynamically.

Expanding Applications in Biomedical & Sensing Technologies

Beyond telecommunications, DBR laser diodes are gaining traction in biomedical imaging and industrial sensing. Their precise wavelength control makes them ideal for spectroscopy, flow cytometry, and optical coherence tomography (OCT). The healthcare sector’s growing reliance on non-invasive diagnostic tools is accelerating this adoption, particularly with handheld medical devices requiring compact, high-performance light sources. Industrial applications such as LIDAR and gas sensing also benefit from the robustness and stability of DBR lasers, especially in harsh environments where conventional lasers may underperform. This diversification into non-telecom sectors is creating additional revenue streams for manufacturers while de-risking dependence on a single industry vertical.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Alliances Drive Market Leadership in DBR Laser Diodes

The global DBR (Distributed Bragg Reflector) Laser Diode market features a dynamic competitive landscape, characterized by a mix of established players and emerging innovators. Photodigm, the commercial pioneer in DBR laser technology, maintains significant market dominance through its proprietary single growth epi and passive grating technology. The company’s ability to deliver high-performance semiconductor lasers continues to give it an edge in critical applications like 5G infrastructure and data centers.

Innolume and Thorlabs have emerged as key competitors, collectively holding a notable market share in 2024. Their growth is driven by expanding product portfolios that cater to the increasing demand for wavelength-stable laser sources in fiber optic communications. While Innolume specializes in high-power DBR lasers for industrial applications, Thorlabs has strengthened its position through vertical integration and widespread distribution channels.

The market sees continuous expansion activities, with TOPTICA and Sacher Lasertechnik recently introducing tunable DBR laser systems targeting research laboratories. These product launches are expected to capture growth in scientific applications, particularly in spectroscopy and quantum technologies. Meanwhile, Asian players like LD-PD are gaining traction through cost-competitive manufacturing and regional partnerships.

Strategic movements in the sector include Vescent Photonics’ 2023 acquisition of a laser stabilization technology firm, enhancing its DBR product performance. Investment in R&D remains intensive across the board, with companies prioritizing wavelength stability improvements and power efficiency to meet 5G network requirements. The competitive intensity is further heightened by increasing venture capital flowing into photonics startups challenging traditional players.

List of Key DBR Laser Diode Manufacturers Profiled

- Photodigm (U.S.)

- Innolume (Germany)

- Thorlabs (U.S.)

- Vescent Photonics (U.S.)

- Inphenix (U.S.)

- TOPTICA (Germany)

- LD-PD (China)

- InnoLas (Germany)

- Sacher Lasertechnik Groups (Germany)

Segment Analysis:

By Type

Wavelength Tuning Range Below 10GHz Dominates the Market Due to High Demand in Precision Applications

The market is segmented based on type into:

- Wavelength Tuning Range Below 10GHz

- Wavelength Tuning Range 10-25GHz

- Wavelength Tuning Range Above 25GHz

By Application

5G Base Station Segment Leads Due to Critical Role in Telecommunications Infrastructure

The market is segmented based on application into:

- 5G Base Station

- Data Center Internal Network

- Wireless Fiber Optic Repeaters

- Others

By End User

Telecommunication Industry Dominates Market Share with Expanding Network Requirements

The market is segmented based on end user into:

- Telecommunication Industry

- Data Centers

- Research Institutions

- Manufacturing Sector

Regional Analysis: DBR Laser Diode Market

North America

The North American DBR laser diode market is driven by strong demand from the telecommunications and data center industries, particularly in the U.S. where rapid 5G infrastructure deployment and cloud computing expansion create sustained need for high-performance optical components. The region benefits from significant R&D investments in photonics and semiconductor technologies, with key players like Photodigm and Thorlabs maintaining strong regional presence. While regulatory standards for optical devices remain stringent, this has fostered innovation in wavelength stability and power efficiency. The growing adoption of coherent communication systems in metropolitan networks presents new opportunities for DBR laser applications, though competition from alternative technologies presents an ongoing challenge for market players.

Europe

Europe’s DBR laser diode market demonstrates steady growth, supported by advanced manufacturing capabilities in Germany and the UK. The region benefits from strong academic-industry collaboration in photonics research, with several Horizon Europe projects focusing on next-generation optical communication components. Strict EU regulations on electronic waste and energy efficiency drive innovation in laser diode longevity and thermal management. A key growth area lies in medical applications, where DBR lasers are increasingly used in precision diagnostic equipment. However, the market faces pressure from Asian manufacturers in consumer-grade applications, leading European producers to focus on high-value niche segments with stringent quality requirements.

Asia-Pacific

As the largest and fastest-growing regional market, Asia-Pacific dominates DBR laser diode consumption, primarily driven by China’s massive investments in 5G infrastructure and data center construction. Japanese and South Korean manufacturers lead in precision manufacturing of telecom-grade DBR lasers, while Chinese producers are rapidly catching up in both quality and production capacity. The region benefits from complete semiconductor supply chains and government support for photonics industries. India represents an emerging market with growing domestic demand, though local manufacturing capabilities remain limited. While cost competition is intense across Asia, premium applications in industrial sensing and scientific instrumentation continue to support value growth alongside volume expansion.

South America

The South American DBR laser diode market remains in early development stages, with Brazil and Argentina representing the primary demand centers. Limited local manufacturing means most products are imported, primarily from North America and Asia. Growth is constrained by infrastructure limitations and economic instability, though increasing fiber optic network deployments and growing interest in Industry 4.0 applications are creating new opportunities. The medical device sector shows particular promise for high-quality DBR lasers, but adoption faces challenges from budget constraints and lack of technical expertise in optical system integration across many industries.

Middle East & Africa

This region presents a developing market for DBR laser diodes, with growth concentrated in Gulf Cooperation Council countries and South Africa. Telecommunications infrastructure upgrades and smart city initiatives drive demand, particularly for fiber optic communication components. The lack of local semiconductor manufacturing capabilities results in complete reliance on imports, though some assembly operations are emerging in Dubai and Riyadh. While the market remains small relative to other regions, high growth potential exists in oil & gas sensing applications and government-funded research institutions. Market expansion is tempered by limited technical expertise in photonics system integration and preference for lower-cost alternatives in many commercial applications.

Report Scope

This market research report provides a comprehensive analysis of the Global DBR Laser Diode Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue (USD millions) and unit shipments (K Units) across major regions and segments. The market was valued at US$ 892.60 million in 2024 and is projected to reach US$ 2.14 billion by 2032.

- Segmentation Analysis: Detailed breakdown by type (Wavelength Tuning Range Below 10GHz, 10-25GHz, Above 25GHz) and application (5G Base Station, Data Center Internal Network, Wireless Fiber Optic Repeaters, Others) to identify growth opportunities.

- Regional Outlook: Market performance analysis across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market was estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of key players including Photodigm, Innolume, Thorlabs, Vescent Photonics, and Inphenix, covering their market share (approximately % in 2024), product portfolios, and strategic developments.

- Technology Trends & Innovation: Analysis of semiconductor laser performance enhancements, integration with 5G infrastructure, and emerging fabrication techniques.

- Market Drivers & Restraints: Evaluation of factors including 5G deployment, data center expansion, optical communication demands, alongside supply chain challenges and regulatory constraints.

- Stakeholder Analysis: Strategic insights for component manufacturers, telecom operators, system integrators, and investors regarding technological adoption and market expansion.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DBR Laser Diode Market?

-> DBR Laser Diode Market size was valued at US$ 892.60 million in 2024 and is projected to reach US$ 2.14 billion by 2032, at a CAGR of 13.26% during the forecast period 2025–2032.

Which key companies operate in this market?

-> Key players include Photodigm, Innolume, Thorlabs, Vescent Photonics, Inphenix, TOPTICA, and Sacher Lasertechnik, with the top five holding approximately % market share in 2024.

What are the key growth drivers?

-> Primary growth drivers include 5G infrastructure deployment, data center expansion, and increasing demand for high-speed optical communication systems.

Which region dominates the market?

-> North America currently leads the market (USD million in 2024), while Asia-Pacific is expected to witness the highest growth rate through 2032.

What are the emerging technology trends?

-> Emerging trends include integration with 5G networks, development of tunable DBR lasers, and miniaturization of laser diode components for advanced applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...